Capital Structure Policy

Tomasz Słoński, PhD

Creating Value through

Financing

1.Reduce Costs or Increase

Subsidies

Certain forms of financing have tax

advantages or carry other subsidies.

2.Create a New Security

Sometimes a firm can find a previously-

unsatisfied clientele and issue new

securities at favorable prices.

In the long-run, this value creation is

relatively small.

2

Basic principles of financing

costs

1. The cost of all sources of financing is

given by the risk profile and the required

rate of return of the investment.

However, the immediate direct

consequences of financial choices cannot

be neglected.

2. For the purpose of managing the liability,

it’s a mistake to take the explicit cost of

a source of financing as its true cost.

3

Implicit costs of outside capital

• The implicit costs of outside capital

are important determinants of capital

selection

– Distressed costs

– Market signaling

– Restricted access to outside financing in

the future

– Incentive effects

4

Treasurers’ policy

1. Corporate treasurers allocate the

cheapest resources to the more

predictable portion of their borrowing

requirements.

2. They then adjust their credit levels using

the financing that is easily available

(bank loans for large groups, overdrafts

in the case of small and medium

enterprise) as new information emerges.

5

Treasuerers’ policy

3. When unexpectedly faced with large

funding requirements, they call on the

resources immediately available, which

are then gradually replaced by less

costly or better structured resources

(term loans, guarantees, etc.)

4. Corporate treasurers have to diversify

their sources of funds to avoid becoming

dependent on the specific features of a

given category of financing.

6

Equity financing

• Organic growth financing and

low-risk profile equity

investments

– Internal source of equity

– Managers’ capital

– Public market (alternative or main floor)

– Shares acquired by new partners or

strategic investor

7

THE EQUITY GAP

Many SME is not willing or able to sell new

equity:

- the opportunity cost is to high

- the threat of losing control

- the information asymmetry is too high

For this kind of companies the question is how

For this kind of companies the question is how

much debt is available?

much debt is available?

Additionally, for SME the choice between bank

financing (bank loans) and market financing is

skewed in favour of bank financing.

8

Equity financing

• External growth financing

(high-risk profile)

– Investment banks

– SPE (special purpose entity)

– Private equity/Venture capital

– Hedge funds

– Manager’s capital in case of

Management Buy Out

9

Private equity

• Private equity make multiple-year investment

in illiquid assets where they can control and

influence over operations or asset

management to influence their long-term

returns. Private equity usually finance:

o

mezzanine financing for start-up projects,

o

wholesale purchase of a privately held company

o

growth capital investments in existing businesses

o

leveraged buyout of a publicly held asset

converting it to private control.

10

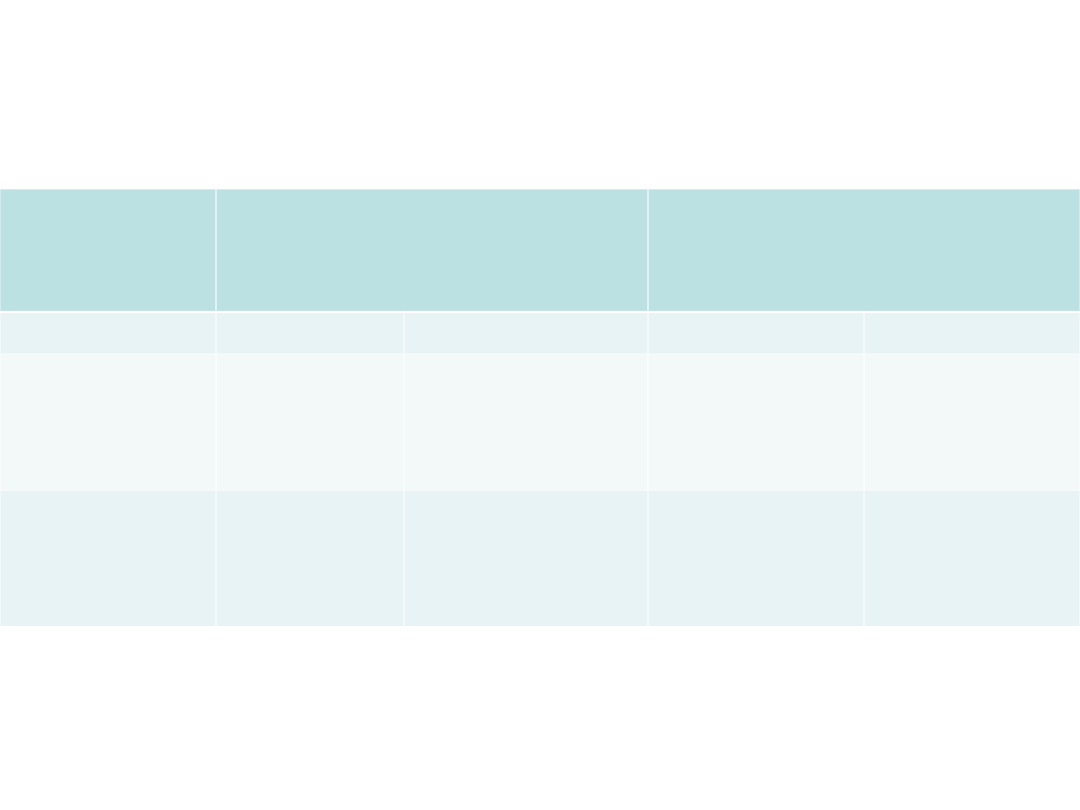

Debt financing

Bank financing Market

financing

Short-term

Long-term

Short-term

Long-term

Asset backed

Factoring

Collateralised

bank loan

Sale/leaseback

Securitization

(asset-backed

commercial

paper)

