Our cookie policy has changed. Review our cookies policy for more details and to change your cookie preference.

By continuing to browse this site you are agreeing to our use of cookies.

More from The Economist

My Subscription

In this section

Lucky lenders

Related topics

Aug 23rd 2014

|

SOPOT

|

Polish banks

Lucky lenders

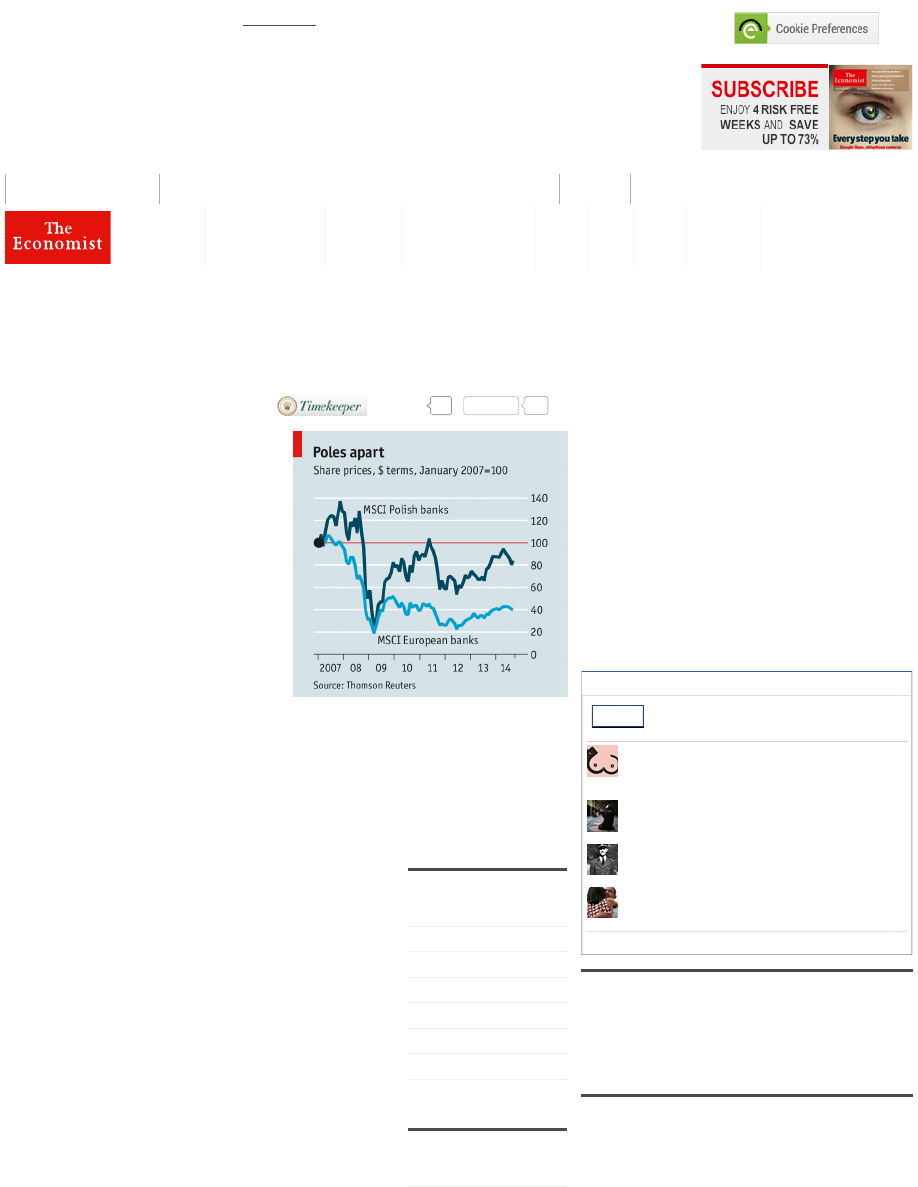

A healthy economy and modern offerings have boosted Poland’s banks

JUST as Poland’s economy and foreign-

policy clout have grown quietly but

significantly, so its banking system has

become one of Europe’s little-known star

performers. Poland’s young, technophile and

internationalised elite have worked out how

to make money as bankers to conservative

and traditionally borrowing-shy consumers.

