Determining capital needs

2

Learning objective

1. What is financial plan?

2. The financial planning model

3. The percentage of sales approach

– Internal growth rate

– Sustainable growth rate

4. Pros and cons of different planning

tools

3

The basic policy elements of

financial planning

• The firms needed investment in

new assets (aggregation process of

new investments).

• The degree of financial leverage

the firm chooses to employ.

• The amount of cash is necessary to

pay shareholders (shareholders

return).

• The amount of liquidity and

working capital the firm needs on

ongoing basis.

The principal components of

the financial plan

1. An analysis of the firm’s current

financial condition

2. The capital budget

3. The cash budget

4. A set of projected financial

statements

5. The external financing plan

4

5

Long-term and short-term

financial plans

• Short-term plans helps to analyse

decisions which effects could be measured

in coming 12 months. Those decisions

usually affects liquid assets and current

liabilities. The purpose of short-term plan

is to anticipate future shortage or surplus

of cash.

• The planning horizon for a long-term plan

is two to five years. The plan focuses

primarily on financing and investment

decisions which increase the market value

of equity. It takes the form of a financial

statement, which allows further value-

orientated modifications.

The financial planning process in long-

term perspective

• The financial planning process can be

broken down into five steps:

1. Set up the system of projected

financial statements.

2. Determine the specific financial

requirements.

3. Forecast the financial resources to be

used.

4. Establish and maintain the systems of

controls.

5. Develop procedures for adjusting the

basic plan.

6

7

Percentage of sales

approach

Defininition. Financial planning method

in which accounts are varied depending

on a firm’s predicted sales level.

1. Some components of a balance sheet

change in proportion with sales. Those

components are called spontaneous or

automatic.

2. The level of those components are

optimal. If not, they will change with

sales after they reach their optimal level.

3. Firm acquire internal source of capital

first than external sources of capital

(debt and new equity).

