1

AUSTRALIA & ASIA

Peter Rowe – Head of AngloGold Ashanti Australia

Diggers & Dealers Forum 2004

Kalgoorlie – July 28, 2004

2

Except for the historical information contained in the presentation to be made, there are matters discussed

here that are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933,

as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Safe Harbor

provisions of the US Private Securities Litigation Reform Act of 1995. Although AngloGold Ashanti

believes that the expectations reflected in such forward-looking statements are reasonable at this time, no

assurance can be given that such expectations will prove to have been correct.

These statements, including those given during the question and answer part of this presentation, are

therefore only predictions and actual events or results may differ materially. You are cautioned not to

place undue reliance on such forward-looking statements. For a discussion of important risk factors

including, but not limited to, development of the Company’s business, the economic outlook in the gold

mining industry, expectations regarding gold prices and production, and other risk factors which could

cause actual results to differ materially from any forward-looking statements, please refer to AngloGold’s

annual report on Form 20-F for the year ended 31 December 2003 which was filed with the Securities and

Exchange Commission on March 19, 2004 and any document filed under Form 6-K in connection with the

merger of AngloGold and Ashanti.

AngloGold Ashanti does not undertake any obligation to update publicly any forward-looking statements

discussed in this presentation, whether as a result of new information, future events or otherwise.

DISCLAIMER

3

2004 compared to 2003

OUTLOOK

•Reserves of some 84 Moz

•Production of 6.3 Moz

•Total cash costs of US$254/oz*

*

Using currency assumption of R6.76/US$ and US$0.74/A$ in 2004

+33%

+12%

+15%

This is AngloGold Ashanti’s fifth Diggers & Dealers Forum since the company listed

on the Australian Stock Exchange and we are very pleased to be participating once

again.

Since that debut appearance, the company has grown earnings and diversified

further to become the truly global producer you saw on the video. That video clip

was distilled from what we think is a unique film encapsulating AngloGold Ashanti’s

values, as viewed through the eyes of the company’s employees. You can watch

the full video at our booth.

You will notice that we have a new logo following the completion of the merger with

Ashanti Goldfields in April. The merger has combined AngloGold’s technical

expertise and financial strength with Ashanti’s world-class people and orebodies

and we expect the benefits to become apparent as we realise the full potential of

these assets over the next few years.

In the short term AngloGold Ashanti’s reserves have been boosted by 33% to 84

million ounces and production this year will rise to between 6.2 and 6.3 million

ounces.

Charles Carter will go into more detail about the Ashanti merger and what it has

brought to the company later in this presentation. In the meantime I’d like to give

you an update on what we have been doing in the Australian and Asian region.

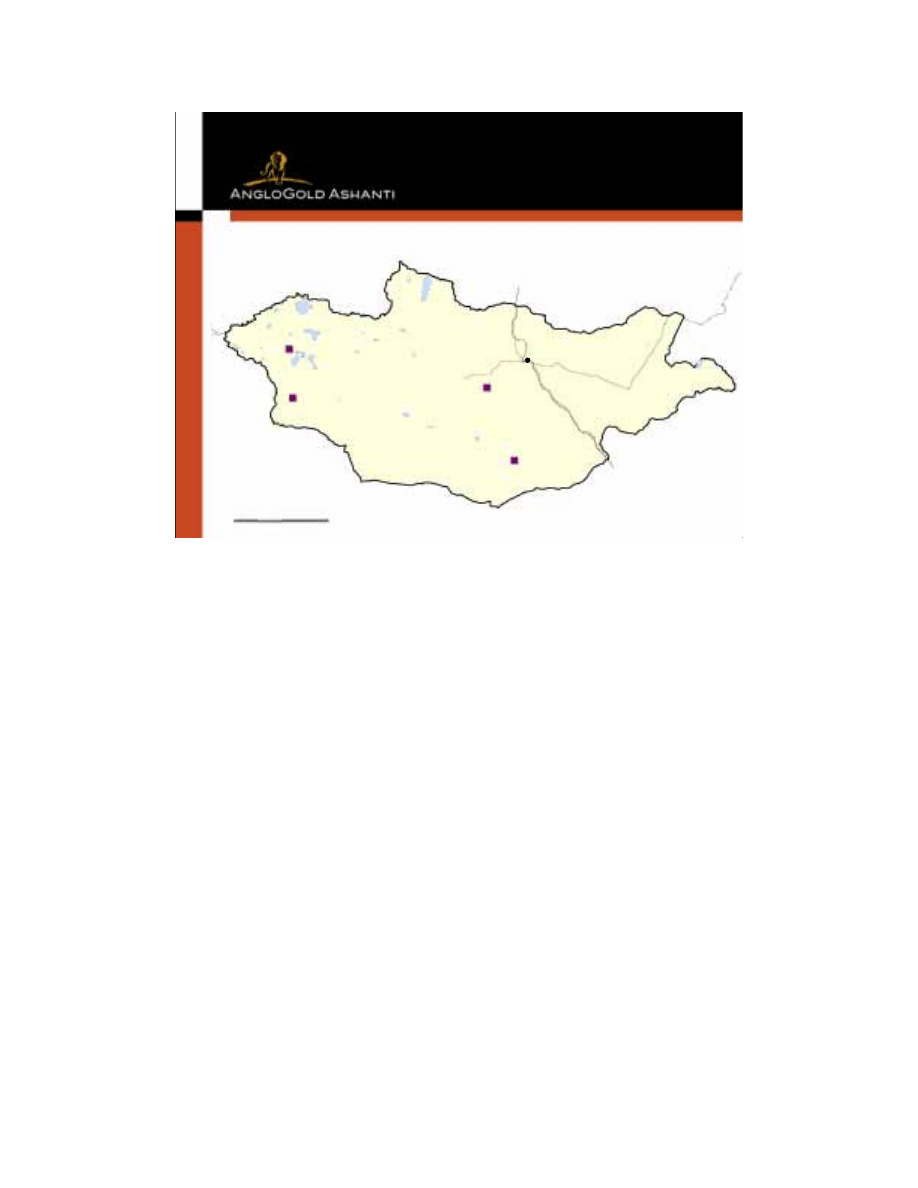

4

BEIJING

BEIJING

ULAANBAATAR

ULAANBAATAR

PERTH

PERTH

China

Mongolia

Australia

AngloGold Ashanti Offices

Laos

Indonesia

Philippines

PNG

REGIONAL FOCUS

Union Reefs

Union Reefs

Sunrise Dam

Sunrise Dam

Boddington

Boddington

AngloGold Ashanti Mines

AngloGold Ashanti’s key assets in the Australian region are the Sunrise Dam gold mine,

220 kilometres north-east of Kalgoorlie, and the Boddington Expansion Project, 100

kilometres south-east of Perth, where we have a 33.3% interest in a joint venture with

Newmont and Newcrest.

As our Boddington partners have said in earlier in this forum, we all remain positive

about the potential of what is the largest undeveloped gold deposit in the world and we

are working together to take this project forward.

A first-rate team is revising the original feasibility study and optimising the project to

generate the best economic benefits possible. We are still considering a range of

throughput rates, all of which are higher than the 25 Mtpa envisaged in the original

study. We’re also considering whether or not to make provision in the flowsheet to allow

for expansion of the plant in the future.

We hope to be in a position to take recommendations to our boards about the expansion

of Boddington in the second half of 2005.

Union Reefs, in the northern Territory, is now in care and maintenance, and we are

considering options for divestment.

We carry out greenfields exploration in Western Australia and have opened an

exploration office in Mongolia and a representative office in China. Activities in these

countries and the other countries in the Asian region that are highlighted on the map are

managed out of our Perth office.

I’d now like to give you an update on our activities at the Sunrise Dam mine.

5

SUNRISE DAM

2 million ounces

produced since

start-up in March

1997

Milestone

I’m pleased to say that this month Sunrise Dam poured its 2 millionth ounce. This

has been achieved at an average cash cost of A$287/ounce.

The pit has reached a depth of 220m at its deepest point on its way to a final design

depth of 450m.

