Managerial

Managerial

Economics

Economics

Jarek Neneman

601305093

Auctions and competitive bidding

(ch. 17, Samuelson & Marks)

Auctions

Everything is worth what

it’s purchaser will pay for it

Auctions

A exercise to start with – bidding for a

jar of money.

Take the look at the jar

Write down:

- estimated value of the jar (i. e. money)

- sealed bid for the jar

The person with the highest bid will win and

pay and be given an equivalent of the money

in the jar

Auctions

Auctions and competitive bidding

Auctions were used by the ancient

Babylonians as a way of distributing wives.

The two most frequently used methods of

selecting a best alternative:

- sealed-bid auction

- English auction,

let’s play it!

- Third kind of auction method is Dutch

auction

Auctions

The advantages of auctions

Auctions are between:

- posted prices, and

- negotiations

Auctions ensure that competition among

buyers sets the highest price.

Auctions are less time-consuming than

negotiations.

Let’s see the example

Auctions

The advantages of auctions – a stock

repurchase

A stock repurchase.

A company is considering buying-back some

of its stocks.

The current price is: $67 per share

Management believes the value of the stock

is: $80 per share

Management’s offer would be: $70, $72 or

$74

The response of shareholders is not known

Auctions

The advantages of auctions – a stock

repurchase

Shareholders response (Q)

Price

strong medium weak

$

(π=1/3) (π=1/3) (π=1/3)

70

13

9

6

72

14

12

8

74

18

15

12

Company’s profit is:

($80-P)*Q

Auctions

The advantages of auctions – a stock

repurchase

What buy back price should the firm set?

Shareholders response (Q)

Price

strong

medium

weak

$

(π=1/3)

(

π=1/3)

(π=1/3)

70

13

9

6

72

14

12

8

74

18

15

12

E(Π

$70

) = 1/3*10*13 + 1/3*10*9 + 1/3*10*6 =

93.3

E(Π

$72

) = 1/3*8*14 + 1/3*8*12 + 1/3*8*8 =

90.67

E(Π

$74

) = 1/3*6*13 + 1/3*6*9 + 1/3*6*6 = 90

Auctions

The advantages of auctions – a stock

repurchase

Instead of setting the buy-back price, the firm

can organize an auction.

In this system, each shareholder tenders any

number of shares at a price he names. eg. „I

will sell 10 at $70 or 20 at $72”.

After collecting of the tenders, the firm buys

the shares at a single common price.

What is the advantage of this „auction?

Before deciding on price, the firm knows the

shareholders’ response.

Auctions

The advantages of auctions – a stock

repurchase

The firm’s most profitable offer (price) is

contingent on demand.

Shareholders response (Q)

Price

strong

medium

weak

$

(π=1/3)

(

π=1/3)

(π=1/3)

70

13

9

6

72

14

12

8

74

18

15

12

Strong response: price: $70, profit: $130

Medium response: price: $72, profit: $96

Weak response: price: $74, profit: $72

Auctions

The advantages of auctions – a stock

repurchase

Strong demand: price: $70, profit: $130

Medium demand: price: $72, profit: $96

Weak demand: price: $74, profit: $72

E(Π)= 1/3*130 + 1/3*96 + 1/3*72 = $99.3

Auction compared to posted prices increased

expected profit by $6.

$6 is the expected value of perfect

information about response

Auctions

The advantages of auctions – bidding vs.

bargaining

Searching for best price revisited

Seller believes that the potential buyers’

offers to purchase the division are uniformly

distributed in the range form $40-64m

The average is $52m

Seller’s reservation price is: $40m

What will be the average price in negotiation

with single buyer?

$46m. on average is very likely (profit from

transaction is split fifty-fifty).

Auctions

The advantages of auctions – bidding vs.

bargaining

Searching for best price revisited

The firm may do better by selling with use of

sealed-bid auction.

With 6 buyers, the price offered by the

highest bidder will be $60m. on average.

The sources of higher price are twofold:

- the higher the number of bidders, the

higher the probability that the one will hold a

high value

- the higher the number of bidders, the

stronger the incentive for them to place bid

near to its true value.

Auctions

Bidder strategies

Optimal bid depends on:

- reservation price

- assessment of the extent of bidding

competition

- type of auction (the most important factor)

Auctions

Bidder strategies

Time for another auction

Vickery auction (second-price (second-

bid) auction)

The highest bid wins the item.

But the price is equal to the second-highest

bid

Auctions

Bidder strategies

Independent private value setting

Each bidder assesses an individual value

(reservation price) for the item up for bid.

Each bidder’s value is independent of the

other’s

Values are private and bidders are aware of

the common probability distribution.