8

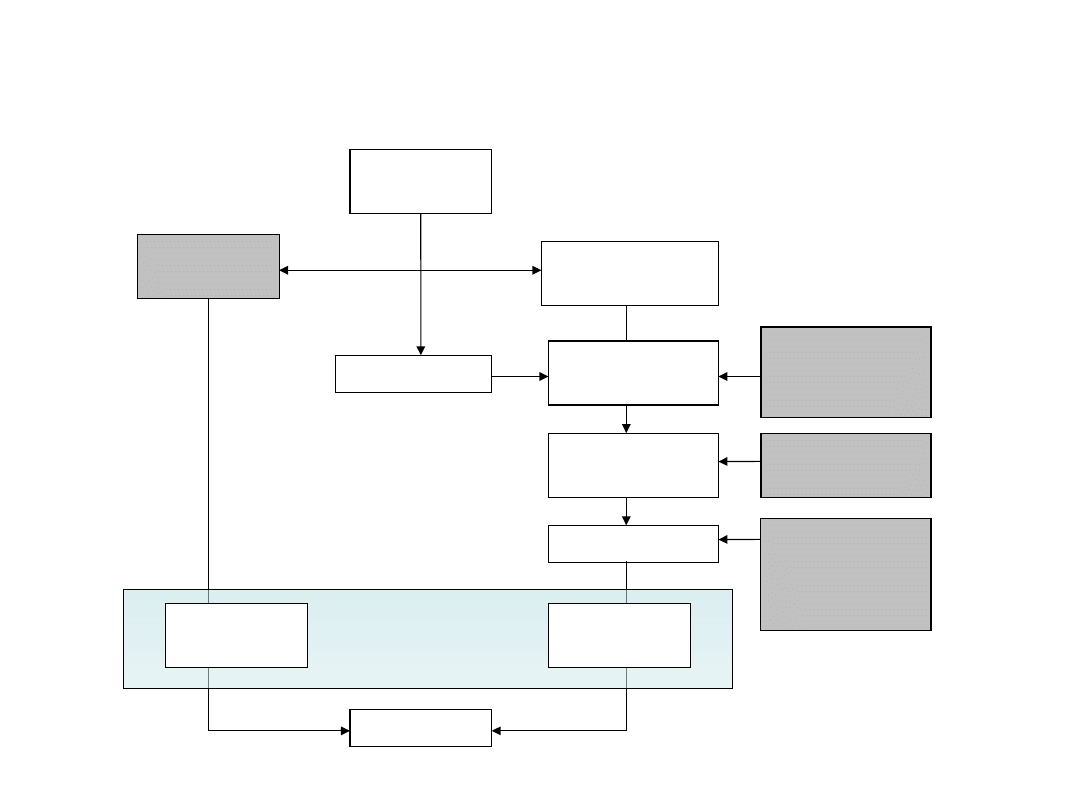

The set up of financial

statementns- financial planning

model

Sales

growth

Asset

growth

Net income

Total

assets

Retained

earnings

New equity

New debt

Balance

sheet

Dividend

payout

ratio

Stock issue

Debt ratio,

Coverage

ratio

Sources of

capital

Total

liabilities

9

Two steps of calculation – the

proportional approximation

On this step of calculation:

• Automatic components change with sales.

• Usually, an increase in assets is greater

then increase in liabilities.

• The difference between the change in

assets and liabilities is reduced by an

capital acquired from internal sources of

capital (retained earnings).

10

External Financing

Requirements (EFR)

• Proportional approximation is

described by following equation:

A* - authomatic assets

S – Sales

∆S – change in sales

L* - authomatic liabilities

NI – net income

b – retention ratio

1

0

0

0

0

0

0

*

*

bS

S

NI

S

S

L

S

S

A

EFR

Internal Growth Rate (g)

–

how much company can

grow

without the need for external

non- authomatic funds

11

Return on

Assets (ROA)

is a popular

profitability

ratio

0

)

1

(

0

*

0

0

g

b

NI

g

L

g

A

EFR

b

NI

g

L

A

1

*

0

0

ROA

b

*

0

0

1

L

A

NI

b

g

Sustainable growth rate

– assets growth will be

financed

with retained earnings and

proportional increase of debt

12

Return on Equity

(ROE) is popular

profitability ratio

0

1

)

1

(

0

0

0

*

0

0

E

D

g

b

NI

g

L

g

A

0

*

0

0

1

*

0

0

E

L

A

b

NI

g

L

A

ROE

b

0

1

E

NI

b

g

13

Second step of calculation –

the financial approximation

• On this step some indispensable

information are required:

– Liquid assets management policy,

– How company will be financed?,

– Dividend policy,

• Once the source of capital is

selected an iteration process take

place in order to take into account

the interaction between P&L

statement and balance sheet.

14

Transaction costs

• For new debt:

– Provisions,

– Handling charges,

– Costs of business plan preparation,

– Interests

• For new equity:

– Brokerage expenses (incl. provisions),

– Discounts for subscribers,

– Costs of business plan preparation,

– Cost of prospectus preparation.