6

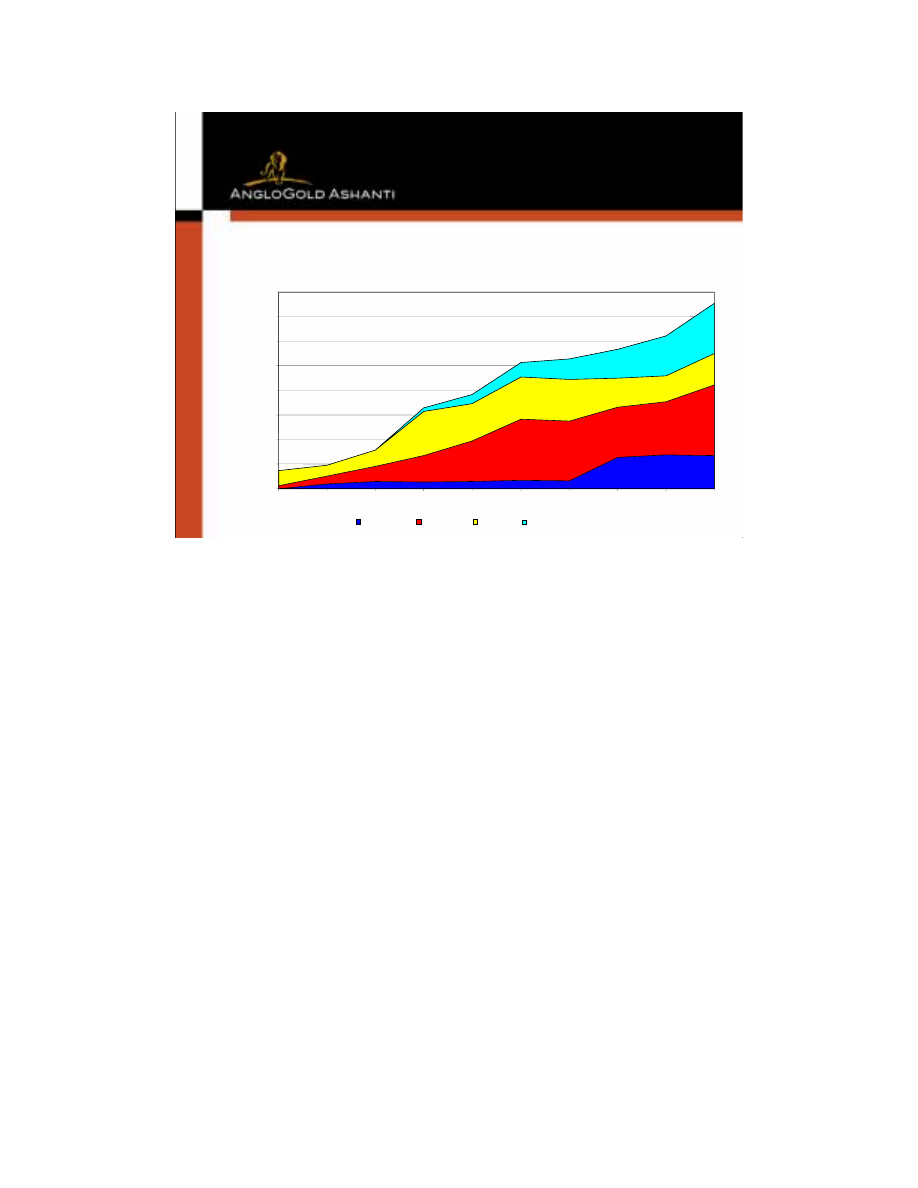

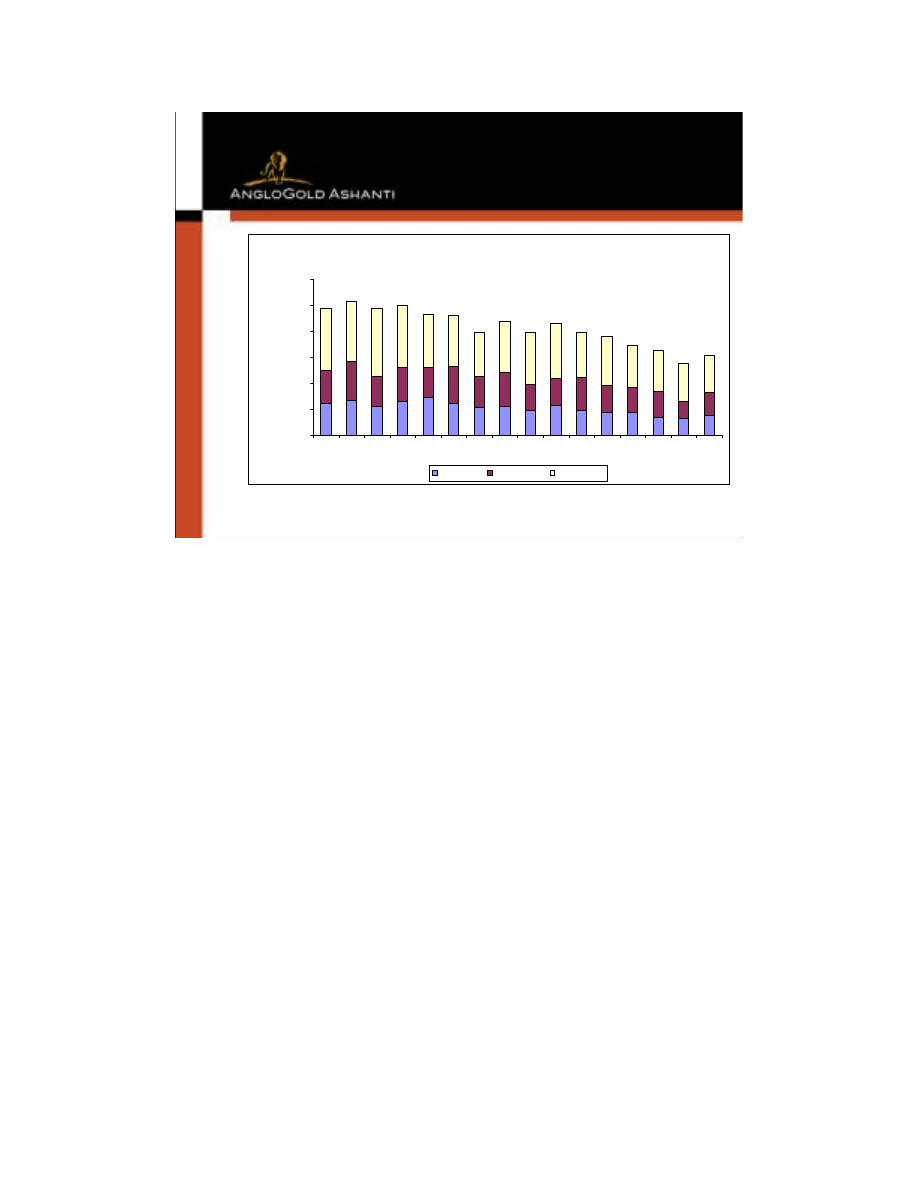

SUNRISE DAM

Sunrise Dam Gold Mine

Mineral Resource Growth

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Dec-94

Dec-95

Dec-96

Dec-97

Dec-98

Dec-99

Dec-00

Dec-01

Dec-02

Dec-03

K Ou

nces

Measured

Indicated

Inferred

Cumulative depletion

A key feature of Sunrise Dam since start-up has been steady growth in reserves

and resources. Drilling success and a remodelling of the orebody enabled the

geologists to add a further 1.34 million ounces to the resource last year, before

mining depletion of 0.44 million ounces, and 1 million ounces of reserves, again

before mining depletion.

The majority of this resource growth was in underground resources, particularly in

the GQ, Sunrise Shear and Hammerhead structures.

As at December 31, 2003, total resources at Sunrise Dam were 5.5 million ounces

and reserves at that date totalled 3.1 million ounces.

Ongoing drilling from surface and underground continues to deliver encouraging

results and we are confident we will add further to resources. We’ve allocated

approximately US$3.75 million for mine exploration this year.

Sunrise Dam is on track to produce 405,000 ounces in 2004 at a total cash cost of

US$237/oz.