The profit of the bidder is:

v

i

- P

Auctions

Bidder strategies – English and Dutch

auctions

English and Dutch auctions

In oral English auctions bids continually

increase until the last and highest bidder

wins.

Bidder’s strategy: bid up to the reservation

price if necessary – dominant strategy

P is close to the second-highest reservation

price: v

2nd

.

The seller can obtain exactly the same price

using Vickery auction (second-price (-

bid) auction)

P

2nd

= P

E

= v

2nd

Auctions

Bidder strategies – English and Dutch

auctions

In Dutch auction the auctioneer starts the

sale by calling out a high price and the

lowers the price until a bid is made.

Optimal strategy in Dutch auction is

significantly different than in English auction

In Dutch auction there is risk, that another

buyer bid and win the item

In English auction there is no risk

Dutch auctions are similar to sealed-bid

auctions – the price achieved by seller is the

same

Auctions

Bidder strategies – sealed-bid auctions

Sealed-bid auctions are used to sell unique

items

Each bidder faces trade-off between

probability and profitability of winning

What bid will maximize the bidder’s expected

profit?

Auctions

Bidder strategies – sealed-bid auctions

Strategy against a bid distribution

To win the auction the firm must beat the

best competiting bid.

The distribution of competing bid is a key to

success.

An example

Auctions

Bidder strategies – sealed-bid auctions –

an example

v

1

= $342 thousand

E(Π) = (342 – b)*[probability (b wins)]

There are two more bidders

Assessment winning chances and expected

profit are given in the table

Auctions

Bidder strategies – sealed-bid auctions –

an example

Bid

Winning Probability

Expected

$

profit

of winning

profit

300

42

0.00

0.00

310

32

0.06

1.92

320

22

0.25

5.50

326

16

0.42

6.67

328

14

0.49

6.86

332

10

0.64

6.40

336

6

0.81

4.86

340

2

1.00

2.00

Optimal bid is:

$328

Auctions

Bidder strategies – sealed-bid auctions –

an example

Firm’s winning chance depends on probability

that the best competing bid (BCB) is

smaller than the firm’s own bid.