The problems with the

percentage of sales

approach

1. Economics of scale

2. Lumpy assets

3. Cyclical and seasonal changes

15

Constant turnover ratios –

the base case

16

Constant

turnover

ratios

Inventor

y

Sales

100 % increase

100%

increase

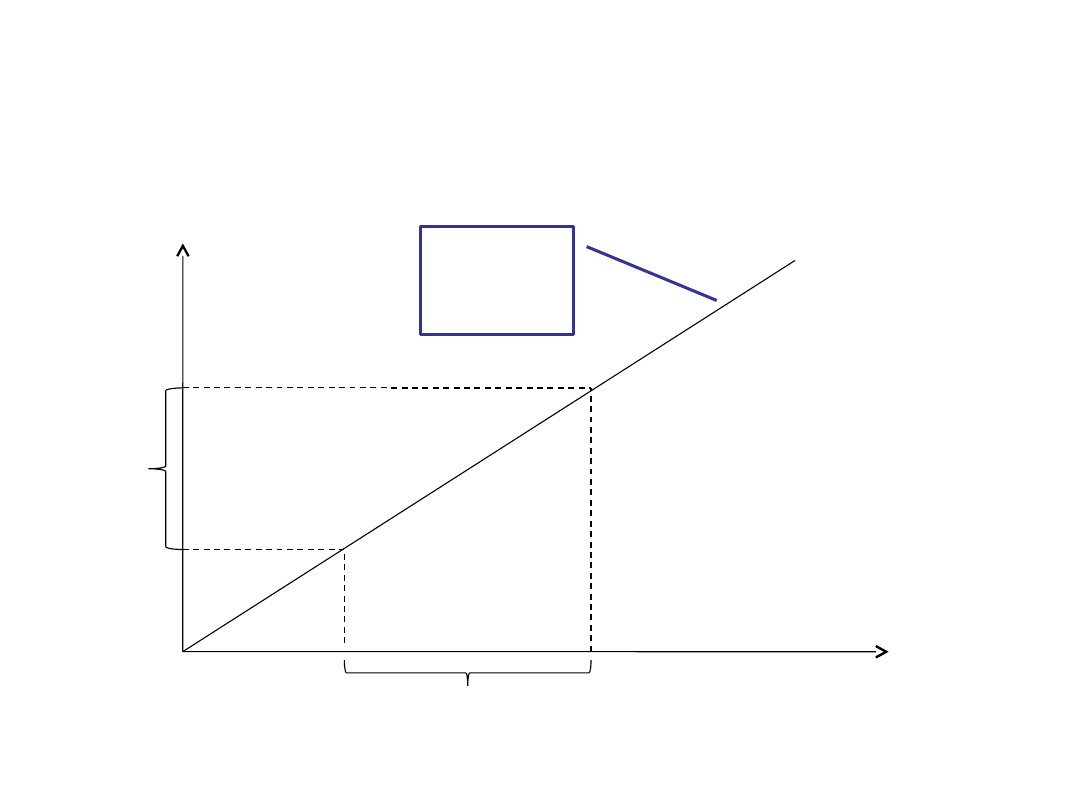

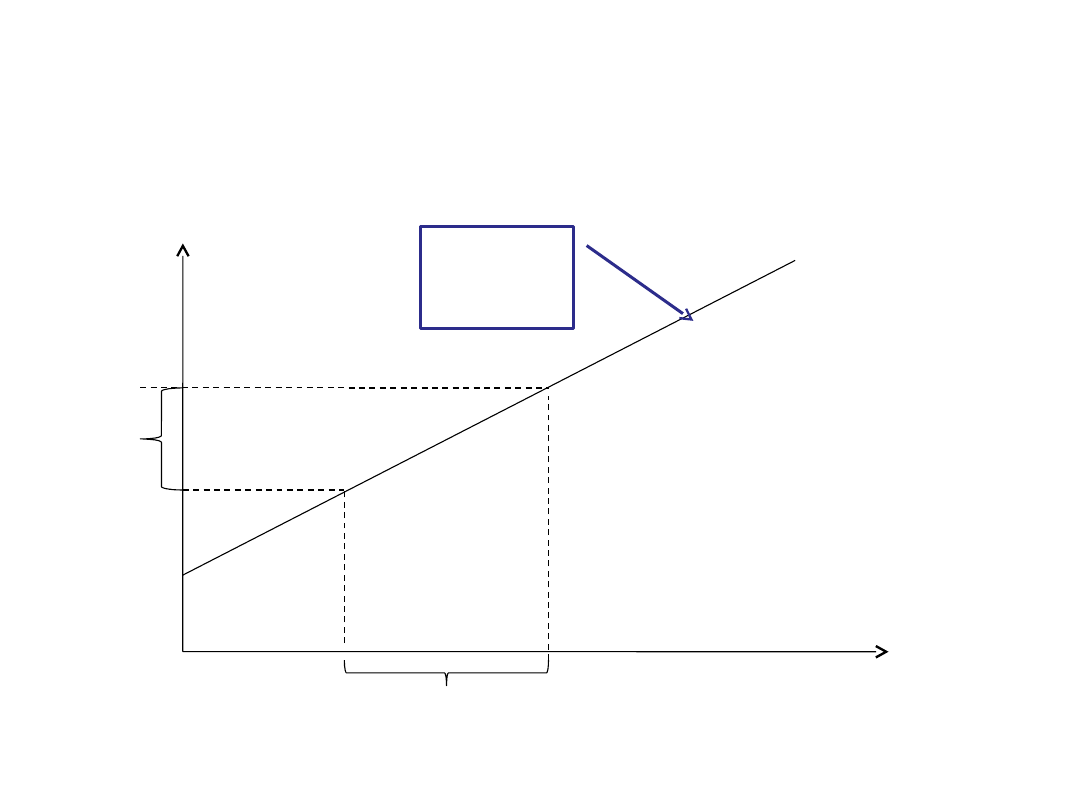

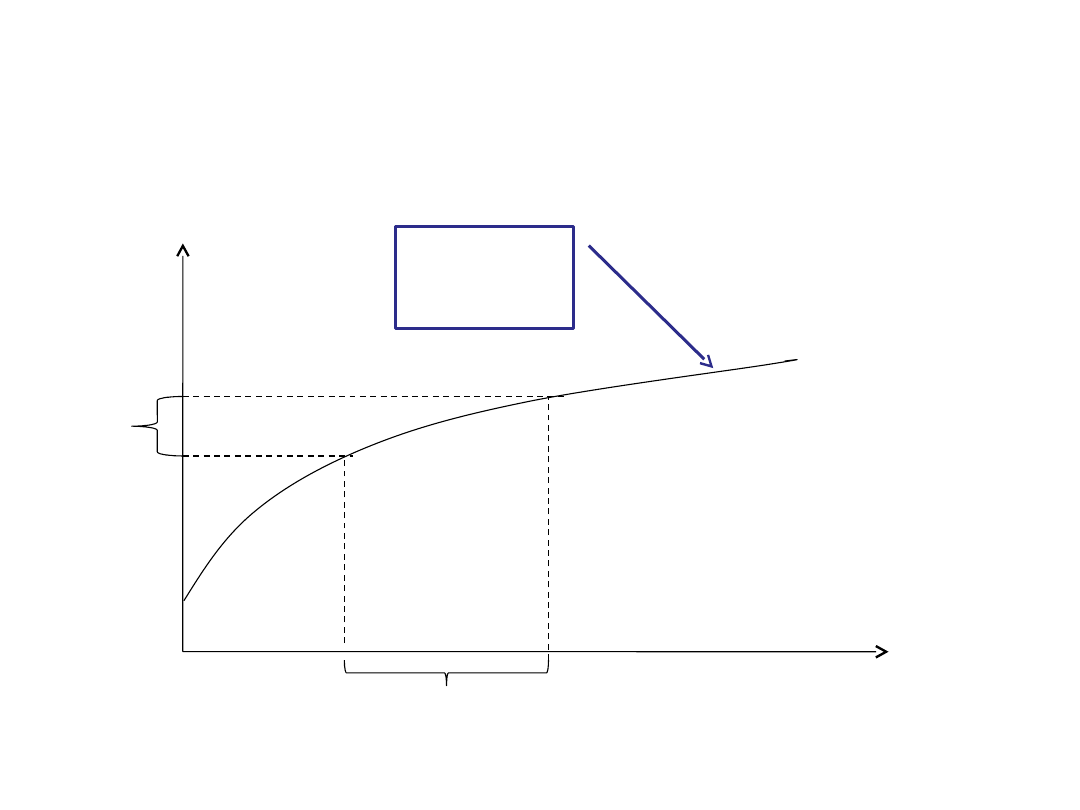

The economy of scale

17

• The turnover ratios (like sales-to-

inventory) are likely to change over

time as the size of the firm increases.

As a result:

– Linear relationship remains but the

turnover ratio is different

– Change in assets is represented by

curvilinear relationship

Example 1 continiued.

The economy of scale

(linear relationship)

18

Turnover

ratio

changes

Inventor

y

Sales

100 % increase

25%

increase

The economy of scale

(curvilinear relationship)

