Course name: Corporate Finance

Textbook: Ross, Westerfield, Corporate Finance; Brealey, Myers: Principles of Corporate Finance

Objective: To provide students with knowledge of the fundamentals of modern corporate finance

theory and practice with an emphasis on value creation.

The course structure: The course consists of 30hrs of lectures plus 15hrs of workshops; workshops

will be case-driven with materials available for home study before the workshops; each course

participant will have opportunity to prepare a presentation based on any financial press article

(Financial Times, Wall Street Journal etc.) with the task to identify any relevant link to the course

material.

The course topics:

1. Introduction to corporate finance; firm’s objectives; owners vs. other stakeholders; operating

vs. financial activities.

2. Financial statements: balance sheet, profit and loss account, cash flow statements;

3. Managerial financial statements; invested capital; net operating profit after tax; interest tax

saving.

4. Annual financial performance evaluation; return on invested capital (ROIC, ROCE); Dupont

analysis, ratio analysis.

5. Working capital management; liquidity vs. capital requirement; working capital financing

strategies.

6. Time value of money; nominal vs. real interest rates; simple and compound interest; present

and future values; annuity.

7. Bond valuation; types of debt financing; yield to maturity; credit rating; bond price

determinants.

8. Equity valuation; EPS; DPS; retention and payout ratios; dividend discount models; PER

valuation.

9. Enterprise valuation; free cash flows; cost of capital; real options.

10. Investment appraisal; incremental cash flows; NPV rule; project’s rate of return rule; ARR;

profitability index.

11. Internal rate of return; IRR vs. NPV; other investment appraisal methods; taxation and

inflation; capital rationing.

12. Risk-return trade off; decision trees; sensitivity and simulation; portfolio theory; CAPM.

13. Weighted average cost of capital (WACC); operating vs. financial leverage; ROE and ROIC vs.

financial leverage.

14. Cost of capital vs. enterprise value; Miller-Modigliani models.

About instructor

Tomasz Berent, PhD in Finance and MA in Banking and Finance from University of Wales, UK; MA in

Economics from Warsaw School of Economics (WSE), Poland.

Lectures in finance and investment at WSE – Top 10 WSE Lecturer; faculty member in prestigious

international postgraduate programmes: e.g. CEMS MIM in cooperation with some 30 leading

institutions worldwide; Warsaw Executive MBA (in co-operation with University of Minnesota, US) –

Outstanding WEMBA Faculty Awards every year since the Award was launched; Executive Studies in

Finance (in co-operation with Ernst and Young). Also lectured in the UK at University of Wales (1992-

1995), University of Bangor (2009), and University of Sussex (2010).

An advisor/expert to Polish Financial Supervision Authority; professional experience includes

executive positions in investment banking sector (incl. Chief Strategist for Emerging Markets at BNP

Paribas in London, Head of Research at Investment Bank Austria in Warsaw); over 100 equity reports

(in English) on valuation and sector analysis on Polish and other Emerging Markets companies.