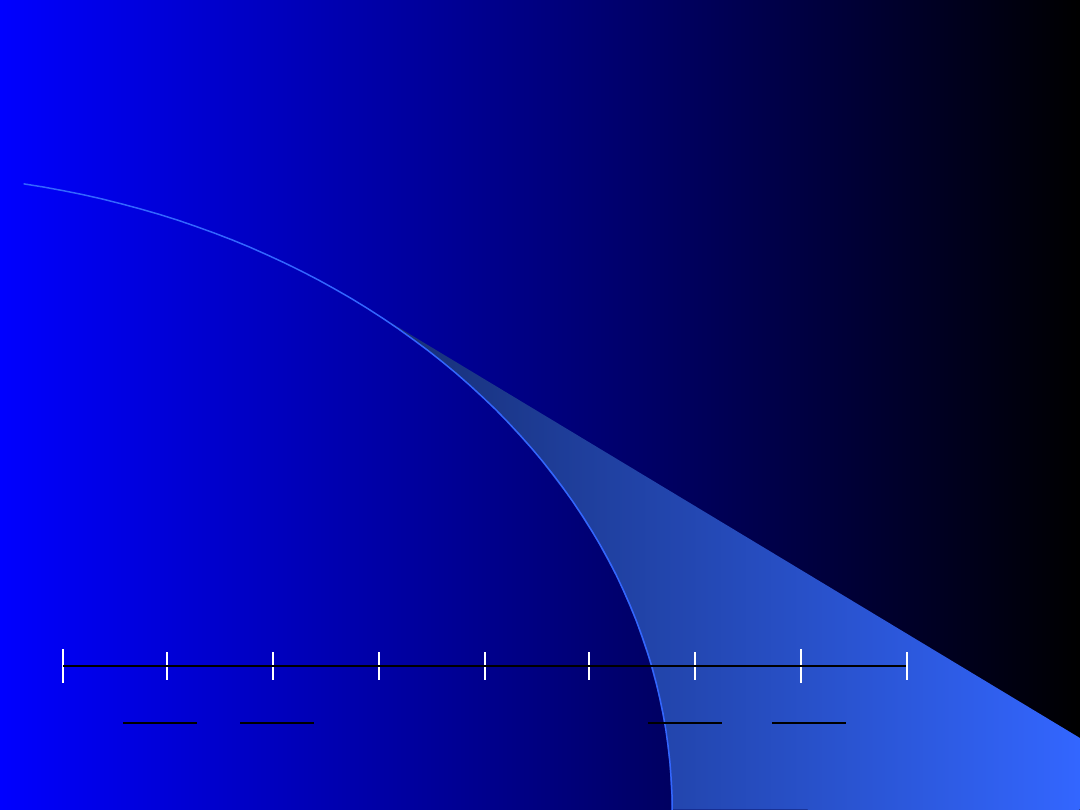

H curve is graphical presentation of BCB

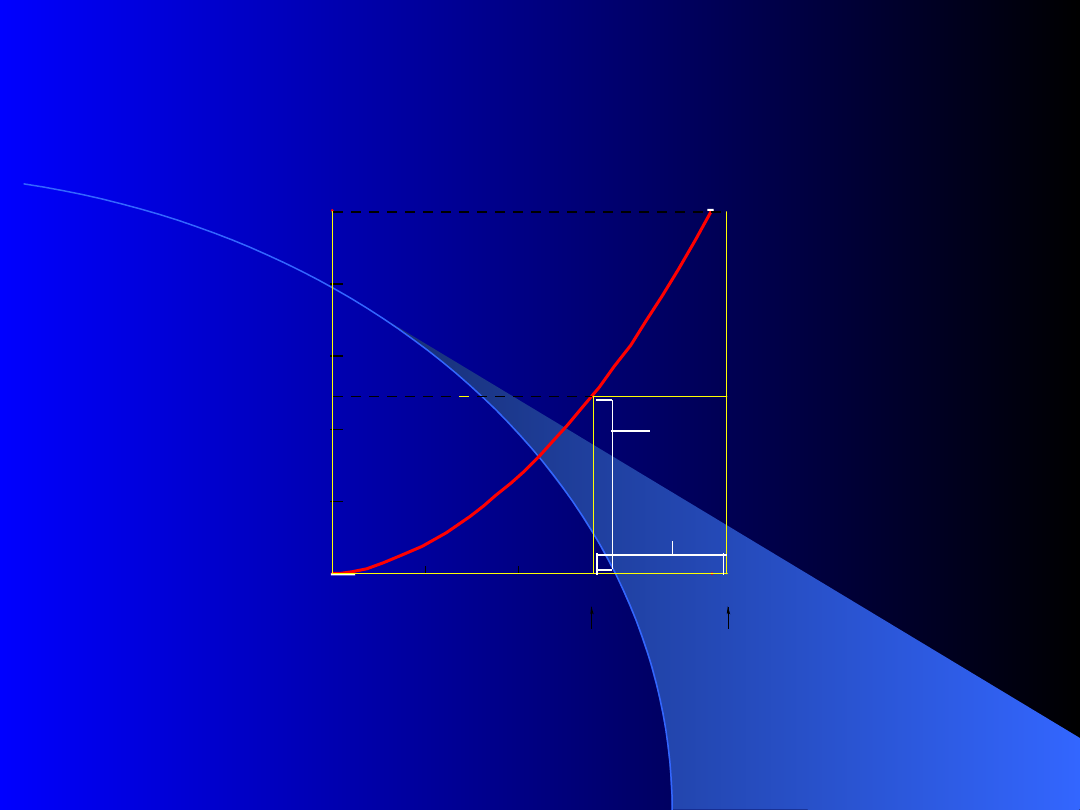

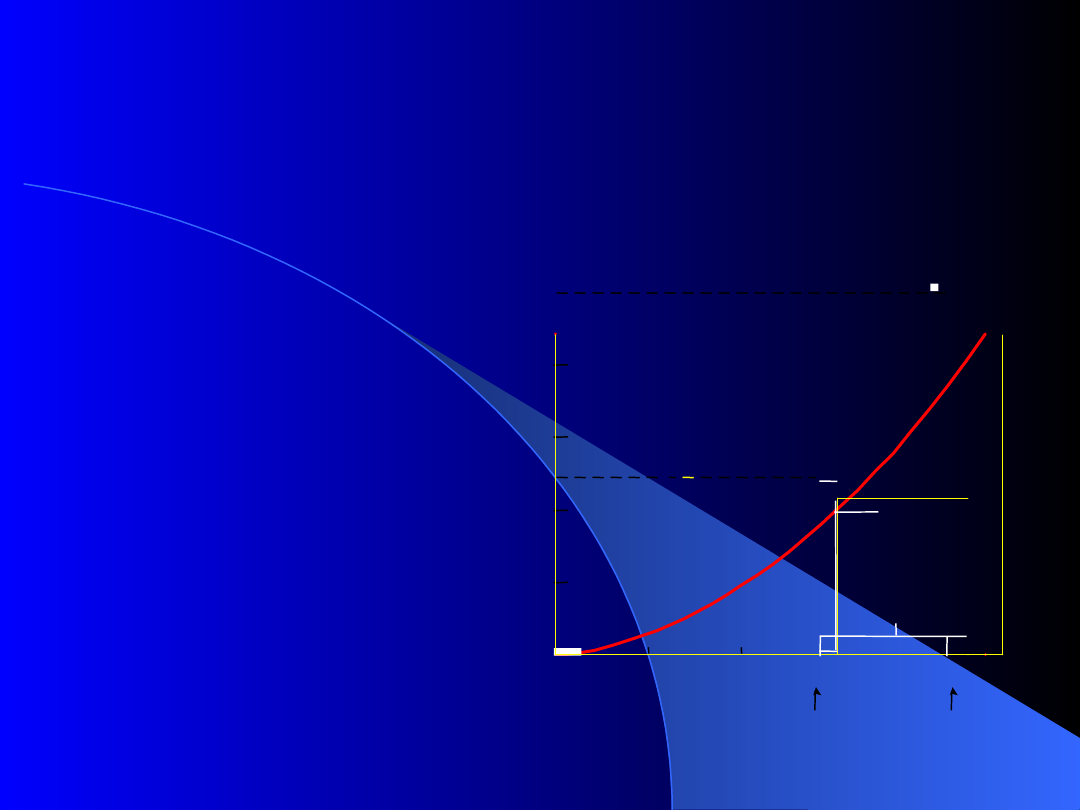

Auctions

Bidder strategies – sealed-bid auctions –

an example

1.0

.8

.6

.49

.4

.2

0

Probability

H curve

Probability

b = 328 wins

Firm 1's profit

v - b

310

300

320 328

342

Firm 1's

optimal bid

Firm 1’s

Reservation

price

At bid = $328, the area of the rectangle (342-b)H(b) is the

biggest.

Auctions

Bidder strategies – sealed-bid auctions –

an example

1.0

.8

.6

.49

.4

.2

0

Probability

H curve

Probability

b = 328 wins

Firm 1's profit

v - b

310

300

320 328

342

Firm 1's

optimal bid

Firm 1’s

Reservation

price

H curve is graphical

presentation of

BCB

It precisely measures

the firm’s winning

chances for its

various bids

Median of the BCB is

slightly higher

than $328.

Auctions

Bidder strategies – sealed-bid auctions –

an example

Arriving at BCB

Let G(b) denote the cumulative distribution

function for the bid of a single competitor.

If firm’s bid is b, then the chances that this

bid is higher than the bid of the single

competitor is G(b)

What if there are two competitors?

If bids are independent of one another, then

probability, that firm’s bid is better than both

competiting bids is:

[G(b)]

