Investment Appraisal

The Basics of Investment

Valuation Methods

1

Learning objective

1. Cash flow supremacy

2. Cash flow definitions

3. Contribution analysis

4. Present value mechanics

5. Investment valuation methods

6. Reinvestment rate problem

7. Unconventional projects

8. Investment’s with different lives

2

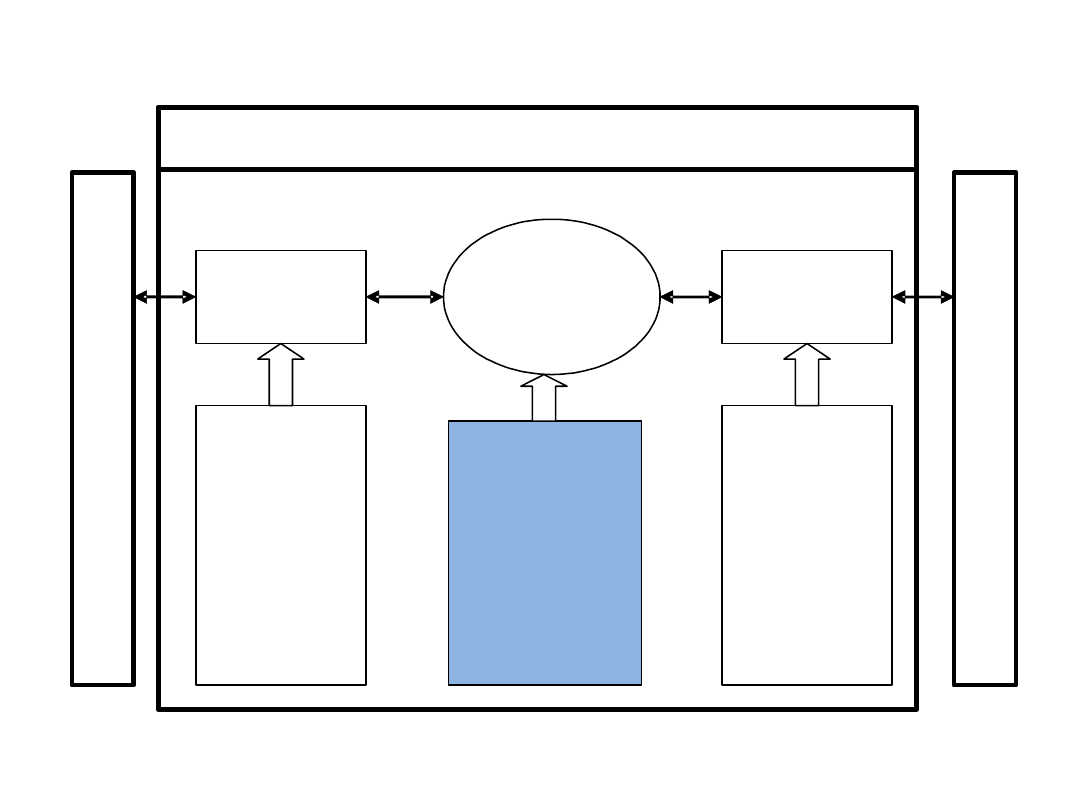

ENTERPRISE

S

T

A

K

E

H

O

L

D

E

R

S

The Financial

Simulation Of

Business Reality

Business

Reality

Capital Market

Reality

C

A

P

I

T

A

L

M

A

R

K

E

T

- Logistics

- Consumer’s

satisfaction,

- Product mix,

- Pricing

strategz,

- TQM,

- R&D,

- Labor Unions

- Ect.

Financial

Parameters

Used In

Valuation

Method

- Investor’s

behaviour,

- Cahs flows,

- The impact

on firm’s

value,

- Cost of

capital

estimation,

- Pricing

decisions

3

How to define income available to

stockholders?

• It is assumed that investment project’s

will be priced in the way other financial

instruments are priced as aggregated

present values of income.

• Three different types of income available

to stockholders are identified, i.e.:

dividends, profits, cash flows. Various

types of valuations methods use these

types of income.

• Company’s financial management

objective requires valuation from:

– Stockholder point of view

– Firm’s point of view (all investors point of view)

4

Definition of an income:

earnings versus cash flows

• Principles Governing Accounting Earnings

Measurement

– Accrual Accounting:

– Operating versus Capital Expenditures:

• To get from accounting earnings to cash flows:

– add back non-cash expenses (depreciation)

– subtract out cash outflows which are not expensed

(capital expenditures)

– make accrual revenues and expenses into cash

revenues and expenses (changes in working

capital).

5

Entity and Equity valuation

• Free Cash Flow gives project’s value from the

all capital provider’s point of view. The

appropriate discount rate is weighted average

cost of capital from all company’s capital

resources.

Project’s Value = Debt + Equity

• Cash Flow to Equity (and dividend model)

evaluates investment from shareholder’s

point of view. The appropriate discount rate is

cost of equity. In this case, the DCF model

leads to the valuation of equity

contribution.

