Italy Country Report

February 2008

1

CONTRACT

SI2.ICNPROCE009493100

IMPLEMENTED BY

FOR

DEMOLIN, BRULARD, BARTHELEMY

COMMISSION EUROPEENNE

- HOCHE -

- DG ENTREPRISE AND INDUSTRY -

Study on Effects of Tax Systems on the Retention

of Earnings and the Increase of Own Equity

Jean ALBERT

Team Leader

- ANNEX 12 -

- ITALY –

- COUNTRY REPORT -

Submitted by Raffaele Di LANDRO

Country Expert

February 15, 2008

ITALY

Dottori Commercialisti Associati

Raffaele Di Landro

Corso Porta Vigentina 35, Milano

ITALY

+39 02 58201406

INTRODUCTION

The tax reform of 2004 introduced in Italy a number of changes, such as:

• Partecipation exemption,

• Thin capitalization,

• Suppression of the tax credit on the dividends and the partial exemption of the

dividends received,

• Tax consolidation,

• Tax transparency for Limited companies.

Every year different developments are introduced.

For example, in 2005 the Partecipation exemption was modified (only the 9% of the

Capital gains contributes to the tax basis).

In 2006 there were many changes concerning VAT regarding buildings.

Italy Country Report

February 2008

2

Italy Country Report

February 2008

3

PART 1 – GENERAL QUESTIONS

1. What are the main characteristics of the tax systems applicable on enterprises

and business owners in your Country (corporate income tax, income tax,

capital gains tax, other profit based taxes, capital based taxes, other taxes)?

Corporate income tax (IRES)

Corporations pay taxes on the basis of the net income adjusted according to tax

provisions.

The tax is levied at the rate of 33%

IRAP- Local tax on productive activities

IRAP is computed on the gross margin basis, as shown in the statutory financial

statements, with adjustements due to tax provisions.

The ordinary Irap rate is 4.25%

Personal income tax

The individual persons are taxable on the total income received (building, wage,

capital, enterprise, others, independent work)

All the income received contributes to the tax basis on wich the individual pays IRPEF

(personal income tax).

The tax rate is progressive from 23% to a maximum of 43%

Capital Gains

The capital gains realized by a corporation are considered as revenue that is included

in the tax basis for Ires.

The capital gains ( i.e. sale of shares and buildings) realized by an individual are

taxed as other income that contributes to the tax basis for the personal income tax.

Individuals also pay Irap in case of independent work or business activity

There are not other direct taxes on profits and on capital.

1

D.P.R. 917, 22/12/1986

2

D.LgS. 446, 15/12/1997

3

D.P.R. 917, 22/12/1986 art. 6

4

D.P.R. 917, 22/12/1986 art. 11

5

D.LgS. 446, 15/12/1997 art. 3

Italy Country Report

February 2008

4

1.1. Corporate

1.1.1

What are the general principles for the computation of taxable

profits?

The computation of taxable profits is based on the operating result adjusted to

specific tax requirements. The general principle is based on the taxation or not of

specific elements of profits and on the deduction or not of specific elements of cost

1.1.2

What are the main differences between the tax balance sheet and

commercial balance sheet?

In Italy a tax balance sheet does not exist. Only the net income is adjusted according

to tax provisions.

1.1.3

What are the most important adjustments for the computation of

taxable profits/taxable gains on the base of accounting profits?

For example: entertainment expenses, directors wages not paid in the year, taxes

(Ires, Irap, ICI).

1.2. Income

1.2.1. What are the general principles of income taxation of business

owners on business income, wages, distributed earnings, interest on

loans and capital gain (sale of shares)?

For individual persons - business owners all kind of incomes are taxable on the basis

of Irpef (Personal income tax) regulation. Irpef is levied at different progressive

6

D.P.R. 917, 22/12/1986, art. 83

7

D.P.R. 917, 22/12/1986, art. 11

Italy Country Report

February 2008

5

1.2.2. Is there a different tax treatment for income from different income

sources?

In case of individual persons all kinds of income are computed as the whole personal

income subject to Irpef rates.

1.3. Capital

1.3.1. Is there a different tax treatment between distributions of earnings

and capital gains realised by the sale of the business or the shares

in the undertaking?

In case the seller is an individual person, the sale of the shares is taxed on the basis

of personal income tax:

• 40% of the capital gain is taxed in case the shareholding is higher than 20% or

than 2% (in case of listed company)

• If the shareholding is lower than 20% (or 2% ) the capital gain is taxed on the

basis of 12,5% rate

In case the seller is a corporation, the capital gain is taxed on the basis of the

corporation tax.

The sale of the business is subject to the corporation tax in case the seller is a

corporation or it’s subject to the personal income tax in case the seller is an

individual person

1.3.2. Are there different tax treatments for long-term capital gains and

short-term capital gains?

8

D.P.R. 917, 22/12/1986, art. 67

9

D.P.R. 917, 22/12/1986, art. 86

Italy Country Report

February 2008

6

No.

1.3.3. Are there different tax treatments for capital gain from SME business

stock and capital gain from larger companies’ business stock?

No.

