In the name of God

C

ontents

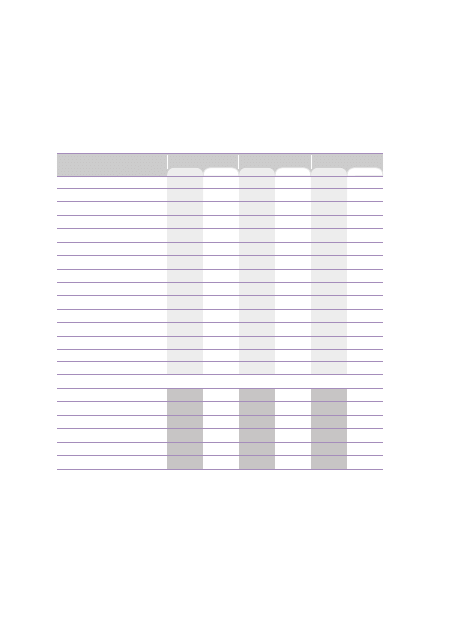

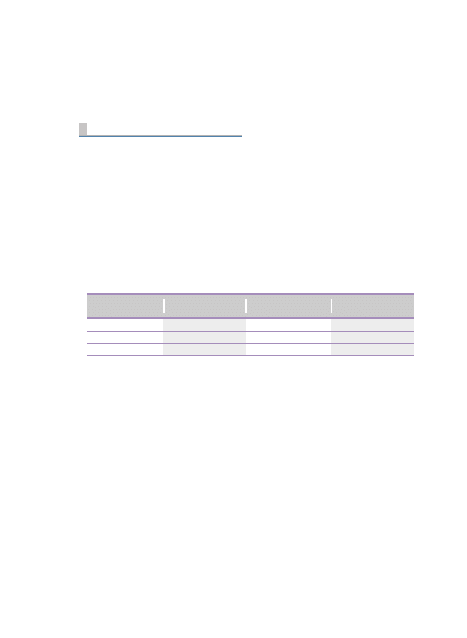

Consolidated Balance Sheet Highlights

4

Message from the Chairman & Managing Director

6

Members of the Board of Directors

10

General Managers

11

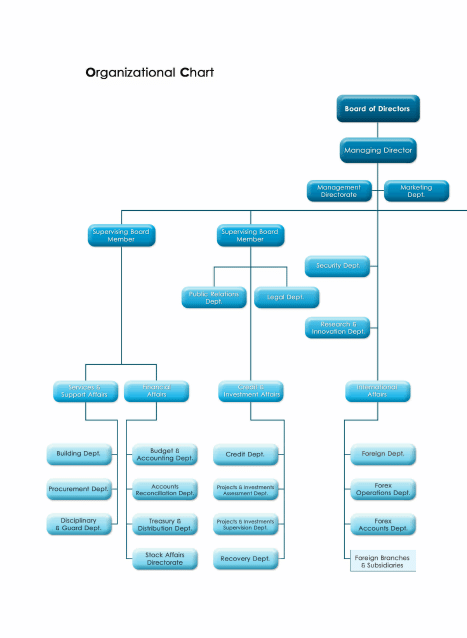

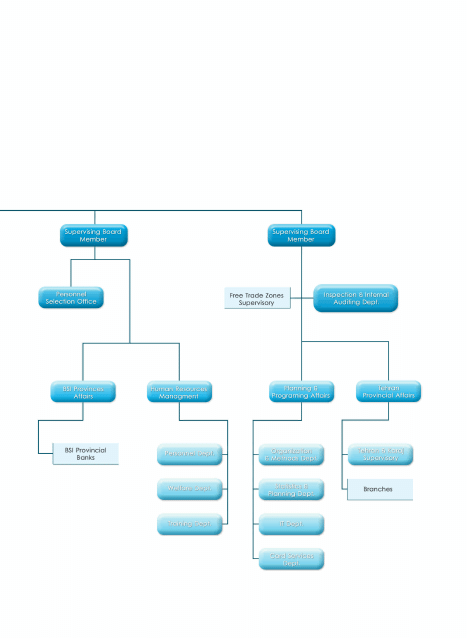

Organizational Chart

12

Iran at a Glance

14

Achievements

17

Islamic Banking in Iran

18

Goals, and Strategic Planning in BSI

19

Mission and Vision

21

Corporate & Commercial Banking Projects

23

25

International Banking

27

Technological Infrastructures

31

Human Resources

37

Free Trade Zones

41

42

43

46

49

59

60

97

98

Iranian Banking System

History

Financial Performance

Anti Money Laundering

Risk Management

International Network

Contact Persons

Financial Statements

105

BSI Subsidiaries & Branches Abroad

Excerpts from the Auditors’ Report

48

Highlights of BSI Success in International and National Arena

Privatization

26

Bank Saderat Iran Group

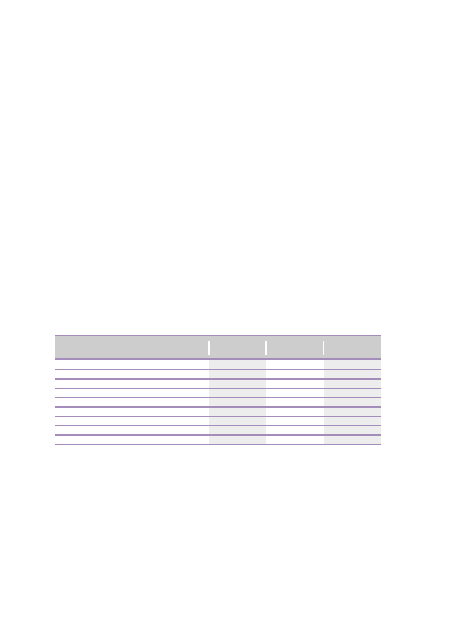

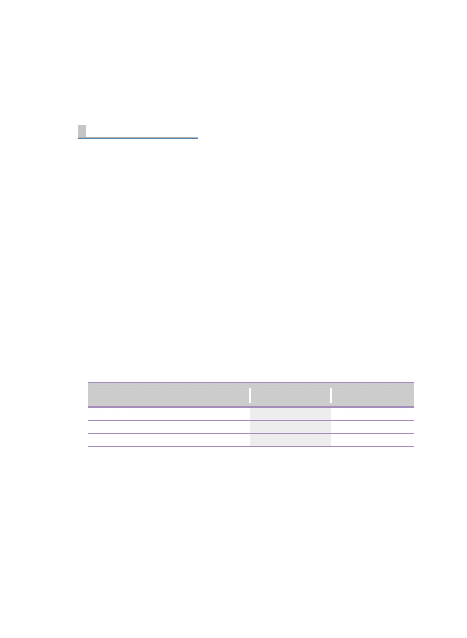

Consolidated Balance Sheet Highlights

*USD/RLS exchange rates as of 20.03.2008 and 20.03.2009 are 8970 and 9723 respectively. Therefore,

decrease in the USD figures in the presented financial statements, compared with the previous year,

is due to the increase in the exchange rate.