Dr Tomasz Berent

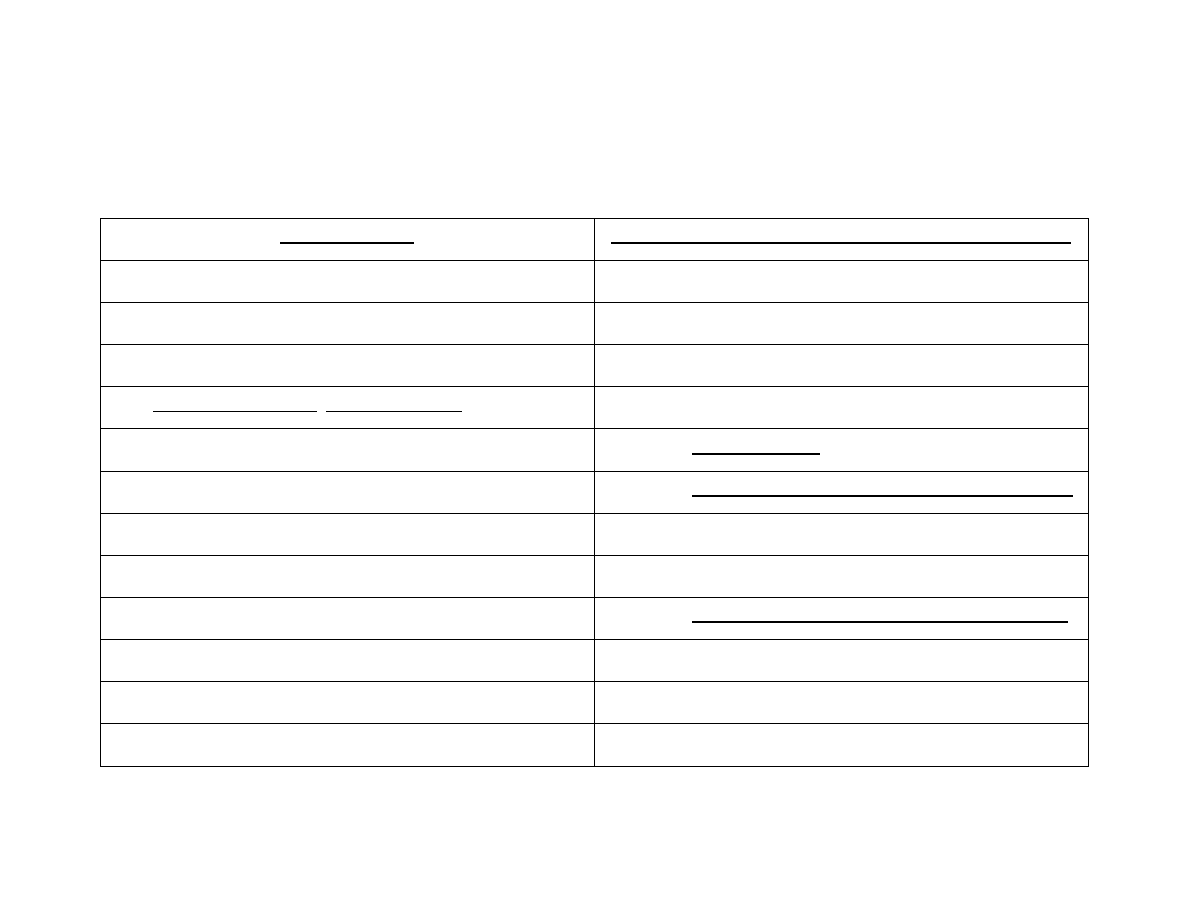

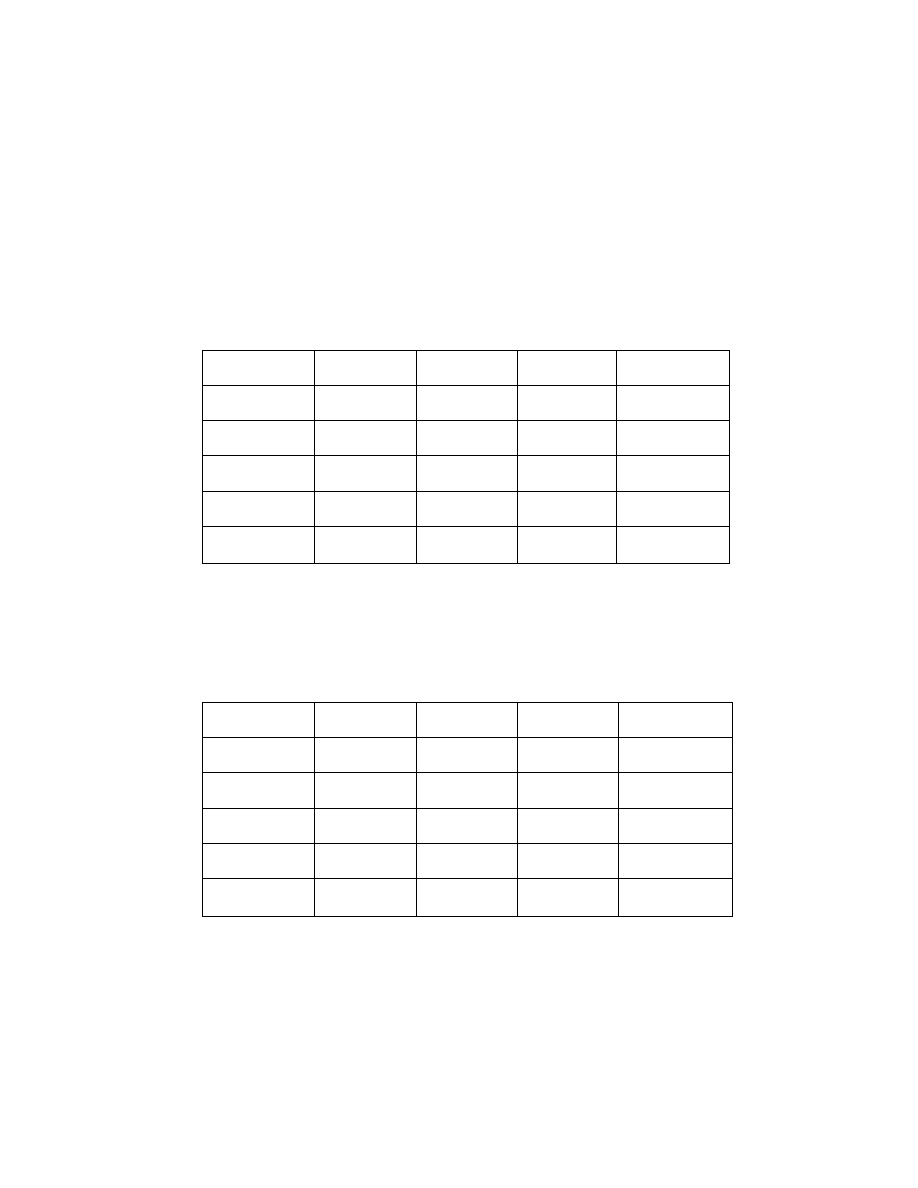

GAAP BALANCE SHEET

ASSETS

EQUITY AND LIABILITIES

Current assets

Liabilities

Cash

Short-term liabilities

Marketable securities

Short-term debt

Receivables

Payables

Inventories

Other short term liabilities

Other current assets

Long-term liabilities

Fixed assets

Long-term debt

Intangible

Other long-term liabilities

Tangible

Owners’ equity

Investments

Common equity

Other fixed assets

Preferred stock

Dr Tomasz Berent

CURRENT ASSETS

Cash

Cash equivalents (marketable securities, e.g. T-bills, CPs)

Accounts receivable

(receivables, trade receivables, debtors, trade debtors)

Inventories

o Raw materials

o Work in process

o Finished goods

Other current assets (e.g. prepaid expenses)

Dr Tomasz Berent

FIXED ASSETS

Intangible assets (e.g. patents, trademarks, goodwill)

Tangible assets

o Property

o Plant

o Equipment

Investments (e.g. real estate, financial assets)

Dr Tomasz Berent

LIABILITIES

Short-term (current) liabilities

o Short-term debt

(e.g. overdrafts, line of credit, promissory notes)

o Accounts payable

(payables, trade payables, creditors, trade creditors)

o Other short-term liabilities

(e.g. accrued expenses such as wage, taxes, Social Security)

Long-term (noncurrent) liabilities

o Long-term debt

o Other long-term liabilities

(e.g. deferred taxes, pension liabilities)