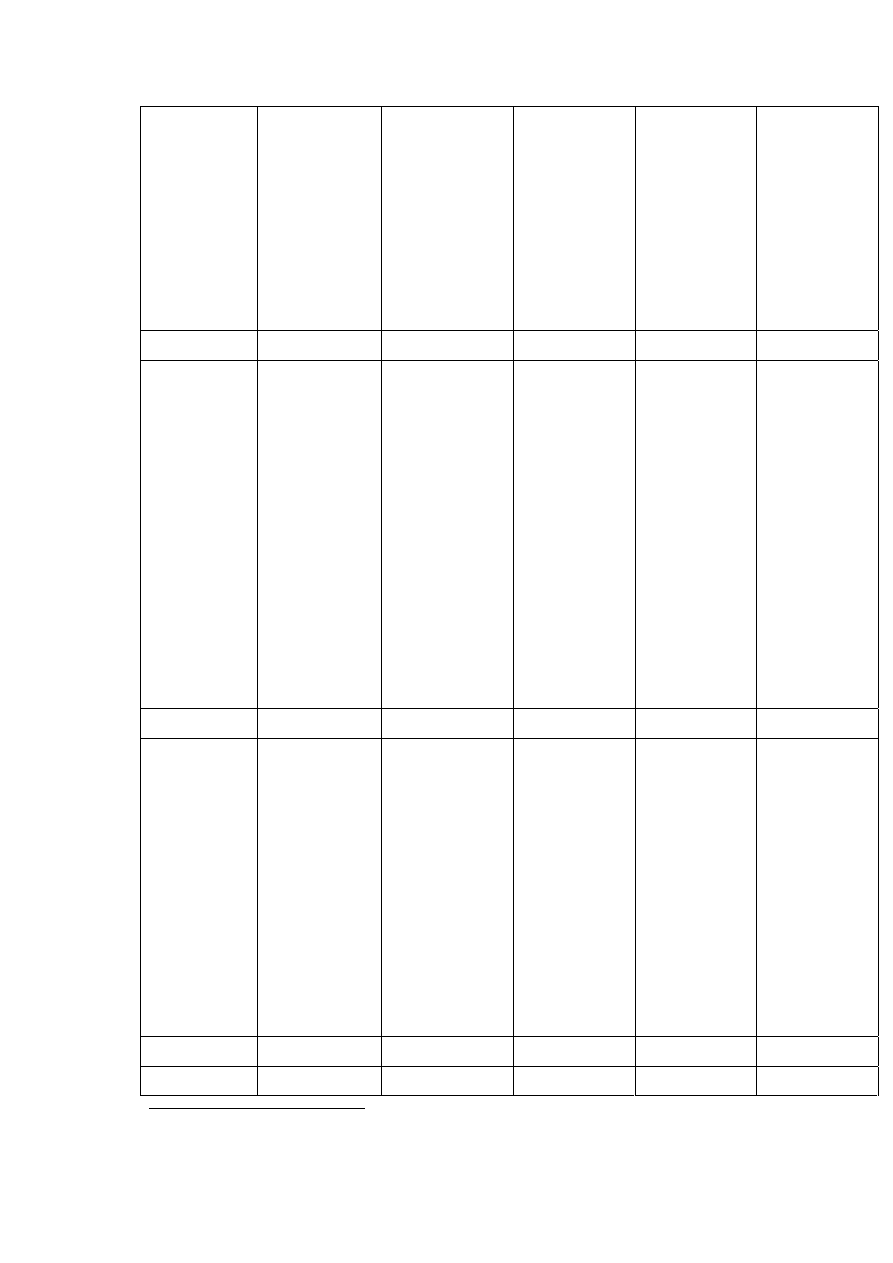

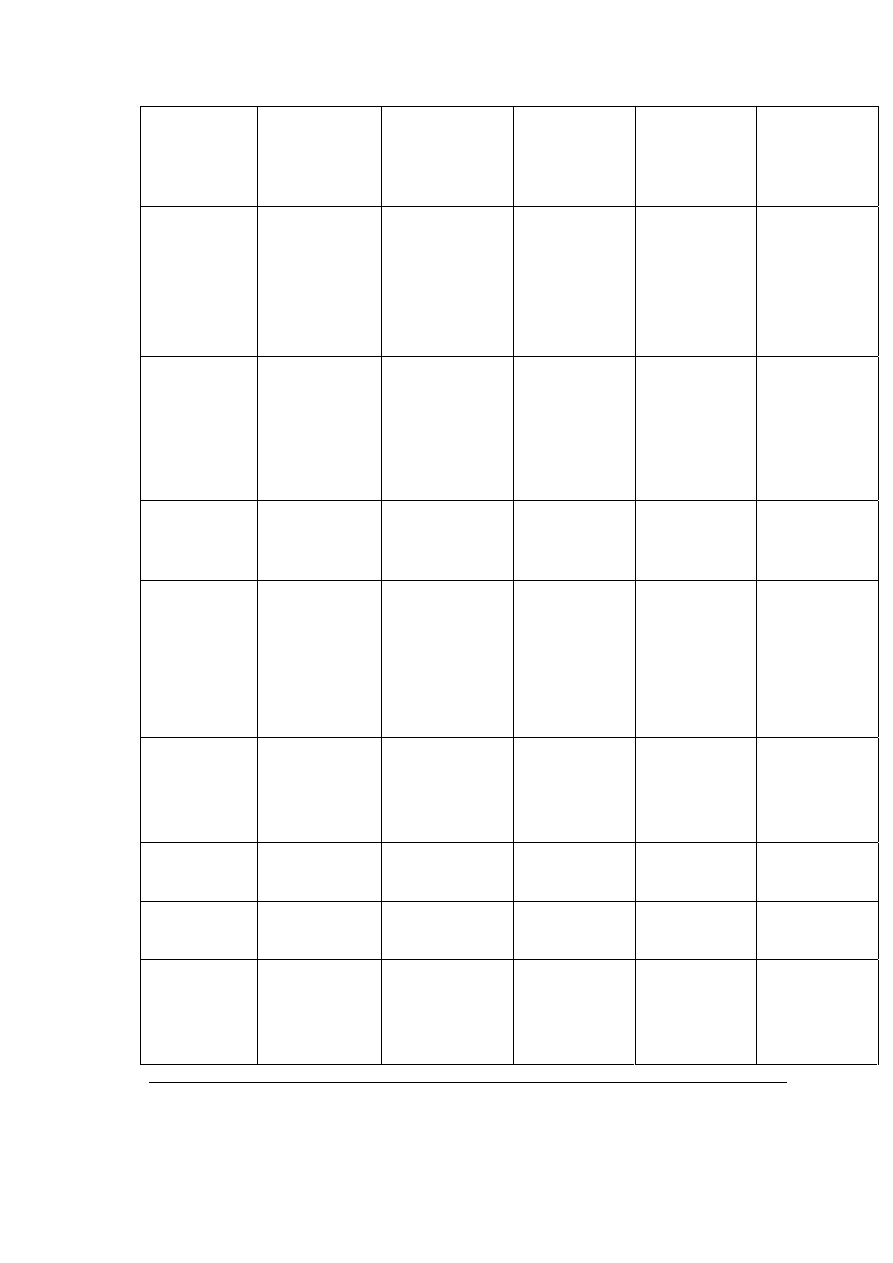

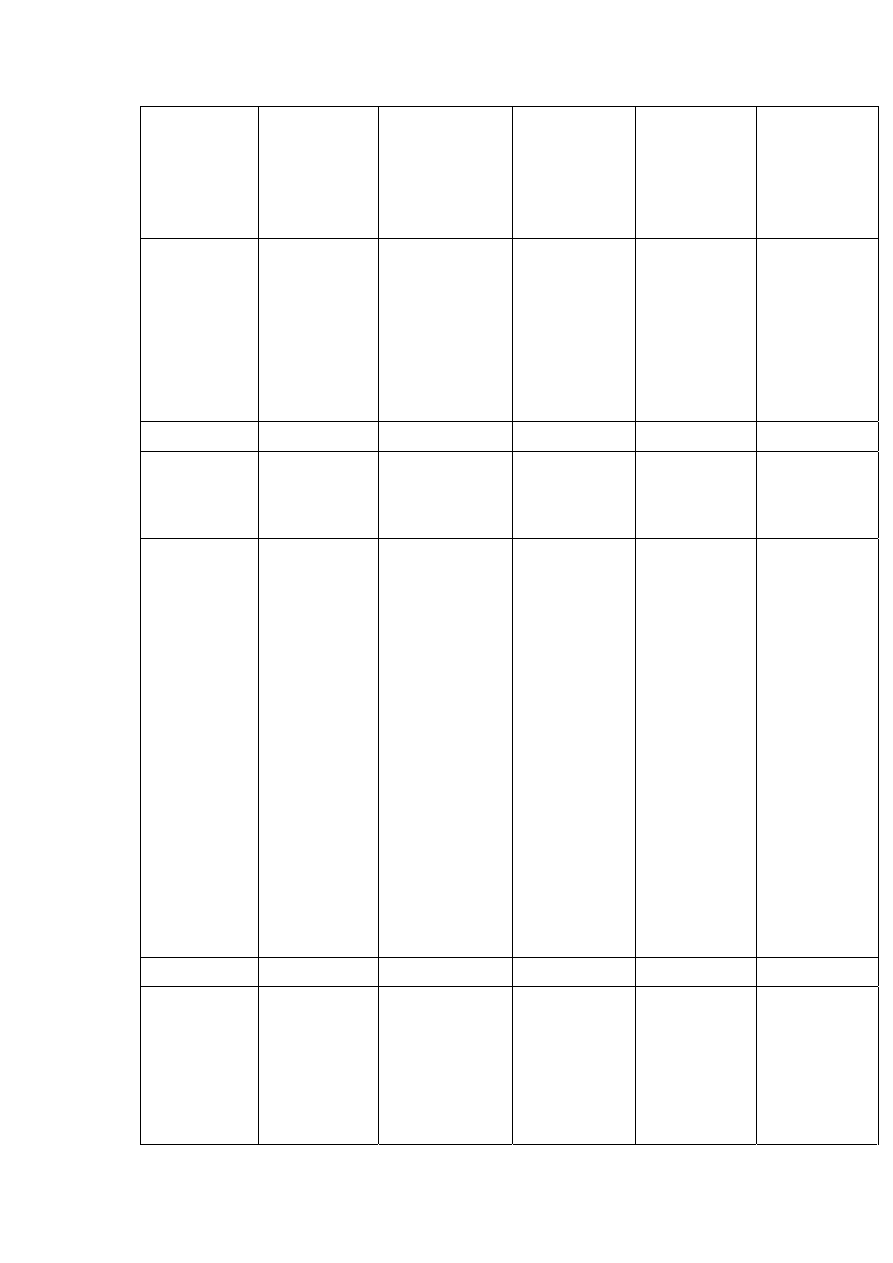

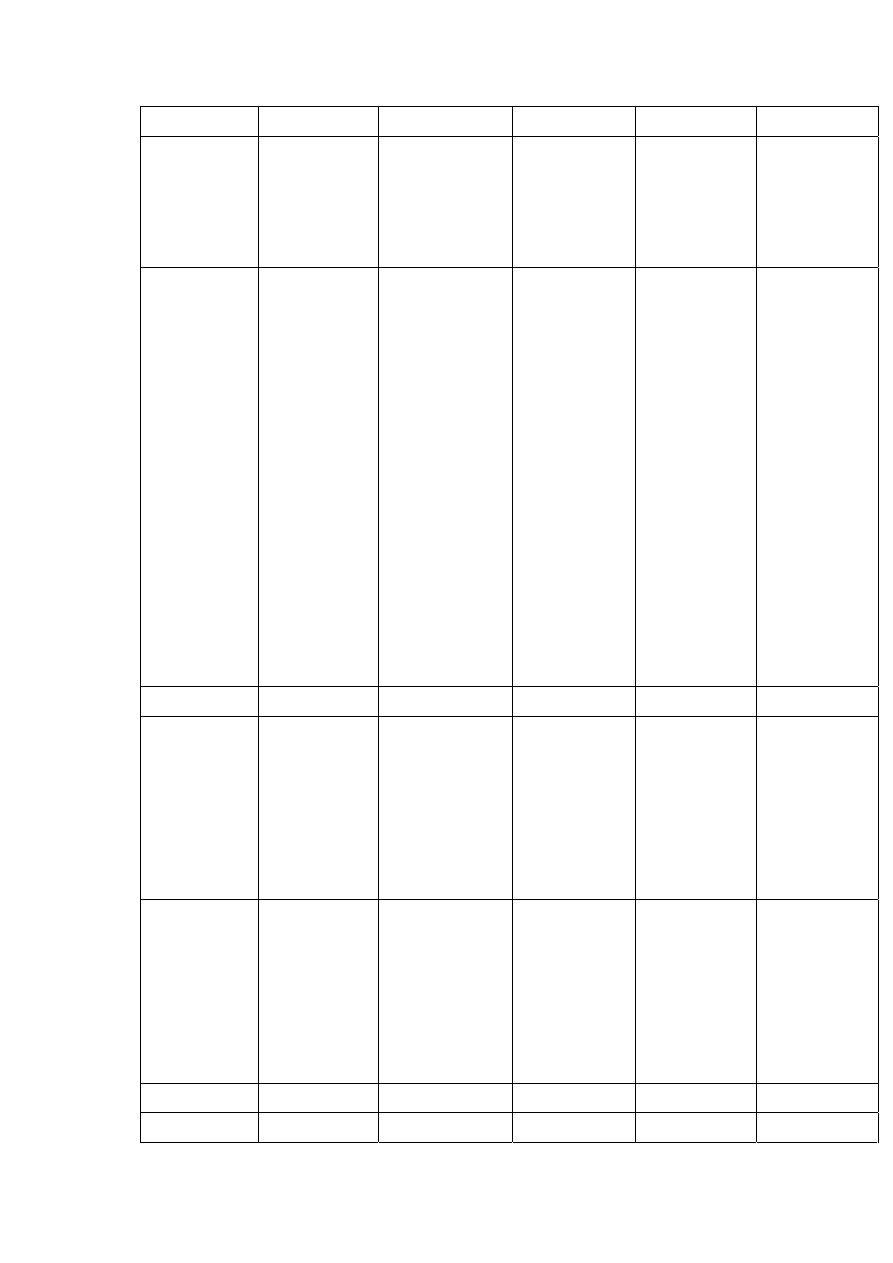

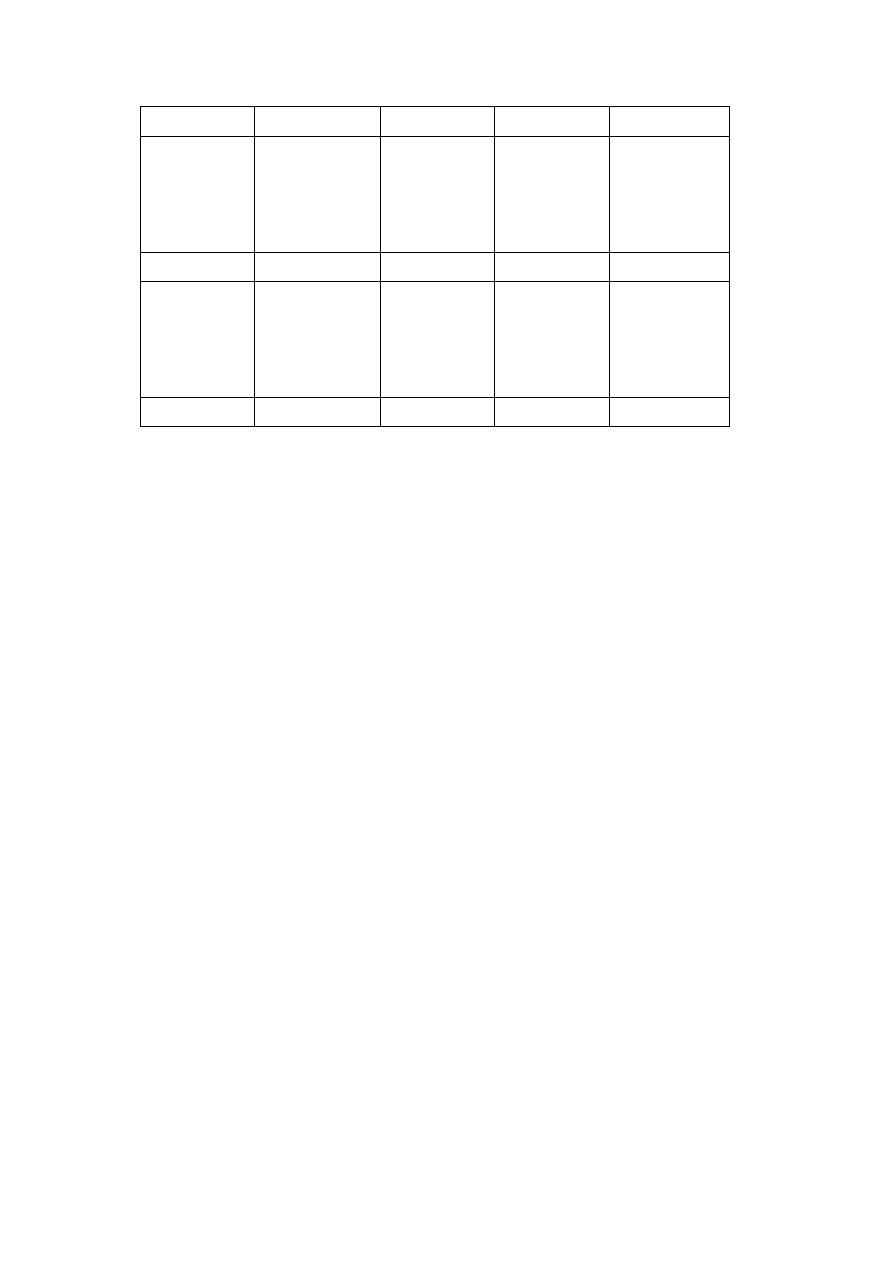

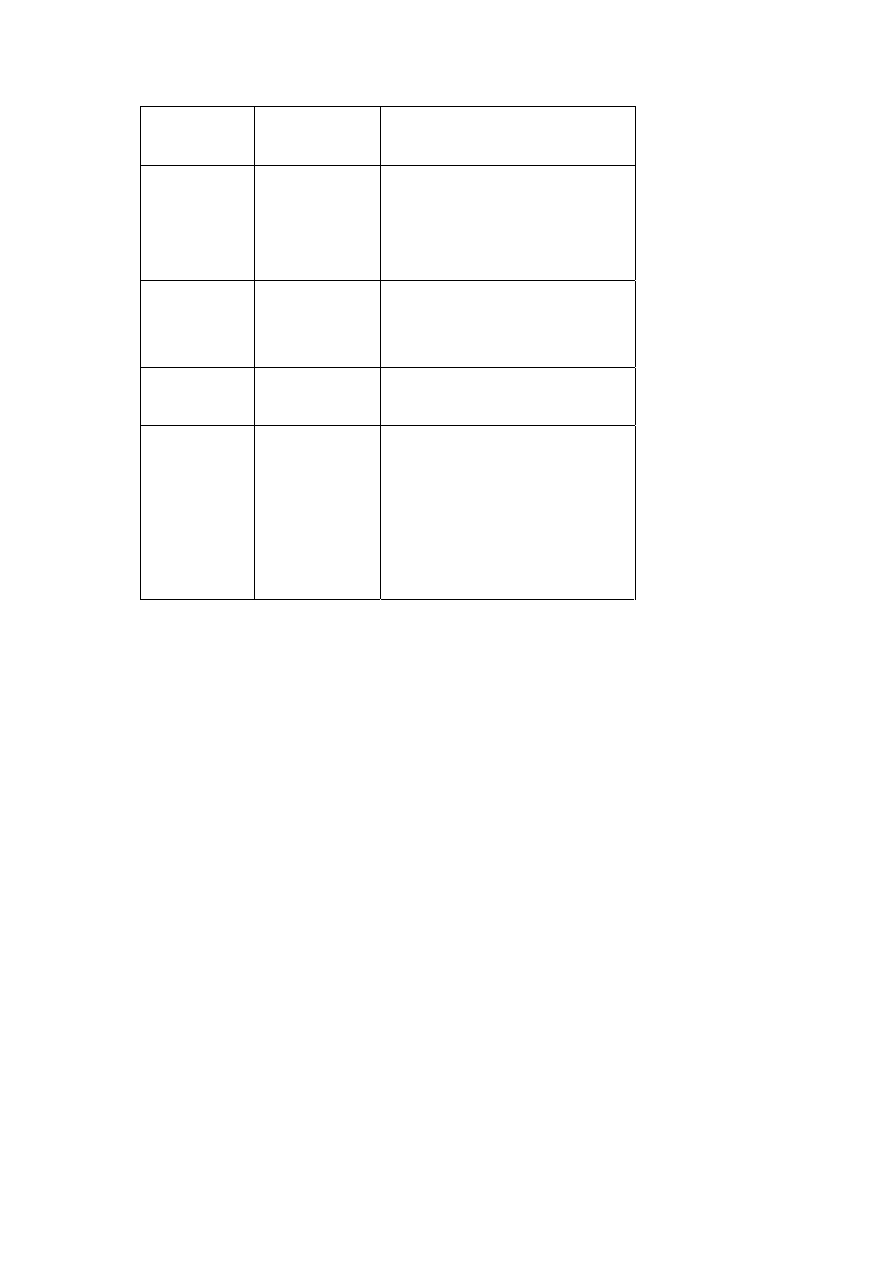

ITALY

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES

For CORPORATIONS (distinguish specific tax rates for SMEs)

2002

2003

2004

2005

2006

Corporate

tax

1. Tax rate

Standard

Irpeg (36%)+ Irap

(4.25%) = 40.25%

Irpeg (34%)+ Irap

(4.25%) = 38.25%

Ires (33%)+ Irap

(4.25%) =

37.25%

Ires (33%)+ Irap

(4.25%) =

37.25%

Ires (33%)+ Irap

(4.25%) =

37.25%

Reduced

Dual Income

Tax: 19% on the

increase in net

equity

Dual Income Tax:

19% on the

increase in net

equity

N.A. N.A. N.A.

Minimum Tax

N.A. N.A. N.A. N.A. N.A.

Special Rates

Particular

business sectors

apply standard

rates on a low

taxable income

Particular

business sectors

apply standard

rates on a low

taxable income

Particular

business sectors

apply standard

rates on a low

taxable income

Particular

business sectors

apply standard

rates on a low

taxable income

Particular

business sectors

apply standard

rates on a low

taxable income

Non profit

tax (local tax

on

corporations,

energy tax…)

on real estate)

rate: can range

from 0.4% to

0.7%. It’s

applied on the

estimated value

of the property.

ICI (local tax on

real estate) rate:

can range from

0.4% to 0.7%. It’s

applied on the

estimated value

of the property.

ICI (local tax on

real estate)

rate: can range

from 0.4% to

0.7%. It’s

applied on the

estimated value

of the property.

ICI (local tax on

real estate)

rate: can range

from 0.4% to

0.7%. It’s

applied on the

estimated value

of the property.

ICI (local tax on

real estate)

rate: can range

from 0.4% to

0.7%. It’s

applied on the

estimated value

of the property.