20.03.2007 20.03.2008 20.03.2009

Assets

Liabilities

Customer Deposits

Loans to Customers

Shareholders' Equity

Income Statement Highlights

Net Interest Income

Non-Interest Income

Operating Income

Operating Expenses

Operating Profit

Other Expenses

Provisions

Income Tax

Net Profit

Key Ratio

Expenses/Income

Net Profit /Operating Income

Return on Equity

Return on Assets

Loans / Deposits

billion Rls *million USD billion Rls *million USD billion Rls *million USD

319,910

289,611

198,322

182,782

30,299

20,727

8,707

29,434

(15,156)

14,278

(7,153)

(4,060)

(576)

2,490

34,610

31,322

21,455

19,774

3,278

2,253

946

3,199

(1,647)

1,552

(777)

(442)

(62)

271

51.5%

8.5%

8.3%

0.8%

92.2%

386,263

356,082

265,413

219,196

30,181

26,897

11,154

38,051

(23,217)

14,834

(8,393)

(4,606)

(310)

1,525

43,062

39,697

29,589

24,437

3,365

2,999

1,243

4,242

(2,588)

1,654

(936)

(513)

(35)

170

61%

4%

5%

0.4%

69.8%

408,185

379,674

271,138

245,234

28,511

32,704

8,250

40,954

(24,052)

16,901

(9,783)

(4,015)

(293)

2,811

41,981

39,049

27,886

25,222

2,932

3,364

849

4,212

(2,474)

1,738

(1,006)

(413)

(30)

289

58.7%

6.9%

9.9%

0.7%

79.8%

M

essage From the Chairman and Managing Director

On the 57th Anniversary of the Bank, on behalf

of the Board of Directors and the diligent staff,

I, would like to seize the opportunity and

express my deepest gratitude to BSI customers

and shareholders.

During 2008, the global economy underwent

massive changes including financial crises and

economic depression which dramatically

affected many countries.

Influenced by many factors, the crises had a

devastating impact on banks and stock markets

all over the world so that the financial indices

lost 50% of their value.

This led to an exacting investigation and a

review of the methods and use of effective

financial management tools. On the other hand,

the Iranian economy, particularly the money

and capital market, was not closely linked to

the corresponding markets abroad and was,

consequently, little affected by the crises, taking

advantage of proper economic policy.

Having the largest overseas branch network

within the Iranian banking system, BSI has,

fortunately, been able to develop its

international banking relations in line with

facilitating money and trade exchanges.

To maintain BSI's commanding presence as an

international bank, the Board of Directors has

implemented thorough and meaningful plans.

The overseas branches produced net profits of

USD 180 million and USD 212 million in 2007

and 2008 respectively, revealing a 17% growth

in profitability and FX income despite existing

sanctions.

BSI started offering banking services in 1952.

Since then, it has continued to achieve success

and to provide its customers with satisfaction

and has, now, the largest domestic and overseas

branch network within the Iranian banking

system with 21 overseas branches, two Regional

Offices, two independent banks (Bank Saderat

PLC, London and Bank Saderat Tashkent),

and two Joint-Venture Banks (Future Bank,

Bahrain and Arian Bank, Afghanistan).

With the highest number of branches in the

country, BSI naturally possesses a large number

of customers. Our bank has equipped all its

branches with Real Time Online System

(SEPEHR), has opened more than 30 million

online accounts, has issued 7.4 million

electronic cards and credit cards, and has 2051

mobile and fixed ATMs and 200,000 POS. Our

customers have welcomed our newest services

including internet banking and mobile banking.

Quality and quantity improvement of new

services in our bank is what our managers and

staff aspire to.

BSI performance highlights in attracting

resources and granting loans are as follows:

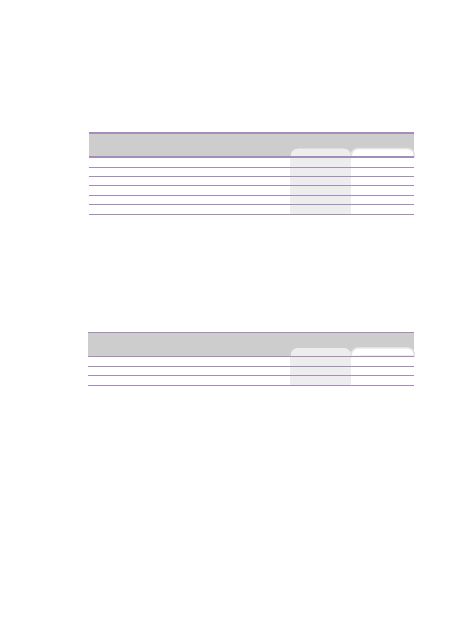

Deposits: Total deposits increased from Rls

265,413 billion in the year ended 20.3.2007 to

Rls 271,138 billion in the year ended 20.3.2008,

showing a growth of 2.2%. It is noteworthy that

operational deposits (4 main deposits) increased

18.5% in the reported year.

Description

20.03.2008

20.03.2007

44,571

26,265

77,236

59,200

63,866

271,138

45,110

22,447

58,721

48,758

90,377

265,413

Interest-free Current Account

Interest-free Saving Account

Short-term Deposits

Long-term Deposits

Other Deposits

Total

Deposits Comparative Table

Facilities granted to public sector

Facilities granted & claims from private sector

Total

Description

20.03.2008

20.03.2007

Facilities Comparative Table

3,011

213,346

216,357

4,867

180,489

185,356

Facilities: Total facilities increased from Rls 185,356 billion in the year ended 20.3.2007 to Rls

216,357 billion in the year ended 20.3.2008, showing a growth of 17%.

After privatization, BSI will bring dramatic changes including dissolution of loss-making branches

or merger with other branches, restructuring in order to improve efficiency, process reengineering,

risk management and credit rating, improving human resources efficiency, developing new

branches and subsidiaries all over the world, diversifying the services, and etc.

Billion RLS

Billion RLS

I would like to express my sincere gratitude to all the people who contributed to the bank

development within the Iranian banking system and all those who continue to believe in Bank

Saderat Iran after 57 years. I wish to assure our shareholders that BSI, as a privatized bank, is

ready to meet the challenges and grasp new opportunities to develop.

Yours sincerely

Dr. Hamid Borhani

Chairman & Managing Director

Members of The Board of Directors

Mr. Ghodratollah Sharifi

Board Member

Mr. Gholamreza Hajizadeh

Board Member

Dr. Hojatollah Saydi

Board Member

Mr. Mahdi Fattahi

Board Member

Mr. Bahman Vakili

Board Member

Dr. Hamid Borhani

Chairman of the Board of Directors

General Managers

Mr. GholamReza Arjmandi

General Manager, Financial Affairs

Mr. Mohammad Rabizadeh

General Manager, Structural & Procedural

Reformations Affairs.