Dr Tomasz Berent

STOCKHOLDERS’ (OWNERS’) EQUITY

Common equity

o Paid-in capital

Common stock at par value

Capital surplus

o Accumulated retained earnings

Preferred stock

Dr Tomasz Berent

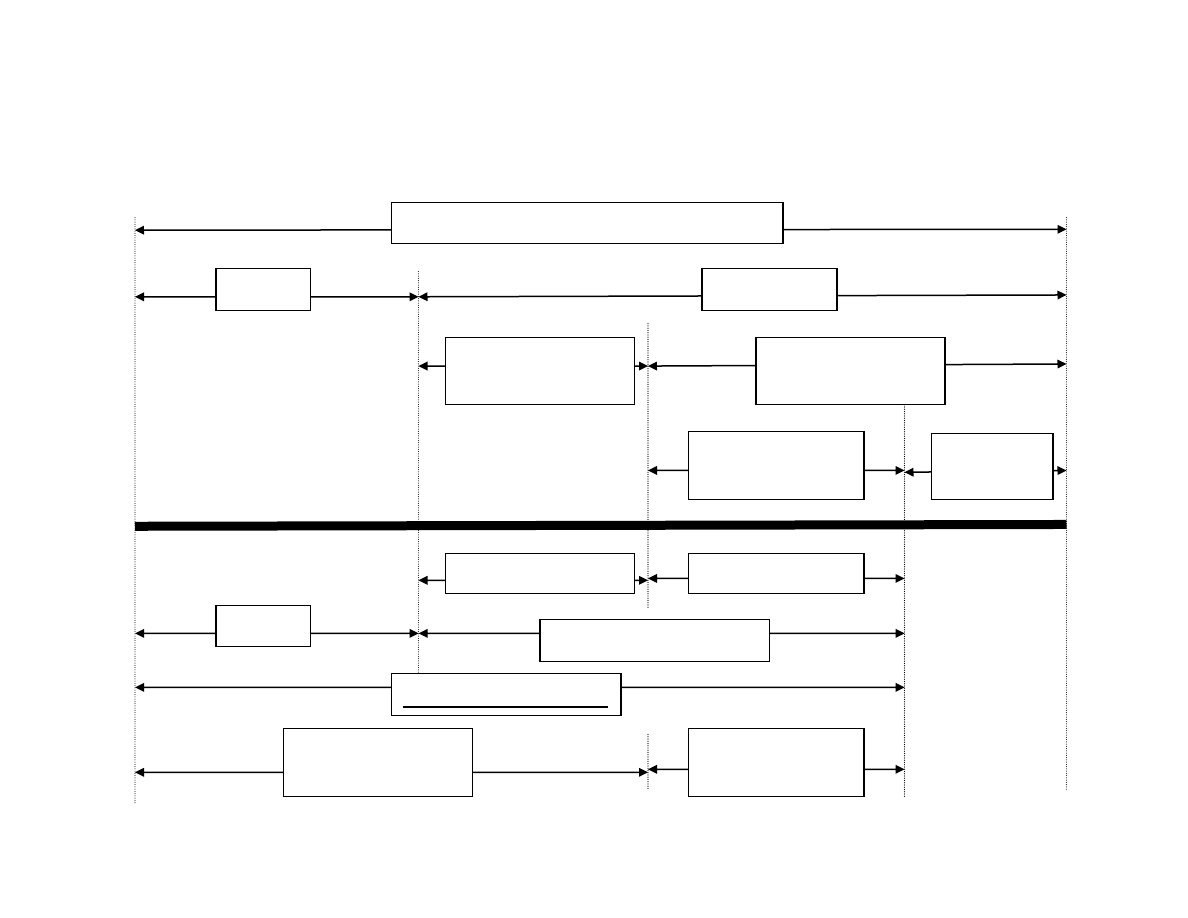

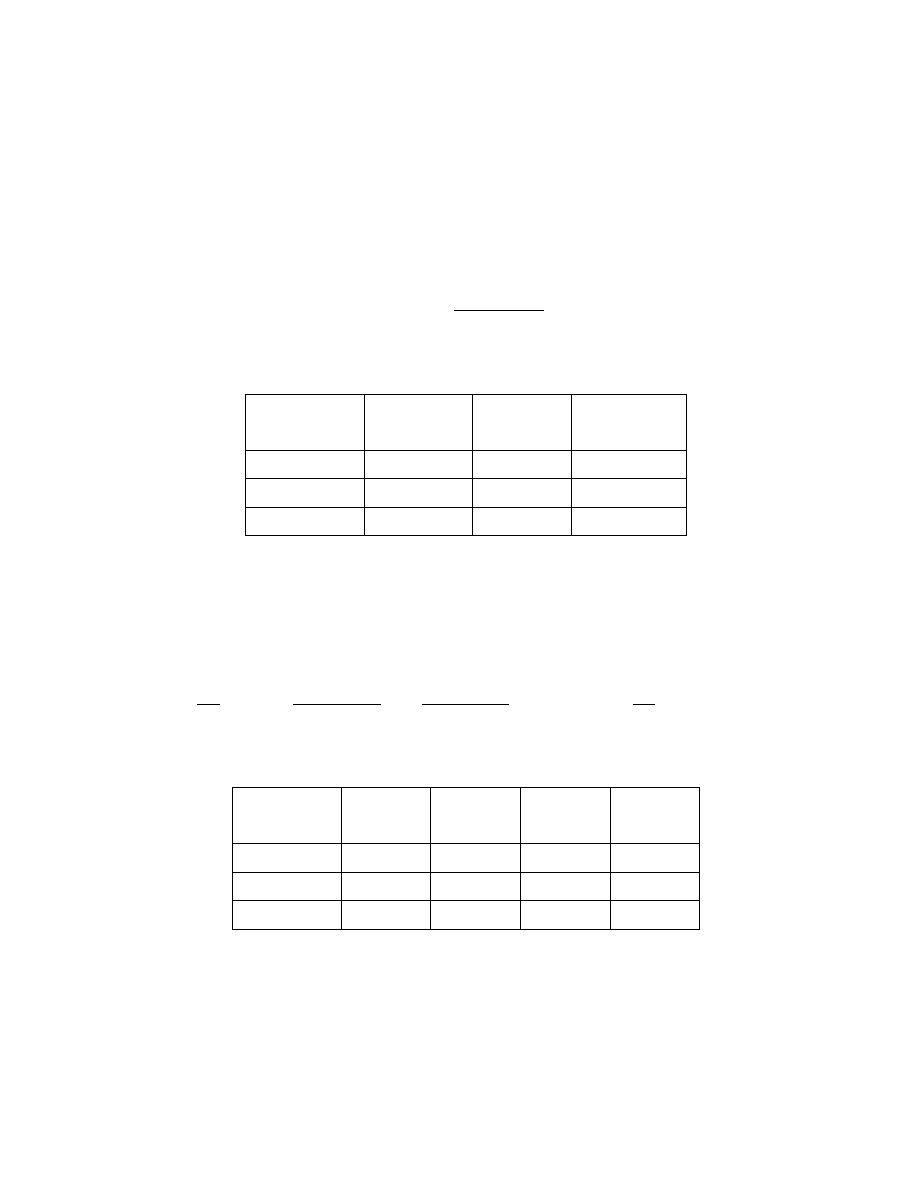

LIABILITIES AND STOCKHOLDERS’ EQUITY

Equity

Liabilities

Liabilities and stockholders’ equity

Long-term

liabilities*

Long-term

financing

Short-term

liabilities

Short-term debt

Debt

Capital employed**

*We assume l

ong-term liabilities=long-term debt

**This will later be adjusted for surplus cash

Long-term debt

Short-term

financing

Equity

Interest bearing

liabilities

Other s-t

liabilities

Dr Tomasz Berent

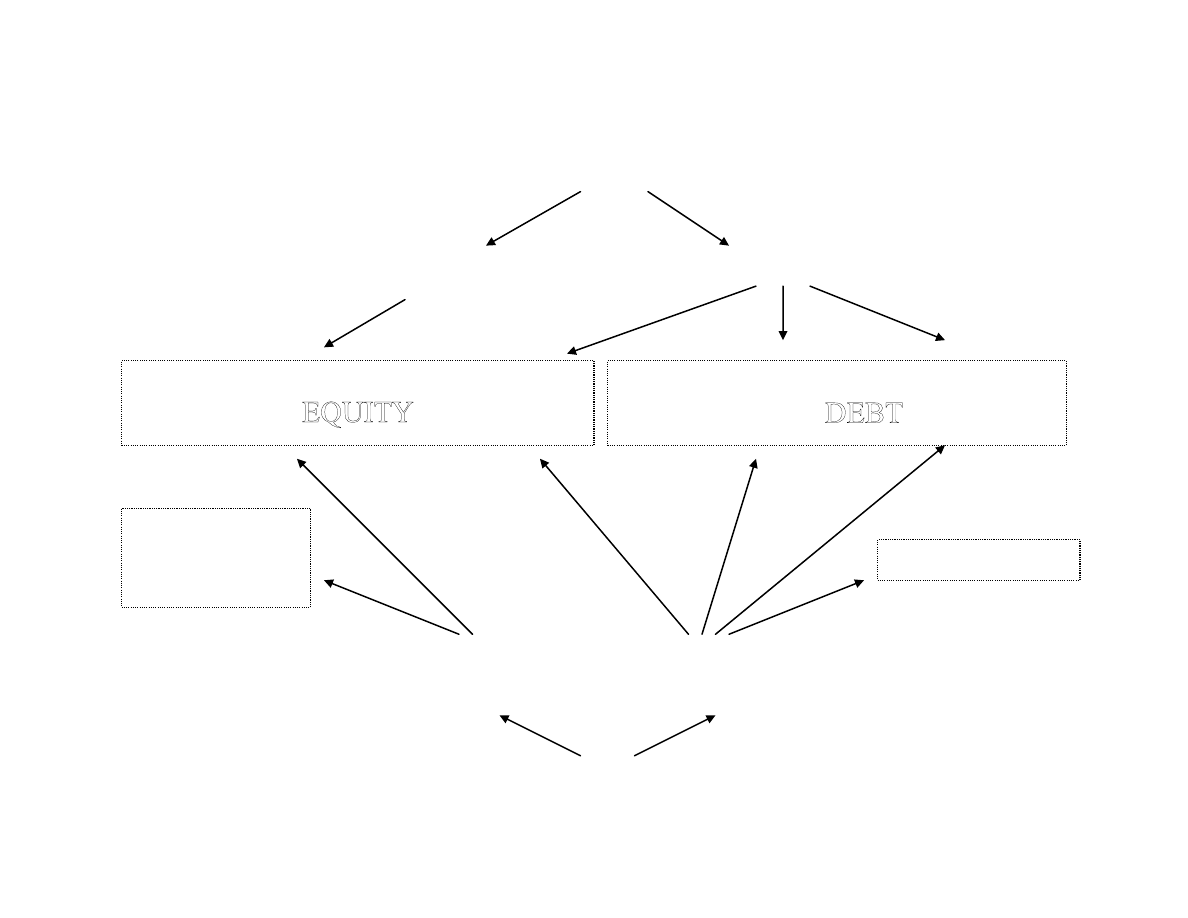

SOURCES OF CAPITAL

Internal

External

Bond issue

Bank loan

D

D

E

E

B

B

T

T

Retained earnings

New equity issue

E

E

Q

Q

U

U

I

I

T

T

Y

Y

SOURCES OF CASH

Internal

External

Depreciation

Cash surplus

Asset sale