6

The Separation Principle

•

The idea is to separate results of financing

decision from other decisions (i.e. operational and

investment). As a result, the change of debt-equity

ratio will not effect project’s cash flow.

•

Free Cash Flow (FCF) is the kind of cash flow that

measures net cash flows between a company and

its providers of finance, (all financial flows are

excluded)

•

The FCF is defined as the sum of net operating

profit after tax and depreciation less investments

in net working capital and capital expenditures

7

Contribution analysis

• The contribution of a decision is defined as the

incremental cash inflows of that decisions less

the incremental cash outflows of that decision

• It should be interpreted as the „contribution

made to overhead free cash flows” by the

decision.

• Clearly, only those decisions that have positive

contribution should be undertaken;

• And where decisions are mutually exclusive,

the one with larger expected is to be preferred

8

Incremental cash inflows

• Incremental cash inflows are defined

as the cash inflow which follow as a

consequence of a particular decision

• We should expect incremental cash

flow to have an explicit current-

period component, a possible

opportunity component, and a

possible future component

9

Incremental cash inflows (part

2)

• An opportunity cash inflow is a cash

outflow avoided as the result of a decision.

• Although there is no actual inflow, the

outflow is avoided so the money otherwise

be spent is still sitting in the bank, and the

net effect is the same

• The future cash inflow is the expected

present value of the contribution to overall

firm’s flows associated with the future

business generated by the decision.

10

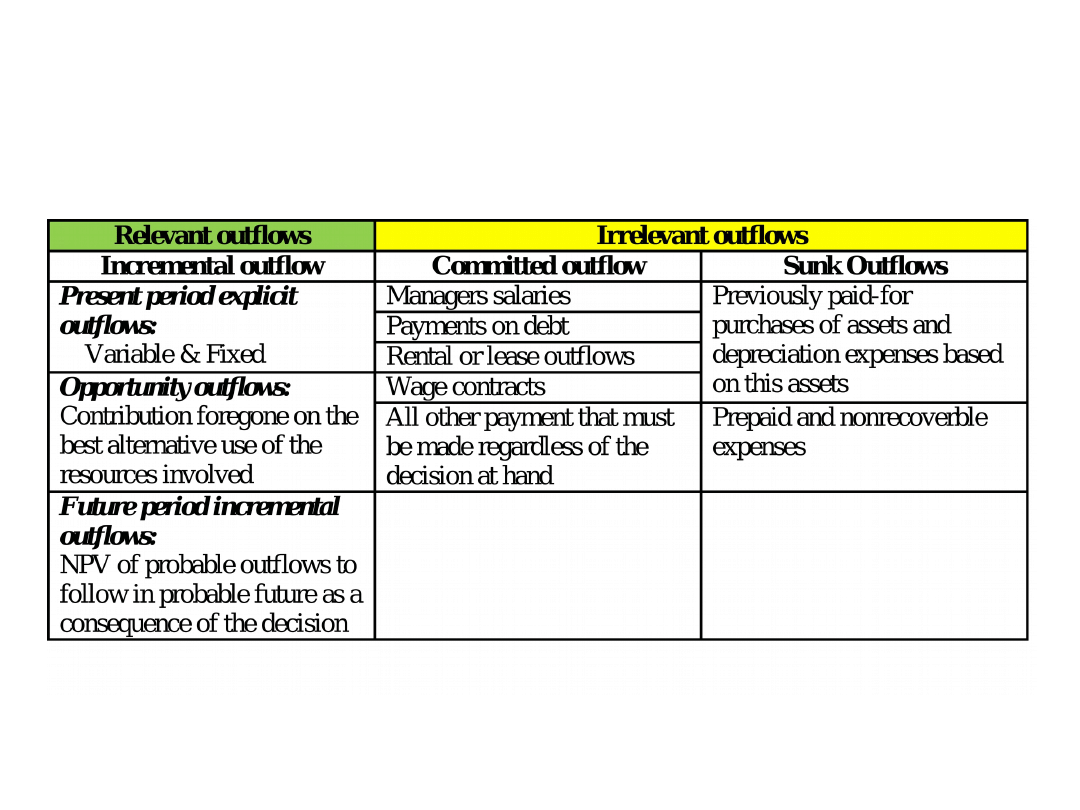

Incremental outflow

• The relevant outflows for decision making

purposes are those outflows that will be

incurred as a result of the decision being

considered. The relevant outflows are

therefore the incremental outflows

• Outflows that have been incurred already

and outflows that will be incurred in the

future regardless of the present decision,

are irrelevant outflows as far as the

current decision problem is concerned

11

Incremental outflows in

investment’s decision making

12

The project’s impact on other

projects (i.e. externalities) should

be evaluated

• Only few projects could be perceived as “truly”

independent.

• Both positive and negative externalities should be

recognized and included in contribution analysis.

Complementary projects

Substitude projects

Interdependent

projects

Mutually exclusive

projects

Independent projects

SYNERGY EFFECT

CANNIBAL EFFECT

13

Time-Weighted Incremental Cash

Flows

• Cash flows across time cannot be added up. They

have to be brought to the same point in time before

aggregation. The general rule is that incremental

cash flows in the earlier years are worth more than

incremental cash flows in later years.