Mr. Parviz Soltani

General Manager, Human Resources Affairs

Mr. Ahmad Mazaheri

General Manager, Credit & Investment Affairs

Mr. Reza Goudarzi

General Manager, Planning & Programming Affairs

Mr. Gholam Ali Shafiee

General Manager, Services & Support Affairs

Mr. Gholam Souri

General Manager, International Affairs

Mr. Hamid Saghar

Manager, Budget & Accounting Department

Mr. Mohsen Hosseini HosseinPoor

Manager, Foreign Department

Mr. Alireza Mousavihassab

General Manager, BSI Provinces Affairs

I

ran at a Glance

Iranian Economy during the First Six

Months of the Year 2008

Due to an upturn in the international crude oil

market and other markets during the first six

months of the year 2008, there was a surplus

foreign payments balance so that the trade

surplus was $31,858 million including non-oil

export trade($9,865 million) and imports

($35,508 million). In this period, the total

foreign assets of Central Bank of Iran (including

Foreign Reserve Accounts) show an increase

of $15,204 million.

During the first and second quarters of 2008,

as a result of the surplus oil income, the earned

profit belonging to prior investment and return

of granted facilities, $28,618 million was

remitted to the Foreign Reserve Account, with

$23,610 million withdrawn. Thus, net cash of

the Foreign Reserve Account (regardless of

cash balance at the beginning of the period)

shows a surplus of $5,008 million during the

above period.

During the first and second quarters of 2008,

crude oil export was about 2,498.4k barrels

per day, showing a 2.7% growth compared to

the same period in 2007.

2008

Balance of Payments

2007

2006

Oil and Gas

Others

Total exports

Total Imports

Trade balance

Net services

Net money transfers

Current account balance

62,011

14,044

76,055

50,020

26,035

(6,146)

513

20,402

81,764

15,637

97,401

56,582

40,819

(7,199)

461

34,081

71,654

14,278

85,932

52,023

33,909

(6,491)

558

27,976

Source: Central Bank of Iran (Nine Months)

At the end of September 2008, the liquidity

had 1.8% growth compared to the previous

year, showing 11.2% decrease in comparison

with the corresponding growth last year. Net

foreign assets of the banking system had a

growth of Rial 54.2k billion which, in turn

caused 3.3% growth in liquidity.

Started from early 2007, prosperity in the

construction industry continued during the

first and second quarters of 2008.

During the first six months of 2008, total state

budget was reported Rial 431.8k billion

consisting of 170.5k, 125.9k, and 135.4k billion

for income, capital assets assignment and

financial assets assignment respectively.

During the same period, Mining and Industries

issued 16,600 establishment licenses and 3,300

new sections development licenses.

During the first and second quarters of 2008,

all the price indices in Tehran Stock Exchange

rose except those of "50 chosen companies".

Also the number and value of traded stocks

increased 86.5% and 265% respectively

compared to the previous year.

Million USD

A

chivements

H

istory

As a private bank and public joint stock

company, BSI was established on September

6, 1952 with Rials 20 million in share capital,

50% of which was paid in cash and launched

its operation on November 13, 1952 with a

staff of thirteen.

BSI overseas activity began by establishing a

branch in Hamburg, Germany and now it has

21 active branches and 3 Regional Offices in

Asian and European countries. Furthermore,

BSI is the shareholder of two active

independent and two joint venture banks.

With more than 3000 active branches and

a paid-up share capital of Rials 16,803 billion,

BSI runs the largest banking network in Iran. In

2000, BSI started offering electronic services and

now pioneers in the number of online

branches, ATM machines, POS machines, and

issued debit cards across Iran and Middle East

banking systems.

I

ranian Banking System

Iranian banking activities have become

very diverse and the banking industry has

experienced impressive improvement thanks

to IT developments and new banking methods.

Nowadays, banking services are not restricted

to offering loans and taking deposits, but

involve a wide array of financial transactions.

Banking may generally be categorized as

wholesale banking, retail banking, and

comprehensive banking.

Offering financial services and products to

customers is the bank's main mission. A bank's

success depends on its good relationship with

its customers and managing information.

A rapidly-growing banking system and the

importance of money and capital markets in

the country's economy in the1950s necessitated

establishing comprehensive rules governing

monetary and banking operations. On May 28,

1960, Iran Monetary and Banking Statute Bill

was announced to the government under the

title of "The Country's Monetary and Banking

Law" after it was passed by Parliament

Common Commissions. The bill was proposed

to be brought into effect for five years as a pilot

scheme. By appointing the first Central Bank

governor on August 9, 1960 the Iranian Central

Bank was formalized. An independent

bank was thus established to oversee the

transactions and guide the banking and

monetary system and the Central Bank

operations were officially separated from those

of Bank Melli Iran.

After the Islamic Revolution and the necessity

to establish the Islamic economic system in

Iran, a Usury-free Banking Operation Law was

passed to omit usury from banking operation

and to reconcile juridical standards with

banking systems in light of the concept of usury

in Islamic jurisdiction and the contents of fourth

article of the Constitution, stating that all the

rules should comply with Islamic standards.

Before nationalization, the Iranian banking

network consisted of 36 banks. Based on Banks

Merger Plan, officially implemented since

November 1979, the banking network (except

Central Bank) included 3 specialized banks

(Maskan, Keshavarzi, Industries and Mines)

and 6 commercial banks (Melli, Sepah, Mellat,

Tejarat, Saderat, Refah Kargaran). Export

Development Bank was founded as a

specialized bank on July 10, 1991.

According to Credit and Money Council

approvals in 1992 and 2000, Non-banking

Credit Institutions and private banks were

authorized to begin their operation respectively.

Along with these banks, a Ministry of

Communications and IT's affiliate, "PostBank"

offers some banking services.

Usury-free Banking Operations Bill was

presented to the cabinet by the Ministry of

Finance and Economic Affairs on May 5, 1982,

passed by the Parliament on September 1983,

and approved by the Guardian Council.

This law requires that allocating resources and

granting facilities by banks are performed in

terms of Islamic contracts.

I

slamic Banking in Iran

The First Step to Islamizing the Banking

System

After the Islamic Revolution, the necessity to

set up an Islamic economic system was felt as

a major requirement. The most important

action would be eradicating usury from the

banking system so that an economy based on

fairness could be developed. Therefore, in 1979,

some steps were taken for Islamizing the

banking system. These steps can be

summarized as omitting interest and initiating

commissions in the banking system, founding

Islamic bank, and developing Qardh - Al

Hassaneh Funds.

I

nterest Omission and Initiation

of Commission

One of the main requirements to omit interest

and usury from our economy and to reconcile

it with principles of Islamic economy is

developing a system, through which

investments take place based on real social

needs rather than to maximize shareholders'

dividends. The system is required to steer

society's material and immaterial resources

towards meeting the basic needs, using

methods other than the interest rate.

For this reason, the Credit and Money Council

approved a number of changes in the banks'

interest rate structure in its 392nd session dated

December 24, 1979, which were put into action

on March 1980:

1.

The minimum possible guaranteed profit for

the deposits

2.

To specify commissions and the minimum

possible guaranteed profit for the loans and

other credit facilities

In 1982, Usury-free banking operations bill

was presented to Islamic Parliament for

omitting interest and reconciling banking

transactions with Islamic standards. The bill

was ultimately passed on August 30, 1984.

According to this law, the banking system was

aimed at setting up a justice-based credit and

money system, characterized by proper money

and credit circulation, especially money value

maintenance, keeping equilibrium in the

balance of payments, facilitating commercial

exchanges and offering services legally

delegated to the banks.