Fortuitously, the business model they arrived

at has kept them away from the assets that

fared worst during the financial crisis.

Zbigniew Jagiello, the boss of PKO BP, the

country’s biggest bank, gives most of the

praise to the wider economy and to sensible public policy. Since his bank is partly state-

owned, he is being astute in offering credit to his biggest shareholder. But the state has also

benefited from the banks—directly in the form of steady dividends from PKO BP, and

indirectly from not having to bail out ailing lenders on the scale of so many other European

countries. “Happily, Poland was not the centre of the financial world,” as Mr Jagiello

delicately puts it.

Most of the rest of Poland’s banks are owned by foreign

parents: Bank Pekao is majority-owned by Italy’s UniCredit;

the third-biggest, Bank Zachodni WBK, by Santander of Spain.

Foreign ownership was useful in the crisis, as banks provided

liquidity to their small Polish subsidiaries. The parents were

well advised to help out; in some cases, the Polish bank has

been the most profitable bit of the group.

For example in 2013 mBank was one of the few star

performers among the operations of Commerzbank, a

German group. It was one of the first entrants into mobile

banking, winning plaudits for its digital efforts. It announced its

first billion-zloty quarter of revenue on July 30th, with net

profits of 325m zloty ($107m), despite low interest rates

hobbling the entire sector.

Advertisement

Follow The Economist

Log In

Recent Activity

Log in to Facebook to see what your friends

are doing.

Why does liberal Iceland want to ban online

pornography?

942 people recommend this.

847 people recommend this.

524 people recommend this.

1,034 people recommend this.

Facebook censorship: Arbitrary and capricious

63

Like

Though boring in their investing and lending, Poland’s banks

are innovative in service. Because the country built its banking system essentially from

scratch, it was never hampered by legacy practices such as paper cheques. Poland is the

European leader in contactless payments. Alior, another young bank (and one of the few

without a majority foreign partner) has targeted some of Poland’s rural “unbanked” (30% or

so of the population do not have a bank account). Alior’s “Kill Bill” campaign promised free

and easy payment of utility bills, and signed up many customers for accounts and loans.

Idea, a rival, asks potential small-business customers for the passwords to their existing

online-banking facilities; after a quick scan of their past transactions it instantly makes a loan

offer.

Factors beyond the control of bankers also helped. Poles did not over-extend themselves

with mortgages, as many other Europeans had, and so took less of a shock when the crisis

hit. One problem was that, like some other central and eastern Europeans, many Poles took

out property loans in Swiss francs and saw their payments balloon as the zloty weakened

against the franc. But the regulators demanded stricter credit criteria for such loans, limiting

the damage the (now-banned) practice did to the economy. A sudden further weakening of

the zloty, or sharply higher interest rates in Switzerland, are among the few potentially big

risks to the banking system, says Pawel Uszko of SNL Financial, a business-intelligence

firm.

But SNL’s underlying numbers show Poland’s banks in good shape. By international

standards, the loans extended to customers are backed by plenty of equity, meaning the

banks have buffers to weather a medium-sized storm. Their costs are under control. And

with a return on equity of 10.9% in 2013, they compare favourably with almost all

neighbours, east or west.

From the print edition: Finance and economics

31

0

More from The Economist

Prostitution: A personal

choice

Capsule hotels at

airports: Sleep tight

Reclining aeroplane

seats: A laid back

approach

The Economist explains: How the

Islamic State is faring since it declared a

caliphate

The Economist explains: Why China

and Taiwan are divided

Prostitution and the internet: More

bang for your buck

New film: "Sin City: A Dame to Kill for":

Lacking in substance

Farming in the Netherlands: Polder

and wiser

Commented

Most popular

Democracy in America | 1 hour 28 mins ago

The Economist explains: How dictionary-

makers decide which words to...

