Фінанси

Зовнішня торгівля: економіка, фінанси, право. №2 2010

114

Grażyna A. Olszewska, Ph.D., assistant professor,

Chair of Business and International Finances, Faculty of Economics,

Kazimierz Pulaski Technical University of Radom.

CHANGES IN THE QUALITY OF BANK CREDIT PORTFOLIOS IN POLAND

IN THE PERIOD OF TRANSFORMATIONS AND THAT

OF THE FINANCIAL CRISIS

Introduction

Restructuring of bad debts is a very complex problem in any circumstances, not only in the situation of

economic transformations. The period of economic transformation is characterized by frequent changes

on the map of the institutional market. In such a situation it is difficult for economic subjects to sustain

continuity of debt servicing. Creating conditions for a proper development of the credit policy system by

means of changes in the field of bank functioning enables these banks effective capital allocation. As

maximum effectiveness of resource utilisation is the essential aspect of market economy, then the basis

for this will be creating a high quality financial system based on the banking system. However, one can-

not speak about effective capital allocation without an effective credit policy of banks. The financial sys-

tem and in particular the banking sector which is its pillar, is as the recent financial crisis revealed, a kind

of a „barometer” for economy. As an effective credit policy can help in such important processes as the

systemic transformation, then its inefficiency can also be a source of serious disturbances

1

.

Causes of bad debt increasing

In literature bad debts are often described as remains of the centrally controlled economy, which is an

erroneous statement. In the producer-dominated economy of deficiency (shortages), unique conditions

arise which eliminate the credit risk for banks. Producers can easily include all costs in the price of prod-

uct without any fear that they will not find buyers. In the previous period there was no problem of repay-

ment of credits which were borrowed by companies. Only the market economy and lack of shortages have

revealed the real risk of losing the creditworthiness by institutional borrowers. A part of bad debts is in-

herited from the monobank system resulting from the inherited asset structure as shaped in the period pre-

ceding the economic reform.

2

Following this period all banks created their credit portfolios

independently, hence also bad debts. They can be attributed to internal factors resulting mainly from the

staff’s lack of qualifications in the field of credit risk assessment and monitoring

3

.

In the period of the 2007-2009 financial crisis, the causes of the credit portfolio quality worsening

were different.. The main channels of the financial crisis transmission for the commercial banks in Poland

were the proprietor’s channel and macroeconomic channel

4

. The activities of the proprietor’s channel

concerned mainly the influence of foreign owners on the activities of the banks controlled by them and

resulted in a stricter credit policy of these banks than in the case of banks where foreign capital was not

the dominating one. The macroeconomic channel’s effect was connected with the decreased external de-

mand due to economic recession in the markets of Poland’s main trade partners

5

.

Quality of credit portfolios

1

M. Mikita, Nowa rola rynku finansowego w gospodarce światowej (New role of the financial market in world

economy), in: J.L. Bednarczyk, S.I. Bukowski, J.Misala (ed.),Globalne rynki finansowe w dobie kryzysu (Global

financial market in the time of crisis), CeDeWu, Warszawa 2009, p. 170-171

2

S. Kawalec, Polska droga restrukturyzacji złych kredytów (Polish way of bad debt restructuring), in: Zeszyty

PBR – CASE No 12/1994, p. 12.

3

A. Ostałecka, Kryzysy bankowe i metody ich przezwyciężania (Banking crises and the ways of overcoming them),

Difin, Warszawa 2009, p. 10-12

4

Polska wobec światowego kryzysu gospodarczego (Poland in the situation of global economic crisis), Narodowy

Bank Polski, September 2009, p.27-28,

http://www.nbp.pl/home.aspx?f=/publikacje/polska_wobec_swiatowego_kryzysu_gospodarczego_2009/polska_wob

ec_swiatowego_kryzysu_gospodarczego.html

5

A. Kacprzyk, Kryzys finansowy 2008-2009 – przesłanki, kontrowersje, perspektywy (Financial crisis 2008-2009 –

premises, controversies, prospects), in: J.L. Bednarczyk, S.I. Bukowski, J. Misala (ed.), Współczesny kryzys

gospodarczy: przyczyny, przebieg, skutki (Modern economic crisis: causes, course, effects), CeDeWu, Warszawa

2009, p.77-79

Фінанси

Зовнішня торгівля: економіка, фінанси, право. №2 2010

115

During the 1990s financial crisis, the banks’ credit portfolio quality clearly deteriorated in 1992 (see:

Table 1). There are no statistics concerning the structure of this debt but it can be assumed, that its pre-

vailing part consisted of credits for economic subjects.