7

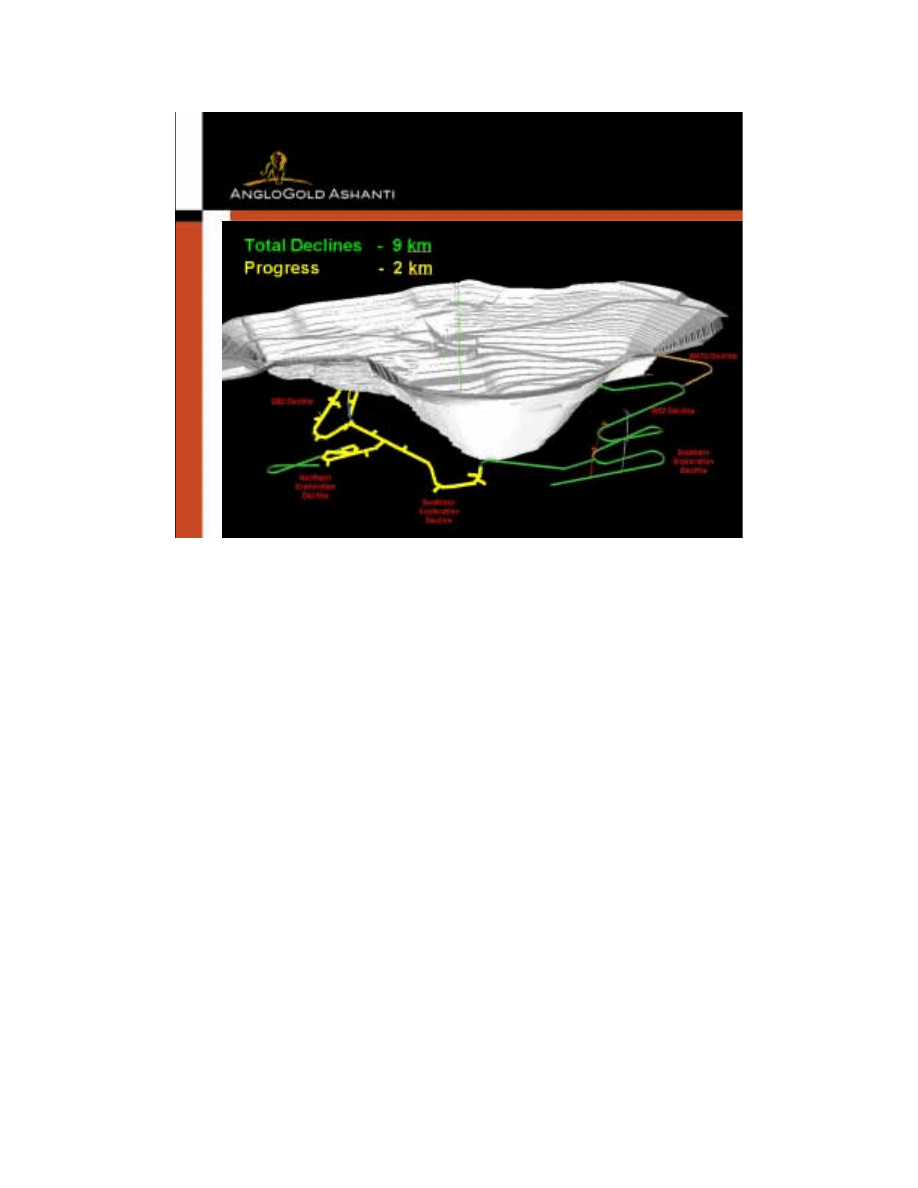

Subtitle

SUNRISE DAM - Underground

Last year when we presented at this Forum the AngloGold board had just approved

a three-year underground feasibility study at Sunrise Dam. To recap, this project

involves development of two declines and about 125 km of underground and

surface drilling to fully explore the underground potential of the operation. The

capital cost of A$87 million will be offset by the mining of known underground

reserves of about 300,000 oz. We hope to be able to make a decision to go ahead

with full scale underground mining early in 2007.

Development of the Daniel Decline, which goes through the Sunrise Shear Zone,

began in October last year and we’ve now completed approximately 2,600 metres of

development, of which 1,700m is decline development.

The Daniel Decline will give underground drilling access to the HQ, Dolly, Cosmo

and Hammerhead zones, which could not be effectively accessed or drilled in

sufficient detail from surface.

A second decline will be developed into the Western Shear Zone in 2005.