The Economist explains | Aug 27th, 23:50

Nigeria and its jihadists: The great

escape

Baobab | Aug 27th, 21:12

Photography: The making of Dorothea

Lange

Prospero | Aug 27th, 16:07

Gulliver | Aug 27th, 16:05

Poland and Germany: Disagreements

over the EU's Ostpolitik

Eastern approaches | Aug 27th, 15:37

Difference engine: Divining reality from

the hype

Babbage | Aug 27th, 15:13

China: What China wants

Race relations in America: The lessons of

Ferguson

Ukraine's rebels: Bloodied but unbowed

Oceans and the climate: Davy Jones’s heat

locker

63

Like

Want more? Subscribe to The Economist and get the week's most

relevant news and analysis.

Products and events

Have you listened to The Economist Radio on

Facebook?

The Economist Radio is an on-demand social

listening platform that allows you to listen, share and

recommend The Economist audio content

Take our weekly news quiz to stay on top of the

headlines

Try our new audio app and website, providing

reporting and analysis from our correspondents

around the world every weekday

Visit The Economist e-store and you’ll find a range

of carefully selected products for business and

pleasure, Economist books and diaries, and much

more

Sponsor Content

Advertisement

Best for Savings, Cds, and MMAs. Listed in a chart

just for you!

Free Introduction to Latin Women. Unlimited Love

Notes + 20 Letters!

Trade Horizons delivered by UPS

A daily look at the innovations transforming

global business

Next in Finance and economics

X

New financial instruments may help to make pension schemes safer

Copyright © The Economist Newspaper Limited 2014. All rights reserved.

Classified ads

Jobs.economist.com

Jobs.economist.com

Jobs.economist.com

Jobs.economist.com

Sections

Debate and discussion

Blogs

Research and insights

United States

Britain

Europe

China

Asia

Americas

Middle East & Africa

Business & finance

Economics

Markets & data

Science & technology

Culture

Multimedia library

The Economist debates

What the world thinks

Letters to the editor

The Economist Quiz

Americas view

Analects

Babbage

Banyan

Baobab

Blighty

Buttonwood's notebook

Charlemagne

Democracy in America

Eastern approaches

Erasmus

Feast and famine

Free exchange

Game theory

Graphic detail

Gulliver

Newsbook

Pomegranate

Prospero

Schumpeter

The Economist explains

Topics

Economics A-Z

Special reports

Style guide

The World in 2014

Which MBA?

The Economist GMAT Tutor

Reprints and permissions

The Economist Intelligence Unit

The Economist Intelligence Unit

Store

The Economist Corporate Network

Ideas People Media

Intelligent Life

Roll Call

CQ

EuroFinance

The Economist Store

Wyszukiwarka

Podobne podstrony:

pobłocki the economics of nostalgia

[Mises org]Mises,Ludwig von The Causes of The Economic Crisis And Other Essays Before And Aft

Polish Firms Come in After the Kill

Good Capitalism, Bad Capitalism, and the Economics of Growth and Prosperity

Guide to Financial Markets The Economist

Economides Wilson The Economic Factor in International Relations

Barbara Stallings, Wilson Peres Growth, Employment, and Equity; The Impact of the Economic Reforms

Sociology The Economy Of Power An Analytical Reading Of Michel Foucault I Al Amoudi

History of the U S Economy in the 20th Century

Prognoza Rothschildów w The Economist na 2019 rok Wariant z odszyfrowywaniem

Isaac Asimov Lucky Starr 06 Lucky Starr and the Rings of Saturn

Text which I chose is strongly connected with the economy and conditions on the market

Who killed the death penalty The Economist

Most favoured nation The Economist

Lucky Starr and the Pirates of Isaac Asimov

The economics of short rotation coppice in Germany 2012

Ritter Investment Banking and Securities Insurance (Handbook of the Economics of Finance)(1)

The Economic System of Islam

Vinay B Kothari Executive Greed, Examining Business Failures that Contributed to the Economic Crisi

więcej podobnych podstron