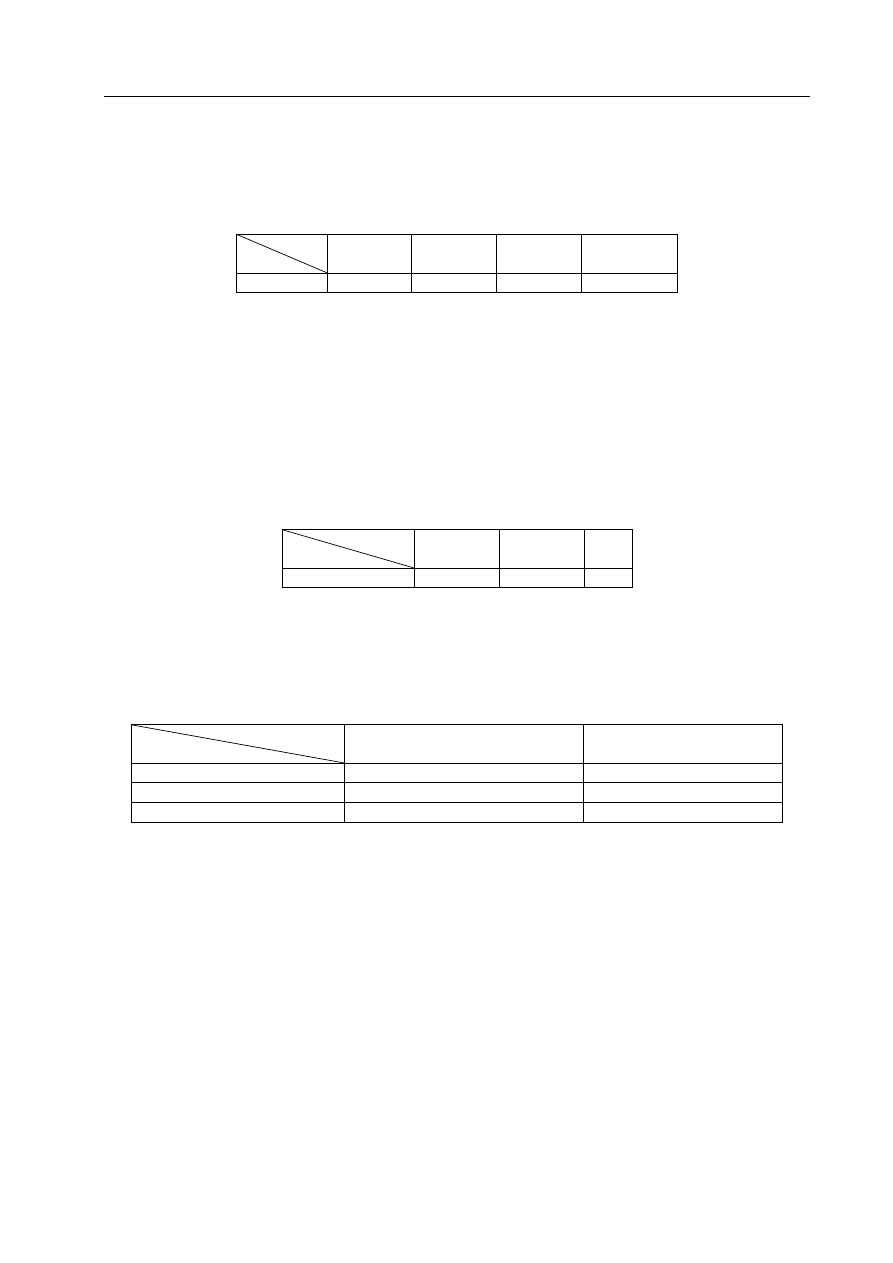

Table 1.