19

Curvilinear

relationshi

p

Inventor

y

Sales

100 % increase

10%

increase

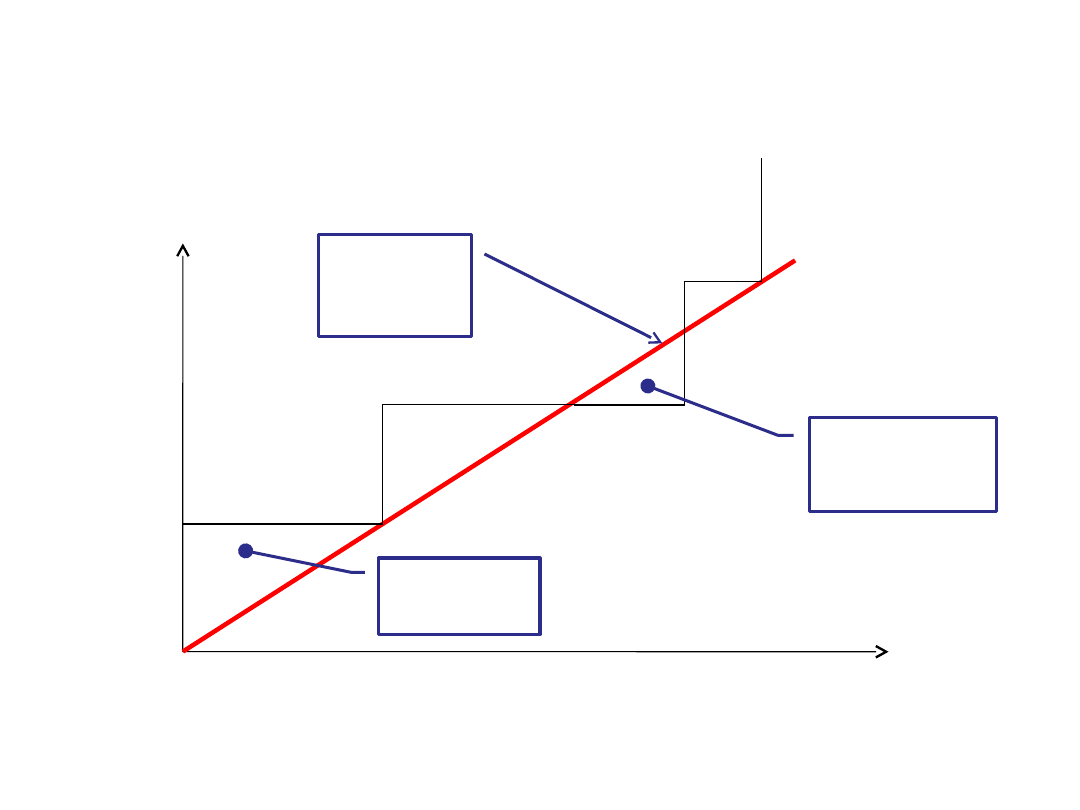

Lumpy assets – assets

increase in large, discrete

units

20

Required

capacity

Fixed

Assets

Sales

Excessive

capacity

The

shortage of

capacity

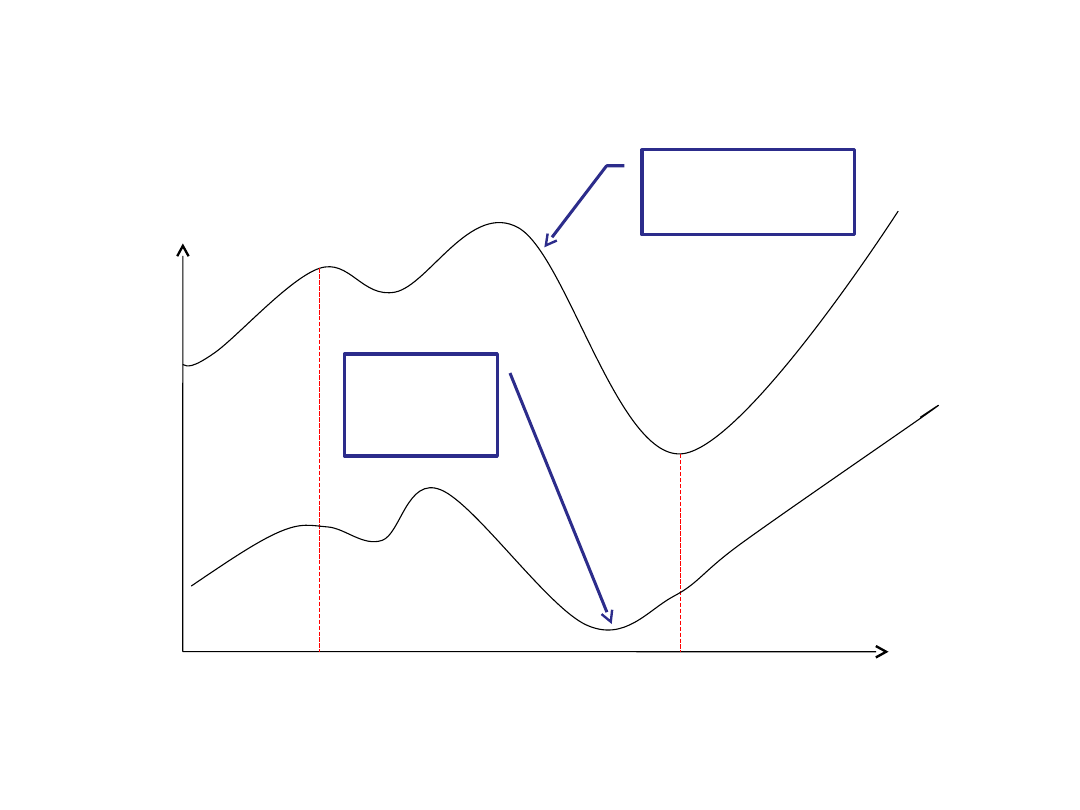

Cyclical and seasonal

changes

21

Average

daily

sales

Receivables

,

Sales

Time

(months)

Receivables

Long Average

Collection Period

(ACP)

Short ACP

22

Pro forma P&L statement and

balance sheet – the pros

• Determines a future capital

requirements and helps to select

the source of capital.

• An iteration process gives exact

amounts of future capital

requirements.

• It is a good starting-point for a

detailed financial analysis.

23

Pro forma P&L statement and

balance sheet – the cons

• A preparation of detailed pro forma

statements is expensive (time and

money consuming).

• Draw a picture the financial status quo

in a one particular day.

• Results will change as new information

will enter the planning model.

• To reduce the effect of impermanence of

results, the planning period:

– The shorten the planning horizon to desirable

minimum (a quarter for example)

– Should be adjusted not to calendar periods but to

terms like: before season, dead season, in season,

etcetera.

The cash budget

• Cash budget is a financial budget

prepared to calculate the budgeted

cash inflows and outflows during a

period and the budgeted cash

balance at the end of the period.

• Cash budget helps the managers to

determine any excessive idle cash or

cash shortage that is expected

during the period. Such information

helps the managers to plan

accordingly.

24

25

Cash budget – the pros

• It deals only with receipts and

disbursements

• It allows to determine cash

requirements as a part of a cash

management process

• excellent tool for short-term planning

and cash management