8

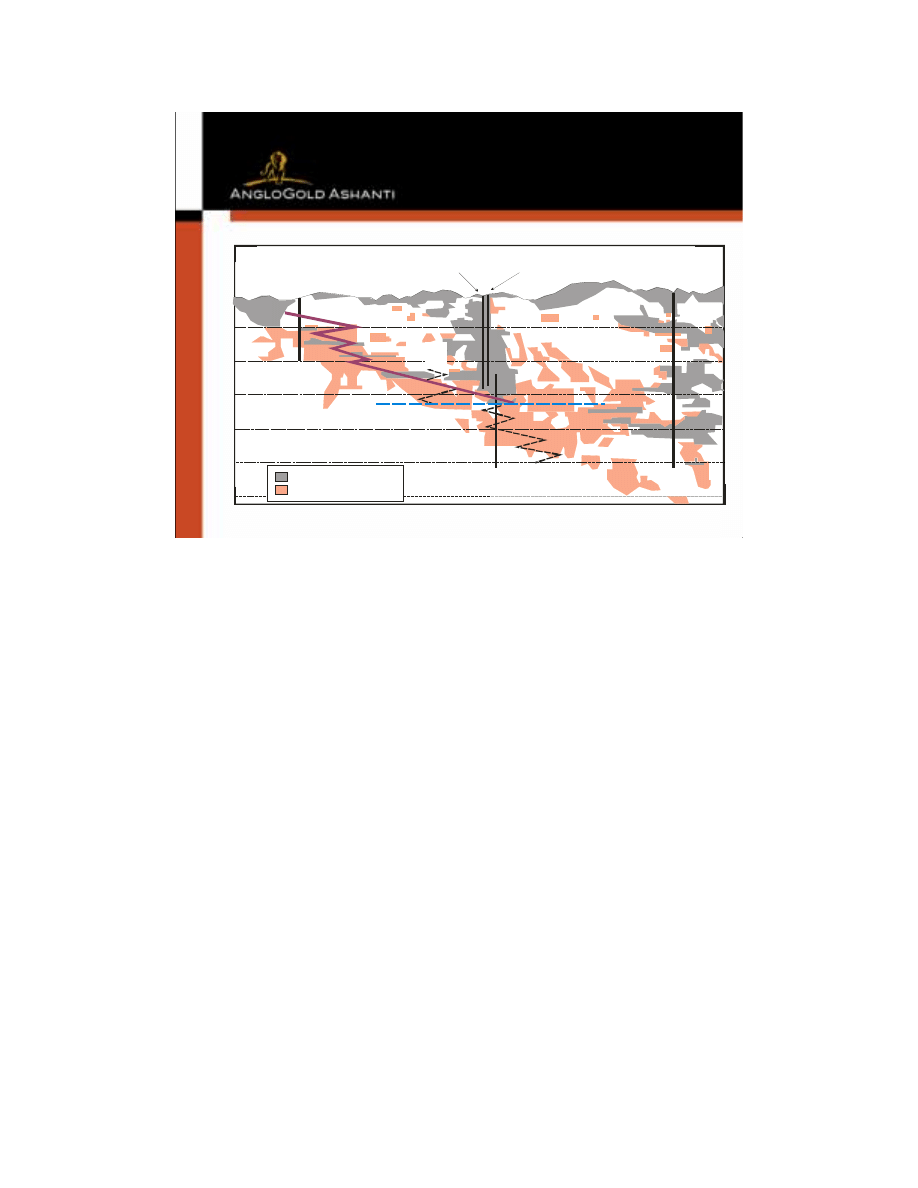

Sunrise Dam underground development

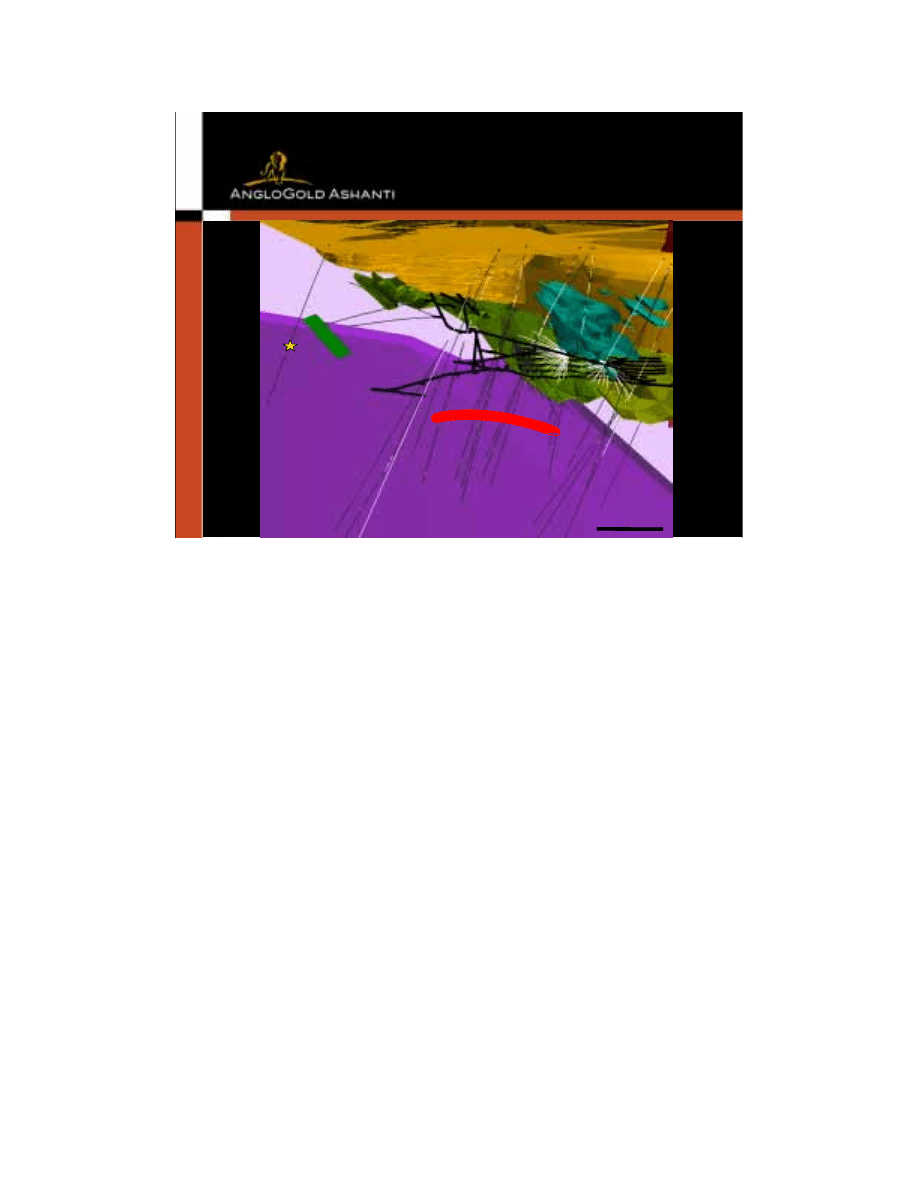

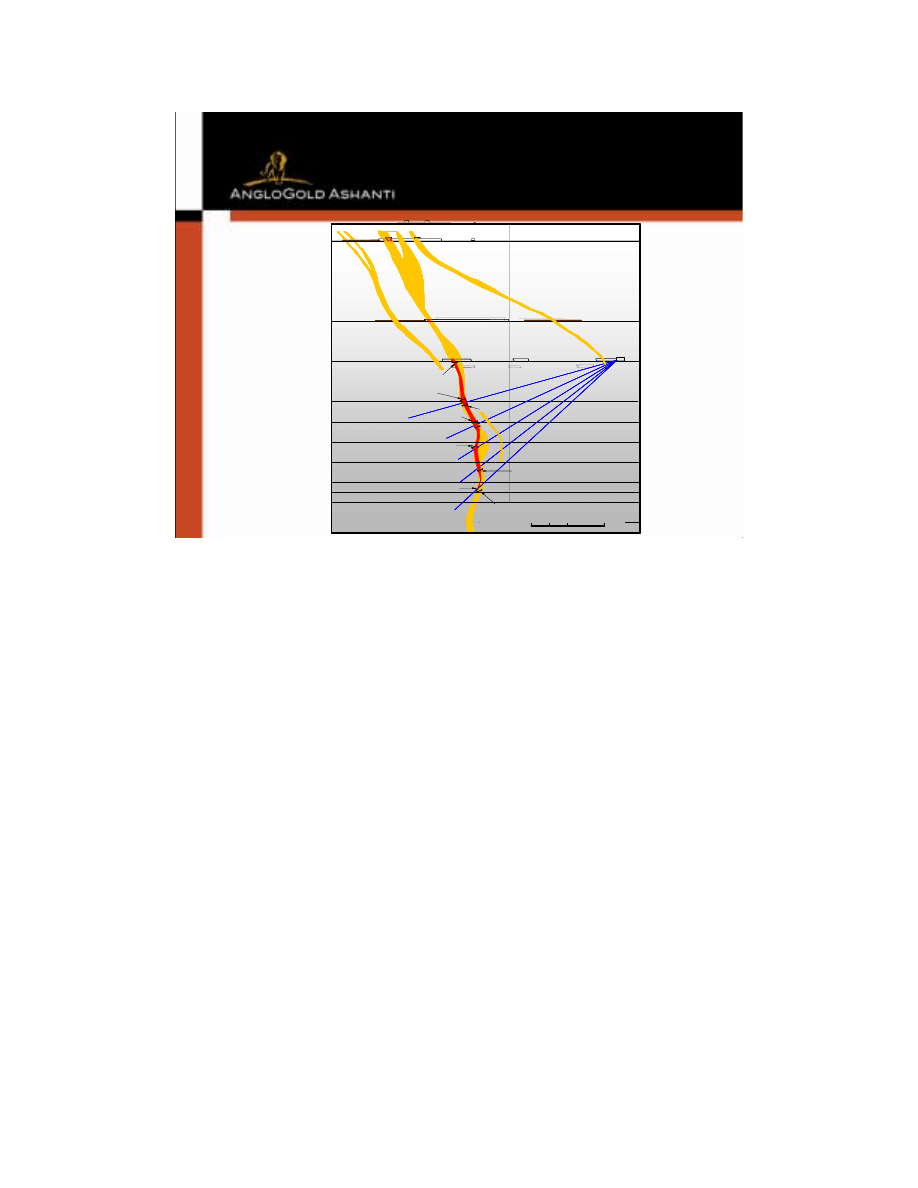

SUNRISE DAM - Northern Section

SOUTH

NORTH

200m

Sunrise

Shear

MAKO

MAKO

TARGET 007

TARGET 007

14m @ 38 g/t

NEW ZONE

NEW ZONE

Beneath Sunrise Pit

2m @ 10.4 g/t

5m @ 5.6 g/t

Care

y Sh

ear

ASTRO

ASTRO

ASTRO

3m @ 37.3 g/t

3m @ 32 g/t

3m @ 13.4 g/t

3m @ 11.7 g/t

This is a section showing the northern part of the deposit, looking to the

east, where underground development has provided the first underground

drilling positions at Sunrise Dam, enabling new zones to be tested at more

favourable orientations and at significantly lower cost.

This year we’ve discovered two new zones of mineralisation in the north.

Surface drilling north of the Sunrise pit ramp, in an area known as Target 7,

intersected strong mineralisation with abundant visible gold in a zone

approximately 8 metres wide, which is open to the north and south. 14m at

38.6 g/t was returned from the first hole and the follow-up programme has

just been completed.

Significant intercepts were also returned in the first underground exploration

hole drilled at Sunrise Dam. These results represent mineralisation located

beneath the Sunrise pit, which is open in all directions.

As you can see from these results, we’ve had encouragement from a

number of areas since the commencement of the Underground Feasibility

drilling programmes late last year.

You can also see on this slide that we have commenced underground

grade control drilling of the Sunrise Shear Zone, which is designed to prove

up the first underground stoping panels to be mined in 2004.