Percentage of difficult credits in total credits of commercial banks in the period of the national

programmes of bad debt restructuring in Poland in the years 1991-1994 (%)

Year

Country

1991

1992

1993

1994

Poland

2.41

19.20

23.80

36.73

R. Chudzik, Kryzys bankowy w gospodarkach postkomunistycznych na przykładzie Czech, Węgier

i Polski (Banking crisis in post-communist economies of the Czech Republic, Hungary and Poland), Bank

i Kredyt 3/1996, p. 20.

Such a high percentage of difficult credits threatened not only specific banks but also stability of the

banking sector as a whole.

An entirely different situation occurred at the beginning of the present crisis. In the first year of the

crisis the percentage of threatened credits in total credits of the banking sector decreased in relation to the

previous year (see: Table 2).

Table 2

Percentage of difficult credits in total credits of commercial banks in Poland

in the years 2007-2009 (%), end of September.

Year

Country

2007

2008

2009

Poland

4.2

3.6

6.1

Source: Informacja o sytuacji banków w okresie styczeń-wrzesień 2009 r. (Information on the situation of banks in

the period between January and September 2009), Komisja Nadzoru Finansowego

http://www.knf.gov.pl/Images/Informacja%20o%20sytuacji%20bankow%202009.09_tcm20-14054.pdf

Table 3

Percentage of threatened credits for economic subjects and households

in banks’ credit portfolios in Poland in the years 2007-2009 (%), end of September

Year

Credit for economic subjects

Credit for households

2007

7.4

4.4

2008

5.6

3.5

2009

10.8

4.9

Source: Informacja o sytuacji banków w okresie styczeń-wrzesień 2009 r. (Information on the situation of banks in

the period between January and September 2009), Komisja Nadzoru Finansowego ,

http://www.knf.gov.pl/Images/Informacja%20o%20sytuacji%20bankow%202009.09_tcm20-14054.pdf

Deteriorated quality of bank credit portfolios was revealed only at the beginning of 2009. It refers

mainly to credits lent to economic subjects. In the case of threatened credits for households, their percent-

age in total credits of the banking sector exceeded the 2007 level very slightly (see: Table 3).

Polish way of restructuring bad debts

The process of bad debt restructuring was carried out alongside enterprise restructuring. It disciplined

negligent debtors, whereas those who regained liquidity were able to start paying their debts off. Difficult

credits were divided into two basic groups – those lent before 1991 and current ones – loaned after 1991.

Banks were ordered not to give credits to clients from the „basic“ group debtors and were put under the

obligation to re-negotiate their credit agreements in order to create a realistic repayment schedule. They

had a chance of having their loans repaid in the open market or a duty of putting their debtors in liquida-

Фінанси

Зовнішня торгівля: економіка, фінанси, право. №2 2010

116

tion if previous options had not proved successful. Banks could use the same package of remedies with

reference to other debtors but they retained a possibility of their further crediting

1

.

Liberalisation of regulations concerning awarding licences for banking activities was the first method

of privatisation. It led to quick development of the market and emergence of many private banks. Imple-

mentation of the new banking law in 1989 resulted in actual and explicit privatisation of the sector

2

.

Emergence of “nine” commercial banks, although still with the dominating shares of the State Treasury,

allowed competitiveness to develop. On the one hand it was an occurrence which had been long expected

and by all means correct. However, the economic situation in the period of transformations showed that

majority of those banks had too low the capital of their own needed in the circumstances of deep market

changes and high economic risk. Hence, in the period from 1989 to 1997, the banking market was charac-

terised by little internal stability. Bank take-overs, liquidation or bankruptcies were frequent then

3

. In the

beginning the number of banks was growing, in the later period it gradually decreased. In the second

stage of privatization nine banks were privatized. It was carried out on the basis of 3 options:

consolidation option; – public offer option; – multi-stage option.

The consolidation option relied on joining the assets of several banks within a holding partnership and

then privatising it with the help of a foreign investor. This option was never used in practice.

