1

PENSION FUNDS

_______________________

1

Marijana Ćurak - University of Split, Faculty of Economics

Academic year 2014/2015

10/23/2014

International Week – New Frontiers in Finance and Accounting 2014

University of Economics in Katowice

Course: Financial Institutions

These lecture slides are based on the

book:

Mishkin F. S., Eakins, S. G. (2012), Financial

Markets + Institutions, Addison Wesley

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

2

AGENDA

Introduction

Defined-benefit and defined-contribution

pension plans

Private and public pension plans

Review points

Marijana Ćurak - University of Split, Faculty of Economics

3

10/23/2014

2

INTRODUCTION (1)

A pension fund is a financial institution that

accumulates contributions over an individual’s

working years and pays out pensions during the

retirement years

Institutional investors

Pension plans are rapidly growing

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

4

INTRODUCTION (2)

Population ageing has been one of the main

driving forces behind pension policies and

reforms in the past two decades

The degree of ageing is measured with the

Dependency ratio: the number of people of pension

age (age 65+) relative to the number of people of

age 15-64

Support ratio: the number of people of working age

relative to the number of pension age

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

5

INTRODUCTION (2)

Ageing is the result of two demographic

changes:

Decline in the number of births

Increasing life expectancy

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

6

3

INTRODUCTION (3)

Fertility rates averaged 1.74 across OECD

countries in the period 2010-15, well below the

level that ensures population replacement (the

number of children needed to keep the total

population constant)

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

7

INTRODUCTION (3)

Additional life expectancy at age 65 for

the period 2060-2065:

Women: 25.8 years

Men: 21.9 years

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

8

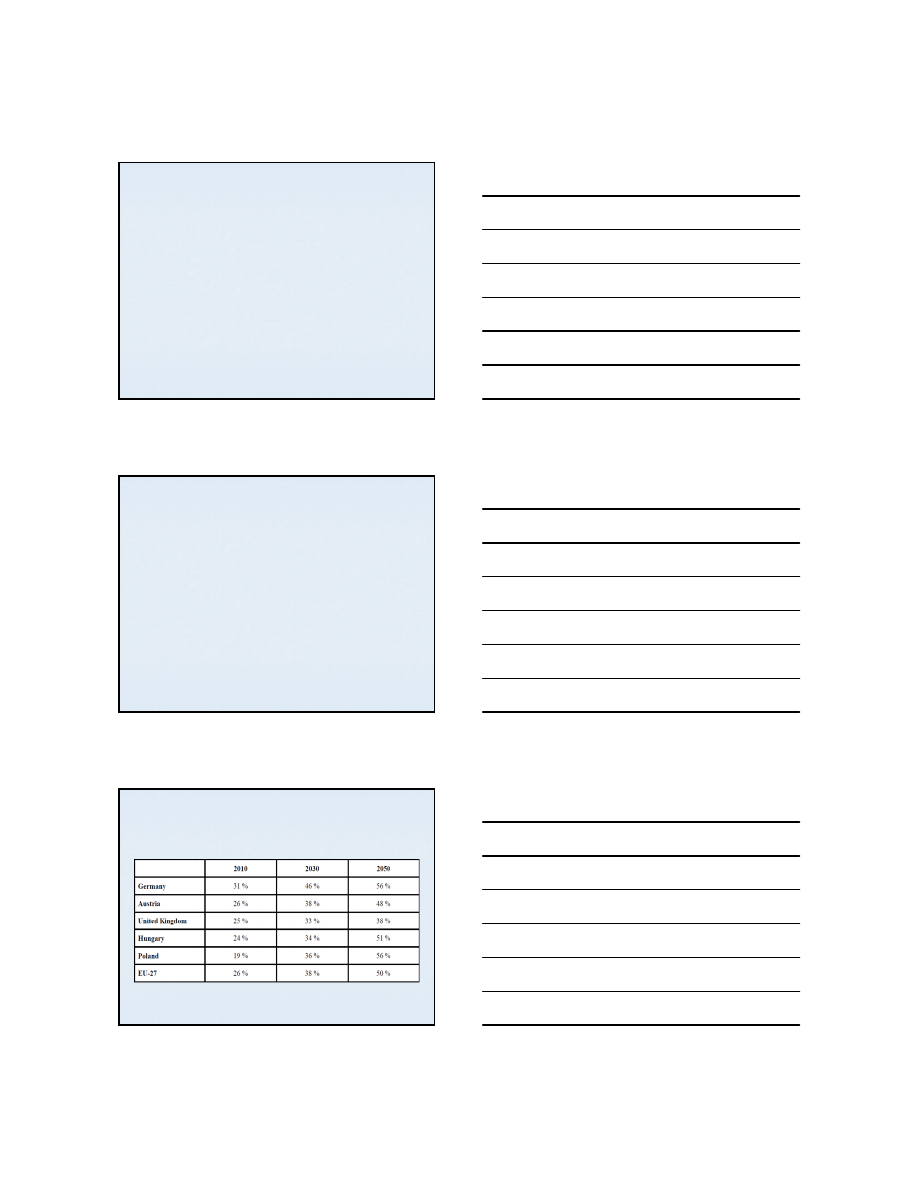

DEMOGRAPHIC DEPENDENCY RATIO

(AGE 65 + RELATIVE TO AGE 15-64)

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

9

Source: Wöss (2011)