2

Auctions

Bidder strategies – sealed-bid auctions –

an example

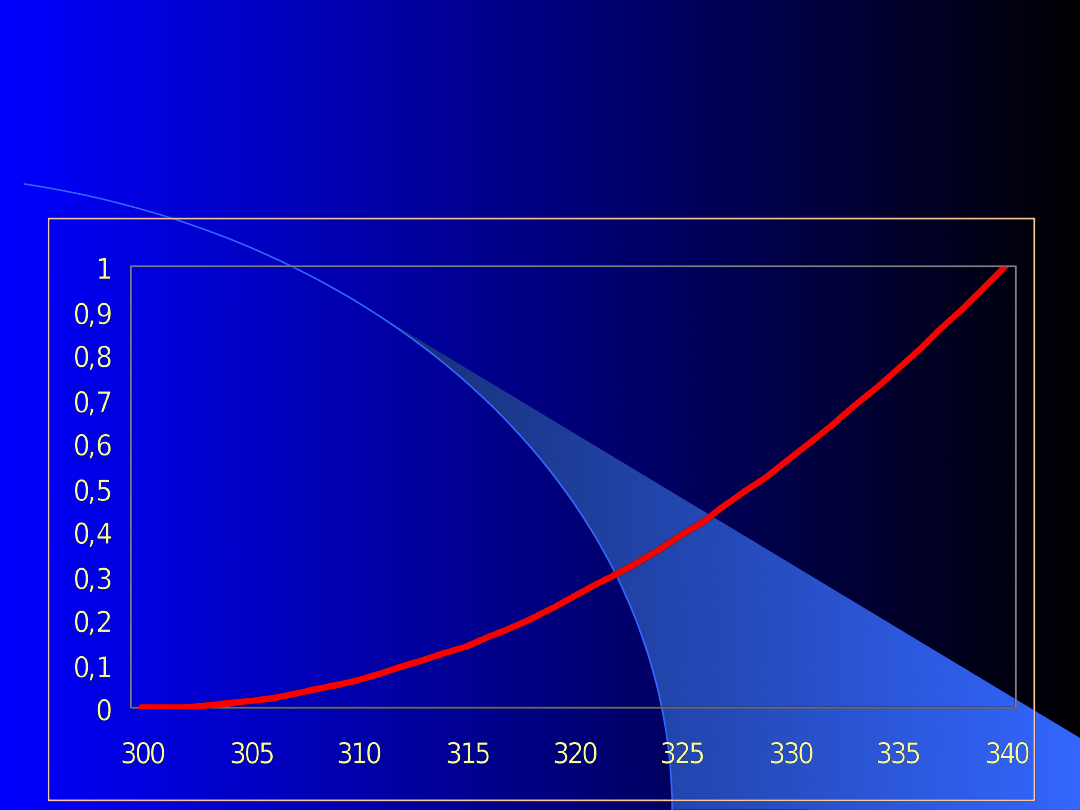

Generally:

H(b) = [G(b)]

n-1

for n-1 competitors firm is facing

An example continued

Firm’s assessment is that each competitor’s

bid will be in the range of $300 and $340,

with all values in between equally likely. This

implies:

G(B) = (b-300)/40

With two competitors: H(b) = [(b-300)/40]