The public offer option was carried out on the basis of the capital market. It was the most common practice.

In the case of the multi-stage option, three privatisation stages had been assumed. The first stage as-

sumed that banks would have a chance to negotiate a merger among themselves; the second one assumed

an offer of a minority interest in these banks to investors via public bidding; the third and the last one was

to be started if the previous ones had not been successful and it relied on transferring the shares of banks

not privatized within the Common Privatisation Programme to National Investment Funds

4

.

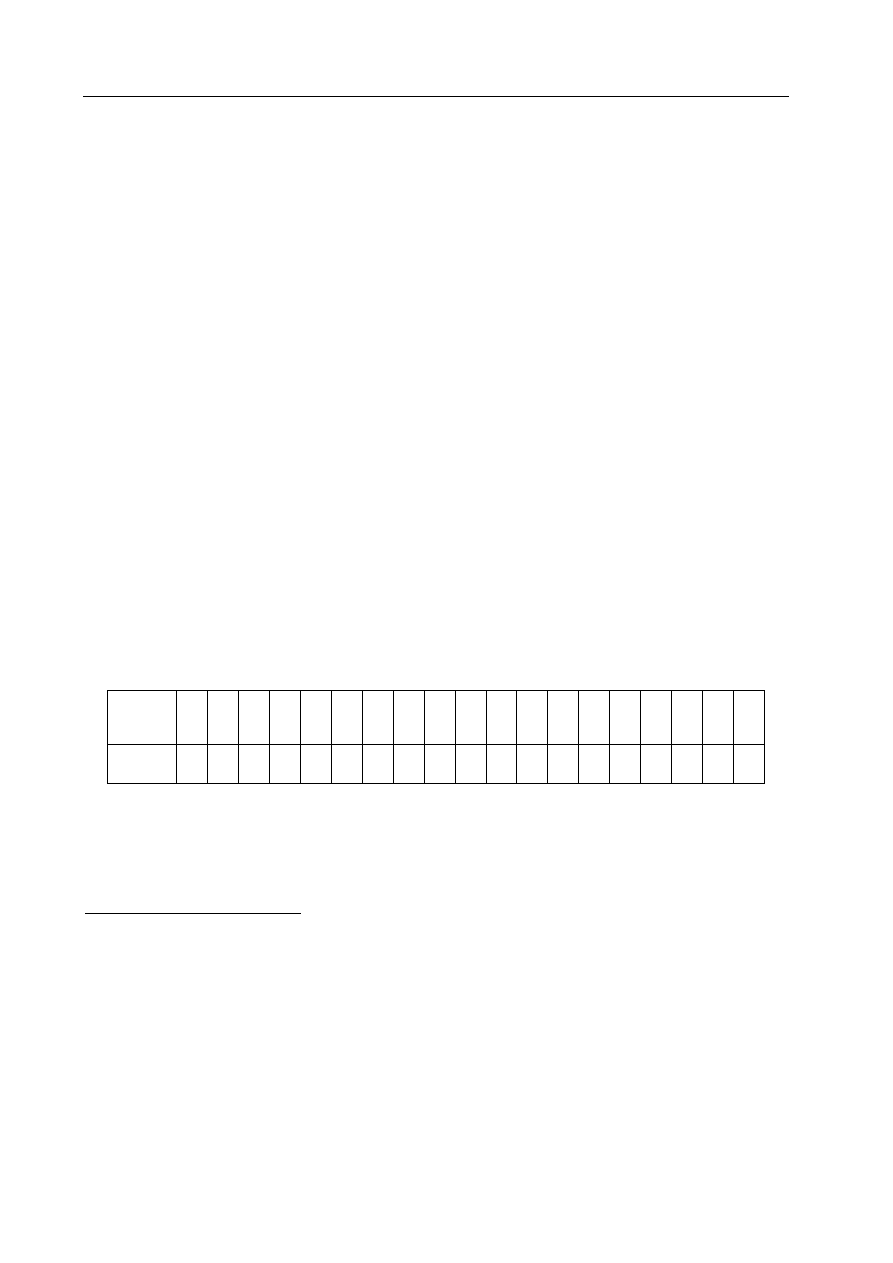

An analysis of the changes in the number of banks indicates that in the first period covered by the

analysis the number of banks rose whereas in later years this number declined gradually. Opponents of

the banking sector privatisation by creating new banks pointed out that the banking system was weakened

due to its fragmentation. Undercapitalised banks, having no market experience, contributed to a rise of

bad debts in the sector.