Securitization

(asset-backed

securities)

Unsecured

Bank

overdraft

Credit

facility

Senior and

subordinated

bank loan

Commercial

paper

Bonds

11

The cost determinants of intermediated

borrowing differ significantly from

market debt

• The interest rates agreed in Continental

Europe between a company and its bank

generally

do not correspond

do not correspond to the actual

cost of funds (money market characteristics)

• The low explicit cost reflects:

– So-called crossing (charging for other services)

– Bank’s strategic choice

– The bank’s financial position (direct and fixed

costs of risk provision, Basel II)

– Company’s bargaining strength

12

Investment banking

• One or more banks may form an

underwriting syndicate to buy the

securities issued and endeavour to

resell them immediately on the market

(firm underwriting).

• Banks can also simply act as agents

selling the securities to investors

without taking any responsibility (best

efforts).

13

bank financing vs market

financing

• Bank loans can be obtained

fairly

fairly

rapidly

rapidly.

• Companies can borrow

the exact

the exact

amount

amount

• Bank loans impose

greater

greater

constraints

constraints on the company with

covenants and guarantees to their

loans

14

Guarantees

•

business loans

business loans, guaranteed solely by the

prospects of the lending company, in

other words, by its financial health

(general balance sheet financing);

•

Specific-purpose loan, secured by the

Specific-purpose loan, secured by the

transaction or asset that they have

transaction or asset that they have

helped finance

helped finance. Collateralised loans are

probably the oldest and most significant

in this category. In general, the amount of

credit granted does not exceed the value

of the asset pledged by the borrower.

15

Covenants

• Positive or affirmative covenants are agreements

to comply with certain capital structure or earnings

ratios, to adopt a given legal structure or even to

restructure.

• Negative covenants can limit the dividend payout,

prevent the company from pledging certain assets to

third parties (negative pledges) or from taking out new

loans or engaging in certain equity transactions, such

as share buybacks.

• Pari passu clauses are covenants whereby the

borrower agrees that the lender will benefit from any

additional guarantees it may give on future credits.

• Cross default clauses specify that, if the company

defaults on another loan, the loan which has a cross

default clause will become payable even if there is no

breach of covenant or default of payment on this loan.

16

Syndicated loans

• Syndicated loans are typically set up for

facilities exceeding €100 mil. that a single

bank does not want to take on alone.

• The lead bank (or banks depending on the

amounts involved) is in charge of arranging

the facility and organising a syndicate of 5–20

banks that will each lend part of the amount.

• Once lending terms are set, pieces of the loan

are sold to other banks. Some bank lenders

are members of the syndicate while others

are not, and buy only ‘‘participations’’ (so-

called quasi-syndication).

17

Lenders’ rationale for using

syndicated credits

• Diversification of bank loan portfolios.

• Reduced risk of default against syndicate

vs. a single bank.

• Access to deals/credits not otherwise

available to some banks.

• Upfront fee income (to managers) + loan

trading and derivative sales potential.

18

Borrowers’ rationale for using

syndicated credits

• The potential to raise larger amounts than

from a single bank.

• The possibility of doing few visits to the

market. This in turn determines lower fixed

costs and scale economies.

• Enhanced visibility among a larger group

of lenders.

• The tradability of syndicated loans. Their

high liquidity determines lower rates.

19

Types of syndicated loans

1. Committed facilities, a legally enforceable

agreement that binds bank to lend up to stated

amounts.

2. Revolving credits. In this case, the borrower has the

right to borrow or ‘‘draw down’’ on demand, repay

and then draw down again. The borrower is charged a

commitment fee on unused amounts. Options include:

– multi-currency option: right to borrow in several currencies;

– competitive bid option: solicit best bid from syndicate

members;

– swingline: overnight lending option from lead manager.

3. Term loans

4. Letters of credit

20

Subordinated (junior) debt

• Subordinated/unsecured creditors

represent a guarantee for the other

creditors because, by increasing the

assets, they contribute to the company’s

solvency.

• Subordinated/unsecured debt allows

creditors to choose the level of risk they

are willing to accept, ensuring a better

distribution of risks and remuneration.

21

Document Outline

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

- Slide 17

- Slide 18

- Slide 19

- Slide 20

- Slide 21

Wyszukiwarka

Podobne podstrony:

196 Capital structure Intro lecture 1id 18514 ppt

197 Capital structure lecture Gdansk 2006 Lecture 2id 18521 ppt

capital structure problem list number 1

196 Capital structure Intro lecture 1id 18514 ppt

Designing the capital structure

A Cebenoyan Risk Management, capital structure and lending at banks Journal of banking & finance v

Structures sp11

4 Plant Structure, Growth and Development, before ppt

Fiscal Policy

Fundusze venture capital

Homework Data Structures

policy work dev

Lesley Jeffries Discovering language The structure of modern English

1916 03 29 Rozporządzenie policyjne Prezydenta Galicjiid 18455

2011 08 KGP Ceremonial policyjn projektid 27380

MANDAT-za-złe-parkowanie, █▬█ █ ▀█▀ RADARY POLICYJNE - instrukcje, Radary- anuluj sobie mandat

07.10.12r. - Wykład -Taktyka i technika interwencji policyjnych i samoobrona, Sudia - Bezpieczeństwo

więcej podobnych podstron