1

INSURANCE COMPANIES

_______________________

1

Marijana Ćurak- University of Split, Faculty of Economics

Academic year: 2014/2015

10/22/2014

International Week – New Frontiers in Finance and Accounting 2014

University of Economics in Katowice

Course: Financial Institutions

These lecture slides are based on the

book:

Mishkin F. S., Eakins, S. G. (2012), Financial

Markets + Institutions, Addison Wesley

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

2

AGENDA

Introduction

Basic insurance principles

Adverse selection and moral hazard problems in insurance

Types of insurance organizations

Types of insurance (life and non-life insurance)

Insurance management

Review points

Marijana Ćurak- University of Split, Faculty of Economics

3

10/22/2014

2

INTRODUCTION (1)

Insurance companies are in the business of

assuming risk on behalf of their customers in

exchange for a fee, called premium

Insurance companies make a profit by charging

premiums that are sufficient to pay the expected

claims to the company plus a profit

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

4

INTRODUCTION (2)

Why do people pay insurance when they know

that over the lifetime of their policy, they will

probably pay more in premiums than the

expected amount of any loss they will suffer?

Most people are risk-averse – they would rather

pay a certainty equivalent (the insurance

premiums) than accept the gamble that they will

lose their house or their car

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

5

PEOPLES’ LIFE WITHOUT OF INSURANCE

Everyone would have to set aside reserves

These reserves could not be invested long-term but

would have to be kept in an extremely liquid form

People would be constantly worried that their reserves

would be inadequate to pay for catastrophic events

Insurance allows us the peace of mind that a single

event can have only a limited financial impact on our

lives

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

6

3

BASIC INSURANCE PRINCIPLES (1)

There must be a relationship between insured

(the party covered by insurance) and the

beneficiary (the party who receives the payment

in case a loss occurs)

The beneficiary must be someone who may

suffer potential harm

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

7

BASIC INSURANCE PRINCIPLES (2)

The insured must provide full and accurate

information to the insurance company

The insured is not to profit as a result of

insurance coverage

If a third party compensates the insured for the

loss, the insurance company’s obligation is

reduced by the amount of the compensation

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

8

BASIC INSURANCE PRINCIPLES (3)

The insurance company must have a large

number of insureds so that the risk can be

spread out among many different policies

The loss must be quantifiable

The insurance company must be able to

compute the probability of the loss occurring

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

9

4

BASIC INSURANCE PRINCIPLES (4)

The purpose of these principles is to maintain the

integrity of the insurance process

Without them, people may be tempted to use insurance

companies to gamble or speculate on future events

The principles provide a way to spread the risk among

many policies and to establish a price for each policy

that will provide an expectation of a profitable return

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

10

ADVERSE SELECTION AND MORAL HAZARD

IN INSURANCE (1)

Despite following these guidelines, insurance

companies suffer greatly from the problems of

asymmetric information

Adverse selection in insurance occurs when the

individuals most likely to benefit from a

insurance are the ones who most actively seek

out the insurance and are thus most likely to be

selected

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

11

ADVERSE SELECTION AND MORAL HAZARD

IN INSURANCE (2)

The implication of adverse selection is that loss

probability statistics gathered for the entire

population may not accurately reflect the loss

potential for the persons who actually want to buy

policies

The adverse selection problem raises the issue of

which policies an insurance company should accept

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

12

5

ADVERSE SELECTION AND MORAL HAZARD

IN INSURANCE (3)

For health and life insurance – insurance

companies require physical exams and may

examine previous medical records before issuing

policy

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

13

ADVERSE SELECTION AND MORAL HAZARD

IN INSURANCE (4)

Moral hazard occurs when the insured fails to take

proper precautions to avoid losses because losses are

covered by insurance

It occurs when the existence of insurance encourages

the insured party to take risks that increase the

likelihood of an insurance payoff

One way that insurance companies combat moral hazard

is by requiring a deductible

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

14

ADVERSE SELECTION AND MORAL HAZARD

IN INSURANCE (5)