2

Auctions

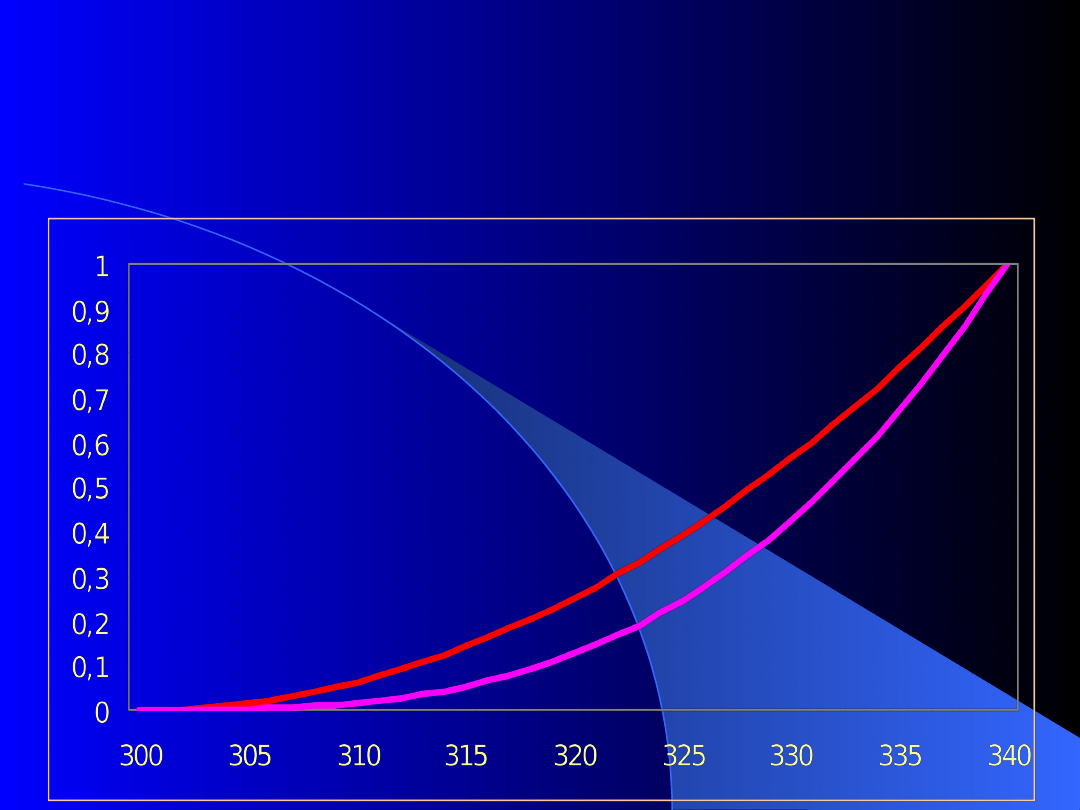

Bidder strategies – sealed-bid auctions –

an example

N-1=

2

Auctions

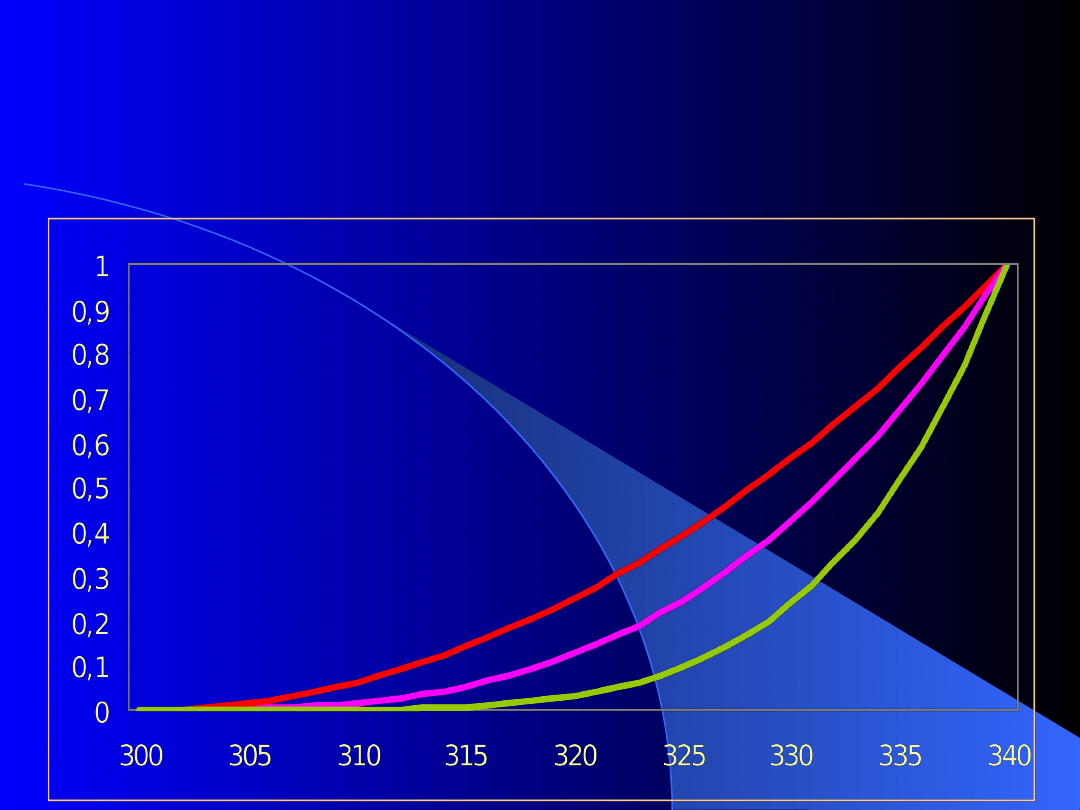

Bidder strategies – sealed-bid auctions –

an example

N-1=

2

, n-1=

3

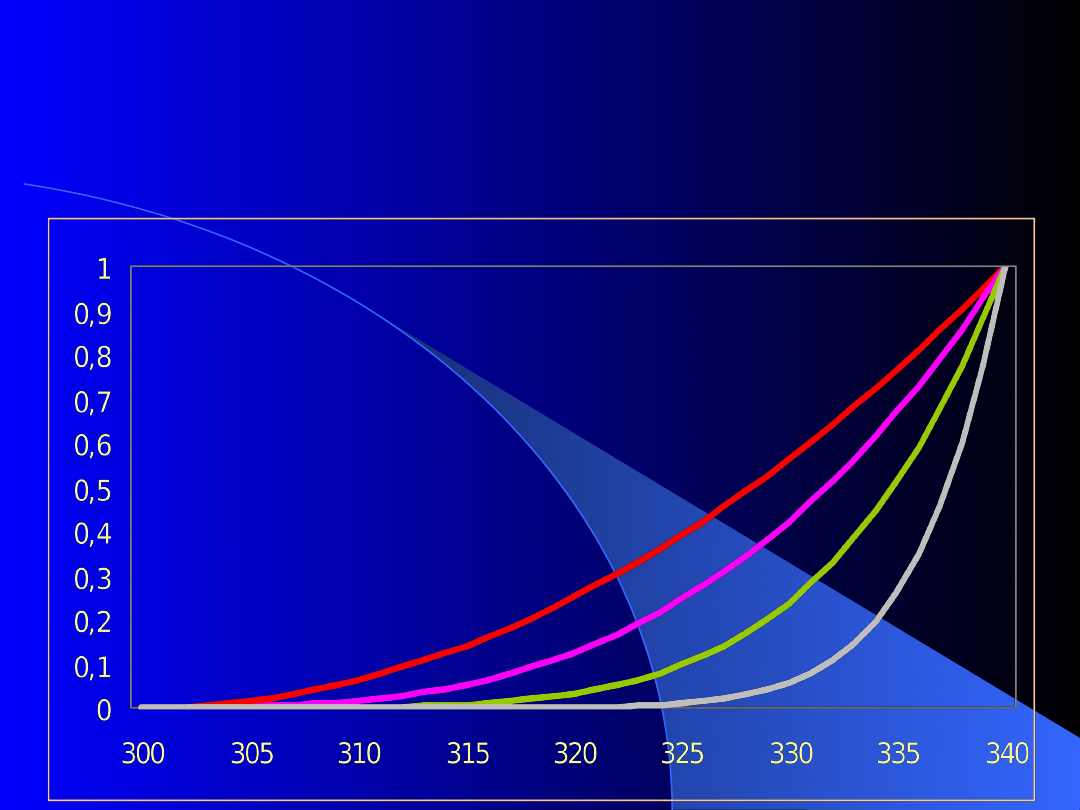

Auctions

Bidder strategies – sealed-bid auctions –

an example

N-1=

2

, n-1=

3

, n-1=

5

Auctions

Bidder strategies – sealed-bid auctions –

an example

N-1=

2

, n-1=

3

, n-1=

5

, n-1=

10

Auctions

Bidder strategies – sealed-bid auctions –

an example

With increasing number of competitors, the

bid distribution of the typical firm, G(b), will

be shifted towards higher bids.

This happens because:

- there are more competitors (that could be

seen on the previous graphs)

- each of them raise its bid

Auctions

Bidder strategies – sealed-bid auctions –

interdependence

Equilibrium bidding strategies

Usually it is difficult for a firm to assess G(b)

or H(b)

All competitors are setting competitive bid,

taking into account others’ strategies, i.e.

there is interdependence among bidding

strategies

Auctions

Bidder strategies – sealed-bid auctions –

interdependence

Bidding for the good with common value.

All bidders have the same reservation price.

The unique equilibrium has each bidder

submitting a sealed bid exactly equal to this

common value (reservation price).

Analogy for Bertrand competition

Auctions

Bidder strategies – sealed-bid auctions –

interdependence

Bidding for the good with different private

values

n bidders,

v

i

private value

b

i

sealed bid

Buyers’ values are drawn independently from

a common distribution

Buyers values are independent

Each buyer’s value is uniformly distributed

between $300 and $360

Auctions

Bidder strategies – sealed-bid auctions –

interdependence

If bidder knows his v

i

but do not know the

reservation prices of the other competitors,

then

his equilibrium bidding strategy is:

b

i