Payables

Dr Tomasz Berent

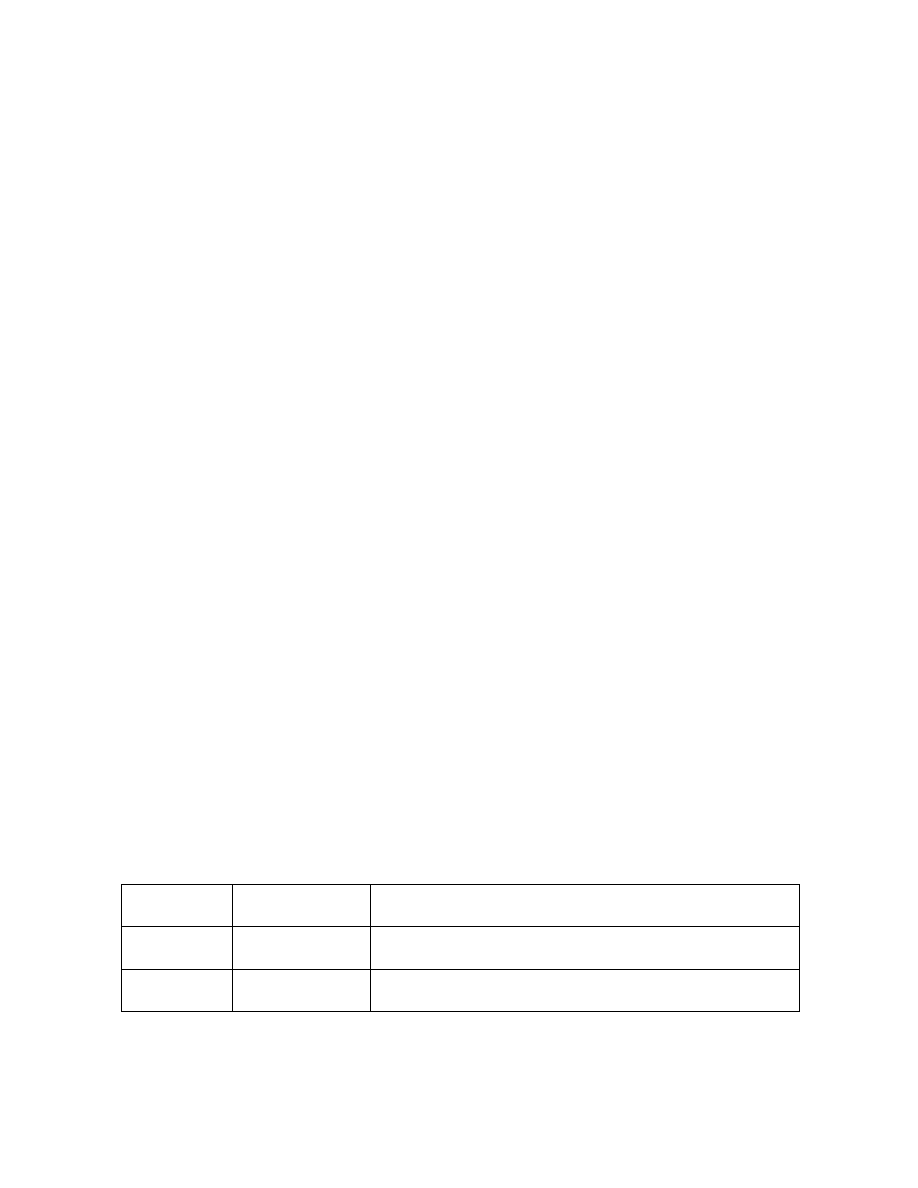

INCOME STATEMENT

Sales (revenue, turnover)

– Cost of goods sold (COGS, e.g. materials, wages, depreciation)

Gross profit

– Selling, general and administrative expenses (SG&A)

+/–

Other operating income/ cost

Net operating profit (NOP,

Earnings before interest and taxes,

EBIT)

– Net interest expense

Pre-tax profit

– Income tax expense

Net income (net profit, bottom line)

–

Dividends

Retained earnings

Dr Tomasz Berent

THE STATEMENT OF CASH FLOWS

Cash flows from operating activities

o Cash operating earnings

o Change in working capital

Cash flows from investing activities

o CAPEX & acquisitions

o Sale of fixed assets

Cash flows from financing activities

o New equity & new debt

o Repurchase of stock & debt repayment

o Dividends paid & interest payment

Dr Tomasz Berent

CASH FLOWS FROM OPERATING ACTIVITIES

Cash operating earnings

+ Earnings before interest and taxes (EBIT, NOP)