The deductible is the amount of any loss that must

be paid by the insured before the insurance

company will pay anything

Contract terms aimed at reducing risk (prevention

activities)

Moral hazard activities could be taken by the

parsons and companies providing services related to

insurance

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

15

6

SELLING INSURANCE (1)

Insurance companies hire large sales

forces to sell their products

The expense of marketing may account

for up to 20% of the total cost of a policy

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

16

SELLING INSURANCE (2)

Insurance distribution channels:

Agents (independent and exclusive)

Brokers

Direct sale

The intermediaries are compensated by

being paid a commission

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

17

SELLING INSURANCE (3)

Importance of underwriters – people who

review and sign off on each policy an

agent writes and who have the authority

to turn down a policy if they deem the risk

unacceptable

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

18

7

TYPES OF INSURANCE ORGANIZATIONS (1)

Stock company

Owned by stockholders and has the objective

of making a profit

Mutual insurance company

Owned by the policyholders

The objective is to provide insurance at the

lowest possible cost to the insured

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

19

TYPES OF INSURANCE ORGANIZATIONS (2)

Policyholder are paid dividends that reflect the

surplus of premiums over costs

Because the policyholders share in reducing

the cost of insurance, there may be some

reduction in the moral hazard that most

insurance companies face

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

20

TYPES OF INSURANCE

Life insurance

Non-life insurance (property-casualty)

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

21

8

LIFE INSURANCE (1)

In its simplest form, life insurance provides income for

the children of the deceased

The cost of life insurance depends on such factors as the

age of the insured, average life expectancies, the health

and lifestyle of the insured and insurance company’s

operating costs

Long-term contracts

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

22

LIFE INSURANCE (2)

Besides financial protection of dying too young,

life insurance provides protection of living too

long

Life insurance company can predict with a high

degree of accuracy when death benefits must be

paid by using actuarial tables that predict life

expectancies

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

23

LIFE INSURANCE (3)

Law of large numbers says that when many people are

insured, the probability distribution of the losses will

assume a normal probability distribution, a distribution

that allows accurate predictions

Because insurance companies insure so many people,

the law of large numbers tends to make the company's

predictions quite accurate and allows companies to price

the policies so that they can earn a profit

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

24

9

TYPES OF LIFE INSURANCE

Term life

Whole life

Universal life

Annuities

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

25

TERM LIFE

It pays out if the insured dies while the

policy is in force

This form of policy contains no saving

element

Once the policy period expires, there are

no residual benefits

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

26

WHOLE LIFE

Policy pays a death benefit when the policyholder dies

It usually requires the insured to pay a level premium for

the duration of the policy

In the beginning, the insured pays more than if a term

policy has been purchased

This overpayment accumulates as a cash value that can

be borrowed by the insured at reasonable rates

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

27

10

UNIVERSAL LIFE

The policies that combine the benefits of

the term policy with those of the whole

life policy

The policy is structured to have two parts,

one for the term life insurance and one for

saving

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

28

ANNUITY

Insurance product that helps people if

they live longer that they expect

For an initial a fixed sum or stream of

payments, the insurance company agrees

to pay beneficiary a fixed amount for as

long as he/she lives

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

29

ASSETS OF LIFE INSURANCE COMPANIES

Since life insurance liabilities are

predictable and long-term, life insurance

companies can invest in long-term assets

(bonds, mortgages and real estate)

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

30

11

NON-LIFE INSURANCE (1)

Property insurance protects property (houses,

cars, boats, and so on) against losses due to

accidents, fire, disasters

Liability insurance protects against liability for

harm the insured may cause to others as a

result of product failure or accidents

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

31

NON-LIFE INSURANCE (2)

The premiums are based simply on the

probability of the loss

The amount of the potential loss is much

more difficult to predict than for life

insurance

Short-term contracts

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

32

NON-LIFE INSURANCE (3)

Property insurance can be provided in

either:

Named-peril policies

Insure against loss only from perils that are

specifically named in the policy

Open-peril policies

Insure against all perils except those specifically

excluded by the policy

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

33

12

REINSURANCE

Reinsurance allocates a portion of the risk

to another company in exchange for a

portion of the premium

It reduces risk exposure for the insurers

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

34

INSURANCE MANAGEMENT

Both adverse selection and moral hazard can

result in large losses to insurance companies

because they lead to higher payouts on

insurance claims

Minimizing adverse selection and moral hazard

to reduce these payouts is therefore and

extremely important goal for insurance

companies

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

35

SCREENING

To reduce adverse selection, insurance

companies try to screen out poor

insurance risks from good ones

Effective information collection procedures

are therefore an important principle of

insurance management

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

36

13

RISK-BASED PREMIUM

Charging insurance premiums on the basis

of how much risk a policyholder poses for

the insurance company is important

principles in order to reduce adverse

selection

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

37

RESTRICTIVE PROVISIONS

They are insurance management tool for

reducing moral hazard

Such provisions discourage policyholders

from engaging in risky activities that make

an insurance claim more likely

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

38

PREVENTION OF FRAUDS

Insurance companies also face moral

hazard because an insured person has an

incentive to lie to the company and seek a

claim even if the claim is not valid

Management tool – conducting

investigations to prevent fraud

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

39

14

CANCELLATION OF INSURANCE

Management tool – be prepared to cancel

policies

Insurance companies can discourage

moral hazard by threatening to cancel a