To secure banking transactions and capital

return in connection with banking facilities,

the law considers the entire contracts made

between the bank and its customers as

indispensable documents subject to the

executive procedures of official documents.

The granted facilities in form of Islamic

Contracts are:

1.

Qardh - Al Hassaneh

2.

Modharebeh

3.

Legal Partnership

4.

Civil Partnership

5.

Direct Investment

6.

Instalment Sale

7.

Lease to Own

8.

Salaf

9.

Je'aaleh

10.

Mozare'eh

11.

Mosaghat

12.

Debt Purchase

13.

Guarantees

G

oals, and Strategic Planning in BSI

1-

Management and Human Resources

Development Projects

A.

The Employees' Performance

Assessment Project

The goal of this project is appraising the

employees' performance to reach a degree of

efficiency and optimum use of the

organization's facilities and resources which is

designed in 4 phases.

In phases 1 and 2, recognizing the bank's

present status and comparative studies under

the title of “knowing the organization's

structure” were completed.

In the third phase, the employees' personal

assessment indices and standardizing them

along with designing the organization's

performance indices with the cooperation of the

department's heads, the representatives of

the organization units and the expert group of

the project, were determined during an

interactive process.

Planning a positive/negative performance

assessment system and estimating the

organization’s performance and personnel

behavior indices has now been put into effect.

B.

Motivating Factors Project

Identifying categorizing and prioritizing the

factors segregated into occupational levels as

well as a study into the current motivating

system in the bank, analyzing the data and

answering letters containing motivating

questions, resulting in a list of motivating and

non-motivating factors.

C.

Appointment and Meritocracy System

Project

The main aim of this project is to design a system

of employees' job promotion and appointment.

To do so, the project is designed in 4 phases,

which the first and the second phases deal with

the present appointment status of the Bank and

the third phase prepares a description of

occupations including the organization status

and structure, job description and engagement

conditions, personal specifications and skills.

Of the most important issues on the fourth

phase is designing an appointment process in

the BSI network, which is done by analyzing

the individual characteristics for any position

and designing a new appointment system

according to 4 factors, i.e. individual

characteristics, skills, motivation, performance.

2-

"The Human Resources

Programming and Provision System

Design" Project

This project, operative in 2008, has the following

important results:

A:

preparing a Human Resources Strategic

Plan for the next five years.

B:

Designing operational improvement plans

for human resource strategies.

C:

Re-engineering the process of employing

staff.

D:

Designing a human resources planning system

through relevant software.

3-

Market Share Projects

In 2007, the BSI Research and Innovation

Department undertook a project named

"Market Management and Research". The

project started with three plans, namely, "BSI

Customers' Satisfaction Assessment", "Iranian

Banking Services Market Categorization for

BSI based on the Bank's Main Goals and

Strategies", and "Customer Relationship

Management System Analysis plus

Contractors' Assessment Pattern and CRM

software" in December 9, 2007. The plans

ultimate outcomes were presented in

September 23, 2008 and were eventually

approved by BSI Board of Directors. The

outcomes were determined to be put into effect

by the related departments.

4-

Increasing Profitability Projects

1)

Improving profitability and financial indices.

2)

Changing organization structures based on

those of private banks.

To implement profitability indices

improvement strategy, BSI undertook

projects about marketing, work-force

productivity improvement, and virtual

banking development. However, improving

financial indices remains under investigation.

M

ission and Vision

BSI Mission

The BSI Mission is to build a lasting

relationship with its clients by giving quality

financial services for the purpose of :

- Promoting economic growth in the Islamic

Republic of Iran

- Giving efficient services to its customers

- Supporting domestic products

- Developing international cooperation

Offering quality services by using innovative

technology and human resources management

in a modern organization culture which is based

on meritocracy while maintaining high ethical

and professional standards.

BSI Vision

The bank’s aims to consolidate its position

as a large international financial group which

meets all its customers' financial needs. For

this purpose, leadership in domestic markets,

public policies, and global reach are taken into

consideration.

Constant search for new products and

services to satisfy the customers' needs and at

the same time outperform competitors in

profitability

Our next purpose is to be the best in all the

markets we take part and achieve the desired

results using knowledgeable experts.

Shareholders

Number of

People

Number of

Stocks

Ownership

Percentage

4163

63

29257

1

1

33485

620,529,003

387,650,997

840,150,000

8,233,470,000

6,721,200,000

16,803,000,000

3.69

2.31

5

49

40

100

Real Entity

Legal Entity

Bank Staff

Islamic Republic of Iran Government

Edalat Stock Agency

Total

P

rivatization

BSI introduction meetings were held on June

3rd, 5th, and 7th 2009 in Dubai, London and

Tehran, respectively prior to offering its stock.

Upon Ministry of Finance and Economic

Affairs'approval to sell BSI stock, 6% was sold

on June 9, 2009, 5% was assigned to BSI staff,

40% to Edalat Stock and the remaining 49%

stayed with the government.

C

orporate & Commercial Banking

Projects

Sugar Cane and Subsidiary Industries

Development Company

Sugar Cane and Subsidiary Industries

Development Company is the biggest group

in cultivating sugar cane and producing sugar

and other products in Iran. This company was

established as per the government's ratified law

in the year ended 20.03.1980. Seven cultivating

and industrial companies i.e. Imam Khomeini,

Amir Kabir, Da'abal Khazai, Mirzakochak Khan,

Salman Farsi, Farabi and Dehkhoda are all its

subsidiaries. The main products of the company

are sugar, paper, livestock food, M.D.F, alcohol

and dry leaven.

The total area under-cultivation of sugar cane

in this company is 84,000 Hectares. Every year,

7 Million tons of sugar cane is obtained from

these units.

The Economic Effects of Sugar Cane

Development Company

Preparing consumable sugar for about 28

Million people with per capita consumption of

25 Kilograms in a year

Preparing consumable paper for about 27

Million people with per capita consumption of

13 Kilograms in a year.

Preparing consumable M.D.F for about 19

Million people with per capita consumption of

5.2 Kilograms in a year

Preparing the facility of producing 80,000

Tons meat by using produced livestock food.

With per capita consumption of 15 Kilograms,

the meat for 5.4 Million people of the country

is provided

Producing biotechnological products (such

as leaven, alcohols, etc) which both have the

domestic use and are exportable

Creating more than 5000 jobs

The granted facilities to the Sugar Cane and

Subsidiary Industries Development Co. Plan

is Rials 5,202.8 Billion by the year ended

20.03.2008

Tose'eh Sakhteman Int. Company

In an area of 220,000 square meters in the heart

of Tehran and its vital highways, Tehran

International Tower has been erected with

more than 160 meters in height as the highest

residential tower in Iran to encourage vertical

construction and to prevent horizontal

development. Having three wide sides, this

tower has 56 floors, consisting of 572 units.

The Bank granted Rials 194.8 billion to the

company.

Abadeh Cement

From the beginning of November 2005, the

development of this factory has been started

with the cooperation of Bank Saderat Iran. The

preparation of this project in less than 2.5 years

with the endeavor of Iranian experts shows

their independence in designing and cement

industry engineering. The factory production

will increase from 500 tons to 1,200 tons a day.