+ Depreciation

– Taxes

+/– Change in working capital

– Increase in inventories

– Increase in receivables

+ Increase in payables

Dr Tomasz Berent

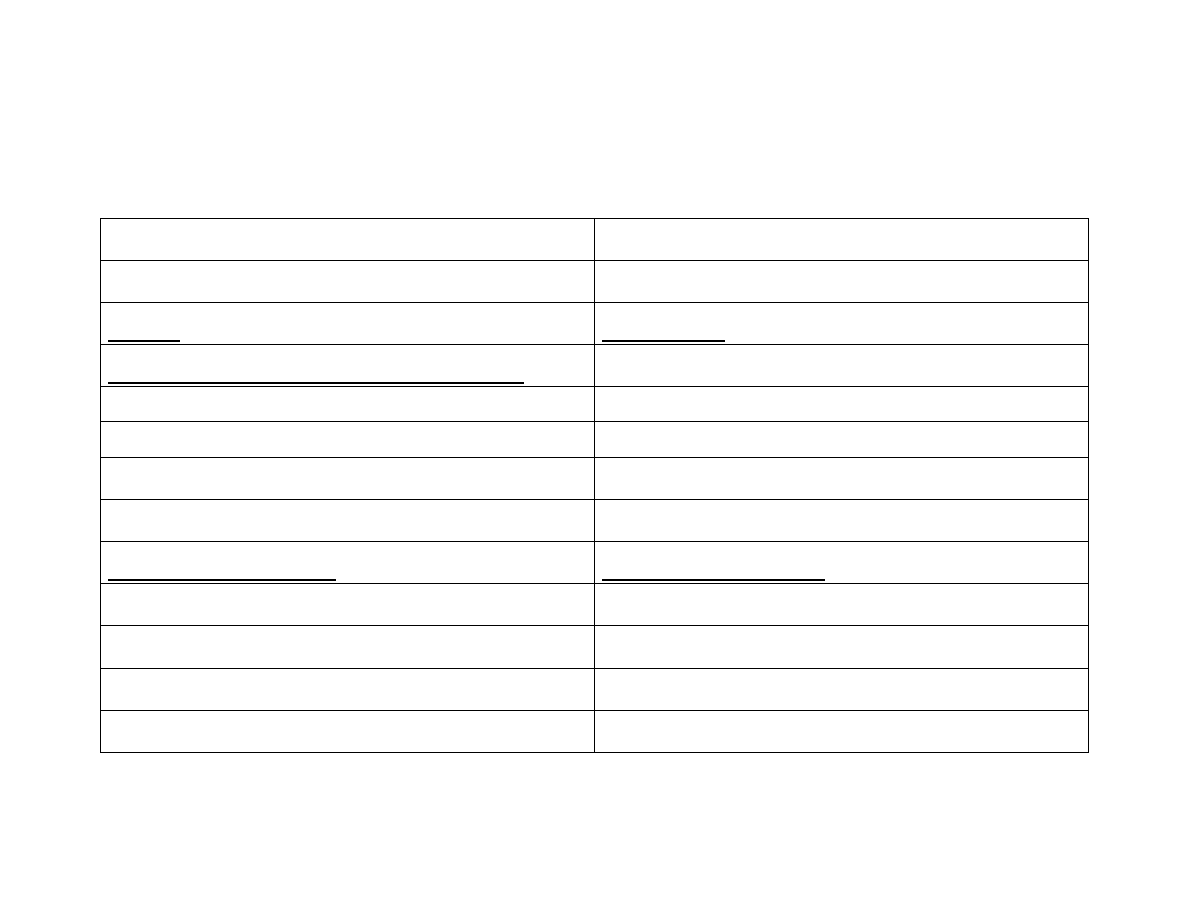

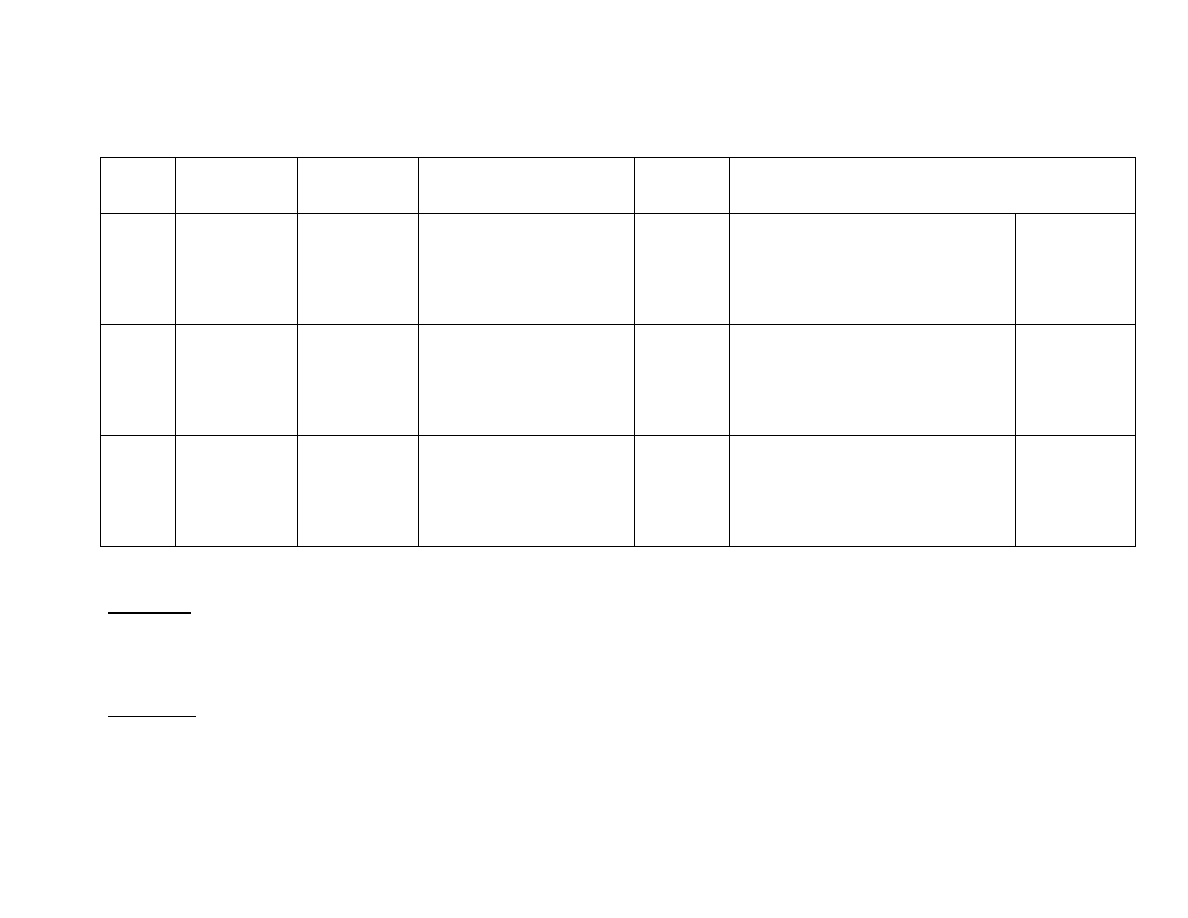

MANAGERIAL BALANCE SHEET (1)

ASSETS

EQUITY AND LIABILITIES

Current assets

Liabilities

Cash

Short-term liabilities

Marketable securities

Short-term debt

Receivables

Payables

Inventories

Other short term liabilities

Other current assets

Long-term liabilities

Fixed assets

Long-term debt

Intangible

Other long-term liabilities

Tangible

Owners’ equity

Investments

Common equity

Other fixed assets

Preferred stock

Dr Tomasz Berent

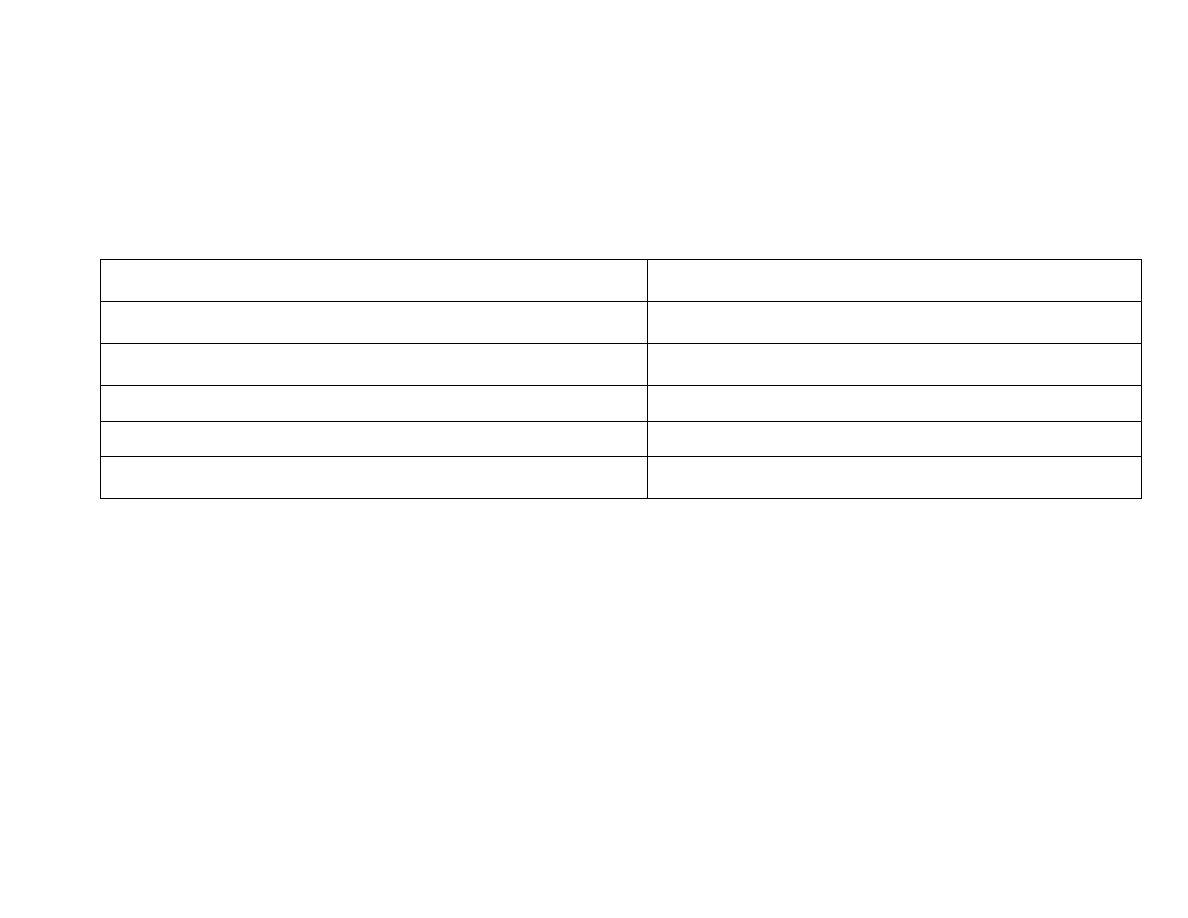

MANAGERIAL BALANCE SHEET (2)

NET ASSETS

CAPITAL EMPLOYED

Cash

Net debt

Working capital requirement

Net short-term debt

+Receivables

+Short-term debt

+Inventories

–Marketable securities

–Payables

Long-term debt

+/– Net other current assets

Net fixed assets

Owners’ equity

+Intangible

+Tangible

+Investments

+/–Net other fixed assets

Dr Tomasz Berent

MANAGERIAL BALANCE SHEET (3)

NET ASSETS

CAPITAL EMPLOYED

Working capital requirement (WCR) Net debt

+Operating current assets

Net short-term debt

–Non-interest bearing liabilities

Long-term debt

Net fixed assets

Owners’ equity

Net assets ≡ Invested capital = Capital employed

Dr Tomasz Berent

NET OPERATING PROFIT AFTER TAX (NOPAT)

NOPAT = NOP – Taxes on NOP

Taxes on NOP = Income taxes + Interest tax saving

Interest tax saving = Net interest expense

Marginal tax rate

Dr Tomasz Berent

DUPONT SYSTEM

Owners’ equity

Capital employed Net assets Sales Operating profit

Net income

ROIC

capital

Invested

NOP

Sales

NOP

capital

Invested

Sales

ROIC

AT

Sales

NOPAT

capital

Invested

Sales

Dr Tomasz Berent

MANAGING INVESTED CAPITAL

How much sales is generated by asset X, or

how much of asset X is required to generate sales X

X

Asset

Sales

X

ratio

Turnover

The higher the ratio, the better!