26

Cash budget – the cons

The disadvantages of cash budget

are:

• The structure of inflows and

outflows has no common

standard

• The sources of deficit financing

are not specified

• The iteration process is difficult

to implement.

Document Outline

- Slide 1

- Learning objective

- The basic policy elements of financial planning

- The principal components of the financial plan

- Long-term and short-term financial plans

- The financial planning process in long-term perspective

- Percentage of sales approach

- The set up of financial statementns- financial planning model

- Two steps of calculation – the proportional approximation

- External Financing Requirements (EFR)

- Slide 11

- Slide 12

- Second step of calculation – the financial approximation

- Transaction costs

- The problems with the percentage of sales approach

- Constant turnover ratios – the base case

- The economy of scale

- Slide 18

- The economy of scale (curvilinear relationship)

- Lumpy assets – assets increase in large, discrete units

- Cyclical and seasonal changes

- Pro forma P&L statement and balance sheet – the pros

- Pro forma P&L statement and balance sheet – the cons

- The cash budget

- Cash budget – the pros

- Cash budget – the cons

Wyszukiwarka

Podobne podstrony:

Financial planning problems

Everyone S Guide To Financial Planning

Financial Institutions and Econ Nieznany

Financial Freedom

BANK organization przybysz, 03 banking & finance

financial market poprawka egzamin

Finance and?nking

Aftershock Protect Yourself and Profit in the Next Global Financial Meltdown

Principles Of Corporate Finance

Financial Times Coach yourself to optimum emotional intelligence

Great Architects of International Finance Endres 2005

Corporate finance 03

Strategic Finance 6

http, www vbm edu pl UserFiles vbm File art e finance 02 09 08

finance glossary, 03 banking & finance

więcej podobnych podstron