This increase in capacity of production is

significant and will solve the problem of cement

shortage for the ongoing project in this area.

Bank Saderat Iran granted 5.2 Million Euros

and 65 billion Rials facilities to this factory.

Karoon Cement

Karoon Cement factory started its activity from

year ended 20.03.2008 with the capacity of

producing 3,000 tons grey cement per day.

This factory is able to produce different kinds

of Portland Cements according to A.S.T.M

standard and tailored to the orders of

customers. The company has played a great

role in the development and progress of the

country and has increased its production

capacity to reach a higher state in the cement

industry.

Having high technology, the second phase of

executive operation along with the first phase

has been started with a capacity of 3500 tons

grey cement. With the cooperation of BSI,

nominal capacity of the company reached 6,500

tons per day. To help this project, BSI granted

Euro 22.6 Million and Rials 265 billion facilities

by the year ended 20.03.2008.

Larestan Cement

Larestan Cement received Euro 21 Million

facilities.

Abyek Cement

The company received Euro 38 Million equal

Rials 70 billion facilities.

Zabol Cement

Sanaye'e Zabol Co. (joint-stock) was

established with a 51% share of Province

Domestic-Private Section and a 49% share of

Iran Consuming Industries Development and

Renovation Organization (IMIDRO) with the

aim of producing 1 million tons of grey cement

per annum. IMIDRO 49% share was

subsequently put in a bid by Country

Privatization Organization and sold to Province

Domestic-Private Section.

The project has received Rials 63.6 billion

facilities from the bank by the end of 2008.

Perlit Asia Casting Industry (joint-stock)

An amount more than Euro 10 Million was

paid for a factory to be built for casting and

producing cast-iron parts of cars with an annual

capacity of 20,000 tons on a day and night shift

and 275 days per annum basis.

Bahman Group

This company produces Mazda vans, Mazda

cars, Pajero, ambulance, and money delivery

vans and has received EUR 7 million and Rials

33 billion facilities from BSI.

Zanjan-Tabriz Freeway

285 km long Zanjan-Tabriz Freeway is one of

the greatest freeway projects in the country,

being built in 16 segments. The second phase

of this project, funded by Ministry of Roads

and Transport, banks, and the private sector,

for Rials 2,000 billion is underway. This freeway

is a complement to 89-km Tehran-Bazargan

freeway on northwest passage of Iran and

passes the Tabriz Belt, Ghezelcheh-Meydan,

Noori-Gol, Yousef Abad, Bostan Abad,

Maragheh Intersection, Hashtrood and

Ghezeh-Aghaj, Sarcheshm Intersection, and

Bijar Intersection.

BSI has granted Rials 411.4 billion to this

syndicated project by the end of the year 2008.

Apadana Ceram Company

Using modern technology of tile production,

the company produces different kinds of

double-baked enamelled wall tiles, unglazed

porcelain tiles (granite tiles), and enamelled

porcelain tiles, with a nominal capacity of 30

million square meters.

Considering this capacity, Apadana Ceram will

rank as one of the greatest tile producers all

over the world. With the execution of the

development plan, the company would be able

to produce tiles with a capacity of 50 million

square meters per annum.

I

nternational Banking

BSI overseas activity started with Hamburg

Branch in Germany in 1961 and now it has the

largest international FX network in Iran, having

21 branches, 2 regional offices, 2 independent

banks, 3 Joint Venture Banks and 122 FX

branches.

Total number of staff working at overseas

branches and offices equals 523, of whom 449

were local and 74 were dispatched.

BSI overseas branches are now engaging in all

kinds of banking activities such as granting

various banking facilities, opening L/Cs, issuing

letter of guarantees, and money transfers after

following anti-money laundering and Basel II

regulations according to the homeland banking

rules.

BSI overseas branches take full advantage of

their potentialities with respect to the following

factors:

A wide variety of banking services and facilities

tailored to customers' needs

Well-designed regulated system

Quick decision-making

Flexibility in the bank's policy-makings

considering the change in economic conditions

and international financial markets.

It is notable that total profit earned by overseas

units rose to Rls 1,893 billion (USD 195 million)

by the end of 2008, an increase of 17.4%

comparing to the preceding year.

By far, overseas branches operation has led to

a positive result so that their income constitutes

a major part of the total profit across BSI

network. This process of profitability is

predicted to continue in the year to come.

To improve in profitability and international

activity, BSI is expanding its overseas branches.

Hence, establishing new branches in Belarus,

Syria, Malaysia, India, China, and Iraq is under

investigation.The operations of some major

BSI overseas units are as follows:

B

ank Saderat PLC, London

The post -tax profit achieved in the year to the

end of December 2008 was EUR 20.2m, an

increase of EUR 1.9m (10.6%) on the figure

achieved in 2007. This result produced an after-

tax return on equity of 12.4% -another record

result.

It is appropriate to note that the Bank remains

very well capitalized. As at 31 December 2008,

the bank had 340% of the minimum capital

requirement calculated in accordance with the

Base II capital adequacy rules.

Furthermore, against the background of

widespread liquidity shortages in the banking

sector, the Bank continues to enjoy comfortable

levels of liquidity that are more than sufficient

to meet its needs.

The Directors were able to pay an interim

dividend of EUR 6.0m in July 2008, and a final

dividend of EUR 14.9m is to be proposed at

the forthcoming Annual General Meeting.

The Bank continues to exercise tight control

over its mainly Sterling expenses, which are

expressed in Euros for purpose of the annual

accounts. In Sterling terms, the Bank's expenses

increased by only 0.8% in 2008 as compared

with 2007.

No new bad debt provisions were raised during

the year under review.

However, the bank was able to write back EUR

321k of provisions relating to impaired loans.

At the end of 2008, provision against impaired

loans totalled EUR 187k.

The Bank continues to adopt a conservative

lending approach, with most of its commercial

loans being fully secured.

Bank Saderat PLC, a UK bank, complies fully

with FSA regulations, with money laundering

and counter terrorist financing regulations, with

international banking practices and standards

and with the laws of England and Wales.

Bank Saderat PLC has been diligent in

establishing the highest standards of

anti-money laundering systems and controls.

To that end, in consultation with a specialist

anti-money laundering company, the bank has

updated its Manual for Preventing Financial

Crime and introduced an updated set of best

practice procedures that reflect the new

risk-based approach of the Regulator.

All staff have recently undergone further

training, which has been provided by specialist

external consultants.

B

SI Branches in Germany

Total assets increased by about 16% from EUR

516 million in 2007-08 to EUR 598 million in

2008-09 and business volume increased by 10%

from EUR 635 million in 2007 to EUR 699

million in 2008.

Operating capital increased from EUR 39

million in 2007 to EUR 49 million in 2008.

Receivables from banks stood at EUR 179

million, involving balances from current

accounts, clearing balance and time deposits

with domestic as well as foreign banks, of which

EUR 205,000 are in foreign currencies.

Receivables from customers stood at EUR 333

million in 2008 against EUR 338 million in

2007.

Liabilities to customers (deposits) amount to

EUR 60 million in 2008, of which 9.2%

accounts for cash received from customer's

guarantees. BSI branches in Germany are

members of German Deposit Insurance Fund

and all deposits are insured up to EUR 11.5 million.