4

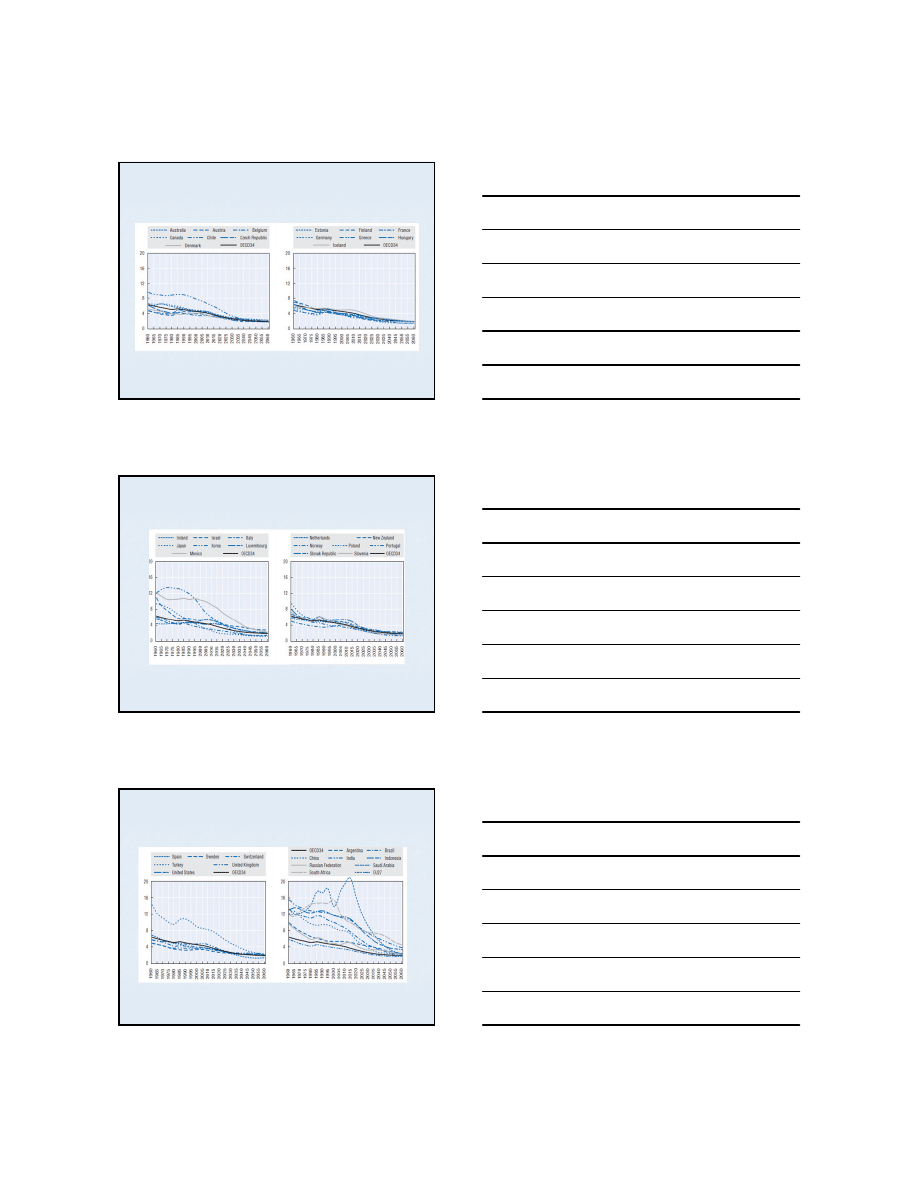

OLD-AGE SUPPORT RATIO (1)

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

10

Source: OECD

OLD-AGE SUPPORT RATIO (2)

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

11

Source: OECD

OLD-AGE SUPPORT RATIO (3)

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

12

Source: OECD

5

TYPES OF PENSIONS

Defined-benefit

plans

Defined-

contribution plans

Private pension

plans

Public pension

plans

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

13

DEFINED-BENEFIT PLANS (1)

Under a defined-benefit plan, the plan

sponsor promises the employees a specific

benefit when they retire

The payout is usually determined with a

formula that uses the number of years

worked and the employee's salary

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

14

EXAMPLE – FORMULA (1)

Annual payment = 2% x average of final 3

years’ income x years of service

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

15

6

EXAMPLE – FORMULA (2)

If a worker had been employed for 35 years and

the average wages during the last three years

were $50,000, the annual pension benefit would

be

0.02 x 50.000 x 35 = 35,000 per year

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

16

DEFINED-BENEFIT PLANS (2)

The plan puts the burden on the employer to

provide adequate funds to ensure that the

agreed payments can be made

Fully funded – if sufficient funds are set aside by

the firm for this purpose

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

17

DEFINED-BENEFIT PLANS (3)

Overfunded – if more than enough funds

are available

Underfunded – if insufficient funds are

available

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

18

7

DEFINED-CONTRIBUTION PLANS (1)

Instead of defining what the pension plan will pay,

defined-contribution plans specify only what be

contributed to the fund

The retirement benefits are entirely dependent on the

earning of the fund

They are becoming popular – the burden is put on the

employee rather than the employer to look out for the

pension plan’s performance (this reduces the liability of

the employer)

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

19

PRIVATE PENSION PLANS

They are sponsored by employers, groups, and

individuals

They are increasingly investing in the stock

market

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

20

ASSET STRUCTURE

Stocks

Government securities

Corporate bonds

Foreign bonds

Money market instruments

Deposits

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

21

8

PUBLIC PENSION PLAN

The plan that is sponsored by a

governmental body

“Pay-as-you-go” system

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

22

REVIEW POINTS

Pension plans are rapidly growing as a

result of population ageing

There are two primary types of pension

plans: defined-benefit and defined-

contribution

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

23

REFERENCES

Mishkin F. S., Eakins, S. G. (2012): Financial Markets +

Institutions, Addison Wesley

OECD (2013): Pension at a glance – OECD and G20

indicators, OECD

Wöss, J. (2011): The impact of labour markets on

economic dependency ratio – Presentation of

Dependency ratio calculator, http://www.oegj.at/servlet/

(Accessed: October 18, 2014)

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

24

Wyszukiwarka

Podobne podstrony:

hedge funds

ROLE OF THE COOPERATIVE BANK IN EU FUNDS

910096-discussion-pension-reform-proposal, Studia, licencjat

Mutual Funds

Sovereign Wealth Funds

hedge funds

(Trading) Gregory Connor and Mason Woo Introduction To Hedge Funds (2003)

2003 06 pension roulette

Joyce, James La pensión

03 una pensionata beffata da due attori truffatori

więcej podobnych podstron