Financial Market

Derivatives Market – Forward & Futures

BUYER

SELLER

Participans:

The deal:

For a specific period of time

BUYER

will have an

OBLIGATION to buy

some underling security for a price specified

today.

Forward’s features:

gives an obligation to buy (buyer –

long position

) or to sell

(seller –

short position

) of a particular security at price specified in contract.

WRITER

has an

OBLIGATION

to deliver

the underlying security.

Strike (Exercise price) (K) = price at which the underlying transaction will occur

upon exercise.

Expiration date / Settlement date (Maturity) (T) = the day when the forward

expiry.

Multiplier (N) = the quantity of the underlying asset.

Underlying security = what security is going to be traded.

FORWARD CONTRACT

=

Financial Market

Derivatives Market - Forward

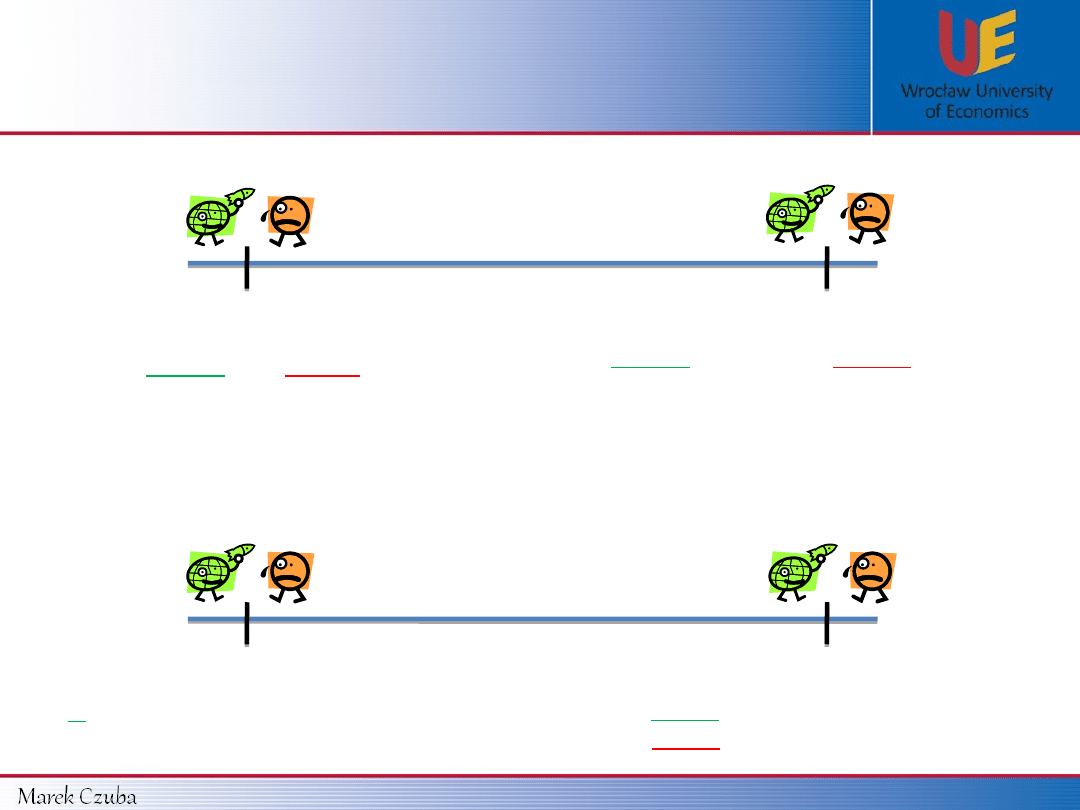

Today

Maturity

Buyer

and

seller

specify a contract

details.

Buyer

must buy,

Seller

must sell

underlying security at priced specified

before.

Example 1:

A is signing a contract with B specifying that in December he will buy 10 Christmas

trees paying 100$ per tree.

Today

December

A

commits to buy 10 Christmas

trees from

B

in December.

A must

buy 10 Christmas trees.

B must

sell 10 Christmas trees.

Financial Market

Derivatives Market - Forward

Data from example 1:

What the

buyer

is about to do at maturity ?