Turnover ratios, or activity, efficiency, rotation ratios

Dr Tomasz Berent

TURNOVER RATIOS

assets

Net

Sales

turnover

asset

Net

WCR

Sales

turnover

t

requiremen

capital

Working

Dr Tomasz Berent

WCR-RECEIVABLES

ceivables

Sales

turnover

ceivables

Re

Re

turnover

ceivables

Sales

ceivables

sales

Daily

ceivables

period

collection

Average

Re

365

365

Re

Re

Dr Tomasz Berent

WCR-INVENTORIES

s

Inventorie

sold

goods

of

Cost

turnover

Inventory

turnover

Inventory

COGS

s

Inventorie

COGS

Daily

s

Inventorie

inventory

in

Days

365

365

Dr Tomasz Berent

WCR-PAYABLES

Payables

COGS

turnover

Payables

turnover

Paybales

COGS

Payables

COGS

Payables

period

payment

Average

365

365

Dr Tomasz Berent

MANAGING OPERATING EXPENSES

Sales

item

Cost

in

m

ofit

1

arg

Pr

Examples:

1.Gross margin

2.Operating margin

Dr Tomasz Berent

RATIOS - SUMMARY

Turnover ratios (e.g. Net asset, WCR, Inventory turnovers)

Profitability ratios (e.g. ROIC, margins, ROA, ROE)

Liquidity (solvency) ratios (e.g. Current ratio, Quick ratio)

Financial leverage ratios (e.g. Debt, Debt-to-equity ratios)

Market value ratios (e.g. EPS, P/E, P/BV, Dividend yield)

COMPOUNDING PERIODS

Future value of $1,000 at the end of T periods,

r

A

– stated annual interest rate, compounding m times

Compounding

Monthly

m=12

Years

r

A

\ T

1

2

5

10

20

10%

1,105

1,220

1,645

2,707

7,328

20%

1,219

1,487

2,696

7,268

52,828

40%

1,482

2,197

7,152 51,151 2,616,408

Annually

m=1

Years

r

A

\ T

1

2

5

10

20

10%

1,100

1,210

1,611

2,594

6,727

20%

1,200

1,440

2,488

6,192

38,338

40%

1,400

1,960

5,378 28,925

836,683

Difference

Years

r

A

\ T

1

2

5

10

20

10%

5

10

35

113

601

20%

19

47

208

1,077

14,490

40%

82

237

1,774 22,225 1,779,725

CONTINUOUS COMPOUNDING

r

efec

vs. r

A

and m

r

A

10.0% 20.0% 50.0% 100.0%

m=1

10.0% 20.0%

50%

100%

m=2

10.3% 21.0%

56%

125%

m=4

10.4% 21.6%

60%

144%

m=12

10.5% 21.9%

63%

161%

m=+

10.5% 22.1%

65%

172%

r

A

vs. r

efec

and m

r

efec

10.0% 20.0% 50.0% 100.0%

m=1

10.0% 20.0%

50%

100%

m=2

9.8% 19.1%

45%

83%

m=4

9.6% 18.7%

43%

76%

m=12

9.6% 18.4%

41%

71%

m=+

9.5% 18.2%

41%

69%

Dr Tomasz Berent

BOND VALUATION

T -

Maturity date (maturity)

F -

Face (redemption, par, principal) value

c -

Coupon rate

y -

Yield to maturity (YTM)

PV -

Bond price

y’ - Current yield

EXAMPLE

A 5-year coupon bond with a face value of $1,000, the

coupon rate of 10%, paid annually, YTM=12.0%

PV<$1,000 ($928, or 92.8%) and y’=10.8%

Dr Tomasz Berent

BOND VALUATION

Pure discount bonds (zero-coupon, zeros, bullets)

T

y

F

PV

)

1

(

c=0%

F=$1,000

T=2

T=5

T=10

y=7%

873.4

713.0

508.3

y=10%

826.4

620.9

385.5

y=13%

783.1

542.8

294.6

Coupon bonds (level-coupon), C = c

F

T

for

y

C

PV

y

F

y

y

C

PV

T

T

)

1

(

)

1

(

1

1

c=10%

F=$1,000

T=2

T=5

T=10

T=

y=7%

1054.2 1123.0 1210.7 1428.1

y=10%

1000.0 1000.0 1000.0 1000.0

y=13%

950.0

894.5

837.2

769.2

Dr Tomasz Berent

BOND PRICE VS. INTEREST RATES

Bond prices move in an opposite direction to

interest rates

o Fall with a rise in interest rate

o Rise with a fall in interest rate

The longer maturity, the higher impact of

interest rate change on bond price

The larger the coupon, the lower impact of

interest rate change on bond price

Bond price (PV) vs. Face value (F)

c < y PV < F Bond sells at a discount

c = y PV = F Bond sells at the face value

c > y PV > F Bond sells at a premium

DIVIDEND PAYMENT VS. GROWTH

r

ROE

d

d

r

EPS

g

r

div

P

G

)

1

(

0

WARNING:

1. DO NOT USE UNCRITICALLY THE FORMULA FOR

FIRMS PAYING NO DIVIDEND. They are NOT worthless!

2. DO NOT USE THE FORMULA FOR COMPANIES, WHERE

GROWTH g IS ASSUMED TO BE HIGHER THAN r.

Such companies simply do not exist! If they did they would be

priceless not worthless (i.e. their share prices, rather than being

negative as suggested by the formula, would approach infinity)

3. DO NOT SUBSTITUTE div WITH EPS IN THE FORMULA

Unless all earnings are paid as dividends, i.e. d=1 and therefore

EPS=div. However, in such case no growth should be assumed,

g=0.* (Using both EPS instead of div and g>0, you simply

double count!)

4. DO NOT FORGET g WHEN USING div

Otherwise, you assume all retained earnings are wasted!

5. NOTE:

Retention of earnings creates value (increases the share

price) only if the return on new projects exceeds required

rate of return (i.e. P

0

G

>P

0

NG

only if ROE>r)!

Dividends may continue to grow for a growth company

and yet P

0

G

<P

0

NG

! It is because dividends grow when

(1-d)>0 and ROE>0, while P

0

G

>P

0

NG

when (1-d)>0 and

ROE>r.

Dr Tomasz Berent

INTERNAL RATE OF RETURN, IRR

CFs

No of sign

change

No of IRR

Decision

NPV

EXAMPLE

r=20%

Decision

-+++

1

1

IRR>rACCEPT

IRR<rREJECT

NPV>0

NPV<0

-100,20,40,60

IRR=8.2% < r=20%

NPV= -20.8 <0

REJECT

REJECT

++----

1

1

IRR<rACCEPT

IRR>rREJECT

NPV>0

NPV<0

50,-10,-20,-30

IRR=8.2% < r=20%

NPV=10.4 > 0

ACCEPT

ACCEPT

+--+-

>1

?

NO RULE

?

-100,130,150,-191

IRR

1

=12.7%, IRR

2

=39.3%

NPV=2.0 > 0

???

ACCEPT

PROS:

A simple, intuitively appealing number

Relevant in sensitivity analysis

CONS:

No definite decision rule

Ignores scale (just as all percentage measures )