policy when the insured person engages in

activities that make a claim more likely

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

40

DEDUCTIBLES

The fixed amount by which the insured’s

loss is reduced when a claim is paid off

They are additional management tool that

helps insurance companies reduce moral

hazard

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

41

LIMITS ON THE AMOUNT OF INSURANCE

There should be limits on the amount of

insurance provided, even though a customer is

willing to pay for more coverage

The higher the insurance coverage, the more

the insured person can gain from risky activities

that make an insurance payoff more likely and

hence the greater the moral hazard

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

42

15

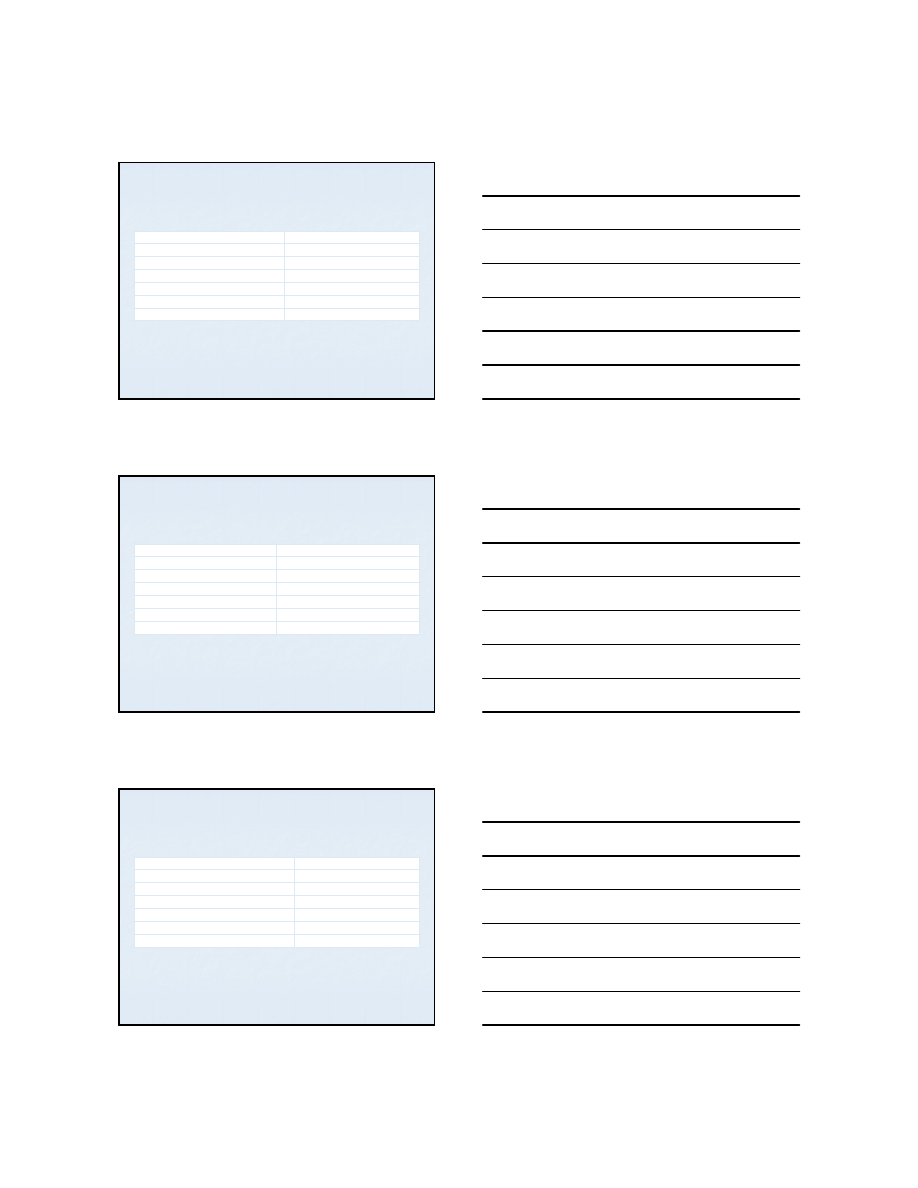

LIFE INSURANCE DESITY (in US$)

Region/Country

Premiums per capita

World advanced markets

2,073.8

Emerging markets

66.9

Western Europe

1,738.2

CEE

64.5

Switzerland (Ranking 1 by total density)

4,211

Poland (Ranking 42 by total density)

217

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

43

Source: Swiss Re, sigma, No. 3, 2014

NON-LIFE INSURANCE DESITY (in US$)

Region/Country

Premiums per capita

World advanced markets

1547

Emerging markets

62.3

Western Europe

1,142.7

CEE

170.2

Swits(Ranking 1 by total density)

4,211

Poland (Ranking 42 by total density)

217

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

44

Source: Swiss Re, sigma, No. 3, 2014

LIFE INSURANCE PENETRATION (% OF GDP)

Region/Country

Premiums/GDP

World advanced markets

4.73

Emerging markets

4.41

Western Europe

4.75

CEE

0.54

Taiwan (Ranking 1 by total penetration)

14.5

Poland (Ranking 42 by total penetration)

1.6

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

45

Source: Swiss Re, sigma, No. 3, 2014

16

NON-LIFE INSURANCE PENETRATION (% OF GDP)

Region/Country

Premiums/GDP

World advanced markets

3.53

Emerging markets

1.31

Western Europe

3.12

CEE

1.41

Taiwan (Ranking 1 by total penetration)

3.1

Poland (Ranking 42 by total penetration)