Provisions made in 2008 were EUR 4 million

against EUR 1.8 million in 2007, which contain

taxes, audit fees, employment cost etc.

Driven by a rising demand at reducing refinance

rates after financial markets crisis, net interest

income increased to EUR 25.6 million.

Net commission income also rose to EUR

6 million. Earnings before provisions amounted

to EUR 26 million in 2008 against EUR 17

million in 2007.

Financial Situation

2008/09

M€

Total assets

Volume of business

Cash

Receivables from banks

Receivables from customers

Liabilities to banks

Liabilities to customers

Clearing balance

Operating Capital

598

699

75

179

333

330

60

132

49

516

635

7

160

338

236

75

140

39

440

495

18

140

272

161

72

164

36

Assets

2007/08

M€

2006/07

M€

B

ank Saderat Iran, Paris Branch

The volume of the transactions of BSI Paris

Branch has slightly been reduced in 2008

compared to 2007, mainly due to the decrease

of the refinancing activities. The profit after tax

for 2008 was Euro7.2 Million compared to

Euro 6.1 Million for 2007(+18.0%).

AS a matter of fact, the profit after tax for 2008

has taken into account the withholding taxes

paid to the tax authorities from 2006 to 2008,

for a total amount of Euro 1.8 Million. Without

these withholding taxes, the profit after tax

for 2008 should have been Euro 9.0 Million,

therefore +47.5% compared to 2007.

The above performance was achieved in a

context of a gloomy French economy, affected

by the global downturn of industrialized

countries. The economic slowdown is being

keenly felt, with corporate bankruptcies and a

higher unemployment rate.

For 2009, perspectives for BSI Paris Branch

seem to remain moderate. On February 1,

2009, all the refinancing transactions of the

documentary credits of BSI Paris Branch have

been assigned to the Head Office, leaving the

Branch the task to manage and to follow up

those transactions which are themselves

recorded in the books of the Head Office.

Revenues for the branch, from then on, are

commissions paid by the Head Office based

on the volume of the transactions handled by

the Branch. To a certain extent, this change

will have an impact on the income of BSI Paris

Branch, regardless of the general economic

situation in France.

Recent forecasts given by IMF and OECD have

shown that no real economic improvement is

expected in 2009, and that the recovery will be

gradual after 2009.

B

SI Branches in the U.A.E

Despite the lack of political stability throughout

the Middle East region , Bank Saderat Iran in

the UAE ( The Bank ) has done very well

during the last five years , our proactive banking

policy continued during the current year, thus,

our trade finance activity, which is our core

business and one of the major sources of our

profitability, continued its growth through

2008.The bank's net profit rose from AED 387

million in 2007 to AED 410 million in 2008.

The upward trend in profit has continued

during the last nine years.

In recent years, the bank has continued its

policy of maintaining a high quality asset

portfolio. Total facilities to customers increased

from AED 3,967 million in 2004 to AED 6,376

million in 2008. The increase represents all

categories of credit and advances, mainly in

trade finance-related areas.

At the end of the year 2008, our lending ratio

was around 87% and Risk Assets ratio was

12.2%.

In the year 2004, after a comprehensive market

study in UAE, the bank launched its first private

banking product called "Balanced Investment

Portfolio". Success of the first private banking

product and the positive feedback from our

valued clients encouraged the bank to offer

another private banking product called

"Conservative Investment Portfolio" in July

2005. The return on these products was far

better than expected and the annual yield

reached 10%.

On January 15, 2008 at the request of our

clients, we launched the third private banking

product which was the extension of our second

product "Conservative Investment Portfolio".

In August 2008, we successfully launched the

fourth private banking product "Conservative

Investment Portfolio - II".

In 2008, our total profit was standing at Dhs

534 million.

Considering our owner's equity of AED 1,306

million, the growth in revenue shows a perfect

capital management. The Returns on Equity

has been 32.2% for 2008, which in comparison

with the other banks in UAE, we are among

the most successful ones.

The bank has also established a full functional

Risk Management Department. The bank has

implemented Basel II in accordance with

CBUAE (Central Bank of UAE) guidelines

and regularly reports to CBUAE.

The bank has performed ICAAP (Internal

Capital Adequacy Assessment Process) as per

Basel II, Pillar II wherein the complete

assessment of risk in the bank was done and

the stress test conducted had a positive result.

In order to keep pace with the changing

banking environment, the bank has capitalized

on staff training and risk awareness programs.

The bank has reviewed and updated the

existing policies and procedures and also

formulated new policies and procedures in

the areas where required.

The bank has successfully completed the

processes project. The processes consist of

various products and services offered across

the bank. The main goal of the project has

been to:

1.

Define a uniform process across all the

branches and departments for all the products

and services.

2.

Identify and minimize the risk at operational

level.

3.

Improve the work process and procedure to

achieve higher efficiency.

4.

A training tool for all staff.

The following table summarizes the bank’s operation results at the overseas units:

2006 2007 2008

million US$ million US$ million US$ Growth (%)

6,050

501

200

174

54.2%

Total Assets

Total Shareholder’s Equity

Net Profit Before Taxation

Net Profit

Percentage of BSI Group Net Profit

2007 to 2008

Million USD

6,361

554

234

172

117.81%

6,092

595

351

195

101%

-4%

7.4%

50%

13.4%

T

echnological Infrastructures

Electronic Banking

Having the largest banking network in Iran,

BSI has started implementing online real time

banking system in the form of SEPEHR Project,

to offer essential and on time services to its

customers. Now after a while, all our branches

offer various online services.

The SEPEHR Project goals are: to strengthen

the banking system's executive authority, to

provide day and night services, to accelerate

banking operations, to diversify into various

quality services, to avoid carrying banknotes,

to have access to updated information for quick

decision-making, to develop more controller

tools, to adapt with international banking and

new banking standards in order to reduce

customers' physical presence at the branches

and to prevent wasting their time and money.

SEPEHR system can provide worthy and

quality services simultaneously all over the

country, using terrestrial and support satellite

telecommunication network and computer

technology. This is a key to electronic

commerce, IT community, and ultimate

development in banking industry.

SEPEHR project exercised great influence on

banking system, on passing from traditional to

modern banking, in BSI network. By adding

subsystems and new capabilities, it turned to

one of the greatest online real time banking

systems in the country. According to statistics

cited by Central Bank of Iran, BSI ranks as the

first bank in terms of the number of POS

machines and transactions, ATM transactions,

centralized accounts, centralized mechanized

branches, and telephone bank customers in

Iran and, in some cases, in the Middle East.

1) Payment of Bills through ATMS and Telephone Banking

2) Offering Internet Banking Services

3) Developing Mobile ATM Services

4) RTGS Services

5) Valued Cheques and Teenage Account Services

6) Developing Intranet Services including Access to Exchange Rate, Circulars, and

Inquiry about Past Records

7) Request for Issuing Substantial Goods Drafts through Intranet

1) Interbank Transactions through Pin Pad

2) Offering Banking Services through Mobile Phones

3) Online Services for FX Accounts (Saving/Current)

4) Initiating Supply, Treasury, and Human Resources Holistic Systems

5) Using Customer-ranking System to Reduce Outstanding Debts while considering

Risk Management

6) Developing POS

1) Developing Internet Banking Products and Services

2) Developing Mobile Banking Services

3) Designing Centralized SEPEHR System in Bank Internal Accounts

(Debits, Credits, and etc.)