Underlying security = Christmas Tree

N = 10

T = December

K = 100$

Let’s assume that Christmas tree price in December is going to be:

a) S

T

=

150$

b) S

T

=

120$

e) S

T

=

100$

c) S

T

= 80$

d) S

T

=

50$

Even thought the current Christmas tree price is higher, the

buyer

will buy

it

for 100$

. His profit will be equal to

a) 50$

or

b) 20$ per

tree

if he will sell the Christmas tree at the market immediately.

Totally he will

earn

to

a) 500$

or

b) 200$

.

Even thought the current Christmas tree price is lower, the

buyer will

have to buy

it

for 100$

. He will

lose c) 20$

or

d) 50$ per tree

if he

will sell the Christmas tree at the market immediately. Totally he will

lose c) 200$

or

d) 500$

.

Buyer won’t make any profit or loss.

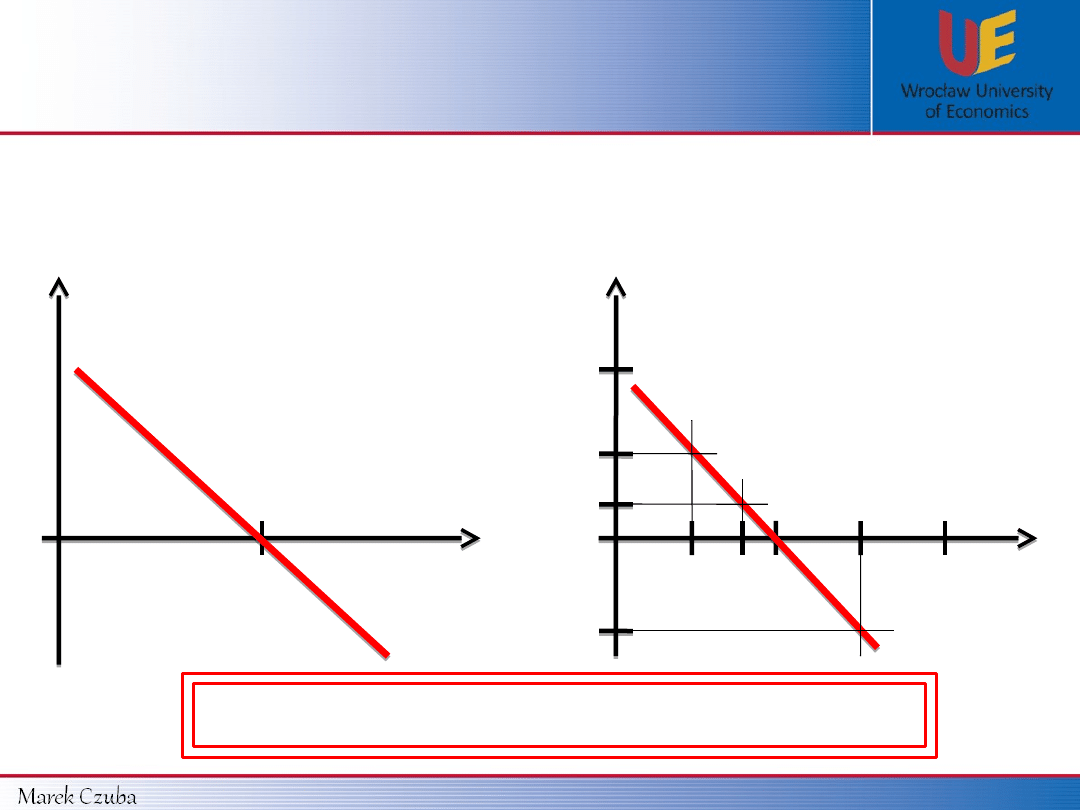

Financial Market

Derivatives Market - Forward

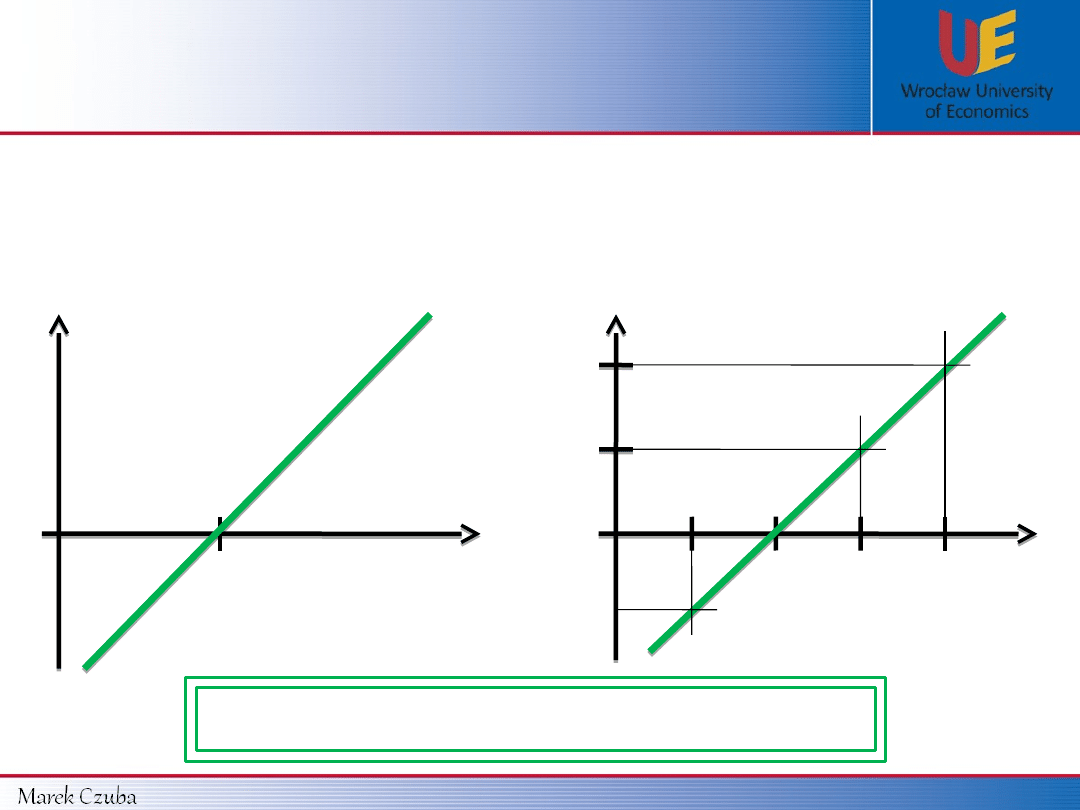

Forward’s

buyer

profit function:

K

0

S

T

Profit

In general:

100$

0

S

T

Profit

Data from example 1 (K = 100$, N =

10):

150$

200$

50$

500

$

1000

$

S

T

– K

Profit function for a

buyer

of a

forward =

- 500$

Financial Market

Derivatives Market - Forward

Data from example 1:

What the

seller

is about to do at maturity ?

Underlying security = Christmas tree

N = 10

T = December

K = 100$

Let’s assume that Christmas tree price after T is going to be:

a) S

T

=

150$

b) S

T

=

120$

e) S

T

=

100$

c) S

T

= 80$

d) S

T

=

50$

Even thought the current Christmas tree price is higher, the

seller

must sell

it

for 100$

. If the seller doesn’t own 10 Christmas trees, he

needs to buy them from the market and then sell it to the forward’s

buyer. He will

lose a) 50$

or

b) 20$

per tree. Totally seller will

lose a)

500$

or

b) 200$.

Even thought the current Christmas tree price is lower, the

seller will

sell

it

for 100$

. If the seller doesn’t own 10 Christmas trees, he needs

to buy them from the market and then sell it to the forward’s buyer. He

will

gain c) 20$

or

d) 50$

per tree. Totally seller will

gain a) 500$

or

b) 200$.

Seller won’t make any profit or loss.