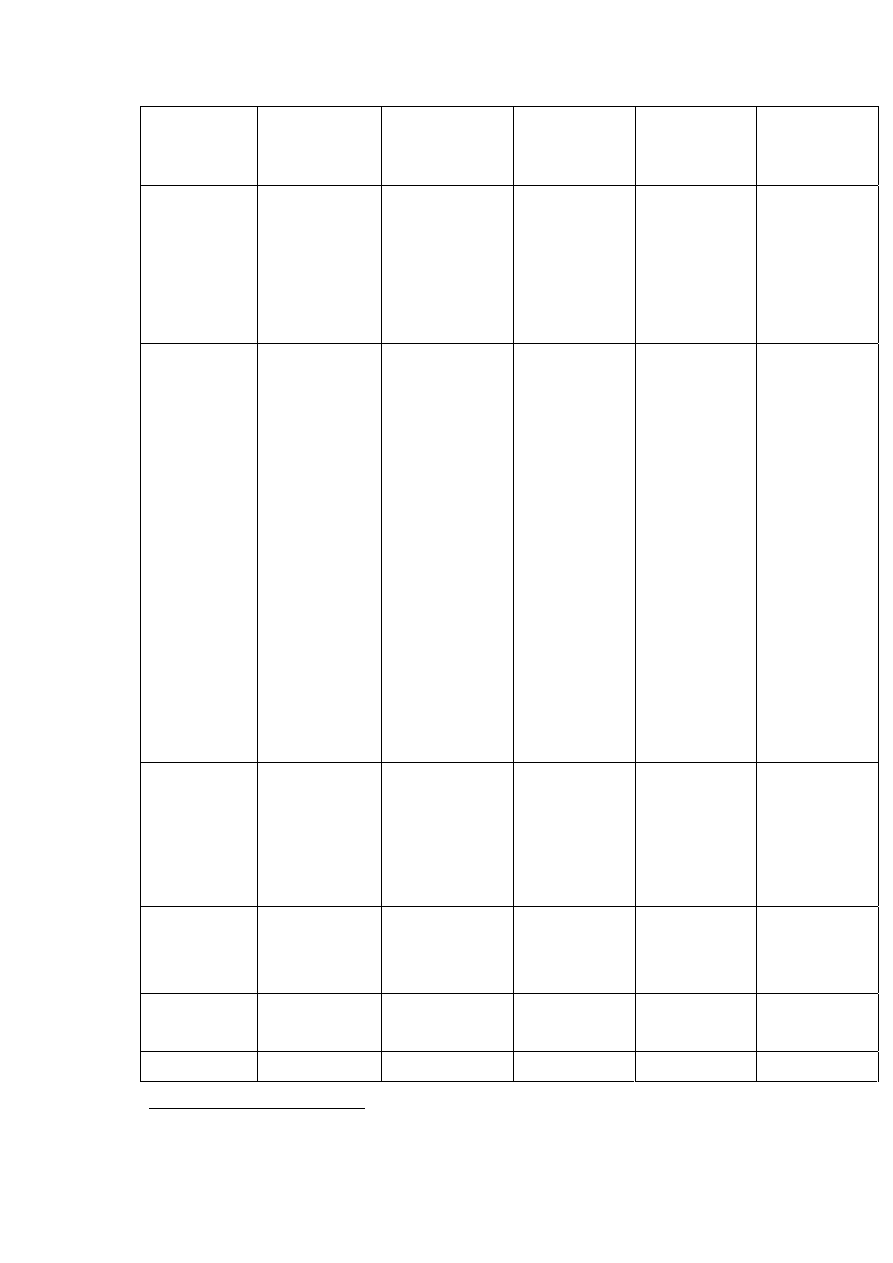

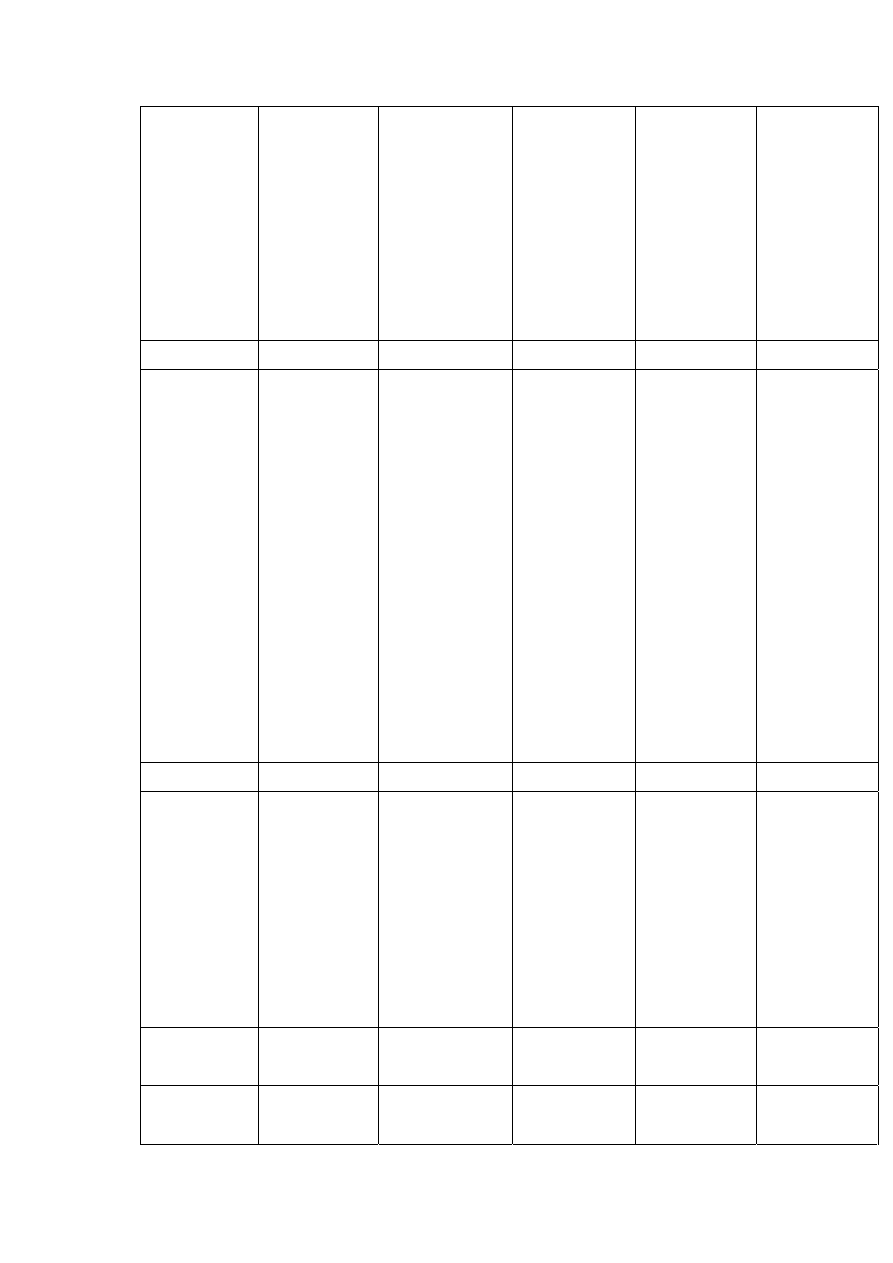

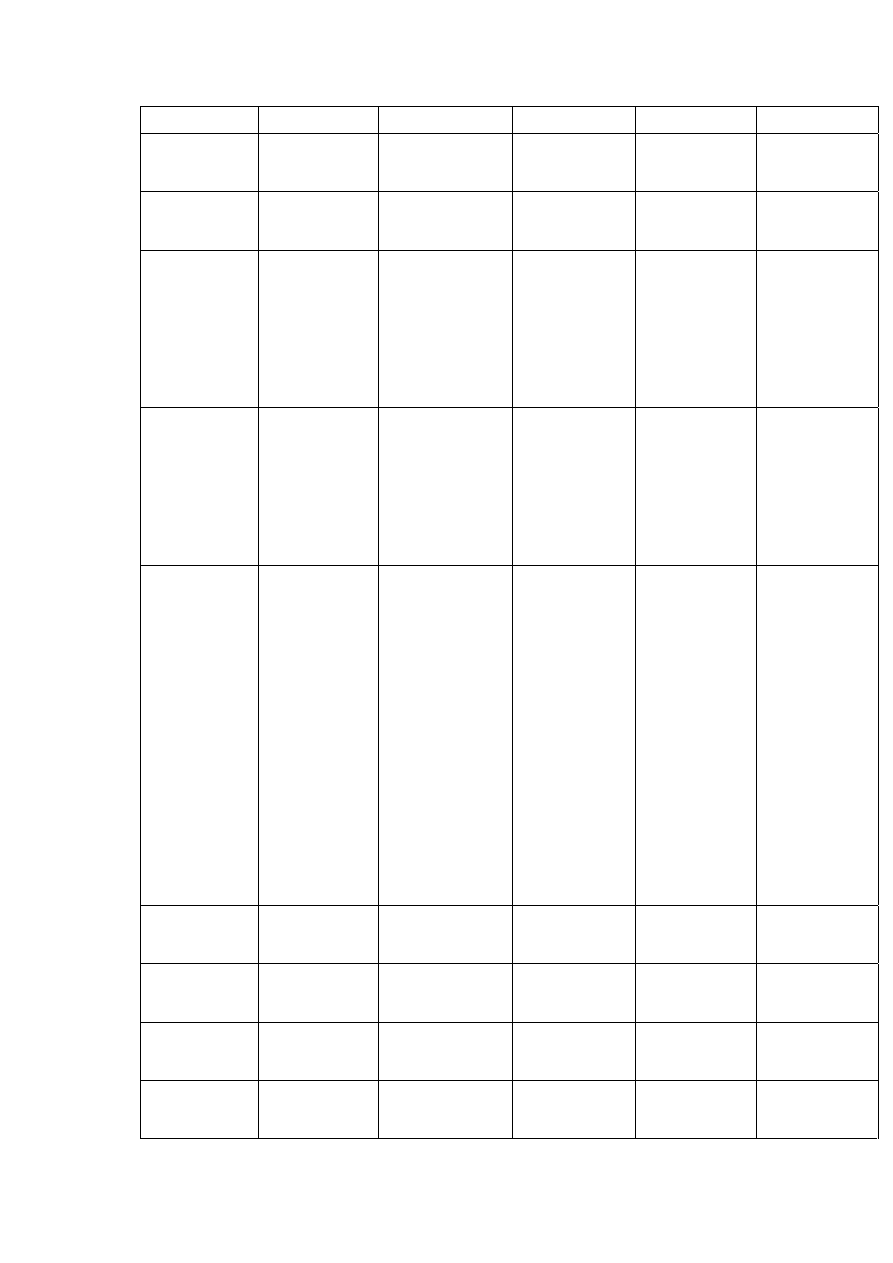

10

D.Lgs. 504, 30/12/1992

Italy Country Report

February 2008

7

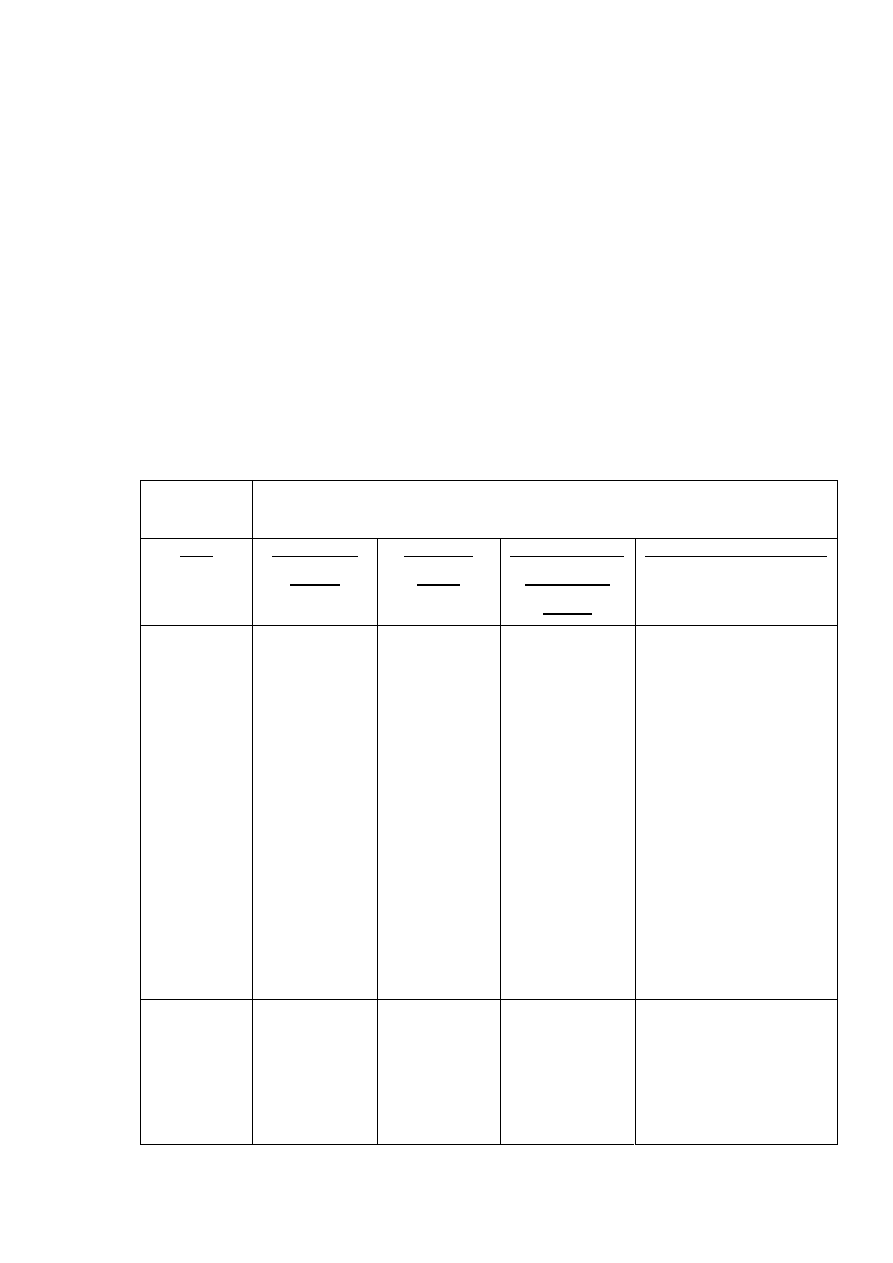

2. Tax

accounting

rules

N.A. N.A. N.A. N.A. N.A.

3.

Depreciation

Basis

Historical cost

Historical cost

Historical cost

Historical cost

Historical cost

Methods

Proportional Proportional Proportional Proportional Proportional

Rates

Different rates

are applicable

on different

categories of

assets

Different rates

are applicable on

different

categories of

assets

Different rates

are applicable

on different

categories of

assets

Different rates

are applicable

on different

categories of

assets

Different rates

are applicable

on different

categories of

assets

Accounting

N.A. N.A. N.A. N.A. N.A.

Intangibles

Different rates

are applicable

on different

categories of

intangibles

Different rates

are applicable on

different

categories of

intangibles

Different rates

are applicable

on different

categories of

intangibles

Different rates

are applicable

on different

categories of

intangibles

Different rates

are applicable

on different

categories of

intangibles

Non

depreciable

assets

Land

Land

Land

Land

From 01/01/06

depreciation of

building is on

the basis of the

historical cost

minus the land

cost.

4. Provisions

Risks and

futures

expenses

Not deductible

Not deductible

Not deductible Not

deductible Not

deductible

Bad debts

12

Are deductible

in the limit of

0.5% of total

amount of

commercial

credits

Are deductible in

the limit of 0.5%

of total amount

of commercial

credits (excluded

covered by

Are deductible

in the limit of

0.5% of total

amount of

commercial

credits

Are deductible

in the limit of

0.5% of total

amount of

commercial

credits

Are deductible

in the limit of

0.5% of total

amount of

commercial

credits

11

D.P.R. 917, 22/12/1986, art. 102

12

D.P.R. 917, 22/12/1986, art.106

Italy Country Report

February 2008

8

(excluded

covered by

insurance)

Credit provision

does not exceed

5% of total

amount of

commercial

credits

insurance) Credit

provision does

not exceed 5% of

total amount of

commercial

credits

(excluded

covered by

insurance)

Credit provision

does not exceed

5% of total

amount of

commercial

credits

(excluded

covered by

insurance)

Credit provision

does not exceed

5% of total

amount of

commercial

credits

(excluded

covered by

insurance)

Credit provision

does not exceed

5% of total

amount of

commercial

credits

Pensions

N.A. N.A. N.A. N.A. N.A.

Repairs

Are deductible

in the limit of

5% of total

amount of asset

historical cost at

the date of the

beginning of the

exercice

(without

Intangibles)

considering

acquisition and

sell during the

year.

Are deductible in

the limit of 5% of

total amount of

asset historical

cost at the date

of the beginning

of the exercice

(without

Intangibles)

considering

acquisition and

sell during the

year.

Are deductible

in the limit of

5% of total

amount of asset

historical cost

at the date of

the beginning of

the exercice

(without

Intangibles)

considering

acquisition and

sell during the

year.

Are deductible

in the limit of

5% of total

amount of asset

historical cost

at the date of

the beginning of

the exercice

(without

Intangibles)

considering

acquisition and

sell during the

year.

Are deductible

in the limit of

5% of total

amount of asset

historical cost

at the date of

the beginning of

the exercice

(without

Intangibles)

considering

acquisition and

sell during the

year.