9

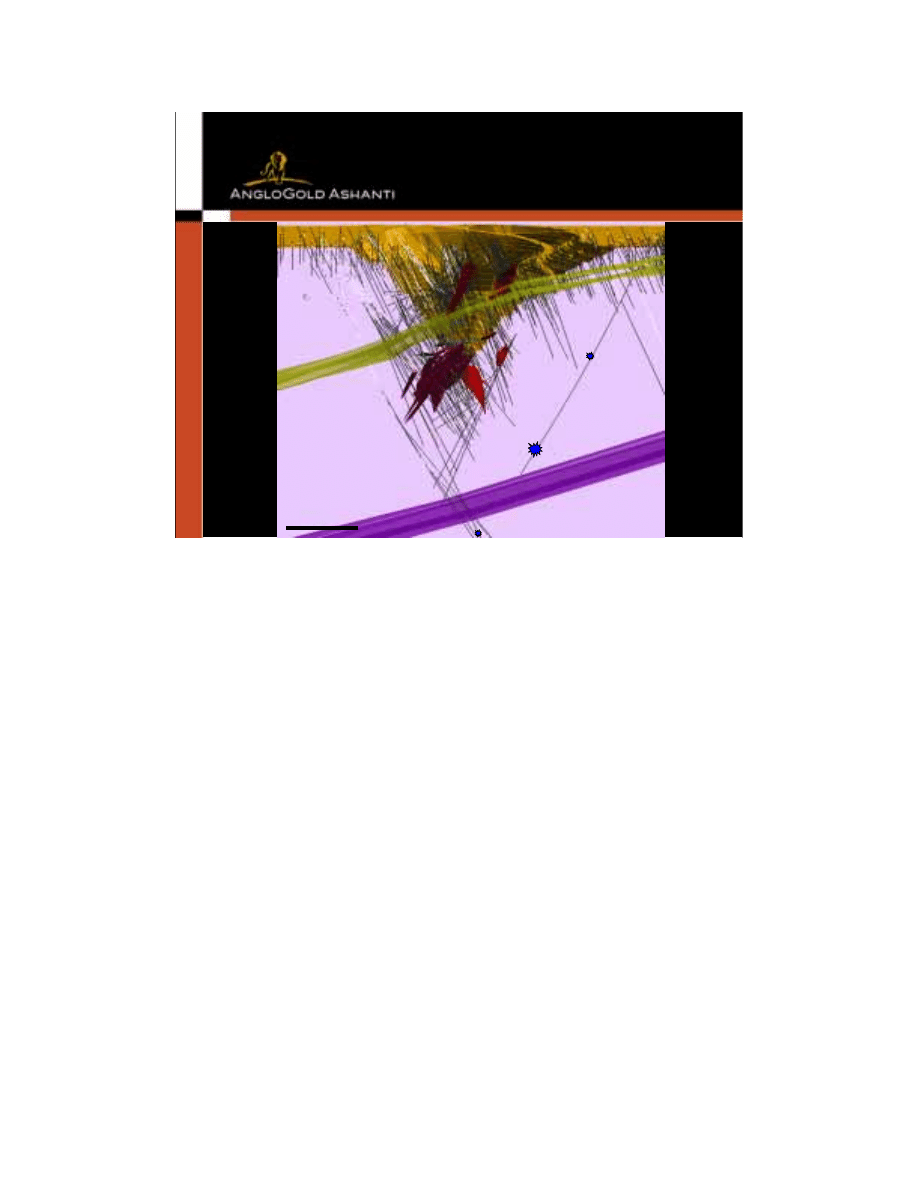

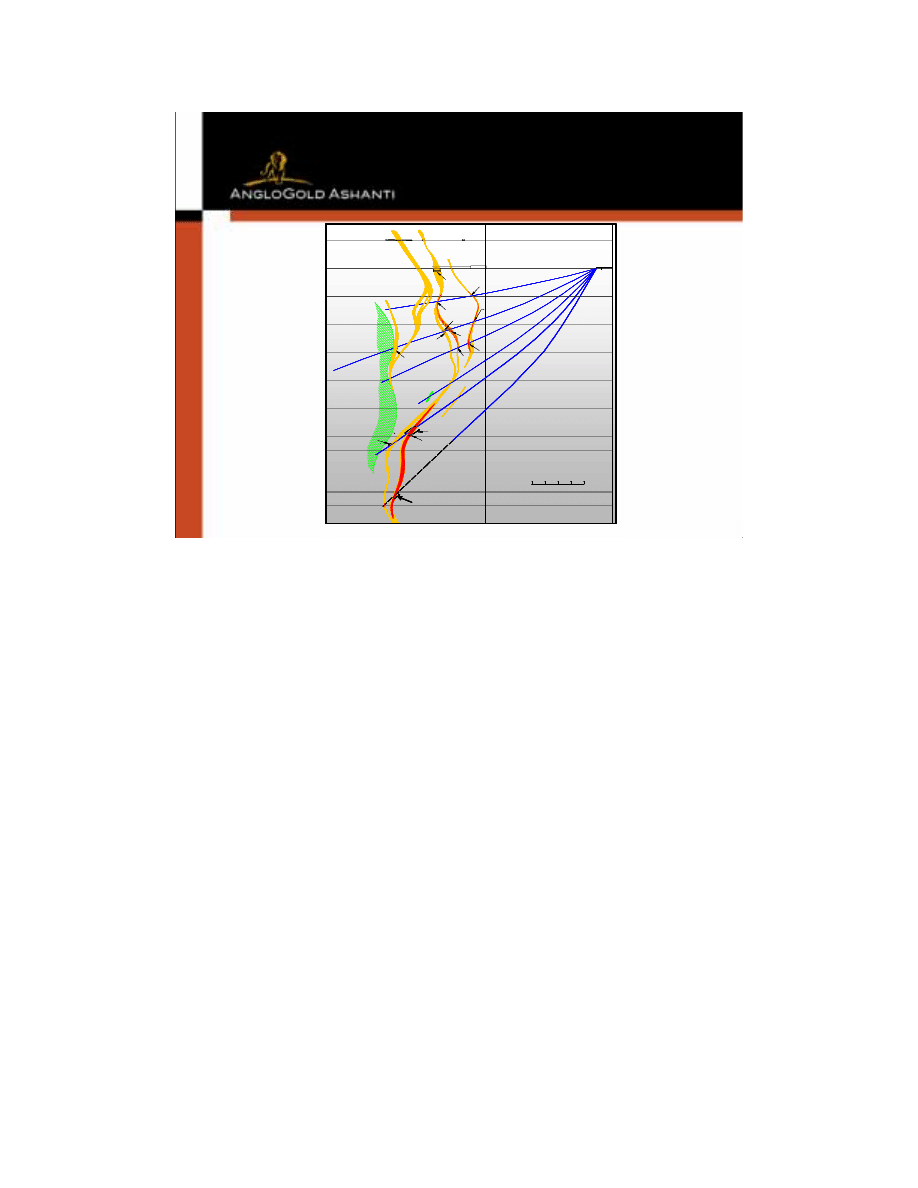

WEST

SUNRISE DAM - Southern Section

400m

EAST

Car

ey S

hea

r

Sun

rise

She

ar

Dolly

3m @ 85.9 g/t

3m @ 19.4 g/t

5m @ 13.5 g/t

6m @ 5.9 g/t

DOLLY

DOLLY

GQ

GQ

COSMO

COSMO

EXTENDED

400m DOWN-DIP

10m @ 53.6 g/t

Hammerhead

11m @ 110 g/t

11m @ 36.6 g/t

20m@ 6.7 g/t

7m @ 6.8 g/t

HAMMERHEAD

HAMMERHEAD

8m @ 5.8 g/t

Drilling last year confirmed the existence of the Carey Shear Zone, which we believe

is geologically analogous to the Sunrise Shear Zone. We also identified high-grade

mineralisation below this zone at a depth of about 1,200m. Gold beneath the Carey

Shear is significant in the geological model because it opens up the potential for the

discovery of new zones in up-dip positions, which, of course, will be at shallower

depths.

In the first half of this year we’ve been focusing on underground targets beneath the

pit including the Sunrise Shear Zone, Northern Deeps and Astro in the north and

Dolly, Cosmo and Hammerhead in the South.

This is a view of the southern part of the deposit looking toward the north.

Surface drilling into Dolly and Hammerhead continues to return high grade results.

Drilling has also extended the Cosmo mineralisation approximately 400 metres

down dip.

The area to the east of Cosmo and Hammerhead will be drilled from the base of the

open pit in the second half of this year. This is a poorly drilled area that has

considerable potential, as indicated by the recent intercept of 8m at 5.8 g/t, which is

similar in style to Hammerhead and open in all directions.

In the second half of the year underground drilling will focus on the southern part of

the deposit from positions that will become available in the Daniel Decline as it

progresses towards the south. Targets include GQ, Dolly, Cosmo and

Summercloud.