Cannot be used to compare two projects, even of the same scale

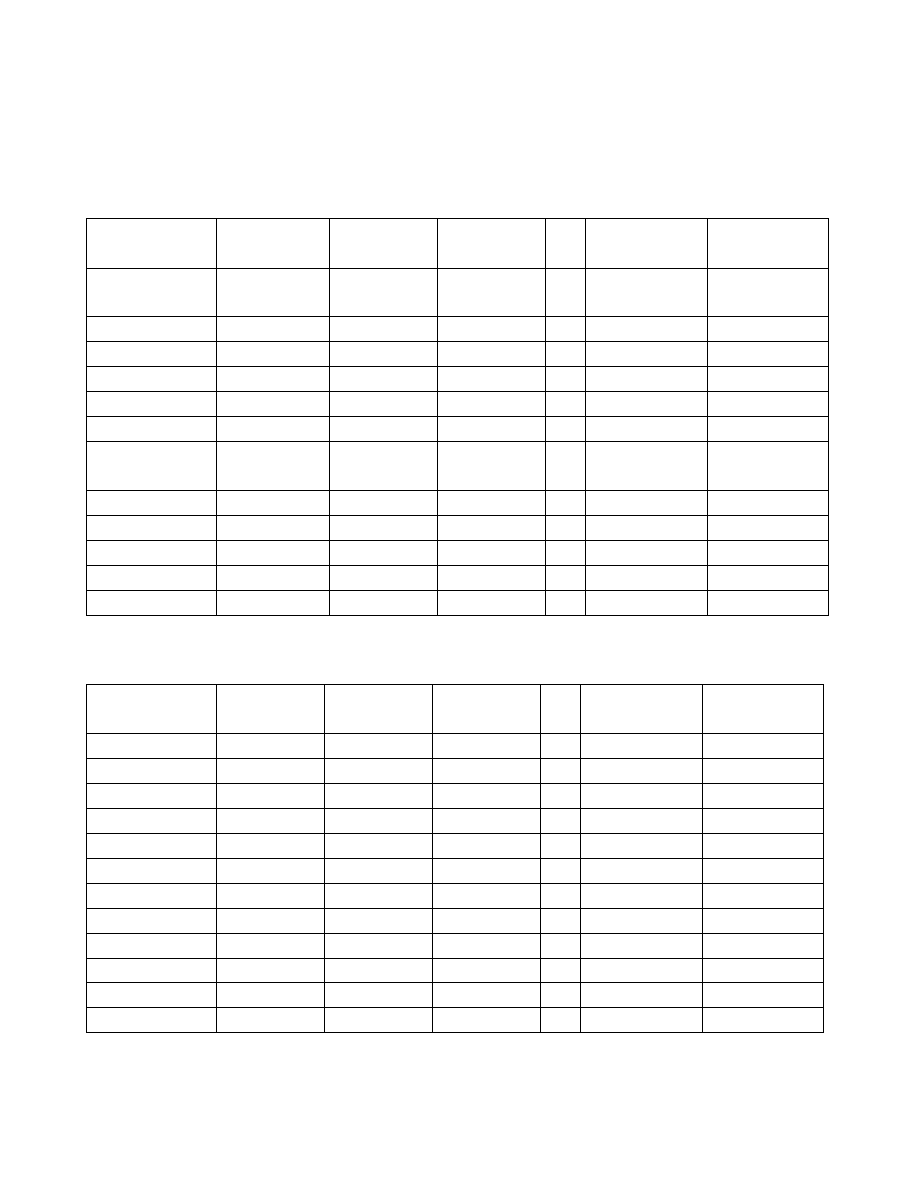

PROJECT APPRAISAL

NCFs for A, B, C, t=0,1,2,3,4 ($)

t

Project A

Project B Project C

Project B

–

Project A

Project B

–

Project C

Nominal

values

0

-1,000

-1,000

-500

0

-500

1

800

100

100

-700

0

2

400

300

200

-100

100

3

300

500

300

200

200

4

100

1,000

340

900

660

Discounted

values

0

-1,000

-1,000

-500

1

727

91

91

2

331

248

165

3

225

376

225

4

68

683

232

Project A Project B Project C

Project B

–

Project A

Project B

–

Project C

r

10%

10%

10%

NPV

351.5

397.5

213.8

46.0

183.7

PI

1.35

1.40

1.43

MIRR

18.6%

19.6%

20.2%

IRR

31.9%

22.4%

25.1%

12.6%

20.2%

ARR

15.0%

22.5%

22.0%

PP

1 6/12

3 1/12

2 8/12

DPP

1 10/12

3 5/12

3 1/12

t

Project A Project B Project C

(B-A) (B-C)

r

NPV(A) NPV(B)

NPVC

Nominal values

0.0%

600

900

440

0

-1,000

-1,000

-500

0

-500

2.0%

544

781

387

1

800

100

100

-700

0

4.0%

491

673

338

2

400

300

200

-100

100

6.0%

442

573

294

3

300

500

300

200

200

8.0%

395

482

252

4

100

1000

340

900

660

10.0%

352

398

214

Discounted values

12.0%

310

320

178

0

-1,000

-1,000

-500

12.6%

299

299

169

1

727

91

91

14.0%

271

248

145

2

331

248

165

16.0%

234

182

115

3

225

376

225

18.0%

199

120

86

4

68

683

232

20.0%

166

63

60

22.0%

135

10

35

22.4%

0

24.0%

105

-39

12

25.1%

0

26.0%

77

-85

-10

28.0%

49

-128

-30

30.0%

24

-168

-49

31.9%

0

32.0%

-1

-205

-67

34.0%

-25

-240

-84

36.0%

-47

-273

-100

38.0%

-69

-304

-115

PV of

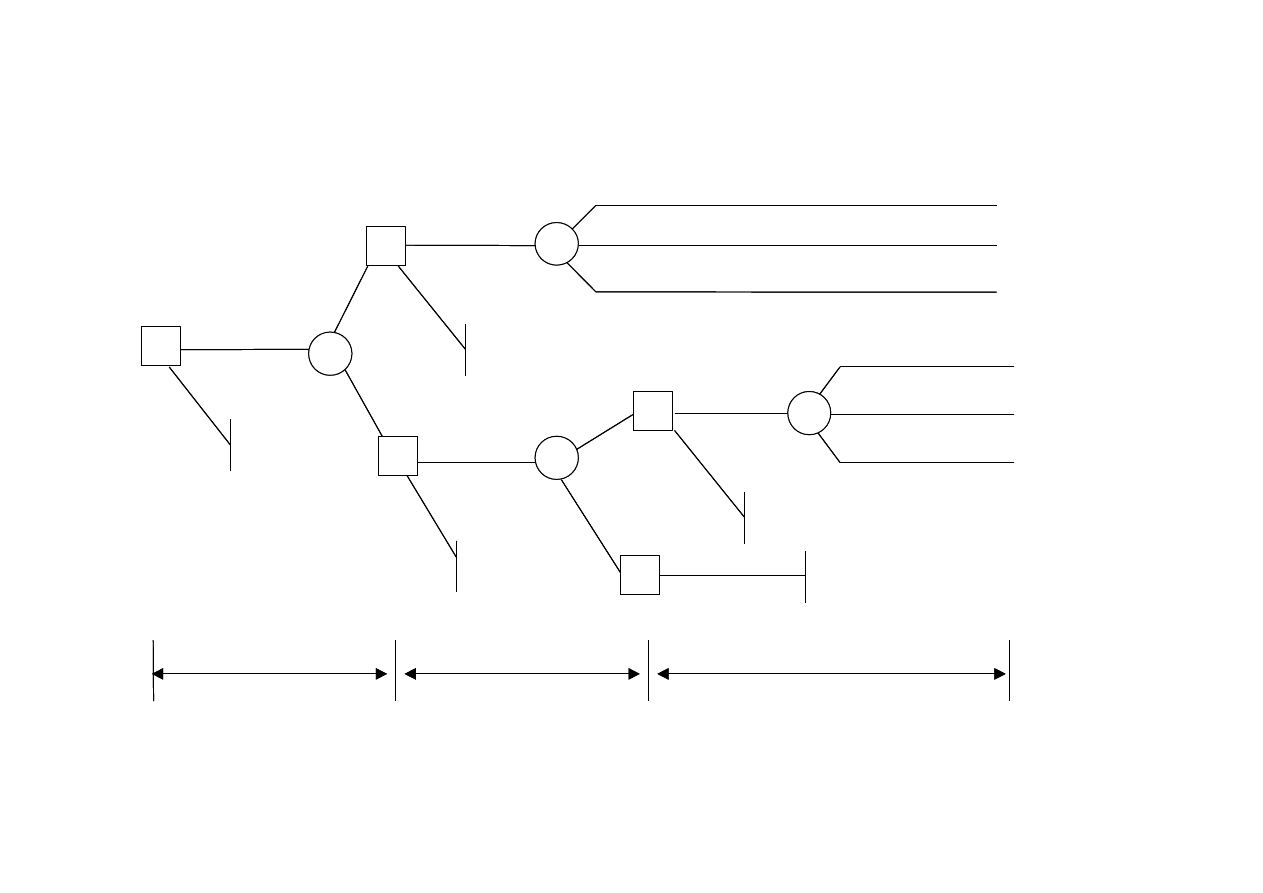

contribution

0.2 Sales high

0.3 Sales low

0.5 Sales medium

2 years

2 years

4 years

Abandon

Abandon

Abandon

Abandon

Abandon

0.1 high

0.4 low

0.5 medium

$1,600k

$800k

$400k

$1,200k

$600k

$300k

Market

product

Further

R & D

(cost $200k)

R & D

success

Market

product

late

(cost $400k)

R & D

success

R & D

failure

R & D

failure

0

0

0

0

0

0.5

0.5

0.3

0.7

1

3

2

2

B

A

C

D

R & D

3

PV of

contribution

0.2 Sales high

0.3 Sales low

0.5 Sales medium

2 years

2 years

4 years

Abandon

Abandon

Abandon

Abandon

Abandon

0.1 high

0.4 low

0.5 medium

Market

product

Further

R & D

R & D

success

Market

product

late

R & D

success

R & D

failure

R & D

failure

0

0

0

0

0

0.5

0.5

0.3

0.7

1

3

2

2

B

A

C

D

R & D

3

Dr Tomasz Berent

ROE and EPS vs. FINANCIAL LEVERAGE

D/E

IC

($)

Equity

($)

Debt

($)

Share

price ($)

No of

shares

NOP

($)

K

D

%

Fin. Cost

($)

Net

income* ($)

EPS

($)

ROE

(%)

0.00

500

500

0

10

50

100

10%

0

100

2.00 20.0%

0.25

500

400

100

10

40

100

10%

10

90

2.25 22.5%

1.00

500

250

250

10

25

100

10%

25

75

3.00 30.0%

1.50

500

200

300

10

20

100

10%

30

70

3.50 35.0%

* No taxes

ROE and EPS rise with financial leverage!!!