1.8

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

46

Source: Swiss Re, sigma, No. 3, 2014

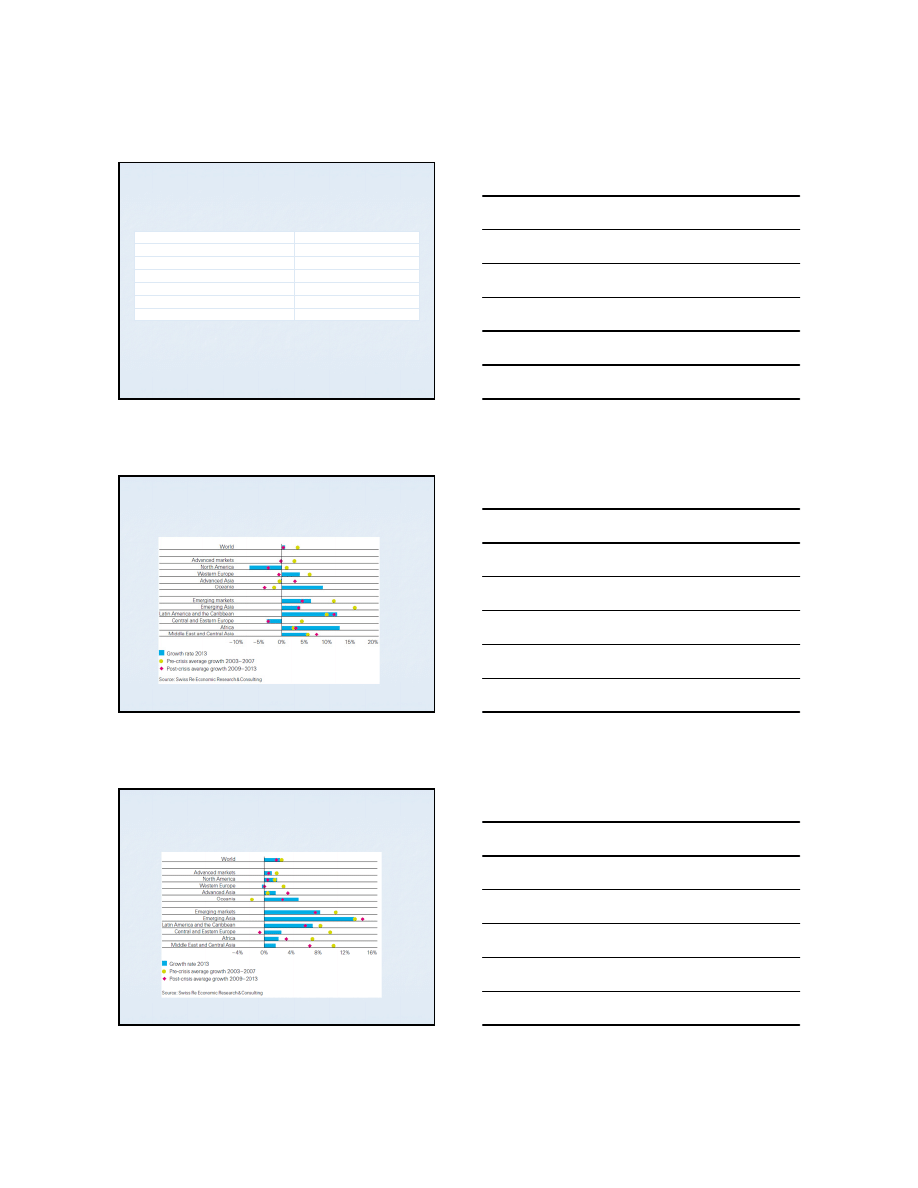

GROWTH RATE OF LIFE INUSRANCE

PREMIUMS

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

47

Source: Swiss Re, sigma, No. 3, 2014, p. 8

GROWTH RATE OF NON-LIFE INUSRANCE

PREMIUMS

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

48

Source: Swiss Re, sigma, No. 3, 2014, p. 11

17

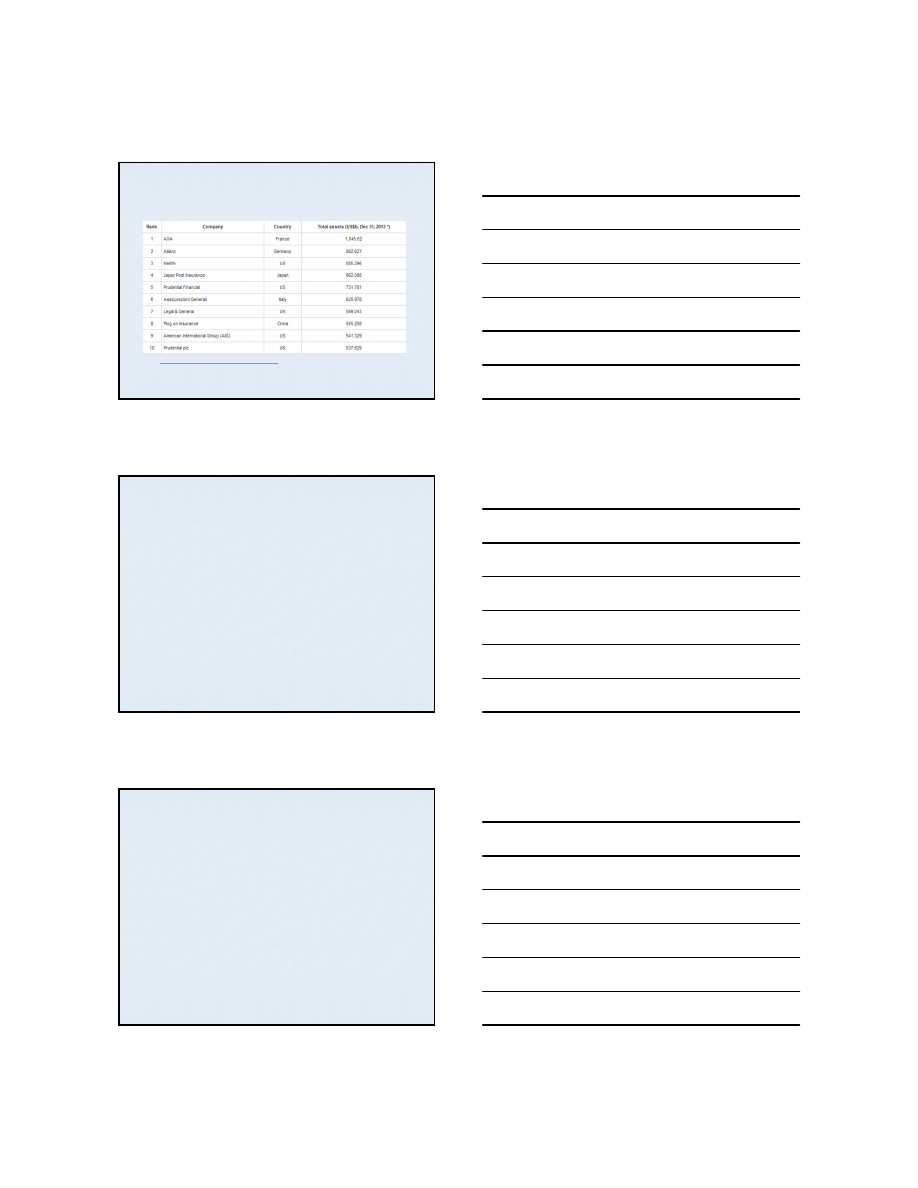

TOP INSURANCE COMPANIES

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

49

Source:

http://www.relbanks.com/top-insurance-companies/world

(Accssed: October 18, 2014)

REVIEW POINTS (1)

Insurance companies underwrite risks and

invest premiums

Life and non-life insurance

Insurance companies face the problems of

adverse selection and moral hazard

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

50

REVIEW POINTS (2)

Insurance companies reduce the problems

of asymmetric information using various

management tools

10/22/2014

Marijana Ćurak- University of Split, Faculty of Economics

51

18

REFERENCES

Mishkin F. S., Eakins, S. G. (2012), Financial

Markets + Institutions, Addison Wesley

Marijana Ćurak- University of Split, Faculty of Economics

52

10/22/2014

Wyszukiwarka

Podobne podstrony:

global companies id 192082 Nieznany

Abolicja podatkowa id 50334 Nieznany (2)

4 LIDER MENEDZER id 37733 Nieznany (2)

katechezy MB id 233498 Nieznany

metro sciaga id 296943 Nieznany

perf id 354744 Nieznany

interbase id 92028 Nieznany

Mbaku id 289860 Nieznany

Probiotyki antybiotyki id 66316 Nieznany

miedziowanie cz 2 id 113259 Nieznany

LTC1729 id 273494 Nieznany

D11B7AOver0400 id 130434 Nieznany

analiza ryzyka bio id 61320 Nieznany

pedagogika ogolna id 353595 Nieznany

Misc3 id 302777 Nieznany

cw med 5 id 122239 Nieznany

D20031152Lj id 130579 Nieznany

więcej podobnych podstron