10

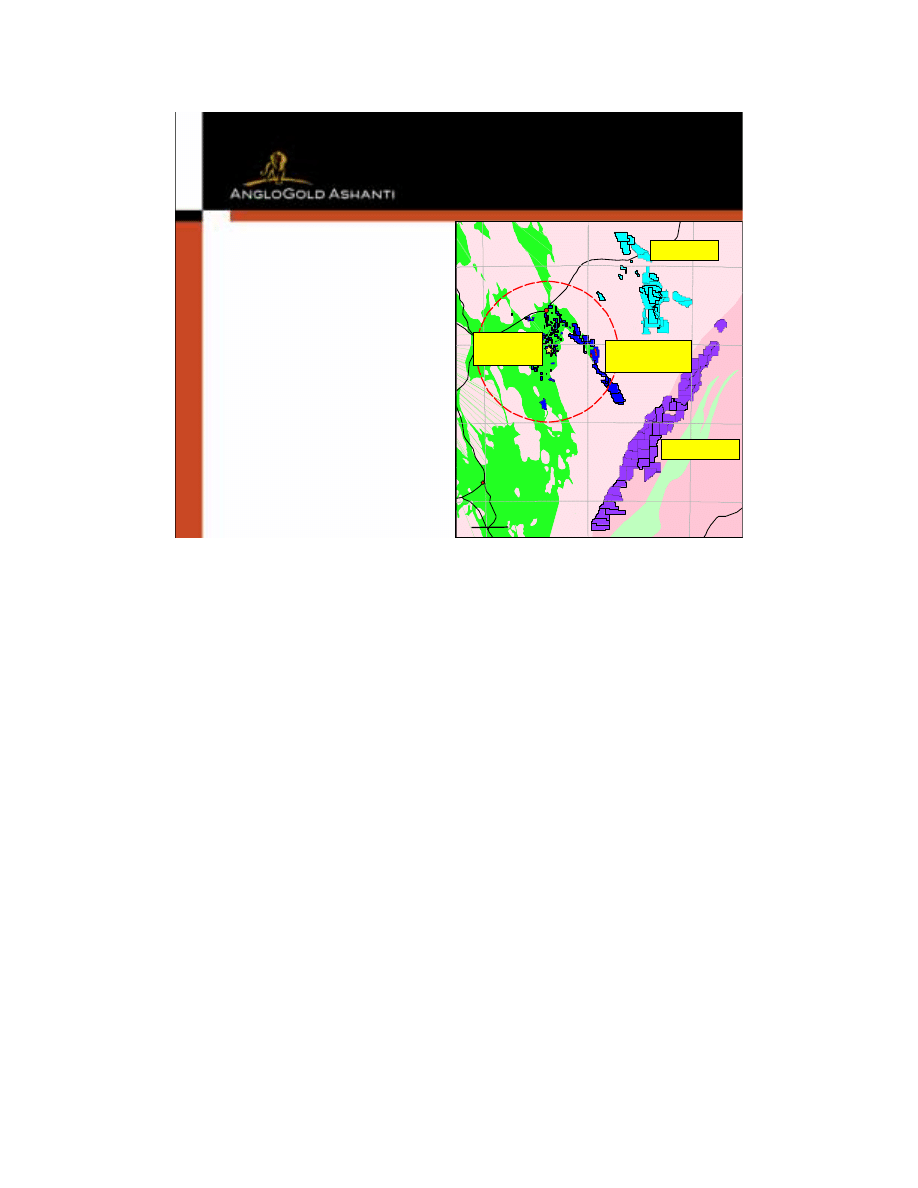

BROWNFIELDS

• Lord Byron & Fish

• Laverton

GREENFIELDS

•Yamarna

•Tropicana

YAMARNA

TROPICANA

LORD BYRON

60km

SUNRISE

DAM

100 km

KALGOORLIE

LAVERTON

121°00

123°00

124°45’

-28°00

-29°00

-30°00

0

50km

EXPLORATION

In the June quarter we completed the acquisition of the Lord Byron and Fish projects

in the Laverton Belt as part of a swap agreement with Apollo Gold (now Crescent

Gold). Previous explorers at Lord Byron and Fish had identified resources of

approximately 343,000 ounces and we are carrying out work to verify and extend

these resources. We will also be testing a number of new targets in the lease area

including a priority target north of the resource where there is a previously untested

high-order soil anomaly. A 40-hole drilling programme is underway at the project. Our

objective in the area is to locate additional resources, which may be exploited through

Sunrise Dam.

AngloGold Ashanti has a total exploration budget for 2004 of US$13.6 million for the

Australian and Asian region and of this we will spend US$6.9 million on greenfields

exploration.

Our two key greenfields exploration plays, also in Western Australia, are Tropicana,

where we are earning 70% from Independence Group and Yamarna, where we are

earning 70% from Terra Gold Mining.

The joint ventures cover large ground positions in both areas. At Tropicana we’ve

completed magnetic surveys and have drilling planned for the second half of this year

as Chris Bonwick explained in Independence’s presentation on Monday.

At Yamarna first pass drilling of the southern targets has been completed, returning a

number of anomalous results requiring follow up. With Aboriginal access agreements

being finalised we plan to test our northern targets in the near future.

11

Alternatives for working with juniors

BUSINESS DEVELOPMENT

•

joint ventures

• option agreements

• buy-back/claw back arrangements

• equity investments

• divest with retained exposure to upside

• strategic alliances

We are actively examining exploration opportunities in a number of Asian countries,

either in our own right, or through partnerships with local companies and juniors.

AngloGold Ashanti believes it is healthy to develop and nurture relationships with

juniors to capitalise on the strengths of both parties and thereby increase our

options.

We are flexible in the arrangements we form with juniors and agreements can range

from simple joint ventures to deals like the one we announced with Trans Siberian

Gold last month where we have taken an equity stake in the company in a staged

agreement.

12

MONGOLIA

ULAANBAATAR

RUSSIA

CHINA

Ikh Shankh

Delgerkhaan

Tsagaan Tolgoi

Baruun Khuurai

MONGOLIA

0

500

kilometres

As traditional exploration areas mature and the acquisition and discovery of

orebodies has become more difficult, AngloGold Ashanti is focusing on prospective

areas in the globe that may have a higher risk profile.

As I mentioned at the start of this presentation, we’re now active in Mongolia and

China as part of this “new frontiers” strategy, which is being managed in the Asia-

Pacific region by the Perth office.

We’ve established an exploration office in Mongolia where we are actively picking

up tenements. Do date the majority of our field work has focused on the Ikh Shankh

property in the Southern Gobi, about 100 km from Oyu Tolgoi. This is a classic

porphyry gold-copper target and we’ve completed mapping, sampling, ground

magnetic and IP surveys. Drilling of a coincident magnetic-IP anomaly is scheduled

to start later this year.

In China we have established a representative office in Beijing, which forms the

base for two expat and two Chinese national geologists. This team is investigating

opportunities, building relationships and developing an understanding of the

operating environment. We are taking a long-term view on China.

I’d now like to hand over to Charles Carter who will give you an update on the

integration of the Ashanti assets.

13

ASHANTI INTEGRATION

Charles Carter - Vice President

Diggers & Dealers Forum 2004

Kalgoorlie – July 28, 2004

Thank you Peter.

In the brief time I have, I want to cover key points about the merger with Ashanti,

with the focus mainly on the Obuasi mine in Ghana, given that this is a large driver

of value in the deal, though by no means the only one.

14

AngloGold Ashanti merger complete 26 April 2004

• significant present and future production, acquired at a good price

• increased reserves by 33%

• focus on:

• adding value to existing Ashanti operations

• exploiting long life assets with significant reserve growth potential

• Obuasi:

• improve production and costs above 50L

• Obuasi Deeps potential

MERGER OVERVIEW

AngloGold’s merger with Ashanti was completed on April 26, 2004. Our second

quarter, which we report on Friday, will account for these assets as from 1

st

May.

On a comparative basis to other transactions in the gold sector, we have gained

significant present and future production at a good price. As Peter has mentioned,

our reserves have increased by 33%. Two strategic imperatives drove this

transaction:

- Adding value to existing Ashanti operations, using our cash flow and balance sheet

strength, together with our diverse technical expertise

- Putting our foot on long life assets with significant reserve growth potential

In terms of value drivers, there are two parts to the Obuasi story, which I’ll discuss

briefly in this presentation

- Improving production and costs above 50 level

- Turning to account the Obuasi Deeps potential

15

WEST AFRICA

0

2

4

6

8

10

12

Mo

z

Ya

te

la

Bi

bia

ni

Sa

di

ol

a

M

ori

la

S

ig

ui

ri

Id

uap

riem

-T

eb

er

eb

ie

Ob

uasi

WEST AFRICA - RESERVES

SENEGAL

MALI

BURKINA

GUINEA

SIERRA LEONE

COTE d’IVOIRE

GHANA

TOGO

LIBERIA

BAMAKO

DAKAR

CONAKRY

FREETOWN

MONROVIA

ADIBJAN

ACCRA

LOME

OUAGADOUGOU

500

0

kilometres

YATELA

YATELA

SADIOLA

SADIOLA

MORILA

MORILA

SIGUIRI

SIGUIRI

BIBIANI

BIBIANI

OBUASI

OBUASI

IDUAPRIEM

IDUAPRIEM

-

-

TEBEREBIE

TEBEREBIE

AFRICA

JOHANNESBURG

CAIRO

MAP AREA

Atlantic

Ocean

First though, let me comment briefly on our now dominant presence in West Africa.

This part of the world, notwithstanding its very long and distinguished history in gold mining,

is emerging as a significant growth region for gold.

In addition to ourselves, you have Gold Fields, Golden Star, Randgold and Iamgold as

producers, with Newmont (thanks to Normandy) and Red Back Mining poised to become

producers from 2005/6. Combined, AngloGold Ashanti and these six companies are

expected to produce an estimated 4 Moz per annum from 2006 in West Africa, with over $1

billion being spent on project development over the next three years.

This year, approximately 22% of AngloGold Ashanti’s production will come from West Africa

(50% from Southern Africa, 10% from East Africa, and 5-8% each from Australia, North and

South America). Obuasi and Geita alone in 2003 produced over 1 million ounces.

Thus this transaction has allowed us to consolidate our ownership of Geita in Tanzania –

which is a very exciting property – and to build on our presence in Mali and now Ghana, to

become the dominant gold player in West Africa.