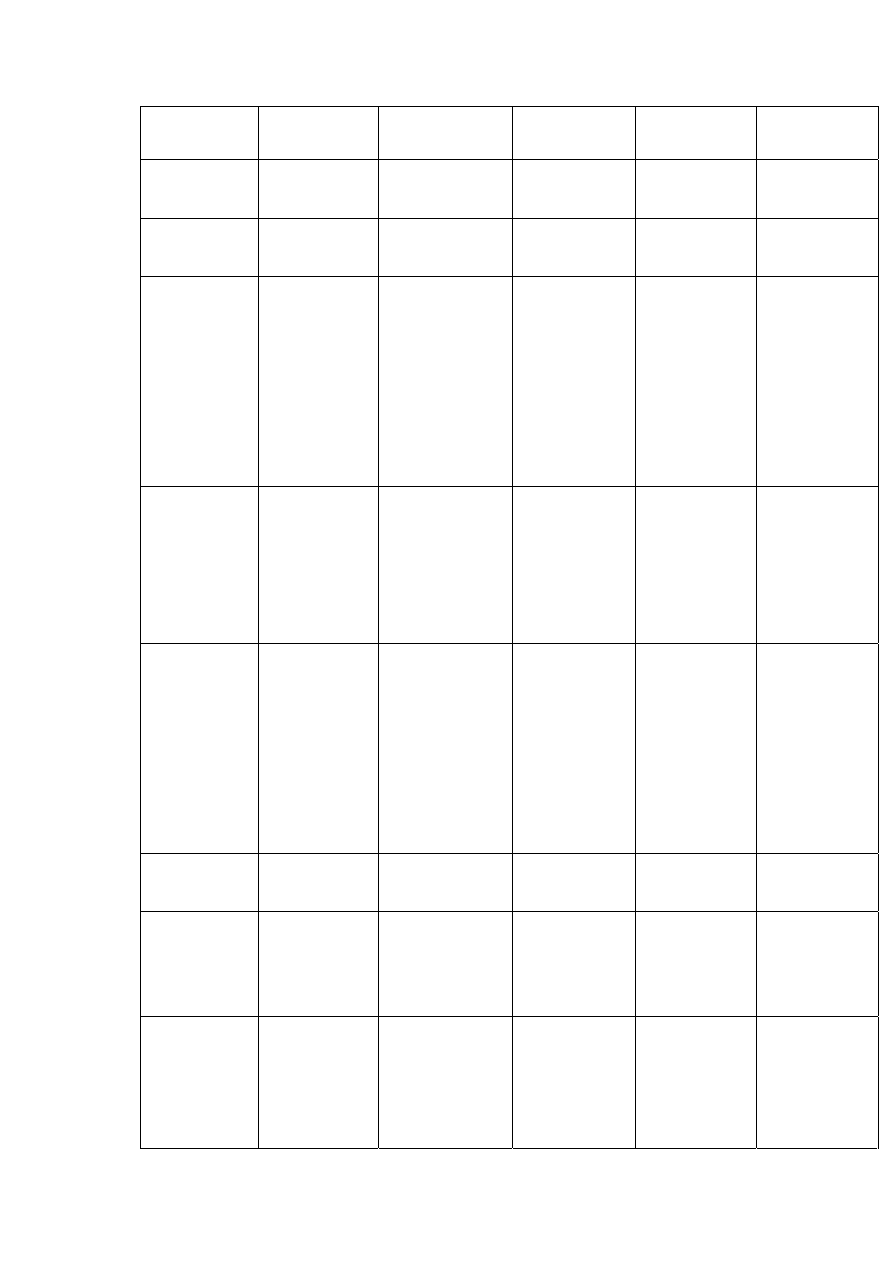

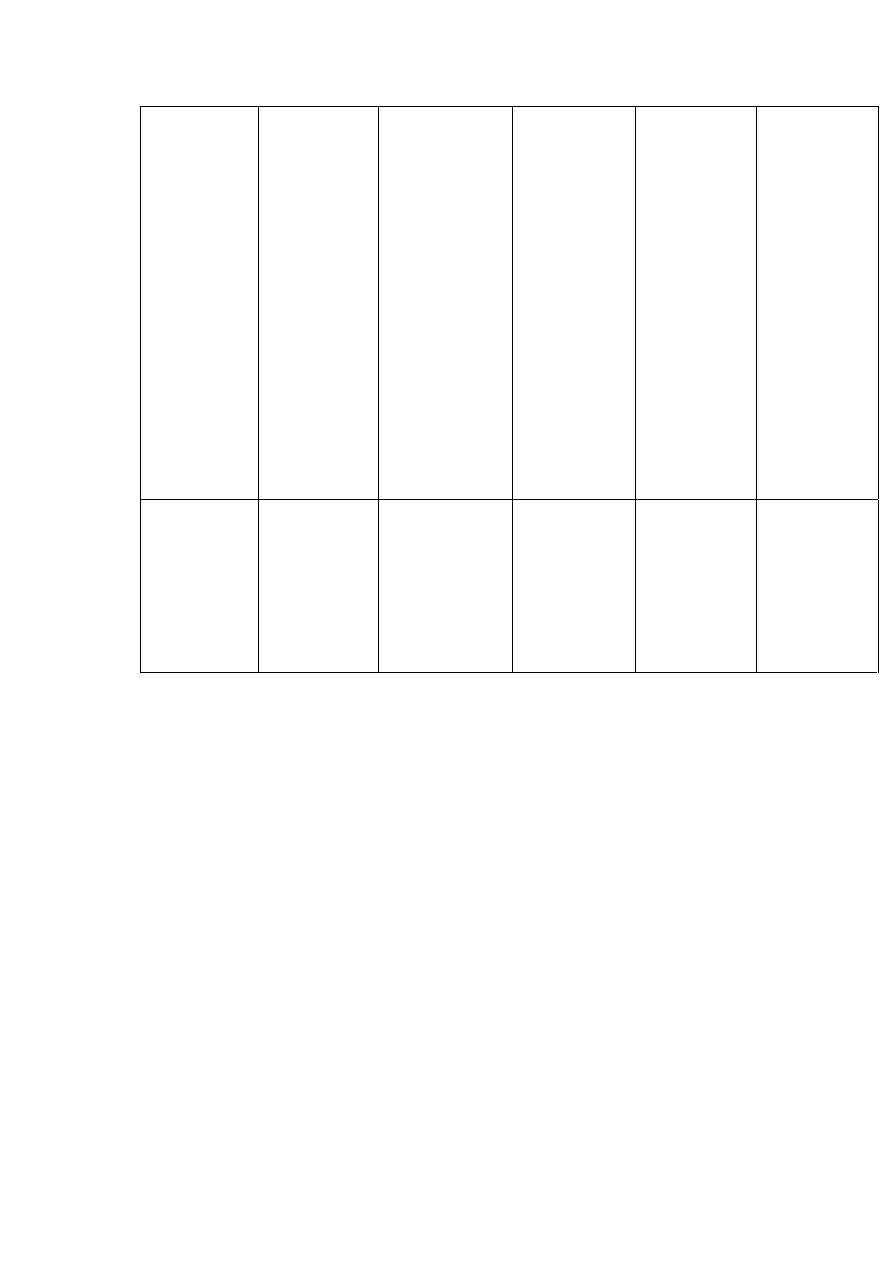

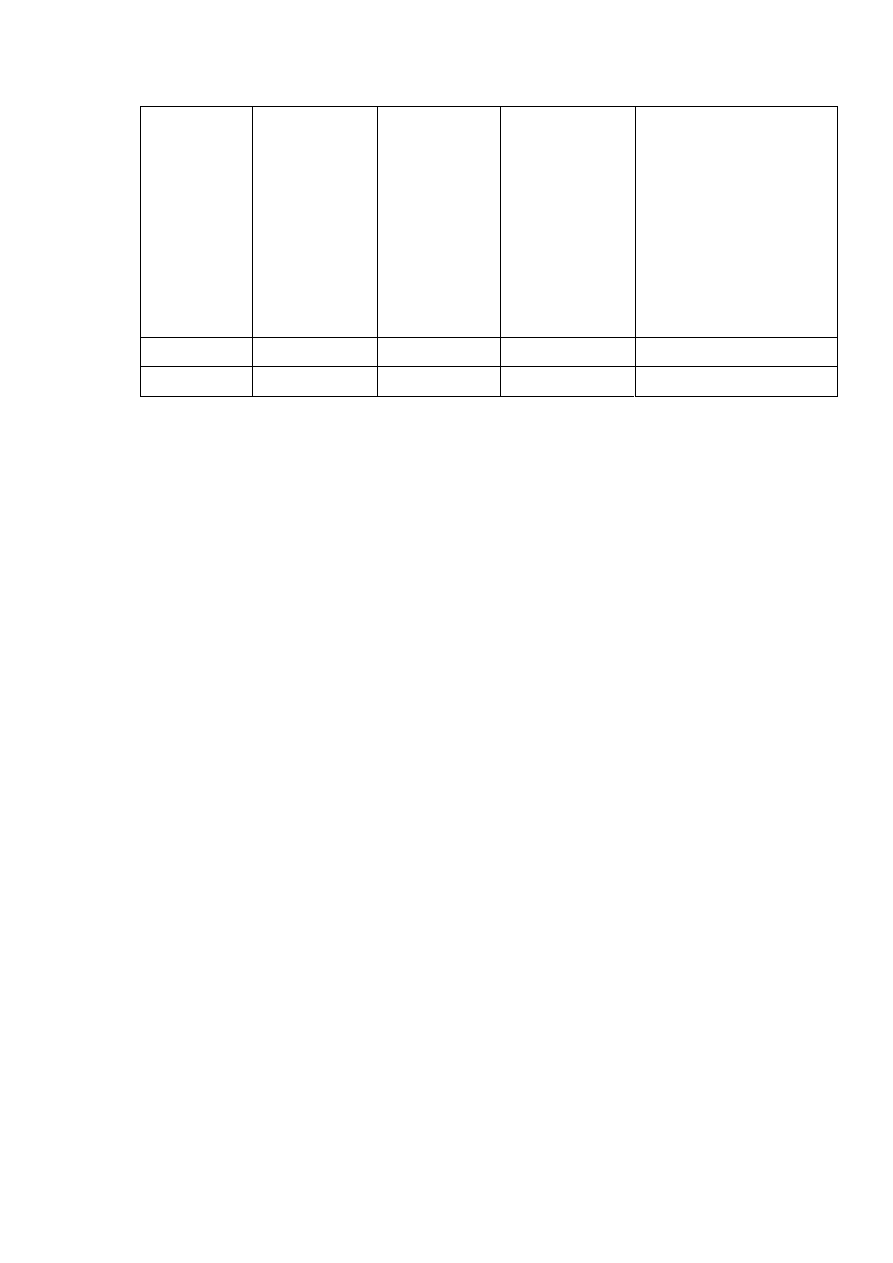

5. Losses

Carry

forward

Losses realized

in the first three

exercises could

be carried

forward without

limitation.

Losses from the

4

th

period could

be carried

forward for

maximum 5

periods.

Losses realized in

the first three

exercises could

be carried

forward without

limitation. Losses

from the 4

th

period could be

carried forward

for maximum 5

periods.

Losses realized

in the first

three exercises

could be carried

forward without

limitation.

Losses from the

4

th

period could

be carried

forward for

maximum 5

periods.

Losses realized

in the first

three exercises

could be carried

forward without

limitation.

Losses from the

4

th

period could

be carried

forward for

maximum 5

periods.

Losses realized

in the first

three exercises

could be carried

forward without

limitation.

Losses from the

4

th

period could

be carried

forward for

maximum 5

periods.

Carry back

N.A. N.A. N.A. N.A. N.A.

Transfer of

Is possible in

Is possible in case

Is possible in

Is possible in

Is possible in

13

D.P.R. 917, 22/12/1986, art. 84

Italy Country Report

February 2008

9

losses

case of merger

and acquisition

(m&a) operation

and

simultaneous

change of

business activity

under certain

circumstances.

of m&a operation

and simultaneous

change of

business activity

under certain

circumstances.

case of m&a

operation and

simultaneous

change of

business activity

under certain

circumstances.

case of m&a

operation and

simultaneous

change of

business activity

under certain

circumstances.

case of m&a

operation and

simultaneous

change of

business activity

under certain

circumstances.

5.

Inventories

Valuation

rules

LIFO, average

and FIFO

methods are

applicable

LIFO, average and

FIFO methods are

applicable

LIFO, average

and FIFO

methods are

applicable

LIFO, average

and FIFO

methods are

applicable

LIFO, average

and FIFO

methods are

applicable

Allocation

methods

Cost of goods

purchased

Cost of goods

purchased

Cost of goods

purchased

Cost of goods

purchased

Cost of goods

purchased

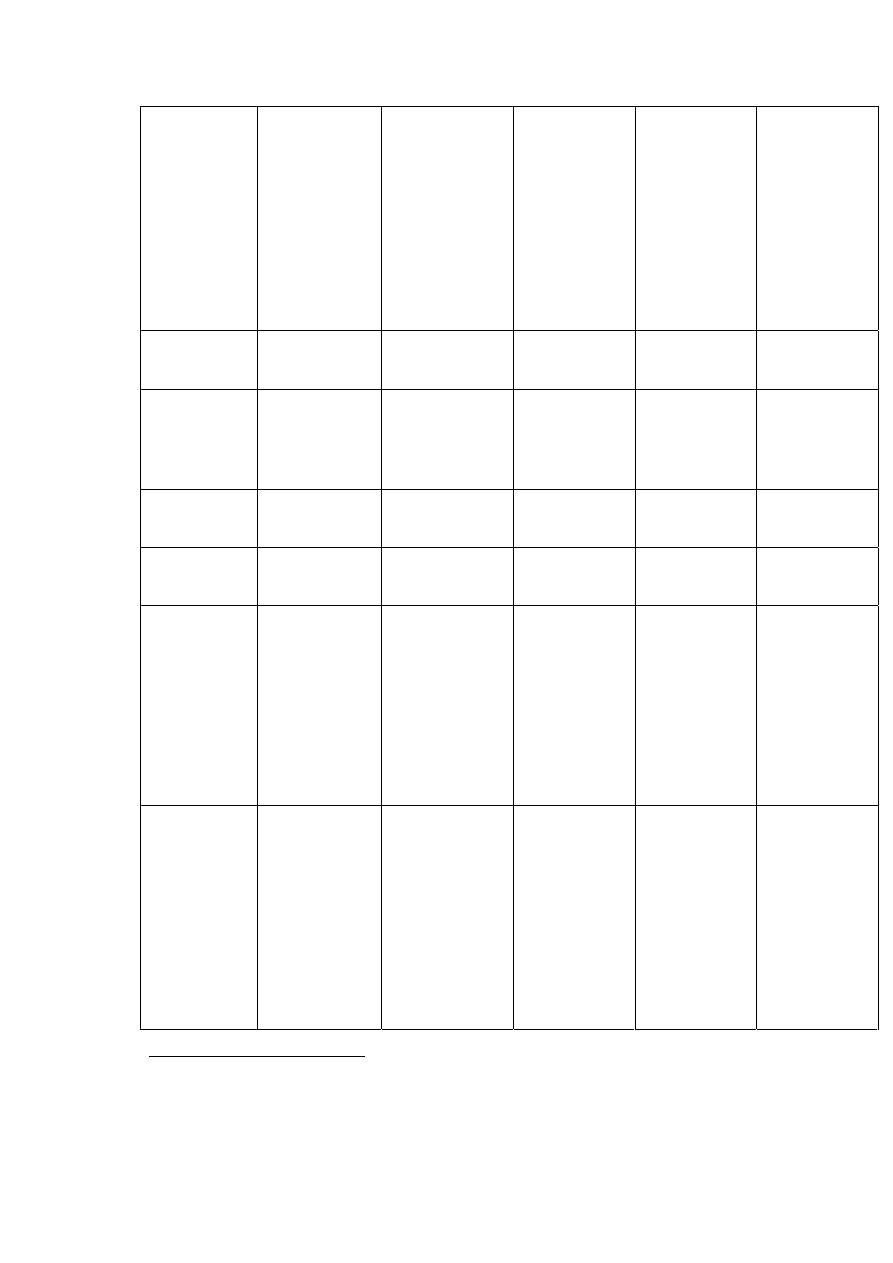

Personal

Income tax

Interest

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a component

of the individual

person income

that is taxable to

the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

Dividends

n.a. because

there was the

tax credit that

off-set the

corporate

taxation.

n.a. because

there was the tax

credit that off-set

the corporate

taxation.