Financial Market

Derivatives Market - Forward

K

0

S

T

100

$

0

S

T

150$

200$

50$

500

$

1000$

K – S

T

80

$

200

$

Profit

In general:

Profit

Data from example 1 (K = 100$, N =

10):

Forward’s

seller

profit function:

Profit function for a

seller

of a

forward =

500

$

Financial Market

Derivatives Market - Forward

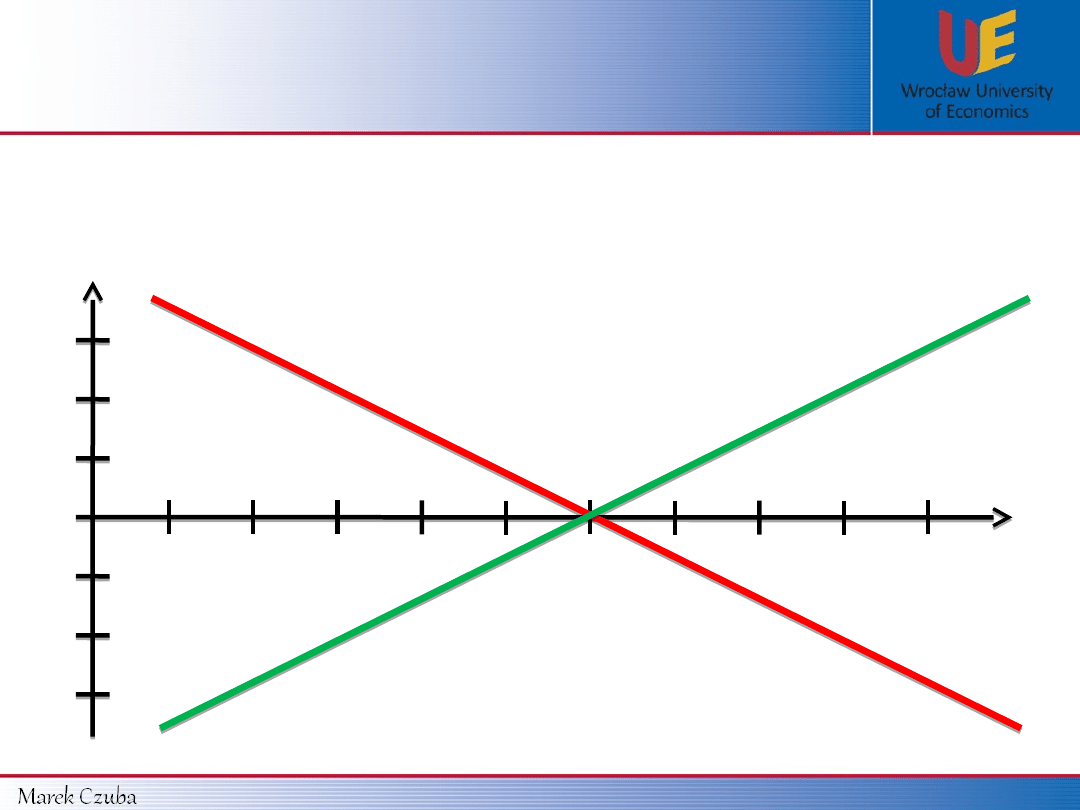

Long vs Short position:

0

S

T

$

K

Lo

ng

Po

sit

ion

Sho

rt P

ositi

on

Financial Market

Derivatives Market - Forward

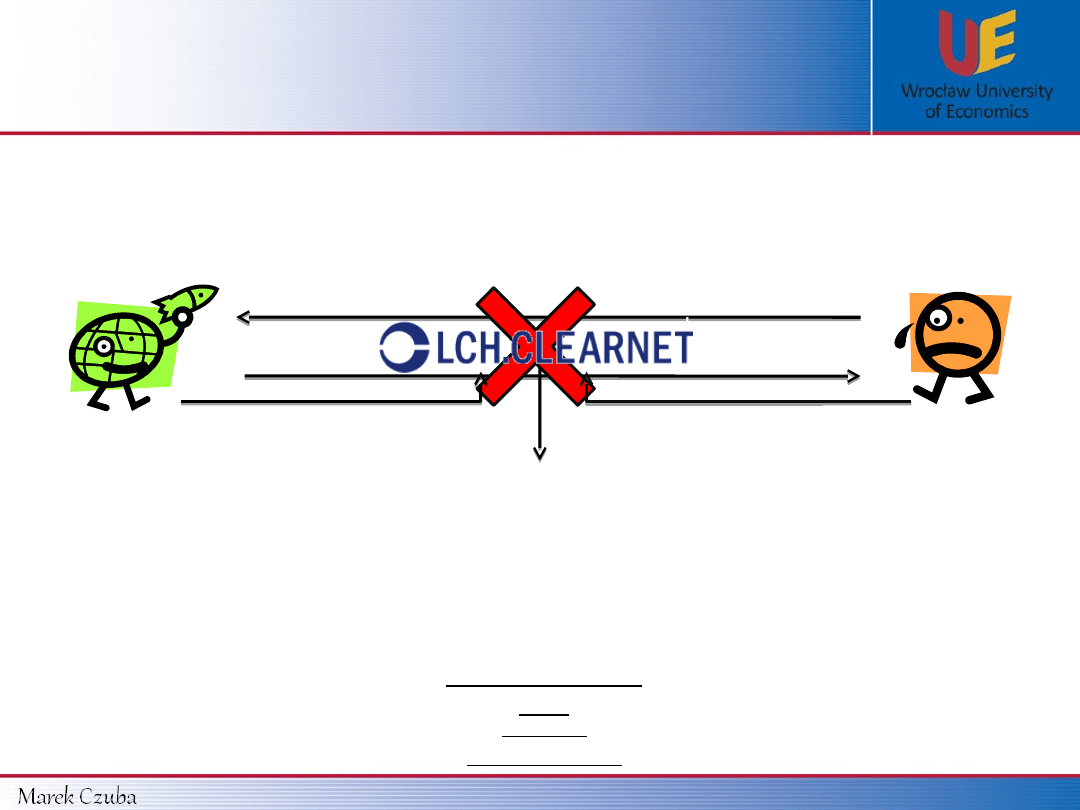

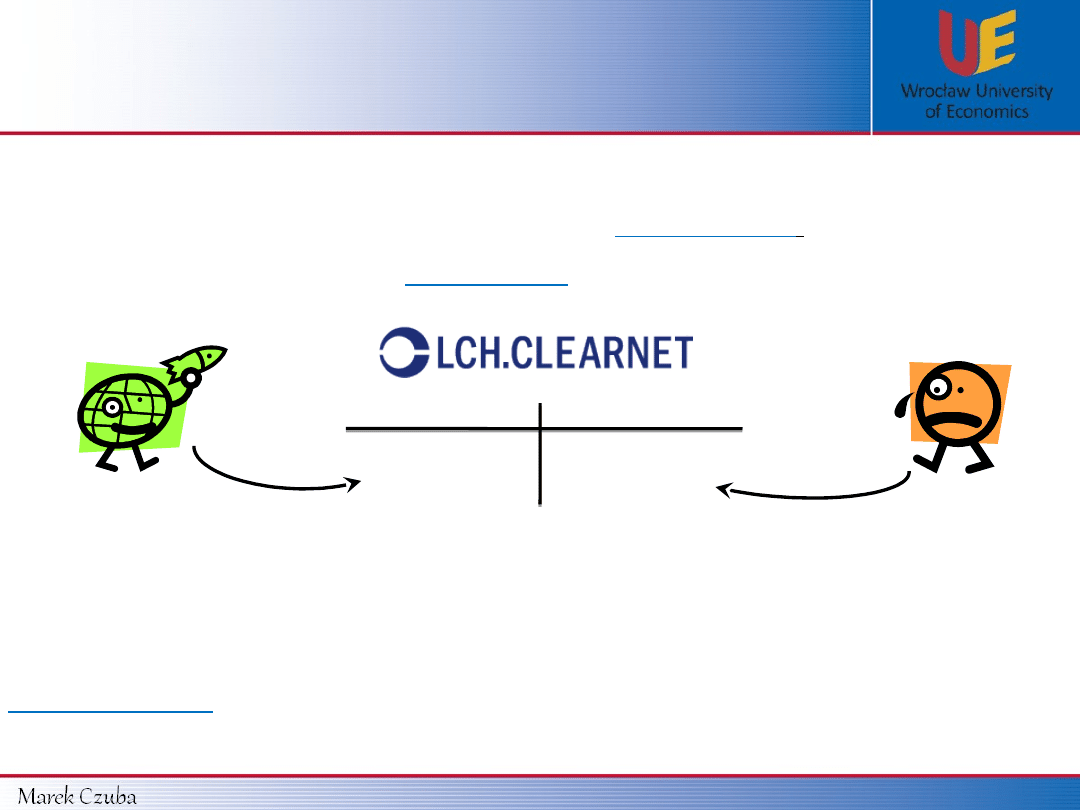