We have completed the restructuring of the Ashanti corporate structure – closing their

London office, relocating some Ashanti officers to Johannesburg, and rationalizing

remaining management. Savings of approximately $11.4m p.a. have been realized through

the repayment of Ashanti’s $139m revolving credit facility, the termination of consulting

contracts, restructuring insurance contracts and procurement procedures, and closing their

London office.

16

Level 50 (1640mbd)

Level 40

Level 30

Level 20

Level 10

Sansu

Shaft

Kwesi

Renner

Shaft

George

Cappendell

Shaft

Brown

Sub V

Shaft

Outen

Kwesi

Mensah

Shaft

West

Shaft

Ellis

Shaft

Adansi

Shaft

E.T.

Shaft

Level 60

Level 75

+ 8km

Mined out ar eas

N

S

Mineral Resource block

Projection of mineralisation

S

N

Obuasi above 50 level has resources of 20.9 Moz and Reserves of 10.8 Moz

Part of the value creation in the transaction involves fully modernizing the existing

Obuasi mines.

This vertical projection, approximately 8km across, shows South Mine, Central Mine

and North Mine

The Obuasi ore body has demonstrated continuity for some 8 km along strike and

1.5 km down dip.

Northern areas of the mine are characterized by thinner, higher grade, quartz vein

ore bodies. Southern areas house wider, lower grade, sulphide ores. The thinner,

higher grade quartz veins are the primary target of the Obuasi Deeps project, which

I’ll discuss in a moment.

Currently mining is predominantly sub-level open stoping, with minor cut and fill.

17

N

S

20L

30L

Mineral Resource block

40L

50L

60L

10L

Sansu

Shaft

Kwesi

Renner

Shaft

George

Cappendell

Shaft

Kwesi

Mensah

Shaft

Brown

Sub V Shaft

Mined out areas

Ramp

32L

S

N

As a result of holing the decline ramp in April, access between 26 and 32 levels in

South Mine has been completed, enabling access from the Sansu mine portal at

South Mine to 26 Level.

Thus in respect of early interventions, the last four months have seen visible

improvements in access for personnel and equipment in South Mine, while work is

ongoing to improve the planning and excavation of truck loading points,

intersections, passing areas and curves, so as to increase productivity and improve

safety. Maintenance areas have also been upgraded.

Work on the 32 Level connection between GCS and KMS shafts has been

prioritized, with completion scheduled for the second quarter of next year.

Once complete, you will be able to drive from surface at South Mine, through

Central Mine, to North Mine. This will have multiple benefits for fleet mobility,

maintenance and efficiency, as well as for ventilation (for South Mine) and

exploration, with 32 Level becoming a drilling platform.

Completion of the BSVS shaft equipping is also underway. Raise boring of 16L to

26L should be completed in December 2004 – this is being done for ventilation. It

will take 6 months to equip the conveyor drive. Targeted start to development is Q3

2005, with development to KMS shaft in 2005/2006. This will allow development and

effective mining of the lower blocks in Central Mine.

We believe there is significant exploration potential at Obuasi above 50 level.

18

Obuasi Development Performance - Metres

-

2,000

4,000

6,000

8,000

10,000

12,000

Q2'00 Q3'00 Q4'00 Q1'01 Q2'01 Q3'01 Q4'01 Q1'02 Q2'02 Q3'02 Q4'02 Q1'03 Q2'03 Q3'03 Q4'03 Q1'04

Me

tr

e

s

North Mine

Central Mine

South Mine

At Obuasi, a lack of developed and drilled reserves, in addition to equipment

availability, is impacting gold production. The delivery of new equipment is in

progress, principally drill rigs, loaders and trucks. Lower than planned development

achievements are being addressed by improving the mining contractor’s equipment.

The cumulative impact of reduced development is what constrains most aspects of

Obuasi’s mine plan today. This we are tackling as we speak.

19

CHALLENGES

At Obuasi, near term challenges include:

• lack of developed and drilled reserves

• refurbishment and rationalisation old equipment

• new equipment starting to arrive

• new planning systems

• ventilation and cooling

Impact of interventions should be visible in 4-6 quarters

In respect of mine equipment, the overall objective is to reduce equipment from 200

units to 160 units and in the process to remove excess equipment from the mine. At

the same time, the fleet is being upgraded and refurbished. A fleet size of less than

30 LHDs, including those used by the contractor, is being targeted.

We have appointed a new GM and have delayered the local management team. A

new Mineral Resource Manager has been appointed and the centralisation of the

MRM office and personnel at Obuasi is underway. GMSI and Datamine are tasked

to assist with a full system design and data processing. Once fully operational, the

new MRM system will result in additional confidence in the calculation of reserves

and resources, greater flexibility in life of mine planning processes, and detailed

reconciliation and production reporting.

A project team, led by a new Workplace Environmental Manager, has been set up

to review all aspects of ventilation and cooling, with the immediate priority on short

and medium term interventions aimed at addressing temperatures particularly in

Central Mine.

Thus while near term we have our work cut out to improve production and

efficiencies at Obuasi above 50 level, there is significant upside for us in achieving

this. We should start to see the beneficial results of these interventions in the next

4-6 quarters.

20

CHALLENGES

Obuasi Deeps

• 45,000m drilling completed in Central Deeps

• Coverage along strike of whole ore body, in 5 year programme

• Two phase development in initial conceptual studies

• Dedicated Deeps project team in place late year

In respect of exploration at depth, thus far 45,000m of diamond drilling has been

completed in Central Deeps, while drilling in North Deeps has started. This is to test

mineralization in the southern corridor gray areas, between North and South mines

(i.e. drilling from 42 North and 19 North, at 39L, testing towards the South).

The focus to date has been around the KMS central shaft and is now shifting to the

North area. The intention is to get coverage along the whole strike of the ore body.

Currently six holes to test the Deeps are being planned, while consideration is also

being given to undertaking at least one long hole to 3 km, so as to confirm structure

at depth.

The current conceptual approach to develop Obuasi Deeps is based on two phases:

First, accessing the top part of the Deeps orebody quickly, using declines, and the

existing shaft infrastructure. In this model the cost would be spread over time,

making the project self-funding. Pre-requisites for fast tracking are increased

hoisting capacity of KMS shaft from 51L and a sufficient supply of cool air. Second,

sinking a new deep shaft, with associated infrastructure, to enable access beyond

65 Level.

These conceptual studies are ongoing, while the expertise to develop plans for a

new vertical shaft and associated infrastructure should be in place at Obuasi by the

end of the year.

21

F/W

OBF

H/W

0

40

80 M

L K

48 L

50 L

52 L

53 L

54 L

55 L

56 L

56.5 L

57 L

-1214m

-1273m

58 L

-1095m

44 L

BHUD50155W10

BHUD50155W11

BHUD50155W21A

BHUD50155W15A

BHUD50155W16A

CHAMBER

BH3565

BH3783

BH3728

8. 5

/4.8m

2. 2

/3.3m

R.D.

28. 0

/6.1m

R.D.

162E

36. 2

4.9m

21. 0

/4.4m

58. 8

/6.4m

/6.3m

26. 9

34. 2

/1.4m

10

.

5

/7.2m

Vis.Au

Vis.Au

Vis.Au

Vis.Au

Vis.Au

155W

18. 7

/2.6m

F/W

OBF

H/W

0

40

80 M

L K

48 L

50 L

52 L

53 L

54 L

55 L

56 L

56.5 L

57 L

-1214m

-1273m

58 L

-1095m

44 L

BHUD50155W10

BHUD50155W11

BHUD50155W21A

BHUD50155W15A

BHUD50155W16A

CHAMBER

BH3565

BH3783

BH3728

8. 5

/4.8m

2. 2

/3.3m

R.D.

28. 0

/6.1m

R.D.

162E

36. 2

4.9m

21. 0

/4.4m

58. 8

/6.4m

/6.3m

26. 9

34. 2

/1.4m

10

.

5

/7.2m

Vis.Au

Vis.Au

Vis.Au

Vis.Au

Vis.Au

155W

18. 7

/2.6m

F/W

OBF

H/W

0

40

80 M

L K

48 L

50 L

52 L

53 L

54 L

55 L

56 L

56.5 L

57 L

-1214m

-1273m

58 L

-1095m

44 L

BHUD50155W10

BHUD50155W11

BHUD50155W21A

BHUD50155W15A

BHUD50155W16A

CHAMBER

BH3565

BH3783

BH3728

BHUD50155W15A

BHUD50155W16A

CHAMBER

BH3565

BH3783

BH3728

8. 5

/4.8m

2. 2

/3.3m

R.D.

28. 0

/6.1m

R.D.