40% of the

dividend

amount in case

of majority

shareholding

applying the

Irpef rates

. In

case of minority

shareholding it

40% of the

dividend

amount in case

of majority

shareholding

applying the

Irpef rates. In

case of minority

shareholding it

40% of the

dividend

amount in case

of majority

shareholding

applying the

Irpef rates. In

case of minority

shareholding it

14

D.P.R. 917, 22/12/1986, art. 92

15

D.P.R. 917, 22/12/1986, art. 44

16

D.P.R. 917, 22/12/1986, art. 59

Italy Country Report

February 2008

10

will apply a

definitive

withholding tax

of 12.5% rate.

will apply a

definitive

withholding tax

of 12.5% rate.

will apply a

definitive

withholding tax

of 12.5% rate.

Employment

income

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a component

of the individual

person income

that is taxable to

the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

Capital gains

tax

Sale of fixed

assets

The capital gain

is an income

that is included

in the tax basis

for Ires and Irap

The capital gain

is an income that

is included in the

tax basis for Ires

and Irap

The capital gain

is an income

that is included

in the tax basis

for Ires and Irap

The capital gain

is an income

that is included

in the tax basis

for Ires and Irap

The capital gain

is an income

that is included

in the tax basis

for Ires and Irap

Timing

rules

Normally

taxable in the

period in which

realized or may

be declared in

equal

instalments over

a period not

exceeding 5

years ( it is

possible only if

the company has

owned fixed

asset more than

three years.)

Normally taxable

in the period in

which realized or

may be declared

in equal

instalments over

a period not

exceeding 5 years

( it is possible

only if the

company has

owned fixed asset

more than three

years.)

Normally

taxable in the

period in which

realized or may

be declared in

equal

instalments

over a period

not exceeding 5

years ( it is

possible only if

the company

has owned fixed

asset more than

three years.)

Normally

taxable in the

period in which

realized or may

be declared in

equal

instalments

over a period

not exceeding 5

years ( it is

possible only if

the company

has owned fixed

asset more than

three years.)

Normally

taxable in the

period in which

realized or may

be declared in

equal

instalments

over a period

not exceeding 5

years ( it is

possible only if

the company

has owned fixed

asset more than

three years.)

Accounting

rules

N.A. N.A. N.A. N.A. N.A.

Inflation

N.A. N.A. N.A. N.A. N.A.

17

D.P.R. 917, 22/12/1986, art. 49

18

D.P.R. 917, 22/12/1986, art. 86

Italy Country Report

February 2008

11

Rates

Ordinary Ordinary Ordinary Ordinary Ordinary

Exemptions

N.A. N.A. N.A. N.A. N.A.

Sale of

If shares have

been held for

more than 3

years may

choose to pay a

substitute tax at

19% rate.

Shares have

been held for

less than 3 years

capital gains are

subject to

income tax

If shares have

been held for

more than 3 years

may choose to

pay a substitute

tax at 19% rate.

Shares have been

held for less than

3 years capital

gains are subject

to income tax

In case shares

are registered

as long-term

investments the

capital gains

are exempt to

taxation.

(Participation

exemption)

In case they are

not registeedr

as long-term

investments

capital gains

are subject to

income tax

Pex Pex

91%

Capital loss

Fixed assets

Deductible costs

Deductible costs

Deductible costs Deductible costs Deductible costs

Shares

The capital loss

realized is

deductible.

The capital loss

realized is

deductible

In case the

participation

exemption is

applicable the

capital losses

are not

deductible.

In case they are

not registered

as long-term

investments are

considered

deductible costs

In case the

participation

exemption is

applicable the

capital losses

are not

deductible.

In case they are

not registered

as long-term

investments are

considered

deductible costs

In case the

participation

exemption is

applicable the

capital losses

are not

deductible.

In case they are

not registered

as long-term

investments are

considered

deductible costs

Wages

Average cost

to the

It could be a 29%

average rate

(cost of

It could be a 29%

average rate

It could be a

29% average

rate

It could be a

29% average

rate

It could be a

29% average

rate

19

D.P.R. 917, 22/12/1986, art. 86-87

Italy Country Report

February 2008

12

Undertaking

compulsory

contribution for

pension and

health)

Average cost

to the

employee

It could be a 9%

average rate

(compulsory

contribution to

be paid by the

employee)

It could be a 9%

average rate

It could be a 9%

average rate

It could be a 9%

average rate

It could be a 9%

average rate

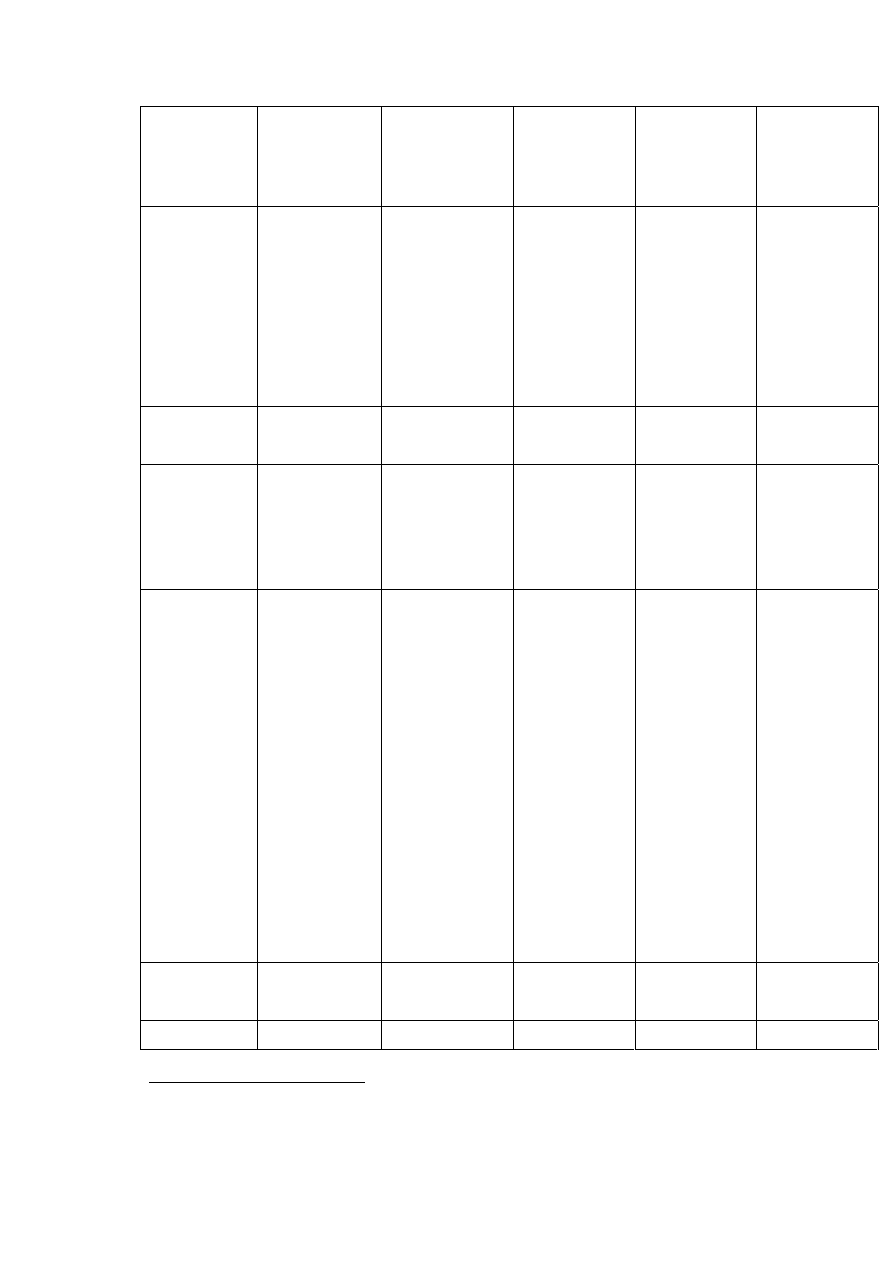

Overall tax

on

distributed

earnings or

Dividends

Timing

Period in which

the dividend

are cashed

Period in which

the dividend are

cashed

Period in which

the dividend

are cashed

Period in which

the dividend

are cashed

Period in which

the dividend

are cashed

Tax credit

structure

Tax credit of

56,25% of the

dividend

Tax credit of

51,51% of the

dividend

Tax credit is

non applicable

Only 5% of the

dividend

collected is

Tax credit is

non applicable

Only 5% of the

dividend

collected is

taxable

Tax credit is

non applicable

Only 5% of the

dividend

collected is

taxable

Excluding

non profit

tax

Non profit tax

is not

applicable on

the dividend

N.A

N.A

N.A

N.A

Including non

profit tax

N.A

N.A

N.A

N.A

N.A

Deduction of

expenses

General rule

Costs related to

business

activity could

be deducted in

Costs related to

business activity

could be

deducted in the

Costs related

to business

activity could

be deducted in

Costs related

to business

activity could

be deducted in

Costs related

to business

activity could

be deducted in

20

D.P.R. 917, 22/12/1986, art. 95

21

D.P.R. 917, 22/12/1986, art. 89

Italy Country Report

February 2008

13

the pertaining

period

pertaining

period

the pertaining

period

the pertaining

period

the pertaining

period

Non-

deductibility

of expenses

Costs related to

cars, taxes.

Some costs like

repairs are

partially

deductible

Costs related to

cars, taxes.

Some costs like

repairs are

partially

deductible

Costs related

to cars, taxes.

Some costs like

repairs are

partially

deductible

Costs related

to cars, taxes.

Some costs like

repairs are

partially

deductible

Costs related

to cars, taxes.

Some costs like

repairs are

partially

deductible

Thin

capitalizatio

n

N.A

N.A

Interests paid

on loan

granted by

shareholders

with at least

25% of shares

are partially

non deductible

in case debt

results five

times major

than the net

equity

attributed to

holding

company.

Interests paid

on loan

granted by

shareholders

with at least

25% are

partially non

deductible in

case debt

results four

times major

than the net

equity

attributed to

holding

company.

Interests paid

on loan

granted by

shareholders

with at least

25% are

partially non

deductible in

case debt

results four

times major

than the net

equity

attributed to

holding

company .

Overall

corporate

tax on

Retained

earnings

Excluding

non profit

tax

N.A

N.A

N.A

N.A

N.A

Including non

profit tax

N.A

N.A

N.A

N.A

N.A

Debt

22

D.P.R. 917, 22/12/1986, art. 98

Italy Country Report

February 2008

14

financing

Interest

deductibility

Always

deductible

Always

deductible

Always

deductible

Always

deductible

Always

deductible

Limits on

interest

deductibility

There are some

limits to the

deductibility of

interest only

when the

corporation has

exempt

revenue.

There are some

limits to the

deductibility of

interest only

when the

corporation has

exempt revenue.

See above thin

capitalization

rules.

The pro-rata

rule is

applicable

when the

corporation has

shares (to

whom the

Participation

exemption is

applicable)

whose amount

is higher to the

Net equity.

See above thin

capitalization

rules.

The pro-rata

rule is

applicable

when the

corporation has

shares (to

whom the

Participation

exemption is

applicable)

whose amount

is higher to the

Net equity.

See above thin

capitalization

rules.

The pro-rata

rule is

applicable

when the

corporation has

shares (to

whom the

Participation

exemption is

applicable)

whose amount

is higher to the

Net equity.

Interest

deductibility

on business

owner loan

to

Undertaking

Always

deductible in

case of a

remunerative

loan.

Always

deductible in

case of a

remunerative

loan.

Always

deductible in

case of a

remunerative

loan, within

the limits of

the Thin Cap.

Always

deductible in

case of a

remunerative

loan, within

the limits of

the Thin cap.

Always

deductible in

case of a

remunerative

loan, within

the limits of

Thin cap..