= 0.5 * 300 + 0.5v

i

For v

i

= 300, b

i

=300

For v

i

= 360, b

i

= 330

Expected profit of the first firm is:

E(Π

1

) = (v

1

– b

1

)[probability(b

1

wins)]

Auctions

Bidder strategies – sealed-bid auctions –

interdependence

If firm 2 uses equilibrium bidding strategy,

then its competiting bids are distributed

uniformly between $300 and $330,

Thus b

1

wins with probability:

(b

1

– 300)/30, plugging this into expected

profit function gives:

E(Π

1

) = (v

1

– b

1

)*[(b

1

– 300)/30]

Setting dE(Π

1

)/db

1

= (v

1

– 2b

1

+300)/30 to

zero, implies:

b

1

= 0.5 * 300 + 0.5v

1

Auctions

Bidder strategies – sealed-bid auctions –

interdependence

For n competiting firms, the common

equilibrium strategy is:

b

i

= (1/n)*L + [(n-1)/n]* v

i

In sealed-bid auction, the equilibrium

strategy is to submit a bid b

i

, equal to the

expected value of the highest of the n-1

other buyers values, conditional on these

values being lower than v

i

.

b

i

= E(v’|v’≤v

i

)

Auctions

Bidder strategies – common values and the

Winner’s curse

Auctions for common but unknown value

Bids (B)

Estimates (E)

B

V

Bid distribution is centered to the left, as

bidders are seeking profits and bid below

the estimate of value

Auctions

Bidder strategies – common values and the

Winner’s curse

Winner’s curse – after the auction (ex post)

winner finds that the good is worth less than

the price paid for it.

Overestimation of the value is the source of

winner’s curse

Winning conveys information about the

bidder’s estimate relative to others.

Winner’s curse depends on:

degree of uncertainty

number of bidders

Auctions

Bidder strategies – common values and the

Winner’s curse

There is a significant difference between

sealed-bid auction and English auction of an

common, but unknown value item.

Observing the number of active bidders and

when they drop out conveys information

about competitor’s estimates of the item’s

value.