162E

36. 2

4.9m

21. 0

/4.4m

58. 8

/6.4m

/6.3m

26. 9

34. 2

/1.4m

10

.

5

/7.2m

Vis.Au

Vis.Au

Vis.Au

Vis.Au

Vis.Au

155W

18. 7

/2.6m

This cross section shows intersections from one site – grades in this fracture zones

are in line with historical quartzite values.

22

?

SCALE

48L

50L

52L

54L

56L

58L

60L

62L

63L

66L

67L

1.3g/t

/

0.4m

2.5g/t

13.0m

4.6g/t

/

0.5m

2.7g/t

/3.0m

4.4g/t

/

0.8m

1.3g/t

/3.2m

1.5g/t

/3.4m

2.3g/t

0.7m

65.8g/t

/13.3m

8.9g/t

/6.1m

17.9g/t

/4.6m

41.6g/t

/21.3m

39.5g/t

/9.0m

Vis Au

Vis Au

Vis Au

BHUD50173E02

BHUD50173E03

BHUD50173E04

BHUD50173E05A

169W

170W

173W

K

J

BHUD50173E10A

BHUD50173E12A

2.0g/t

7.1m

3.0g/t

5.8m

20

0

20

40

60 M

?

SCALE

48L

50L

52L

54L

56L

58L

60L

62L

63L

66L

67L

1.3g/t

/

0.4m

2.5g/t

13.0m

4.6g/t

/

0.5m

2.7g/t

/3.0m

4.4g/t

/

0.8m

1.3g/t

/3.2m

1.5g/t

/3.4m

2.3g/t

0.7m

65.8g/t

/13.3m

8.9g/t

/6.1m

17.9g/t

/4.6m

41.6g/t

/21.3m

39.5g/t

/9.0m

Vis Au

Vis Au

Vis Au

BHUD50173E02

BHUD50173E03

BHUD50173E04

BHUD50173E05A

169W

170W

173W

K

J

BHUD50173E10A

BHUD50173E12A

2.0g/t

7.1m

3.0g/t

5.8m

20

0

20

40

60 M

?

SCALE

48L

50L

52L

54L

56L

58L

60L

62L

63L

66L

67L

1.3g/t

/

0.4m

2.5g/t

13.0m

4.6g/t

/

0.5m

2.7g/t

/3.0m

4.4g/t

/

0.8m

1.3g/t

/3.2m

1.5g/t

/3.4m

2.3g/t

0.7m

65.8g/t

/13.3m

8.9g/t

/6.1m

17.9g/t

/4.6m

41.6g/t

/21.3m

39.5g/t

/9.0m

Vis Au

Vis Au

Vis Au

BHUD50173E02

BHUD50173E03

BHUD50173E04

BHUD50173E05A

169W

170W

173W

K

J

BHUD50173E10A

BHUD50173E12A

2.0g/t

7.1m

3.0g/t

5.8m

20

0

20

40

60 M

SCALE

48L

50L

52L

54L

56L

58L

60L

62L

63L

66L

67L

1.3g/t

/

0.4m

2.5g/t

13.0m

4.6g/t

/

0.5m

2.7g/t

/3.0m

4.4g/t

/

0.8m

1.3g/t

/3.2m

1.5g/t

/3.4m

2.3g/t

0.7m

65.8g/t

/13.3m

8.9g/t

/6.1m

17.9g/t

/4.6m

41.6g/t

/21.3m

39.5g/t

/9.0m

Vis Au

Vis Au

Vis Au

BHUD50173E02

BHUD50173E03

BHUD50173E04

BHUD50173E05A

169W

170W

173W

K

J

BHUD50173E10A

BHUD50173E12A

2.0g/t

7.1m

3.0g/t

5.8m

20

0

20

40

60 M

The second cross section shows the deepest drilling to date down to 67 level and

further good grades below 60 level. If mineralization is extrapolated down to 100

level (3000m) – and there’s no reason why this shouldn’t be the case – then there’s

a long life ahead for Obuasi Deeps.

23

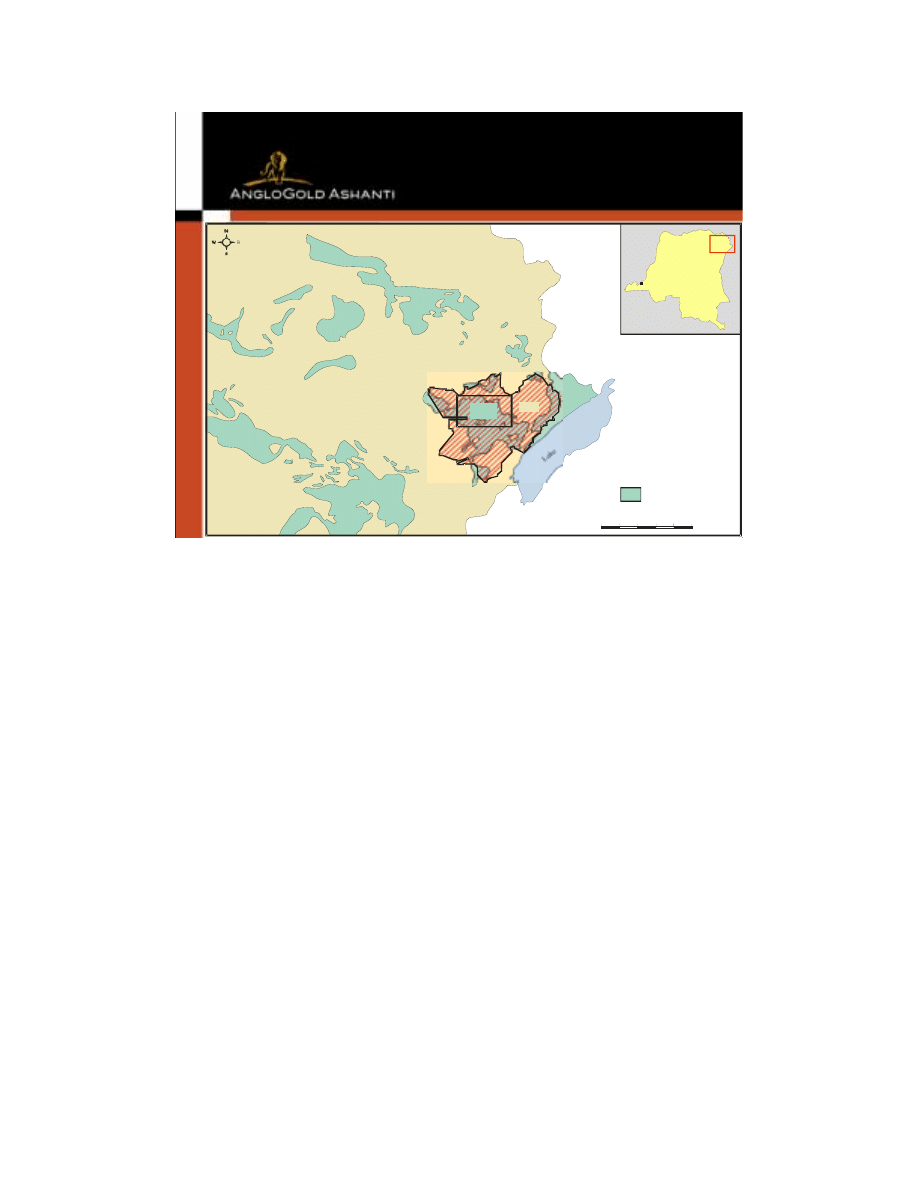

Sudan

Uganda

Lake Albert

0

100 km

Kinshasa

Democratic

Republic

of Congo

Greenstones

Doko

Kimin

C40

C40

EXPLORATION

Lastly, let me comment briefly on our African exploration activities.

The combined AngloGold and Ashanti African exploration teams have been merged

and rationalized, and have relocated to Accra.

Exploration presence has been withdrawn from Sierra Leone, Burkino Faso and

Cote d’Ivoire.

Outside of West Africa, where we are exploring in Ghana and Mali, preparations are

being made to commence exploration drilling on the Kimin prospect in the Ituri

region of the DRC. While this is obviously a tough environment right now, we are

looking forward to the opportunity to fully explore the properties we have in the

Congo, believing that we now have access to potentially exciting growth prospects

in Central Africa.

Thank you.

Wyszukiwarka

Podobne podstrony:

The Gold diggers song

Carol Lynne Solo (Grave Diggers MC 1)

Waste Diggers Animal companions

Bucket clam diggers basket

#0499 – Marrying a Gold Digger

aqua digger 3d

Gold digger Badboy

Erle Stanley Gardner [Mason 26] The Case of the Gold Digger s Purse (rtf)

tommy emmanuel diggers waltz

więcej podobnych podstron