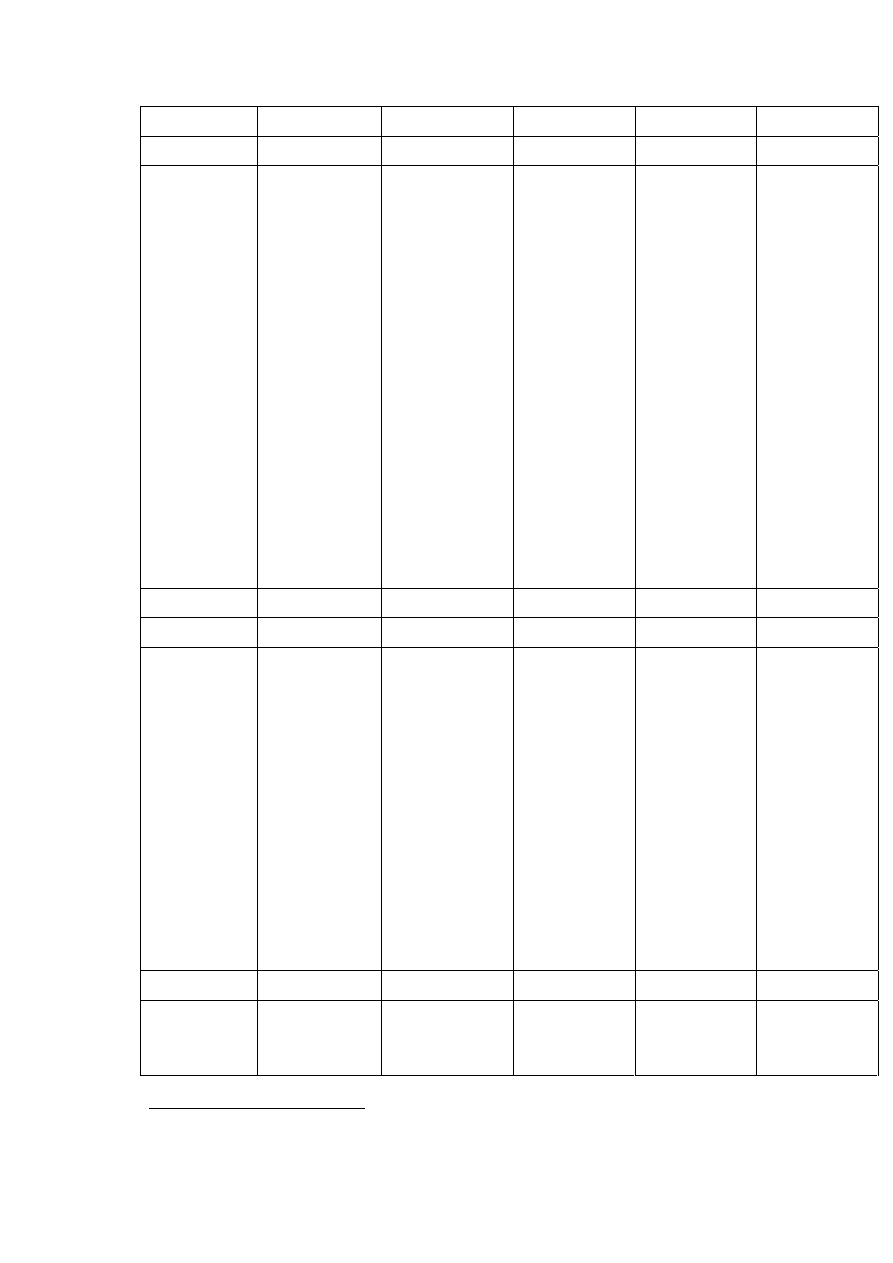

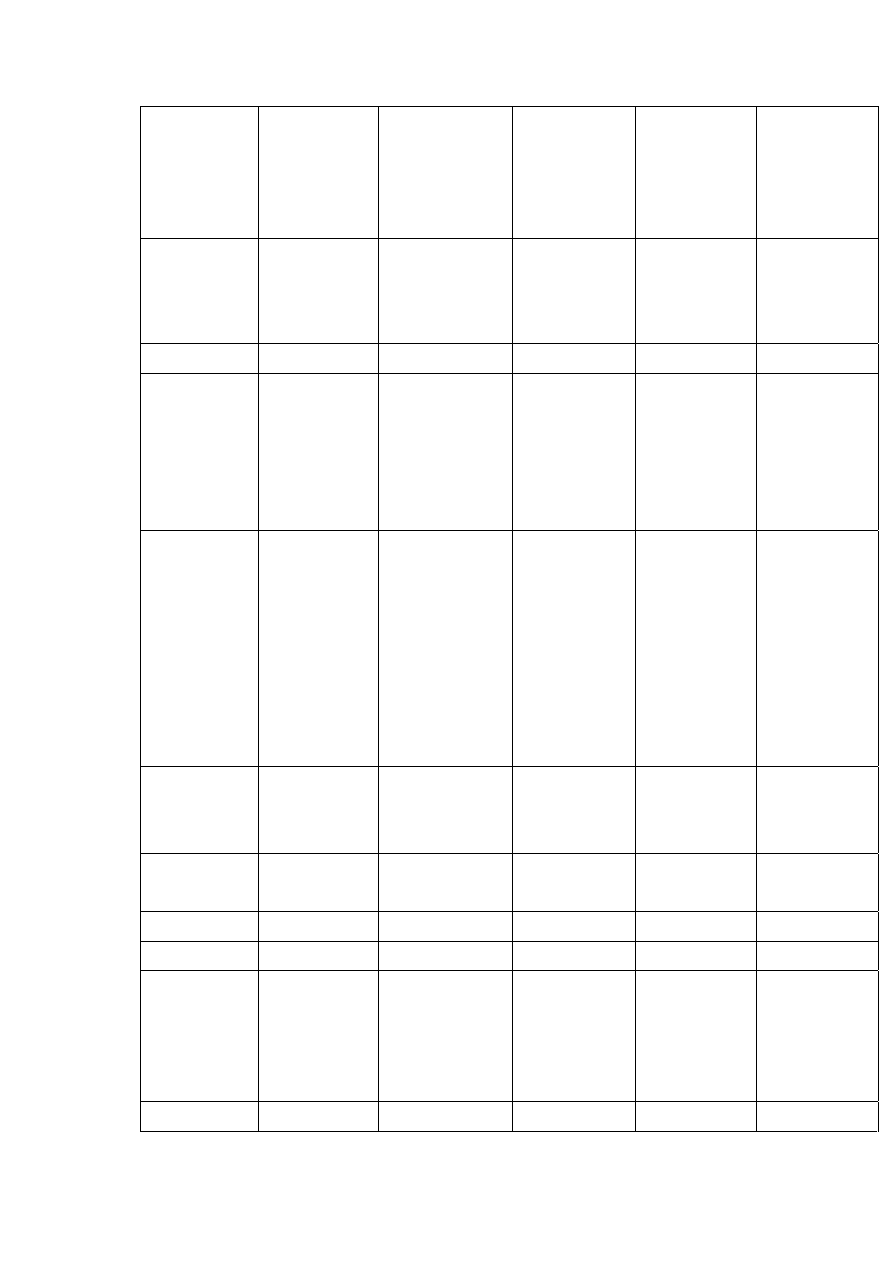

ITALY

RELEVANT TAX PROVISIONS AND SUBSEQUENT CHANGES

For PARTNERSHIPS (distinguish specific rates for SMES)

2002

2003

2004

2005

2006

Tax

applicable to

partnerships

1. Tax rate

Standard

Partnership is

Partnership is tax

Partnership is

Partnership is

Partnership is

23

D.P.R. 917, 22/12/1986, art. 97

Italy Country Report

February 2008

15

tax

transparent.

Partnership is

subject to Irap

(4.25%)

transparent.

Partnership is

subject to Irap

(4.25%)

tax

transparent.

Partnership is

subject to Irap

(4.25%)

tax

transparent.

Partnership is

subject to

Irap (4.25%)

tax

transparent.

Partnership is

subject to Irap

(4.25%)

Reduced

Dual Income

Tax: 19% on

the increase in

net equity

Dual Income Tax:

19% on the

increase in net

equity

Minimum Tax

N.A. N.A. N.A. N.A. N.A.

Special Rates

Particular

business

sectors apply

standard rates

on a low

taxable income

Particular

business sectors

apply standard

rates on a low

taxable income

Particular

business

sectors apply

standard rates

on a low

taxable income

Particular

business

sectors apply

standard rates

on a low

taxable income

Particular

business

sectors apply

standard rates

on a low

taxable income

Non profit

tax (local tax

on

corporations,

energy tax…)

ICI (local tax

on real estate )

rate: can range

from 0.4% to

0.7%. It is

applied on the

estimated

value of the

property.

ICI (local tax on

real estate )

rate: can range

from 0.4% to

0.7%. It is

applied on the

estimated value

of the property.

ICI (local tax

on real estate )

rate: can range

from 0.4% to

0.7%. It is

applied on the

estimated

value of the

property.

ICI (local tax

on real estate )

rate: can range

from 0.4% to

0.7%. It is

applied on the

estimated

value of the

property.

ICI (local tax

on real estate )

rate: can range

from 0.4% to

0.7%. It is

applied on the

estimated

value of the

property.

2. Tax

accounting

rules

N.A. N.A. N.A. N.A. N.A.

3.

Depreciation

Basis

Historical cost

Historical cost

Historical cost

Historical cost

Historical cost

Methods

Proportional Proportional Proportional Proportional Proportional

Rates

Different rates

are applicable

on different

categories of

assets

Different rates

are applicable on

different

categories of

assets

Different rates

are applicable

on different

categories of

assets

Different rates

are applicable

on different

categories of

assets

Different rates

are applicable

on different

categories of

assets

Accounting

N.A. N.A. N.A. N.A. N.A.

Italy Country Report

February 2008

16

Intangibles

Different rates

are applicable

on different

categories of

intangibles

Different rates

are applicable on

different

categories of

intangibles

Different rates

are applicable

on different

categories of

intangibles

Different rates

are applicable

on different

categories of

intangibles

Different rates

are applicable

on different

categories of

intangibles

Non

depreciable

assets

Land Land Land Land

From

01/01/06

depreciation of

building is on

the basis of the

historical cost

minus the land

cost.

4. Provisions

Risks and

futures

expenses

Not deductible

Not deductible

Not deductible

Not deductible Not deductible

Bad debts

Are deductible

in the limit of

0.5% of total

amount of

commercial

credits

(excluded

covered by

insurance)

Credit

provision do

not exceed 5%

of total

amount of

commercial

credits

Are deductible in

the limit of 0.5%

of total amount

of commercial

credits (excluded

covered by

insurance) Credit

provision do not

exceed 5% of

total amount of

commercial

credits

Are deductible

in the limit of

0.5% of total

amount of

commercial

credits

(excluded

covered by

insurance)

Credit

provision do

not exceed 5%

of total amount

of commercial

credits

Are deductible

in the limit of

0.5% of total

amount of

commercial

credits

(excluded

covered by

insurance)

Credit

provision do

not exceed 5%

of total

amount of

commercial

credits

Are deductible

in the limit of

0.5% of total

amount of

commercial

credits

(excluded

covered by

insurance)

Credit

provision do

not exceed 5%

of total

amount of

commercial

credits

Pensions

N.A. N.A. N.A. N.A. N.A.

Repairs

Are deductible

in the limit of

5% of total

amount of

asset historical

cost at

the

Are deductible in

the limit of 5% of

total amount of

asset historical

cost at

the date

of the beginning

Are deductible

in the limit of

5% of total

amount of

asset historical

cost at

the date

Are deductible

in the limit of

5% of total

amount of

asset historical

cost at

the date

Are deductible

in the limit of

5% of total

amount of

asset historical

cost at

the date

Italy Country Report

February 2008

17

date of the

beginning of

the exercice

(

without

Intangibles )

considering

acquisition and

sell during the

year.

of the exercice

(without

Intangibles)

considering

acquisition and

sell during the

year.

of the beginning

of the exercice

( without

Intangibles )

considering

acquisition and

sell during the

year.

of the beginning

of the exercice

( without

Intangibles )

considering

acquisition and

sell during the

year.

of the beginning

of the exercice

( without

Intangibles )

considering

acquisition and

sell during the

year.

5. Losses

Carry

forward

Losses realized

in the first

three exercises

could be

carried

forward

without

limitation.

Losses from

the 4

th

period

could be

carried

forward for

maximum 5

periods.

Losses realized in

the first three

exercises could

be carried

forward without

limitation. Losses

from the 4

th

period could be

carried forward

for maximum 5

periods.

Losses realized

in the first

three exercises

could be

carried forward

without

limitation.

Losses from the

4

th

period could

be carried

forward for

maximum 5

periods.

Losses realized

in the first

three exercises

could be

carried forward

without

limitation.

Losses from the

4

th

period

could be

carried forward

for maximum 5

periods.

Losses realized

in the first

three exercises

could be

carried forward

without

limitation.

Losses from the

4

th

period

could be

carried forward

for maximum 5

periods.

Carry back

N.A. N.A. N.A. N.A. N.A.

Transfer of

losses

It is possible in

case of m &a

operation and

simultaneous

change of

business

activity under

certain

circumstances.

It is possible in

case of m&a

operation and

simultaneous

change of

business activity

under certain

circumstances.

It is possible in

case of m&a

operation and

simultaneous

change of

business

activity under

certain

circumstances.

It is possible in

case of m&a

operation and

simultaneous

change of

business

activity under

certain

circumstances.

It is possible in

case of m&a

operation and

simultaneous

change of

business

activity under

certain

circumstances.

5.

Inventories

Valuation

rules

LIFO, average

and FIFO

LIFO, average

and FIFO

LIFO, average

and FIFO

LIFO, average

and FIFO

LIFO, average

and FIFO

Italy Country Report

February 2008

18

methods are

applicable

methods are

applicable

methods are

applicable

methods are

applicable

methods are

applicable

Allocation

methods

Cost of goods

purchased

Cost of goods

purchased

Cost of goods

purchased

Cost of goods

purchased

Cost of goods

purchased

Personal

Income tax

Interest

Income

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a component

of the individual

person income

that is taxable to

the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

Dividends

N.A.

Because

earnings of a

corporation

are treated

transparent

N.A.

Because earnings

of a corporation

are treated

transparent

N.A.

Because

earnings of a

corporation are

treated

transparent

N.A.

Because

earnings of a

corporation are

treated

transparent

N.A.

Because

earnings of a

corporation are

treated

transparent

Employment

income

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a component

of the individual

person income

that is taxable to

the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

It is a

component of

the individual

person income

that is taxable

to the ordinary

progressive tax

rate (Irpef).

Capital gains

tax

Sale of fixed

assets

Taxed with the

standard

method of

partnership

Taxed with the

standard method

of partnership

Taxed with the

standard

method of

partnership

Taxed with the

standard

method of

partnership

Taxed with the

standard

method of

partnership

Timing rules

Normally

taxable in the

period in which

realized or

may be

Normally taxable

in the period in

which realized or

may be declared

in equal

Normally

taxable in the

period in which

realized or may

be declared in

Normally

taxable in the

period in which

realized or may

be declared in

Normally

taxable in the

period in which

realized or may

be declared in

Italy Country Report

February 2008

19

declared in

equal

instalments

over a period

not exceeding

5 years ( it is

possible only if

the company

has owned

fixed asset

more than

three years.)

instalments over

a period not

exceeding 5

years ( it is

possible only if

the company has

owned fixed

asset more than

three years.)

equal

instalments

over a period

not exceeding

5 years ( it is

possible only if

the company

has owned

fixed asset

more than

three years.)

equal

instalments

over a period

not exceeding

5 years ( it is

possible only if

the company

has owned

fixed asset

more than

three years.)

equal

instalments

over a period

not exceeding

5 years ( it is

possible only if

the company

has owned

fixed asset

more than

three years.)

Accounting

rules

N.A. N.A. N.A. N.A. N.A.

Inflation

N.A. N.A. N.A. N.A. N.A.

Rates

N.A. N.A. N.A. N.A. N.A.

Exemptions

N.A. N.A. N.A. N.A. N.A.

Sale of

shares

If shares have

been held for

more than 3

years may

choose to pay

a substitute

tax at 19%

rate.

Shares have

been held for

less than 3

years capital

gains are

revenues that

concur to the

ordinary net

profit of the

partnership

If shares have

been held for

more than 3

years may

choose to pay a

substitute tax at

19% rate.

Shares have been

held for less than

3 years capital

gains are

revenues that

concur to the

ordinary net

profit of the

partnership

In case shares

are booked as

long-term

investments

the capital

gains are

exempt to

taxation on 60%

of the amount.

(Participation

exemption)

In case they

are not register

as long-term

investments

capital gains

concurs to the

ordinary net

profit of the

partnership

In case shares

are booked as

long-term

investments

the capital

gains are

exempt to

taxation on

60% of the

amount.

(Participation

exemption)

In case they

are not register

as long-term

investments

capital gains

concurs to the

ordinary net

profit of the

partnership

In case shares

are booked as

long-term

investments

the capital

gains are

exempt to

taxation on

60% of the

amount.

(Participation

exemption)

In case they

are not register

as long-term

investments

capital gains

concurs to the

ordinary net

profit of the

partnership

Italy Country Report

February 2008

20

Capital loss

Fixed assets

Deductible

only in

ordinary

accounting

system

Deductible only

in ordinary

accounting

system

Deductible only

in ordinary

accounting

system

Deductible only

in ordinary

accounting

system

Deductible only

in ordinary

accounting

system

Shares

The capital

loss realized is

deductible

The capital loss

realized is

deductible

In case of

participation

exemption is

applicable the

capital losses

are not

deductible on

the base of 60%

of the amount.

In case they

are not register

as long-term

investments

are considered

deductible

costs

In case of

participation

exemption is

applicable the

capital losses

are not

deductible on

the base of 60%

of the amount.

In case they

are not register

as long-term

investments

are considered

deductible

costs

In case of

participation

exemption is

applicable the

capital losses

are not

deductible on

the base of 60%

of the amount.

In case they

are not register

as long-term

investments

are considered

deductible

costs

Wages

Average cost

to the

Undertaking

It could be a

29% average

rate (cost of

compulsory

contribution

for pension

and health)

It could be a 29%

average rate

It could be a

29% average

rate

It could be a

29% average

rate

It could be a

29% average

rate

Average cost

to the

employee

It could be a

9% average

rate

(compulsory

contribution to

be paid by the

employee)

It could be a 9%

average rate

It could be a 9%

average rate

It could be a

9% average

rate

It could be a

9% average

rate

Dividends

Timing

N.A N.A N.A N.A N.A

Italy Country Report

February 2008

21

Tax credit

structure

N.A

N.A

N.A

N.A

N.A

Deduction of

expenses

General rule

Costs related

to business

activity could

be deducted in

the pertaining

period

Costs related to

business activity

could be

deducted in the

pertaining period

Costs related

to business

activity could

be deducted in

the pertaining

period

Costs related

to business

activity could

be deducted in

the pertaining

period

Costs related

to business

activity could

be deducted in

the pertaining

period

Non-

deductibility

of expenses

Costs related

to cars, taxes.

Some costs like

repairs are

partially

deductible

Costs related to

cars, taxes.

Some costs like

repairs are

partially

deductible

Costs related

to cars, taxes.