Auctions

Optimal auctions – expected auction

revenue

Optimal auctions from the seller’s perspective

Expected auction revenue

In private value model and risk-neutral buyer,

English, sealed-bid, Dutch and Vickrey

auctions generate identical expected

revenues – revenue equivalence theorem

Auctions

Optimal auctions – expected auction

revenue

Optimal auctions from the seller’s perspective

Seller’s expected revenue in the English and

Vickrey auctions:

E(P

E

) = E(v

2nd

)

Seller’s expected revenue in the Dutch and

sealed-bid auctions:

b

i

= E(v’|v’ ≤ v

i

)

Auctions

Optimal auctions – expected auction

revenue

A uniform example

Assume n buyers with reservation prices

independently and uniformly distributed

between L and U.

E(v

max

) = [1/(n+1)]L + [n/(n+1)]U

E(v

2nd

) = [2/(n+1)]L + [(n-1)/(n+1)]U

L

U

E (v

m ax

)

E (v

2nd

)

1

n+ 1

2

n+ 1

n - 1

n + 1

n

n + 1

Auctions

Optimal auctions – expected auction

revenue

V

max

is n/(n+1) toward U, and

He applies the factor in shading his bid below

his value: (n-1)/n

b

i

= (1/n)*L + [(n-1)/n]* vi

Multiplying: n/(n+1) by (n-1)/n gives:

(n-1)/(n+1) toward U – exactly as in English

auction

L

U

E (v

m ax

)

E (v

2nd

)

1

n+ 1

2

n+ 1

n - 1

n + 1

n

n + 1

Auctions

Optimal auctions – expected auction

revenue

Common-value setting

English auction produces greater revenue, on

average, than the sealed bid auction

Why?

Intuitively:

In common-value settings, buyers must

discount their bids to avoid the winner’s

curse.

The greater the uncertainty (and the number

of bidders) the greater the bid discount.

Auctions

Optimal auctions – expected auction

revenue

Common-value setting

English auction conveys more information

about others bidder’s estimates of value.

Thus English auction informational advantage

translates into revenue advantage for the

seller.

In auction experiments, however, bidder fall

pray to the winner’s curse and sealed-bid

auction holds a slight revenue advantage to

English auction, especially when the item’s

value is highly uncertain and when

competition is high.

Auctions

Optimal auctions – expected auction

revenue

Bidder risk aversion

No effect on bidding in English auction

(bidding up to full value is still dominant

strategy

In sealed-bid auctions this implies higher bids

– smaller but more certain profit.

If a bidder’s value for an item is uncertain,

risk aversion implies reduction in certainty

equivalent value, which in turn lowers bids.

Auctions

Optimal auctions – expected auction

revenue

Value asymmetry

Buyers values are draw from different

distributions

Sealed-bid auction gives higher expected

revenue than English auction

Auctions

Optimal auctions – summary

Experiments confirm the following:

For common-value auctions:

For risk-neutral bidder, the rank order is:

English

> second highest sealed bid > Dutch =

highest price sealed bid

The seller does better with English auctions, whether

risk neutral or not.

Auctions

Optimal auctions – expected auction

revenue

Experiments confirm the following:

For private-value auctions:

For

risk neutral bidders

, English, Dutch, highest

sealed bid, or second highest bid auctions are all

alike in their outcome.

When bidders are

risk-averse,

the rank order from

highest is:

Dutch = highest price sealed bid

> English = second

highest sealed bid

Auctions

Additional readings

http://www.auctusdev.com/auctiontypes.html

Document Outline

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

- Slide 17

- Slide 18

- Slide 19

- Slide 20

- Slide 21

- Slide 22

- Slide 23

- Slide 24

- Slide 25

- Slide 26

- Slide 27

- Slide 28

- Slide 29

- Slide 30

- Slide 31

- Slide 32

- Slide 33

- Slide 34

- Slide 35

- Slide 36

- Slide 37

- Slide 38

- Slide 39

- Slide 40

- Slide 41

- Slide 42

- Slide 43

- Slide 44

- Slide 45

- Slide 46

- Slide 47

- Slide 48

- Slide 49

- Slide 50

- Slide 51

- Slide 52

Wyszukiwarka

Podobne podstrony:

ME Optimal search ppt

03 Sejsmika04 plytkieid 4624 ppt

Choroby układu nerwowego ppt

10 Metody otrzymywania zwierzat transgenicznychid 10950 ppt

10 dźwigniaid 10541 ppt

03 Odświeżanie pamięci DRAMid 4244 ppt

Prelekcja2 ppt

2008 XIIbid 26568 ppt

WYC4 PPT

rysunek rodziny ppt

więcej podobnych podstron