4) Developing Gift Cards, Credit Cards, Smart Cards and Pin Pads

5) Designing and Initiating Advance Cards, Special Cards, Virtual Cards and SEPEHR

Money Cards

6) Completing SEPEHR Supporting Network, Initiating Intranet Supporting Site,

Improving Physical and Virtual Security of the Sites

7) Selling IranCell and Talia Credits through ATM

8) Preparing a Holistic Financial System and Developing Interbank Markets

Description of the Major Subsystems

2006

2007

28

50

2008

60

Year

Total

Number of

Subsystem

The following tables show the highlights of new banking services during the period 2006-2008:

The Latest Information Technology in BSI

6,000,000

5,000,000

4,000,000

3,000,000

2,000,000

1,000,000

0

Debit Card

2007

2008

2007

2008

Performance of

2008

Development of Electronic Banking Services

Development of Mobile Banking Services

Development of Gift Cards

Development of Credit Cards

Development of ATMs

Development of POSs

Development of Pin Pads

75,991

61,862

30,396

59,526

1,919

171,394

4,920

Description of the Plan

Performance of

2007

31,195

200

_

21,276

1,655

85,000

4,719

1

2

3

4

5

6

7

Statistical data and status of the new banking products and services during the years 2007

and 2008:

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

2007

2008

2007

2008

Credit Card

ATM

2,000

1,900

1,800

1,700

1,600

1,500

2007

2008

2007

2008

POS

200,000

150,000

100,000

50,000

0

2007

2008

2007

2008

H

uman Resources

It is obvious that despite human society advances and moves towards the information age,

the workforce plays an important role as an organization's greatest wealth. Having more than

30,000 employees and taking advantage of educated and experienced personnel, BSI has committed

them to giving top priority to the customers' satisfaction.

Workforce Breakdown by Educational Level (Feb 2009)

Workforce Breakdown by Age (Feb 2009)

Workforce Breakdown by Occupational Category (Feb 2009)

Workforce Breakdown by Work Experience (Feb 2009)

Educational

level

Percent

Secondary

School

High School

Diploma

Associate

Degree

Bachelor

Degree

Doctorate

Total

9.02

49.38

10.52

29.69

1.37

0.02

100

Percent

Total

4.02

100

Age

Under 25

years old

26 - 35

Years old

36 - 45

Years old

More than

46 years old

29.15

52.37

14.46

100

Percent

Total

100

Occupation

Management

Specialized

Operative

33.72

5.38

60.90

Percent

Total

100

History of

occupation

Less than

5 years

5 to 10

years

10 to 15

years

15 - 20

years

20 to 25

years

25 to 30

years

More than

30 years

22.28

9.01

7.80

33.03

24.59

3.25

0.03

Masters

Degree

F

ree Trade Zones

The Free Trade Zones have been established

to enhance exports, reduce importing costs,

develop the private sector, support the areas

with potential for investment, absorb domestic

liquidity, new job opportunities and attract

investments especially foreign ones.

Free Trade Zones Regional Office is now

operating with 138 staff in front and back

offices, 17 branches, 9 counters and 5 FX

branches.

At present, The Free Trade Zones branches

are located in Kish, Qeshm, Chabahar, Djolfa,

and Anzali and Arvand Free Zones branch is

underway.

Fiscal year

2006

2007

2008

Attraction IRR

Resources

IRR Loans

Granted

Attraction FX

Resources

1,399,724

1,358,931

6,239,474

482,756

300,930

556,855

143,092

519,409

344,409

Free Trade Zones Resources and Loans

R

isk Management

In Banking, Risk Management has developed

through diverse banking services, intense

competition, innovations and the market

development. Risk Management, thus, includes

all kinds of tools, methods and risk operating

procedures in banks.

As the mediators for attracting and offering

resources, banks always face different kinds of

risks such as credit risk, market risk, liquidity

risk, operational risk and so on. Hence, ignoring

risk management may make the banks suffer

enormous expenses and lead them to

bankruptcy or serious financial crises. As a

result, establishing risk management system,

as a management tool, is essential for a bank

to ensure authentic activity and reduced

vulnerability and to prevent potential loss to

the shareholders' equity and other assets. This

can be achieved through investigation,

identification, analysis, proper decision-making,

and intelligent management.

With respect to the status, special structure,

numerous branches inside and outside of the

country, plentiful customers, long history and

good reputation in banking industry, BSI felt

obliged to maintain an efficient risk

management system to maximize profit and to

reduce potential loss to shareholders' equity

and other assets.

C

redit Risk Management

Credit risk is based on non-repayment of

principle and interest of loan at maturity by the

borrower. Credit risk may be defined as the

exposure of credit portfolio to probable

outstanding, doubtful or bad debts due to

internal factors (weakness in credit

management, internal controls, or supervision)

or external factors (economic depression, crisis,

and etc.).

Credit risk can be controlled by resource

allocation adjustment for different activities,

customers' credit level assessment and getting

enough guarantees. Key factors in credit risk

are:

Lack of a management system and composition

for credit portfolio

Lack of a systematic customer identification

procedure

Non-recognition of the required cash

Lack of experienced experts

T

aken Steps to Reduce Credit Risk in BSI

Investigating the status quo regarding KYC

(Know Your Customer).

A study into determining a proper pattern

for customer-ranking system.

Specifying effective indicators in ranking.

Developing "Special Customers Identification"

project.

Preparing software program for ranking

customers with the assistance of creditable

companies.

Assenting to Credit Assessment System,

affirmed by Central Bank of Iran, which has

come into operation by Ranking Counseling Co.

Examining and naturalizing Basel II

recommendations through standardizing

banking operations at international level.

Preparing new reporting forms for credit

information to use in ranking program.

Creating customers data bank

L

iquidity Risk Management

Liquidity risk in banks results from liquidity

shortage and lack of confidence. Cash adequacy

provides the possibility of paying liabilities and

depositors' liquidity requirement on due date.

Taken Steps to Reduce Liquidity Risk:

In order to reduce liquidity risk, BSI has set up

a liquidity management task force to plan an

optimum assets management system in a way

that a parallel between liquidity and profit be

made. BSI has also attempted to synchronize

assets maturity date with liabilities maturity

date to more reduce the risk.

C

apital Adequacy Risk Management

Capital adequacy ratio represents the extent to

which the depositors and creditors are

supported against unprecedented losses.

According to Capital Adequacy Bylaw

approved by Money and Credit Council dated

February 14, 2004, adequate capital is a

necessity for a healthy bank system. To

guarantee a stable status, banks and credit

institutions ought to maintain a proper ratio

between capital and risk in their assets. This

ratio helps protect banks, depositors and

creditors, against unprecedented losses and has

been determined to be at least 8% as per the

Central Bank of Iran's regulations.

P

rofit Rate Risk Management

Profit rate risk can be investigated from "granted

facilities" and "deposits" point of view.