Some costs like

repairs are

partially

deductible

Costs related

to cars, taxes.

Some costs like

repairs are

partially

deductible

Costs related

to cars, taxes.

Some costs like

repairs are

partially

deductible

Thin

capitalization

N.A

N.A

Interests paid

on loan granted

by partners

(25% of quota)

are partially

non deductible

in case debt

results five

times major

than the net

equity

attributed to

the partners.

Interests paid

on loan

granted by

partners are

partially non

deductible in

case debt

results four

times major

than the net

equity

attributed to

the partners.

Interests paid

on loan

granted by

partners are

partially non

deductible in

case debt

results four

times major

than the net

equity

attributed to

the partners.

Retained

earnings

N.A

N.A

N.A

N.A

N.A

Debt

financing

Interest

deductibility

Always

deductible

Always

deductible

Always

deductible

Always

deductible

Always

deductible

Limits on

interest

There are

some limits to

There are some

limits to the

See above thin

capitalization

See above thin

capitalization

See above thin

capitalization

Italy Country Report

February 2008

22

deductibility

the

deductibility of

interest only

when the

partnership has

exempt

revenue.

deductibility of

interest only

when the

partnership has

exempt revenue.

rules.

There is the

pro-rata rule

that is

applicable

when the

partnership has

shares (to

whom the

Participation

exemption is

applicable)

which amount

is superior to

the Net equity.

rules.

There is the

pro-rata rule

that is

applicable

when the

partnership has

shares (to

whom the

Participation

exemption is

applicable)

which amount

is superior to

the Net equity

rules.

There is the

pro-rata rule

that is

applicable

when the

partnership has

shares (to

whom the

Participation

exemption is

applicable)

which amount

is superior to

the Net equity

Interest

deductibility

on business

owner loan

to

Undertaking

Always

deductible in

case of a

remunerative

loan.

Always

deductible in

case of a

remunerative

loan.

Always

deductible in

case of a

remunerative

loan.

Always

deductible in

case of a

remunerative

loan.

Always

deductible in

case of a

remunerative

loan.

Italy Country Report

February 2008

23

2.

What are the main types of business entities and the main differences in

(corporate) income taxation for sole traders, general partnerships, limited

partnerships and corporation and other business entities if relevant?

Corporations (Limited Company, Limited liability company, Limited partnership with

a share capital): they are taxed on the basis of ordinary tax rate.

In some cases, they should opt to be treated transparent for tax purposes.

Partnerships (Unlimited Partnership, Limited Partnership, Informal partnership): they

are treated transparent for tax purposes.

General partnership cannot have only one partner.

Corporations can also have only one partner.

2.1. Are partnerships treated transparent for tax purposes?

Yes

2.2. Can partnerships opt for corporate income tax?

NO, they can not opt for it.

2.3. Once they have opted for a regime is it easy to switch back?

Not applicable

2.4. Is there a difference in this respect between general and limited

partnerships?

Not applicable

Italy Country Report

February 2008

24

2.5. Can corporations opt to be treated tax transparent?

Yes

2.6. Once they have opted for a regime is it easy to switch back?

The regime is valid for a minimum period of three years and they could not switch

back to the original regime until the end of this period.

2.7. Are their differences in this respect between the different types of

corporations?

There are no difference.

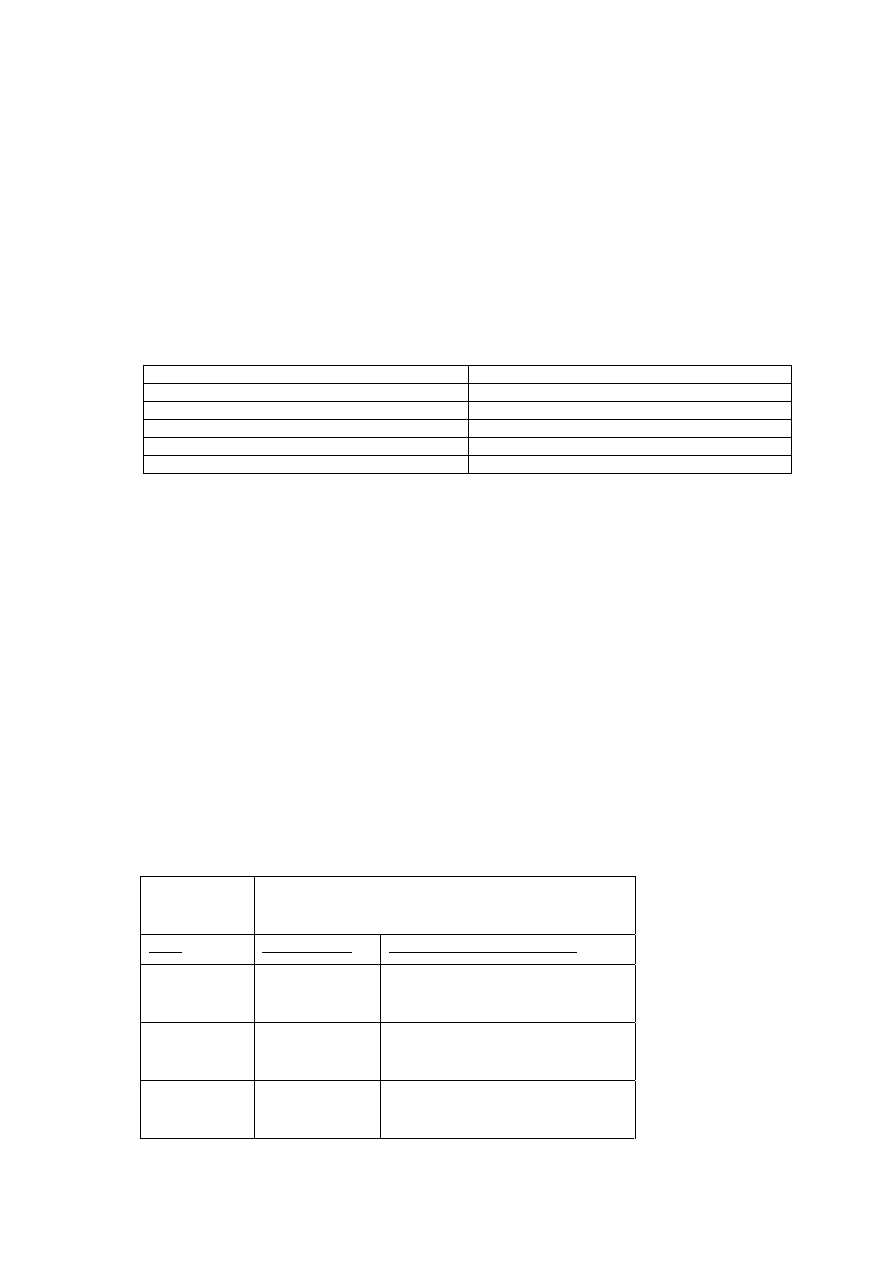

INCLUDE RELEVANT TAX PROVISIONS IN 2002 AND

SUBSEQUENT CHANGES UP TO 2007

ITALY

General

Partnership

Limited

Partnership

Corporation

Sole Trader

Corporate

tax

4,25% irap and

irpef

progressive

rates

4,25% irap

and irpef

progressive

rates

4,25% irap

33% ires

N.A.

Income tax

4,25% irap and

irpef

progressive

rates

4,25% irap

and irpef

progressive

rates

4,25% irap

33% ires

The business

income

defines the

individual

person

income that

is subject to

progressive

Italy Country Report

February 2008

25

Irpef rates.

Capital gains

tax

4,25% irap and

irpef

progressive

rates

4,25% irap

and irpef

progressive

rates

4,25% irap

33% ires

…

Option for

Transparent

treatment

It’s always tax

trasparent

It’s always

tax

trasparent

It’s possible

opt for the

tax

trasparency

n.a

…

3.

Are there any special tax regimes for SMEs for (corporate) income tax

purposes?

NO

3.1. What are the conditions to be fulfilled in order to benefit from

these special tax regimes?

Not applicable

3.2. Are there limits on the length of time during which these special tax

regimes are available, or other limits?

Not applicable

Italy Country Report

February 2008

26

4.

Are there any special tax incentives, such as (re-)investment reserves or

provisions, special depreciations/capital allowances deductible for

(corporate) income tax purposes?

YES

Only the cooperative societies have tax deductions on the basis of the retentions

of earnings.

Cooperative pay taxes only on the 30% of net income if all the income is retained.

4.1. Do these elements of internal financing represent an important

alternative to the financing by retained earnings?

NO

4.2. Are there any compulsory measures in relation to the retention of

earnings (e.g. legal constraints for the distribution of profits and

dividend

policy)?

YES

Profits could be distributed only if the amount of legal reserve is equal to 20% of

In case of intangibles registered in accounting, law states that a specific reserve has

to be held for an amount equal to the intangibles cost not yet depreciated, before

distributing profits.

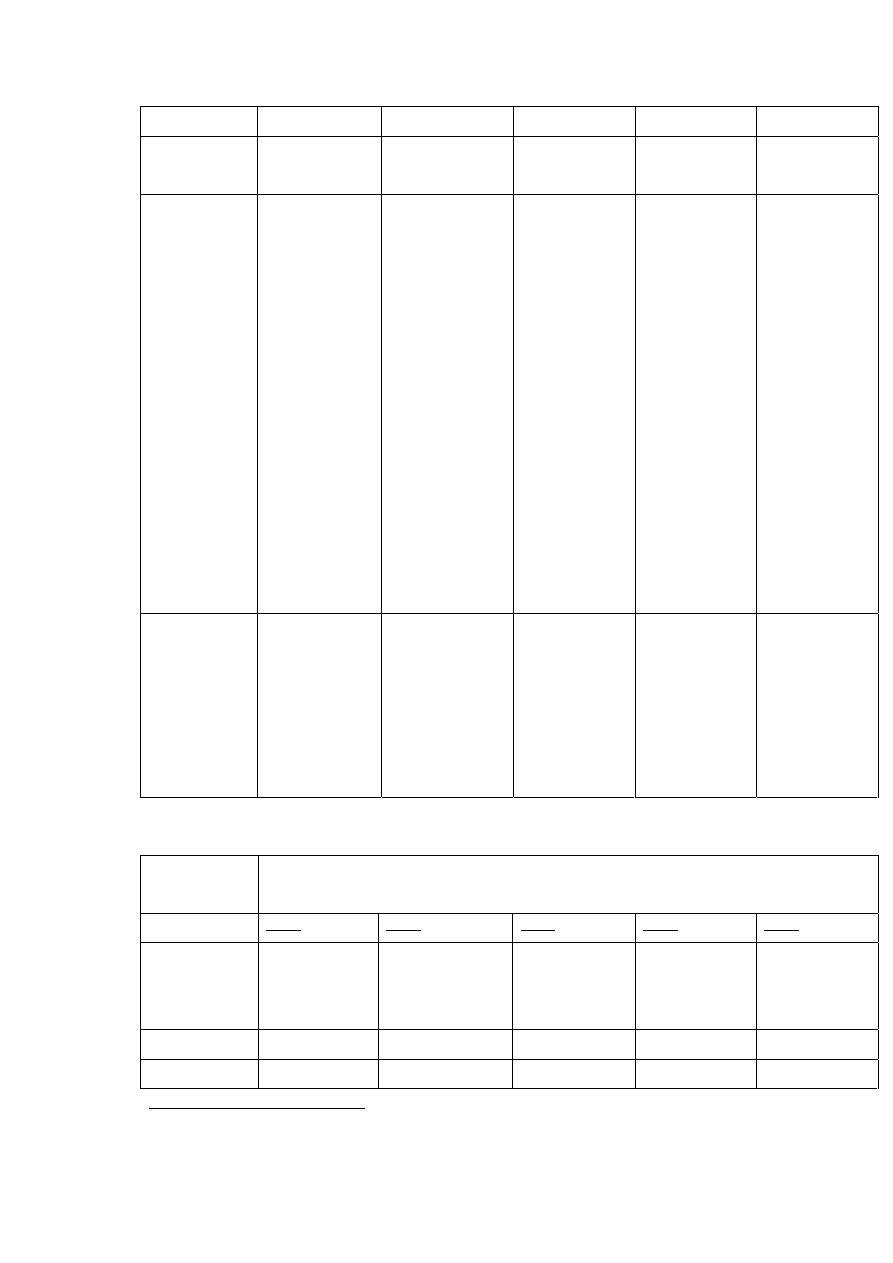

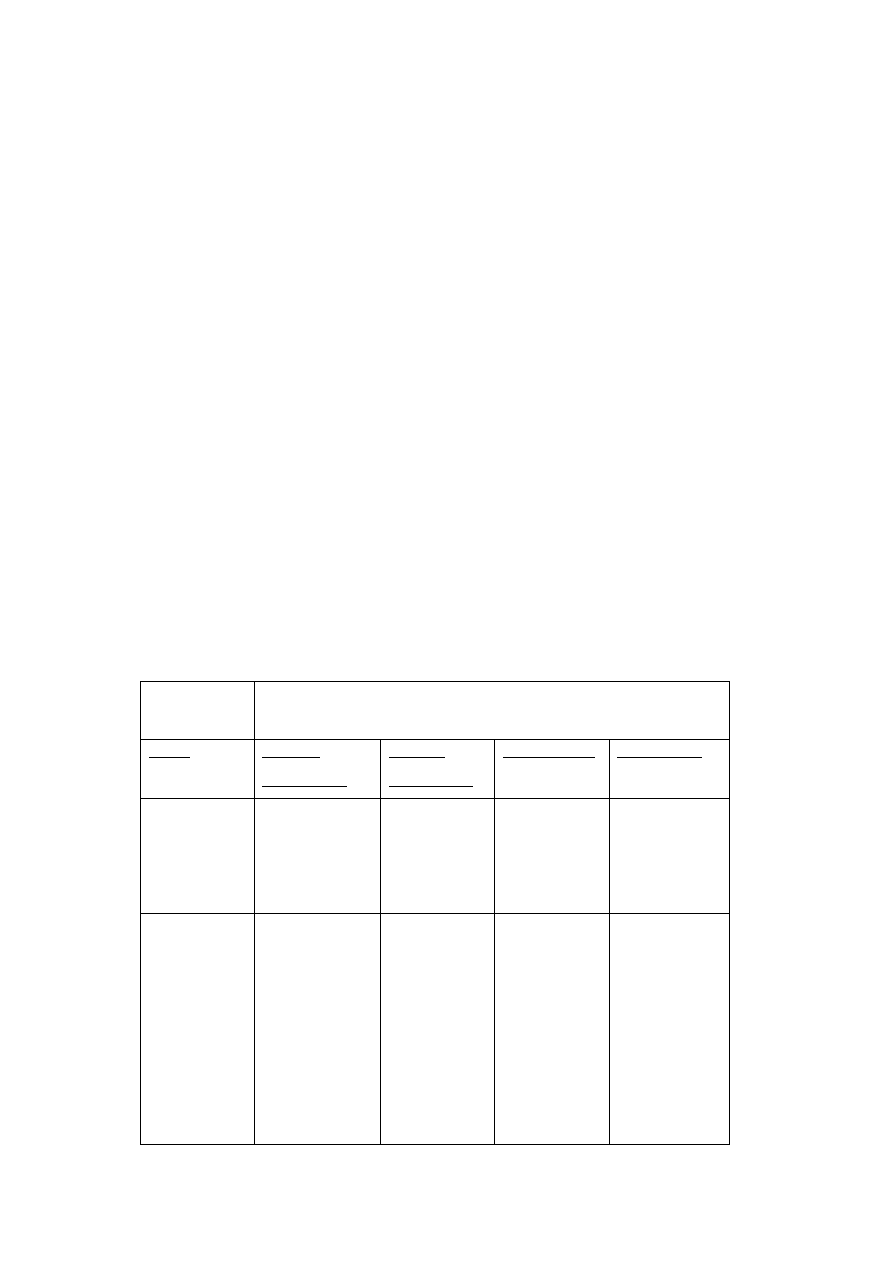

Table 1 – legal reserve

Equity

1000

Legal Reserve

150

Profits

1000

Profits allocated as Legal reserve

50

New Legal Reserve

200

20% of Equity

Profits distribution

950

Table 2 – other reserve

Equity

1000

Legal Reserve

200

Other Reserve

80

Profits

100

Intangibles

100

Profits allocated as Other reserve

20

New Other Reserve

100

Profits distribution

80

5.