• This process of moving cash flows through time is

– discounting, when future cash flows are brought to the

present

– compounding, when present cash flows are taken to the

future

• The discounting and compounding is done at a

interest rate that will reflects opportunity cost of

capital (which captures nominal interest rates and

risk premiums)

14

Present Value Mechanics

Cash Flow Type

Discounting Formula Compounding Formula

1. Simple Cash Flow (CF) CF

n

/ (1+r)

n

CF

0

(1+r)

n

2. Annuity (A)

3. Growing Annuity

4. Perpetuity

A/r

5. Growing Perpetuity (CF

1

)/(r-g)

r

r)

+

(1

1

-

1

A

n

A

(1+r)

n

- 1

r

A(1+g)

1 -

(1+g)

n

(1+r)

n

r- g

15

Investment’s valuation methods

• Net Present Value (NPV): The net present value is the

sum of the present values of all cash flows from the project

(including initial investment).

NPV = Sum of the present values of all cash flows on the project,

including the initial investment, with the free cash flows being

discounted at the appropriate opportunity costs

– Decision Rule: Accept if NPV > 0;

– While making the ranking of investments: The set of

investments which max. NPV is optimal

16

N

t

t

t

k

FCF

NPV

0

)

1

(

Investment’s valuation methods

• Internal Rate of Return (IRR): The internal rate of return

is the discount rate that sets the net present value equal to

zero. It is the percentage rate of return, based upon

incremental time-weighted cash flows.

– Decision Rule: Accept if IRR > hurdle rate

17

N

t

t

t

IRR

FCF

NPV

0

)

1

(

0

Case 1. NPV, IRR and the

reinvestment rate

assumption

• Using the NPV rule it’s assumed that intermediate

cash flows will be reinvested at the discount rate

(which is based upon opportunity cost of capital).

• Using the IRR rule it’s assumed that intermediate

cash flows will be reinvested at the IRR. It means

that company has an access to projects with

similar IRRs. Consequently, when this assumption

is not met then IRR will overstate the true return on

the project.

• It convenient to assume, that IRR shows the

maximum opportunity cost of capital, the

project could face.

18

Solution to reinvestment problem is to

differentiate opportunity cost rate and

reinvestment rate

• In such a case one should calculate the

modified NPV (MNPV)

• CF

t(+)

is a positive free cash flow period t,

• CF

t(-)

is a negative free cash flow period t

• The interpretation of MNPV is the same

like standard NPV

19

N

y

opportunit

N

t

t

N

y

opportunit

N

t

t

N

reinvest

t

k

CF

k

k

CF

MNPV

)

1

(

)

1

(

1

0

)

(

0

)

(

Solution to reinvestment problem is to

differentiate opportunity cost rate and

reinvestment rate

• Modified IRR (MIRR) is calculated

• The MIRR ranking of projects shows

which project gives the biggest

return per one monetary unit

invested.

20

1

)

1

(

1

1

0

0

N

N

t

t

y

opportunit

t

N

t

t

N

reinvest

t

k

CF

k

CF

MIRR

CASE 2. Unconventional projects

• Conventional projects – projects with the

only one change of a sign of cash flows. It is

a typical situation, when after cash outflow

(or a negative net cash flow) in the beginning

come cash inflows (or a positive net cash

flow) till the end of the project.

• In case of unconventional projects there is

more than one change of a sign of cash

flows. The analysis of unconventional

projects calls for MNPV!

21

Case 3. Projects with

different lives

• The net present values of mutually

exclusive projects with different lives

cannot be compared, since there is a

bias towards longer-life projects.

• To do the comparison, we have to:

– replicate the projects till they have the

same life (or)

– convert the net present values into

annuities (preferable!) or

– replicate the projects infinitely

22

Steps in annuity calculation

Step 1. Calculate the NPV of each

alternative

Step 2. Divide the result by present value

interest factor for annuity (equation from

slide 19)

Step 3. Choose a project with higher

annuity!

23

1

r

r)

+

(1

1

-

1

*

NPV

Annuity

n

Document Outline

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

- Slide 17

- Slide 18

- Slide 19

- Slide 20

- Slide 21

- Slide 22

- Slide 23

Wyszukiwarka

Podobne podstrony:

Principles Of Corporate Finance

Corporate finance 03

all slides Corporate Finance MR BERENT

corporate finance

Principles Of Corporate Finance

corporate finance

Corporate Finance 7 01 2014

financial statements (Corporate Finance)

Creation of Financial Instruments for Financing Investments in Culture Heritage and Cultural and Cre

GEORGE M MORTON Valuation Maximizing Corporate Value WILEY FINANCE

Investor Psychology A Behavioral Explanation Of Six Finance Puzzles

CORPORATE BANKING glossary, 03 banking & finance

Valuation Of Cash Flows Investment Decisions Capital Bud

więcej podobnych podstron