Table 1

Number of banks in Poland in the years 1991-2009 (operating at the end of September in a given year;

banks in bankruptcy or under liquidation are not included)

Year

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Number

of banks

78 82 87 82 81 81 81 83 77 73 69 59 58 57 61 63 51 52 51

Source: author’s own development on the basis of „Sytuacja finansowa banków w I kwartale 2006 roku” (Finan-

cial situation of banks in the 1st quarter of 2006); www.nbp.pl/Publikacje/nadzór-bankowy/pdf/synteza2006-3.pdf

and for the years of 2007-2009 „Informacja o sytuacji banków w okresie styczeń-wrzesień 2009 r.” (Information on

the situation of banks in the period between January and September 2009), Komisja Nadzoru Finansowego

http://www.knf.gov.pl/Images/Informacja%20o%20sytuacji%20bankow%202009.09_tcm20-14054.pdf

1

M. Pawłowska, Wpływ procesów konsolidacyjnych na poziom konkurencji i efektywność systemów bankowych –

wyniki badań ilościowych (Effect of consolidation processes on the banking sector competitiveness and effectiveness –

results of quantitative research) in: Konkurencyjność sektora bankowego po wejściu Polski do Unii Europejskiej

(Banking sector competitiveness following Poland’s EU accession), Zeszyt BRE Bank – CASE, No 76/2005, p. 25-47.

2

See: The Banking Law Act and the Act on the National Bank of Poland of 31 Dec. 1989in the Journal of Laws of

1989 N4. The consolidated text of both Acts was published in Dziennik Ustaw of 1992, No72 item. 359.

3

J. Majewska, Z doświadczeń restrukturyzacji banków w latach 80.i 90 (The experience of bank restructuring in the

1980s and 1990s),

http://www.nbportal.pl/library/-pub_auto_B_0100/KAT_B4844.PDF

4

See: A. Szelągowska, Znaczenie funduszu prywatyzacji banków polskich w procesie restrukturyzacji sektora

banków w Polsce (The significance of the Polish Bank Privatisation Fund in the banking sector restructuring in

Poland), Bank i Kredyt 6/2004, p. 74-77.

Фінанси

Зовнішня торгівля: економіка, фінанси, право. №2 2010

117

Still another method was basing privatisation of banks being joint-stock companies of the State

Treasury on the sale of share packages in the capital market via a public bid offer. This method proved

effective with reference to small banks. In the case of medium-sized and large banks, the problem of capi-

tal valuation turned out to be a barrier.

The last method of banking sector privatisation was to allow foreign private banks to enter the Polish

market in the capacity of strategic investors. Great hopes were cherished that they would help quick pri-

vatisation of small and medium-sized banks and solve the problem of undercapitalisation.

Conclusions

The financial crisis of the early 1990s in Poland was a serious threat to the developing banking system.

Adoption of a specific way of bad debt restructuring was of great significance for the future of the sector.

Lack of support might have made its further development difficult. Similarly, excessive support from the

state might have “demoralised” banks by freeing them from responsibility for their decisions. It can be

stated that to a great extent we owe sustainable high quality of bank credit portfolio in Poland to the re-

structuring programmes implemented in those days. Quality deterioration of this portfolio can be ac-

counted for by an economic downturn in the main markets but it does not threaten stability of the banking

sector and savings of depositors. Reaction of the latter to the worldwide financial crisis proves their high

trust for domestic banks.

Bibliography

1. Chałaczkiewicz M. Czynnik własnościowy a efektywność sektora bankowego. Część I – przegląd literatury

(Ownership factor and the banking sector effectiveness. Part I – literature review), Bank i Kredyt 9/2004, p.