Are there any differences in the tax treatment of stock and cash

Italy Country Report

February 2008

27

24

Civil Code, article 2426 and 2430

Italy Country Report

February 2008

28

Dividends are normally paid by cash. It’s possible to pay dividends so that hey are

taxed at the market value. In case of increase of the own equity with reserves, the

shareholders receive more shares that are not taxed until they are sold

6.

Have there been any changes in the tax regulation in recent years - since

2002 – that have had an important effect on the retention of earnings, the

distribution earnings or the reinvestment of profits for a particular

purpose?

YES

Until 2003 the Dual Income Tax was applicable: a rate of 19% was applied on a

specific part of income determined on the basis of the increase in net equity.

From 2004 interests paid on loan granted by holding companies or by

shareholders with at least 25% of shares are partially non deductible in case the debt

results 4 times higher than the net equity attributed to the shareholder

From 2004 a part of interests are non deductible in case the amount of the shares (to

whom is applicable the participation exemption) will be higher than the net equity

7.

Are there any current plans for tax reforms that have as their object to

have an impact on the retention of earnings?

YES

The Government is studying the modification of the taxation of the capital

gain, increasing the tax rate of some kind of capital gain.

25

For the Undertaking stock dividend means increased own equity. For the shareholder it

means additional shares in the Undertaking which may be untaxed until sold, unlike a cash

dividend.

26

D.P.R. 917, 22/12/1986, art. 47

27

D.P.R. 917, 22/12/1986, art. 98, Thin Cap

28

D.P.R. 917, 22/12/1986, art. 97, Pro Rata

Italy Country Report

February 2008

29

This new rule could facilitate the retention of earnings.

Italy Country Report

February 2008

30

PART 2 – TAX ASPECTS OF RETAINED EARNINGS VERSUS DISTRIBUTED PROFITS AND

WAGES

8.

What is the tax treatment of retained earnings compared to distribution of

earnings on the level of the Undertaking and at a combined level of

Undertaking (corporate) and business owner (individual)?

Earnings are taxed on the level of the Undertaking as taxable income.

The distribution of earnings does not involve a second level of taxation. However, in

case of distribution of particular no taxable reserve (for example the reserves

retained for revalutation of buldings) there will be a second level taxation.

Earnings distributed to business owners are partially (5% if the shareholder is a

company, if the shareholder is an individual person at maximum are taxed at 40% of

the amount received) taxed on the bases of individual income tax. In these case,

there is an economic double taxation at the undertaking level and at the business

owner level.

8.1. Is there an economic double taxation of distribution of earnings (taxation

of Undertaking income and then taxation on the distribution of earnings

at the Undertaking level or at the business owner level)?

YES

At first there is the taxation of undertaking income at a rate of 37.25 %. In case it

decides to distribute earnings to business owner he will be taxed on the 40% of the

dividend amount in case of majority shareholding applying the Irpef rates. In case of

minority shareholding, it will apply a 12.5% rate of deduction at source.

Income before tax

159

Tax 37.25 %

59

Earnings 100

Italy Country Report

February 2008

31

1. Owner with majority shareholding receiving 100 of dividends:

Dividend amount taxable 40% of 100 = 40

The income taxable of 40 will be added to others kind of income of the owner and

the total amount will be taxed with Irpef rates

Progressive Irpef rates from 01/01/2007:

Income (EURO)

Rates (%)

Up to 15.000

23

15.000-28.000 27

28.000-55.000 38

55.000-75.000 41

Over 75.000

43

2. Owner with minority shareholding receiving 100 of dividends:

Dividend amount taxable 100% of 100 = 100

Tax applicable 12.5% rate as deduction at source

100 x 12.5% = 12.50

3. Shareholder corporate

Also in this case there will be the taxation of undertaking income at a rate of 37.25

%.

The shareholder corporate will be taxed on 5% of dividends received applying the

normal income rate of 37.25 %.

INCLUDE RELEVANT TAX PROVISIONS IN 2002

AND SUBSEQUENT CHANGES UP TO 2007

Italy

Undertaking

Individual Business owner

Corporate

tax

33% N.A.

Income

tax n.a.

Irpef tax rates (see table

above)

Dividend tax

2002-2003

A) If the

shareholder is

A) the shareholder in this case

doesn’t pay taxes and doesn’t

Italy Country Report

February 2008

32

an individual

who owns less

than 25% of

the shares,

the company

applies on the

dividend

payed a

withholding

tax of 12,5%

b) if the

shareholder

owns more

than 25%, the

withholding

tax is not

applicable

declare the dividend cashed,

because the withholding

applied by the company is

definitive.

b) in this case the shareholder

has to declare the dividend

that concurs to the personal

income tax basis, but can use a

tax credit of 56,25% (51,51%

from 2003) of the dividend

received to avoid the double

taxation

Dividend tax

2004-2007

A) If the

shareholder is

an individual

who owns less

than 25% of

the shares,

the company

applies on the

dividend

payed a

withholding

tax of 12,5%

b) if the

shareholder

owns more

than 25%, the

withholding

tax is not

a)

In

case

of

minority

shareholding it will apply a

12.5% rate of deduction at

source and the shareholder

which received dividend

doesn’t pay anything

b) In case of a majority

shareholding, only on the 40%

of the dividend amount

applying the Irpef rates.

The tax credit was abolished

and was introduced a limited

taxation, but there is always a

limited double taxation

Italy Country Report

February 2008

33

applicable

Dividend

credit 2002-

2003

N.A.

56,25% of the dividend cashed

that off set the corporation

tax.

51,51% from 2003

Dividend

credit 2004-

2007

N.A. n.a.

Capital gains

tax

n.a. n.a.

If option for

Transparent

treatment

chosen 2004-

2007

The earnings of the undertaking

are always taxed by the

shareholder even if not cashed,

so in case of collection of

dividend the shareholder

doesn’t pay taxes anymore

9.

Please described the differences in the tax treatment of distribution of

earnings realised as a capital gain in the context of a sale of the shares or

of the business compared to that (i) of retained earnings, (ii) of wages

salaries paid to the business owner and (iii) of a loan granted by the

Undertaking to the business owner?

The capital gain realized selling shares, if the shares are subject to the Pex, is

taxable only at 9% (in 2006), 16% (in 2007) of the capital gain realized.

The capital gain realized selling an enterprise is completely subject to the

corporation tax.

With the capital gain realized, the company may decide to distribute earnings, retain

it, pay salary to the business owner and grant a loan to the businnes owner.

If the company distributes earnings it is not subject to taxation, but the shareholder

will be taxed.

Italy Country Report

February 2008

34

If the company decides to retain earning no taxes are due and there is an increase of

the net equity that in some case permits to deduce more payable interests (Thin cap

rules- pro rata rules).

The company can decide to pay a salary to the business owner. This salary will be

deductible from the tax basis (subject, for the corporation, to the tax rate of 33%).

This salary will increase the personal income of the businnes owner that is taxed at

the progressive rates. In some case, the total tax burden of the company and the

shareholder can be reduced.

The loan to the shareholder can be remunerative or not.

If it is remunerative, it is necessary to evaluate the total tax burden considering the

tax charge of the company and the tax charge of the shareholder.

INCLUDE RELEVANT TAX PROVISIONS IN 2002 AND SUBSEQUENT CHANGES

UP TO 2007

Italy

Distributed

profits

Retained

Profit

Wages/Salaries

to business

owner

Loan to business owner

Sale of

shares

The net

equity is the

same. The

company

doesn’t have

any tax

consequences

The net

equity

increases.

The company

may have a

reduction of

the basis due

to Thin cap

and pro- rata

(these rules

have been

introduced

from 2004)

The salary cost

are deductible

from the tax

basis. It’ s

possible to

have a

reduction of

the total tax

burden of the

company and

the shareholder

If the loan is

remunerative it’s

possible to modify the

total tax burden of the

company and the

shareholder.

Sale of

business

The net

equity is the

same. The

company

doesn’t have

The net

equity

increases.

The company

may have a

The salary costs

are deductible

from the tax

basis. It’ s

possible to

If the loan is

remunerative it’s

possible to modify the

total tax burden of the

company and the

Italy Country Report

February 2008

35

any tax

consequences

reduction of

the basis due

to Thin cap

and pro- rata.

these rules

have been

introduced

from 2004)

have a

reduction of

the total tax

burden of the

company and

the shareholder

shareholder.

…

….

10.

Is the combination of wages (paid to the business owner by the

Undertaking), profit distributions and retained earnings a tax planning

issue that is anticipated and addressed by business owners in view of

minimising the overall tax burden of the business owner and the

Undertaking?

YES

In case of profit distribution without paying salary, the Undertaking will have a major

taxable income. The owner will pay 40% of the dividend amount in case of majority

shareholding applying the Irpef rates. In case of minority shareholding, it will apply

a 12.5% rate of deduction at source.

Paying a salary, the Undertaking will have a minor taxable income but the owner will

pay more taxes on salary.

11.

In respect to the previous question, is the business owner more interested

in minimising his/her tax burden and then the Undertaking’s or both

equally?

Both cases are equal in view of minimising the overall tax burden.

12.

Are there instances in which minimising the tax burden of the business

owner would mean dramatically increasing the tax burden of the

Undertaking?

In case of profit distribution without paying salary, the Undertaking will have a major

taxable income. The owner will pay 40% of the dividend amount in case of majority

shareholding applying the Irpef rates. In case of minority shareholding, it will apply

a 12.5% rate of deduction at source.

Paying a salary the Undertaking will have a minor taxable income, but the owner will

pay more taxes on salary.

Table 3

Case 1a

Undertaking

Salary

0

Income before tax

159

Tax 37,25%

59

Profit

100

Profit distributed

100

Owner taxation

11,52

Total tax (Undertaking+Owner)

70,52

Case 1b

Profit distributed

100

Owner taxation

12,5

Total tax (Undertaking+Owner)

71,5

calculated on 40% of dividend applying Irpef

rates (2007) in case of majority shareholding

calculated on 100% of dividend applying 12.5%

rate in case of minority shareholding

Table 4

Italy Country Report

February 2008

36

Case 2

Undertaking

Salary

100

Income before tax

59

Tax 37,25%

22

Profit

37

Profit distributed

0

Owner taxation

36,17

Total tax (Undertaking+Owner)

58,17

calculated applying Irpef rates

(2007)without considering the social

contribution of about 10%

13.

For corporate income tax or capital gains tax purposes, are there any

incentives/disincentives to retain earnings rather than distribute them or

pay wages?

YES

Until 2003 the Dual Income Tax was applicable: a rate of 19% was applied on a

specific part of income determined on the basis of the increase in net equity.

From 2004 there are the Thin Cap and Pro Rata rules permitting a major

deduction of payable interest in case of increasing net equity.

13.1.

Are there any limitations or ceilings for these incentives?

Yes

From 2004 interests paid on loan granted by holding companies or by

shareholders with at least 25% of shares are partially non deductible in case debt

results 4 times major than the net equity attributed to the shareholder

From 2004 a part of interests are non deductible in case the amount of the shares (to

whom the participation exemption is applicable) is higher than the net equity

29

D.P.R. 917, 22/12/1986, art. 98 (Thin Cap), art. 97 (Pro Rata)

30

D.P.R. 917, 22/12/1986, art. 98, Thin Cap

31

D.P.R. 917, 22/12/1986, art. 97, Pro Rata

Italy Country Report

February 2008

37

Italy Country Report

February 2008

38

13.2.

Is there a risk that these incentives can be used more than one

time by the business owners by splitting up the business activities

into different legal entities?

NO

Because it is better having a company with a bigger net equity.

14.

What is the tax treatment of declared loans granted by the Undertaking to

the business owner?

The interest collected by the Undertaking is ordinary revenue and concurs to the net

profit and to the tax basis of the Undertaking.

14.1. Is there a minimum interest rate to be charged for tax purposes?

The level of interest must be at the same level of the market price.

14.2. How is the interest rate treated for tax purposes for the

Undertaking?

They are financial revenues that concur to the determination of the tax basis of

the Undertaking.

14.3. How is the interest rate treated for tax purposes for the business

owner?

Italy Country Report

February 2008

39

It is a capital income taxed at the ordinary tax rate applicable to the individual

person.

14.4. What are the combined tax effects of such a loan compared to a

distribution of earnings equivalent in amount?

The distributions of dividends have no tax effects for the Undertaking.

The loan granted by the Undertaking to the Business Owner and the related

interest revenue provide an increase of the net profit and the tax basis.

15.

Are there any other taxes (e.g. net worth tax) which are imposed or based

on the net equity of the Undertaking?

NO

16.

Are there any other tax incentives for either the retention of earnings or

their distribution of profits?

NO

Actually the increase of the net equity permits a major deduction of interest

expenses due to the Thin cap and Pro-rata rules.

Italy Country Report

February 2008

40

PART 3 – TAX ASPECTS OF RETAINED EARNINGS FINANCING VS DEBT FINANCING

17.

In debt financing, what is the tax treatment of interest expenses paid or

accrued by the Undertaking?

Interest expenses are normally deductible.

17.1. Is there a different tax treatment to deductions on interest paid when

the lender is a resident or a non-resident for tax purposes?

It is the same but, in some cases, there are witholding tax problems on the payment

of abroad interest.

17.2. Is there a different tax treatment on interest on long-term debt and

interest on short-term debt?

NO, it is the same.

18.

Are there any tax benefits that are actionable based on specific amounts of

equity (e.g. notional interest expense based on the increase of own equity

or the total amount of equity)?

Interest expenses are normally deductible under three specific conditions: revenues

higher than 7,500,000 euros; loan granted by holding companies or major partner

and annual average financial stock higher than 4 times of holding net equity;

interest expenses are partially non deductible in case debt results major than the net

equity attributed to holding company for a determined quantity.

Italy Country Report

February 2008

41

There is also the Pro Rata rule that indicates that a part of interests are non

deductible in case the amount of the shares (to whom is applicable the participation

exemption)is higher than the net equity.

18.1. What is the exact calculation method used to implement this incentive

and to evaluate the benefits once this incentive is implemented?

The three conditions mentioned above should been verified.

1. evenues higher than 7,500,000 euros,

2. loans should be granted directly by the major partner

3. the total amount of the loan ( calculated on the annual average financial

stock ) should be higher than four times the net equity of the major partner

If the three conditions are verified we could calculate the deductible and not

deductible interest costs.

For example,

taking an annual average financial stock of 1000 and considering the net equity of

the major partner of 200 and considering an average return rate of 5% we obtain an

interest expense of 50.

The ratio between the annual average financial stock (1000) and net equity of the

major partner (200) is equal to 5 major than 4 (condition number 3).

The not deductible interest costs are calculated using the over financing quote

multiply by the average return rate.

The over financing quote (200) is calculated subtracting from the annual average

financial stock (1000) four times the net equity of the major partner (200 x4= 800)

Multipling the over financing quote (200) by the average return rate (5%) we obtain