Dr Tomasz Berent

BUSINESS RISK

Recession

Expected

Boom

-chg +chg

Economic risk

Sales

300.0

500.0

700.0

-40% 40%

Variable costs

-180.0

-300.0

-420.0

Sales after variable costs

120.0

200.0

280.0

-40% 40%

Operational risk

Fixed costs (1)

0.0

0.0

0.0

NOP (1)

120.0

200.0

280.0

-40% 40%

Fixed costs (2)

-40.0

-40.0

-40.0

NOP (2)

80.0

160.0

240.0

-50% 50%

Fixed costs (3)

-100.0

-100.0

-100.0

NOP (3)

20.0

100.0

180.0

-80% 80%

Fixed costs (4)

-150.0

-150.0

-150.0

NOP (4)

-30.0

50.0

130.0

-160% 160%

Business risk (economic + operational risks)

Dr Tomasz Berent

FINANCIAL RISK

D/E Recession

Expected

Boom

-chg +chg

NOP (3)

20.0

100.0

180.0

-80% 80%

Interest expense (3.1)

0.00

0.0

0.0

0.0

Net income (3.1)

20.0

100.0

180.0

-80% 80%

Interest expense (3.2)

0.25

-10.0

-10.0

-10.0

Net income (3.2)

10.0

90.0

170.0

-89% 89%

Interest expense (3.3)

1.00

-25.0

-25.0

-25.0

Net income (3.3)

-5.0

75.0

155.0

-107% 107%

Interest expense (3.4)

1.50

-30.0

-30.0

-30.0

Net income (3.4)

-10.0

70.0

150.0

-114% 114%

Dr Tomasz Berent

RETURN ON EQUITY (ROE)

D/E

Recession

Expected

Boom

ROIC (3)

4.0%

20.0%

36.0%

ROE (3.1)

0.00

4.0%

20.0%

36.0%

ROE (3.2)

0.25

2.5%

22.5%

42.5%

ROE (3.3)

1.00

-2.0%

30.0%

62.0%

ROE (3.4)

1.50

-5.0%

35.0%

75.0%

ROE does not always increase with financial leverage!!!

Dr Tomasz Berent

EARNINGS PER SHARE

D/E

Recession

Expected

Boom

EPS (3.1)

0.00

0.40

2.00

3.60

EPS (3.2)

0.25

0.25

2.25

4.25

EPS (3.3)

1.00

-0.20

3.00

6.20

EPS (3.4)

1.50

-0.50

3.50

7.50

EPS do not always increase with financial leverage!!!

Dr Tomasz Berent

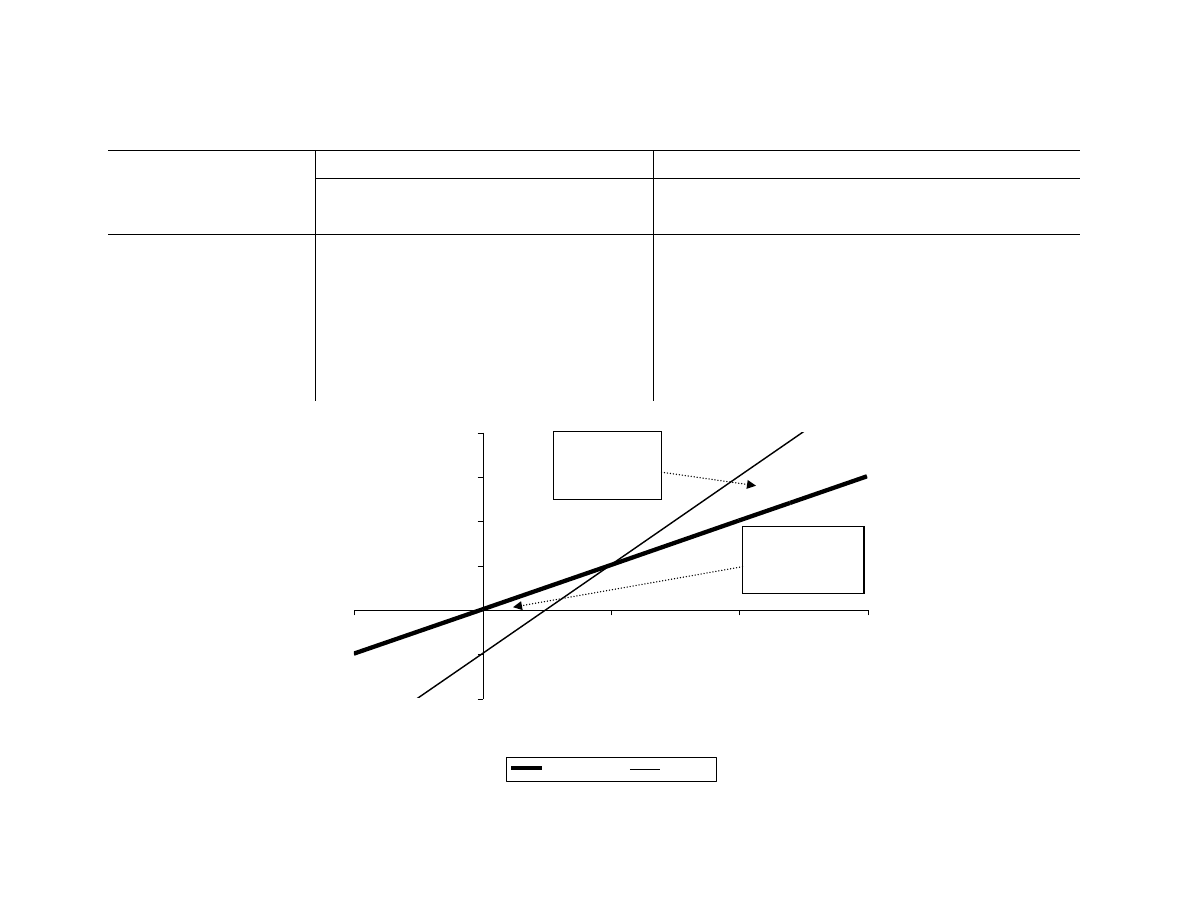

NOP vs. EPS

Unlevered

Levered, D/E=1

NOP

($)

k

d

%

IC

($)

Net inc.

($)

No of

shares

EPS

($)

D/E

D

($)

Net inc.

($)

No of

shares

EPS

($)

-50

10%

500

-50

50

-1.0

1

250

-75

25

-3.0

0

10%

500

0

50

0.0

1

250

-25

25

-1.0

50

10%

500

50

50

1.0

1

250

25

25

1.0

100

10%

500

100

50

2.0

1

250

75

25

3.0

120

10%

500

120

50

2.4

1

250

95

25

3.8

150

10%

500

150

50

3.0

1

250

125

25

5.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

-50

0

50

100

150

NOP

EPS

Unlevered

D/E=1

Advantage

to debt

Disadvantage

to debt

Wyszukiwarka

Podobne podstrony:

Principles Of Corporate Finance

Corporate finance 03

corporate finance

Principles Of Corporate Finance

Corporate finance investment valuation

corporate finance

Corporate Finance 7 01 2014

financial statements (Corporate Finance)

CORPORATE BANKING glossary, 03 banking & finance

Mr Corporate (Mister #3) JA Huss

mr all the fixin

GEORGE M MORTON Valuation Maximizing Corporate Value WILEY FINANCE

MR prezentacja

Positron emission tomography slides

IO ALL

więcej podobnych podstron