18-19.

2. Chudzik R., Kryzys bankowy w gospodarkach postkomunistycznych na przykładzie Czech, Węgier i Polski

(Banking crisis in post- communist economies of the Czech Republic, Hungary and Poland), Bank i Kredyt

3/1996

3. Informacja o sytuacji banków w okresie styczeń-wrzesień 2009 r.(Information on the situation of banks in

the period between January and September 2009), Komisja Nadzoru Finansowego

http://www.knf.gov.pl/Images/Informacja%20o%20sytuacji%20bankow%202009.09_tcm20-14054.pdf

4. Kacprzyk A., Kryzys finansowy 2008-2009 – przesłanki, kontrowersje, perspektywy (Financial crisis 2008-

2009 – premises, controversies, prospects), in: J.L. Bednarczyk, S.I. Bukowski, J.Misala (ed.), Współczesny

kryzys gospodarczy: przyczyny, przebieg, skutki (Modern economic crisis: causes, course, effects), CeDeWu,

Warszawa 2009

5. Kawalec S., Polska droga restrukturyzacji złych kredytów (Polish way of bad credit restructuring), in:

Zeszyty PBR – CASE No 12/1994.

6. Majewska J., Z doświadczeń restrukturyzacji banków w latach 80.i 90 (The experience of bank restructuring

in the 1980s and 1990s), http://www.nbportal.pl/library/-pub_auto_B_0100/KAT_B4844.PDF

7. Mikita M., Nowa rola rynku finansowego w gospodarce światowej (A new role of the financial market in

world economy), in: J.L. Bednarczyk, S.I. Bukowski, J.Misala (ed.),Globalne rynki finansowe w dobie

kryzysu (Global financial markets in the time of crisis), CeDeWu, Warszawa 2009.

8. Ostałecka A., Kryzysy bankowe i metody ich przezwyciężania (Banking crises and the methods of overcom-

ing them), Difin, Warszawa 2009.

9. Pawłowska M., Wpływ procesów konsolidacyjnych na poziom konkurencji i efektywność systemów

bankowych – wyniki badań ilościowych (Effect of consolidation processes on the banking system competi-

tiveness and effectiveness – results of quantitative research), in: Konkurencyjność sektora bankowego po

wejściu Polski do Unii Europejskiej (Competitiveness of the banking sector following Poland’s EU acces-

sion), Zeszyt BRE Bank – CASE, No 76/2005.

10. Polska wobec światowego kryzysu gospodarczego (Poland and the worldwide economic crisis), Narodowy

Bank Polski, September 2009,

http://www.nbp.pl/home.aspx?f=/publikacje/polska_wobec_swiatowego_kryzysu_gospodarczego_2009/pols

ka_wobec_swiatowego_kryzysu_gospodarczego.html

11. Szelągowska A, Znaczenie funduszu prywatyzacji banków polskich w procesie restrukturyzacji sektora

banków w Polsce (The significance of the Polish Bank Privatisation Fund in the banking sector restructur-

ing in Poland), Bank i Kredyt 6/2004, p. 74-77.

Wyszukiwarka

Podobne podstrony:

123 To improve the quality of passing in a 5v5 or 6v6 ( GK)

121 To improve the quality of passing in a 3v3 or 4v4 ( GK

122 To improve the quality of passing in a 5v5 or 6v6 ( GK)

116 To improve the quality of passing in a 1v1 ( 2) practic

118 To improve the quality of passing in a 2v2 ( 2) practic

120 To improve the quality of passing in a 3v3 or 4v4 open

119 To improve the quality of passing in a 3v3 practice whe

Improve the quality of traditional education of calligraphy in Iran by implementing e learning

117 To improve the quality of passing in a 2v2 ( 2) practic

Improving the Quality of Automated DVD Subtitles

Robert F Young The Quality of Mercy

139 To improve the quality of the players shooting & finish

The Quality of Mercy Robert F Young

Approaches to improving the quality of dried fruit and vegetables

141 To improve the quality of the players shooting & finish

więcej podobnych podstron