Using the data on the revenue resulted from

income assets and the costs of the profits paid

to depositors, and the shares of the resources

and facilities, one can calculate the profit rate

difference, which can be viewed as one of the

most important criteria for looking into this

kind of risk.

The positive difference between BSI deposit

rates and those of the private banks shows that

BSI procedure is consistent with the law of

profit rate rationalization.

M

arket Risk Management

One of the subcategories of market risk,

exchange rate risk is caused by exchange rate

fluctuations. The risk receives even more

attention when foreign investment, L/C and

L/G-related activities form a major part of a

bank's portfolio.

To reduce exchange rate risks, BSI has

conducted a series of studies as follows:

The effects of exchange rate fluctuations on

the bank's portfolio

To specify a model suitable for the bank to

calculate risk level

To specify the optimum exchange rate

portfolio with respect to risk level of every single

currency

O

perational Risk Management

Operational risk is defined as the risk of loss

resulting from inadequate or failed internal

processes, people and systems, or from external

events. Basel II has given guidance to 3 broad

methods of Capital calculation for Operational

Risk

1- Basic Indicator Approach

2- Standardized Approach

3- Advanced Measurement Approaches

Quantifying operational risk is the most

important challenge for the bank, allowing for

calculating the capital allocation to meet the

contingencies.

Considering the increasingly widespread

banking operations and the implications of

operational risk for banks' efficiency and

profitability, BSI has taken major steps to tackle

the problems as follows:

Initial identification of operational risk in

the bank

Designing a questionnaire to carry out a poll

of different units in the bank

Gathering the answer sheets to determine

the final results

Specifying the contingencies and damage

resulted from the risk

Estimating the degree of damage using

statistics

Selecting an effective model for calculating

the minimum required capital

A

nti-Money Laundering

3- "Systematizing Suspicious Operations Reports Received from Branches" Software

Program

The software was designed for statistical analysis of suspicious operations reports received from

branches based on Central Bank of Iran predetermined formats and launched in bank since

February 23, 2009.

2008

Job title

2007

Management

Specialized

Executive

172

93

176

2,250

332

1,409

BSI Anti-Money Laundering Department

officially started its operation on April 17, 1999.

The department took remarkable steps toward

fulfilling the bank's senior management goals

and implementing the regulations regarding

anti-money laundering in compliance with

international organizations standards. A

summary of these steps are as follows:

1- Naturalization and Preparing Know

Your Customer (KYC) Instructions

It includes four parts: Customer Acceptance

Policy, Customer Identification Procedures,

Ongoing Monitoring of Accounts, and Risk

Management.

2- Training Programs

With regard to the importance of staff training

and creditable international organizations

emphasis on the role of trained staff in executing

anti-money laundering rules, BSI has offered

some training courses and is planning to

continue them to inform all the staff of money

laundering and the ways to fight against it.

The following table shows the number of trained staff in 2008

compared with its previous year:

4- Anti-Money Laundering Committee

Since BSI Anti-Money Laundering Department

establishment, a number of meetings, attended

by the Committee members, have been held

to discuss suspicious operations reports

received from branches.

5- Suspicious Transactions Recognition

Software System (AML System)

With respect to the importance of systematizing

Anti-Money Laundering process and providing

Suspicious Transactions Recognition Software,

BSI has started producing the latter in order to

install subsystems such as Suspicious

Transactions Recognition Software and Anti-

money Laundering Software.

6- Branch Performance Form concerning

Anti-Money Laundering

After a full-scale investigation into the existing

rules and conforming to the standards of

International Organizations, an Anti-Money

Laundering Investigation Form was prepared,

which was at the Inspectors' and Auditors'

disposal all over the country.

H

ighlights of BSI Success in International and National Arena

International Arena

Won "Best Islamic Financial Institutions

Award" 2008 awarded by Global Finance

Best Islamic Bank in Iran in 2006 by Islamic

Finance Institute

Won the Award for Best Debt House in Iran

2005 awarded by EUROMONEY magazine

Awarded the "Bank of the Year 2001-Iran"

by The Banker magazine

National Arena

Ranked No.1 among Subsidiary Organizations

of Ministry of Finance and Economic Affairs

in 2009

Best Electronic Bank in 2004

Second best Bank of Iran in 2003

Ranked No.1 in Offering Services in 2004

Ranked No.1 in Responsiveness

Most Preferred Bank in Islamic Banking

Chosen Bank by Ministry of Finance and

Economic Affairs

F

inancial

P

erformance

F

INANCIAL PERFORMANCE

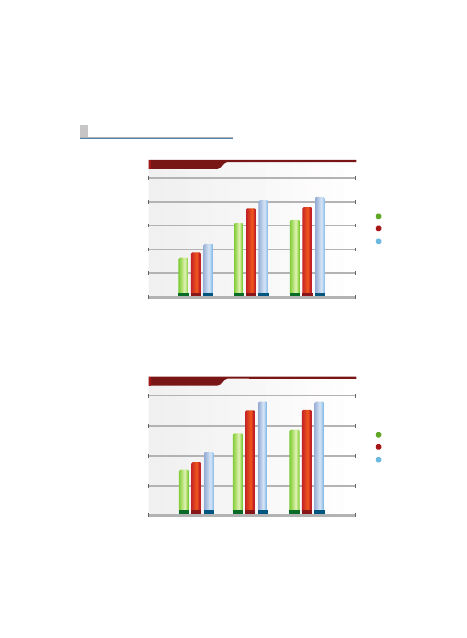

Total Assets

500,000

400,000

300,000

200,000

100,000

0

In Billion RLS

2006

2007

2008

Network

Group

BSI

198,189

235,943

172,295

370,895

404,588

305,583

386,263

408,185

319,910

BSI Group's total assets increased by 5.7% from Rls 386,263 billion in 2007 to Rls 408,185 billion

in 2008 . This mainly resulted from Cash, Due from Government ,Facilities Granted and Claims

from Private Sector.

Total Liabilities

400,000

300,000

200,000

100,000

0

In Billion RLS

2006

2007

2008

BSI

Network

Group

178,559

212,193

152,789

351,250

379,638

286,179

356,082

379,674

289,61

1

BSI Group's total liabilities increased by 6.6% from Rls 356,082 billion in 2007 to Rls 379,674

billion in 2008. This mainly resulted from due to Central Bank and Term Investment Deposits.

Wyszukiwarka

Podobne podstrony:

Final 47 100 Non Back

121220142825 bbc english at work episode 46 final

46 practice final exam

Treating Non Specific Chronic Low Back Pain Through the Pilates Method

Architecting Presetation Final Release ppt

od 33 do 46

Opracowanie FINAL miniaturka id Nieznany

Hine P Knack and Back Chaos

46

Neural networks in non Euclidean metric spaces

Art & Intentions (final seminar paper) Lo

46 zasad zdrowego rozsadku(1)

09 1993 46 50

43 46

Microwaves in organic synthesis Thermal and non thermal microwave

GMap MVT dedykowany back end dla potrzeb wizualizacji zjawisk meteorologicznych w środowisku Go

MPO 2007 46 547

bluzka 21size 46

więcej podobnych podstron