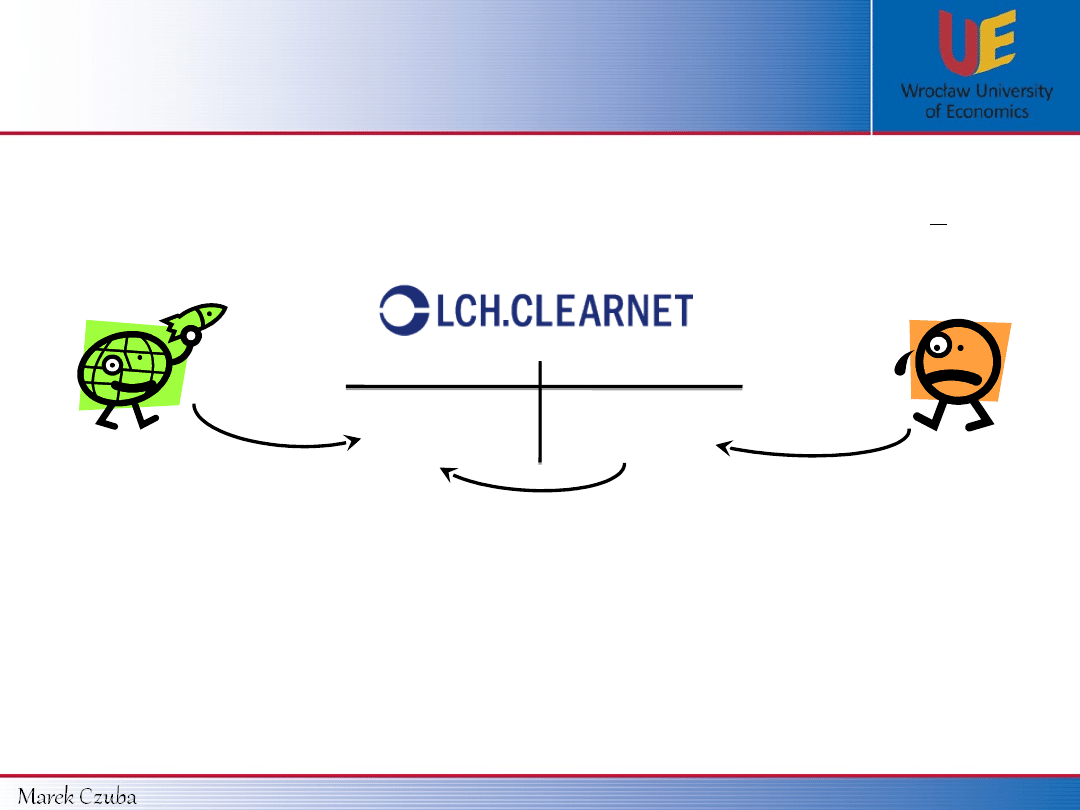

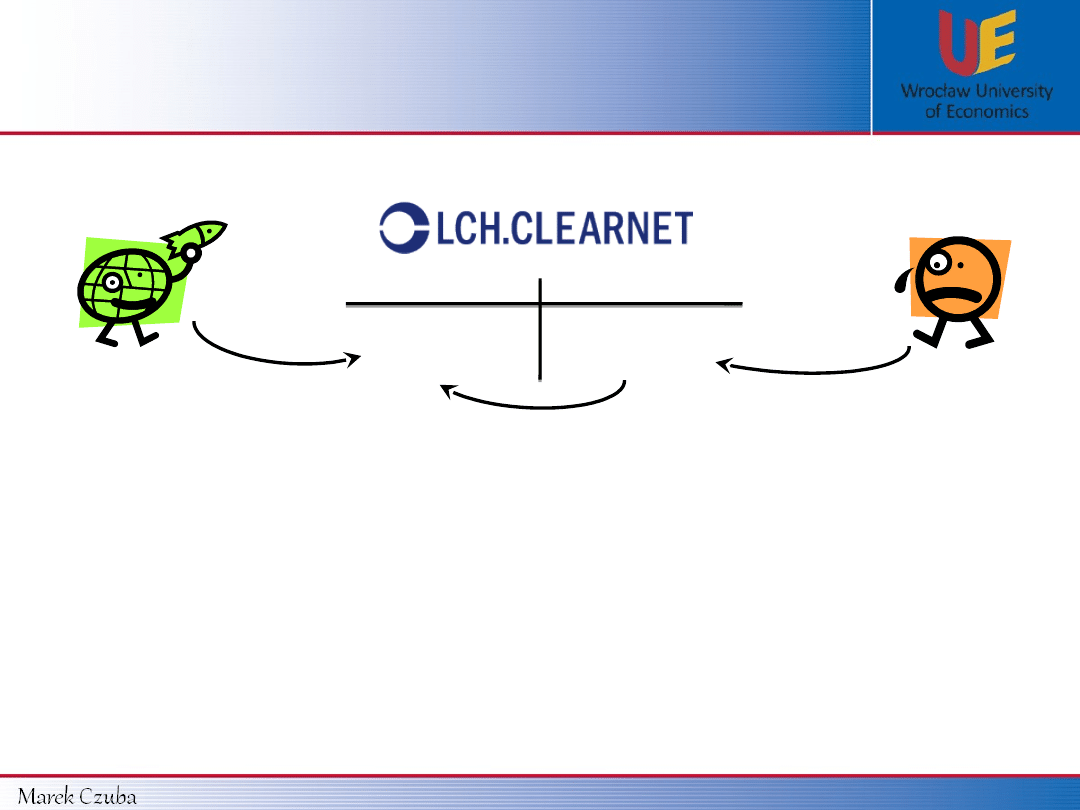

Futures contract = standardized forward contract.

BUYER

SELLER

Setting contract specification

specifies Futures parameters:

Underlying securities

Quantity

Settlement date

Takes deafault

risk

Clears

transaction

Financial Market

Derivatives Market - Futures

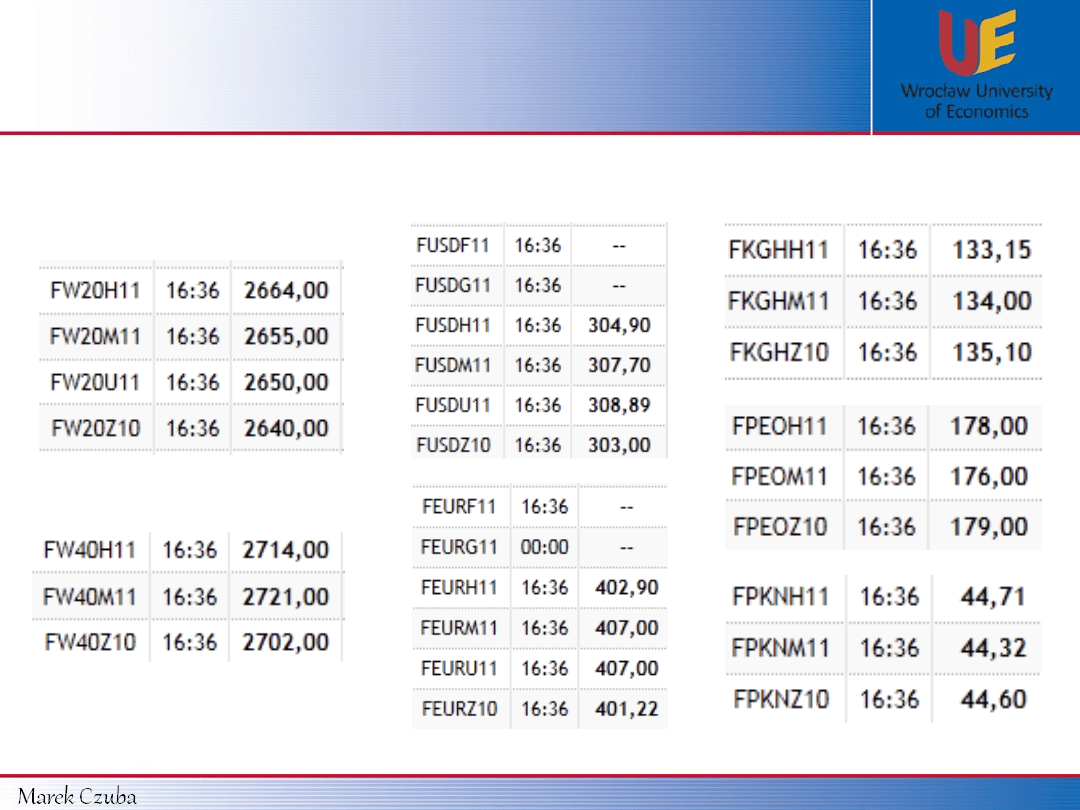

Indices:

WIG20:

FW20xx

Stocks:

TPSA: FTPSxx

PKN : FPKNxx

Currencies:

Euro: FEURxx

USD: FUSDxx

F

W20

Z

12

Futures

Underlying instrument sybmol

Maturity:

Month

,

Year

F: January

G:

February

H: March

J: April

K: Mai

M: June

V: October

X: November

Z: December

N: July

Q: August

U:

September

Examples:

Financial Market

Derivatives Market - Futures

Warsaw Stock Exchange (Friday, 26 XI 2010)

Multiplier: 10

Multiplier: 10 000

Multiplier: 100

Financial Market

Derivatives Market - Futures

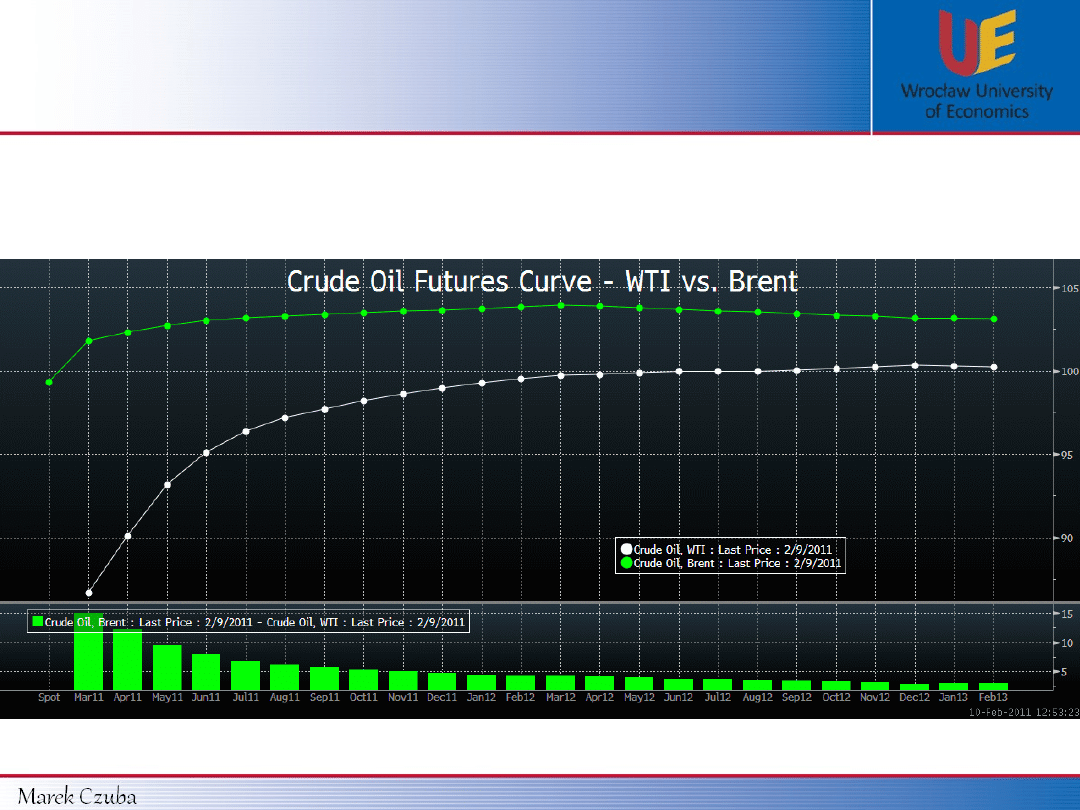

Financial Market

Derivatives Market - Backwardation

Backwardation

(normal futures yield)

Financial Market

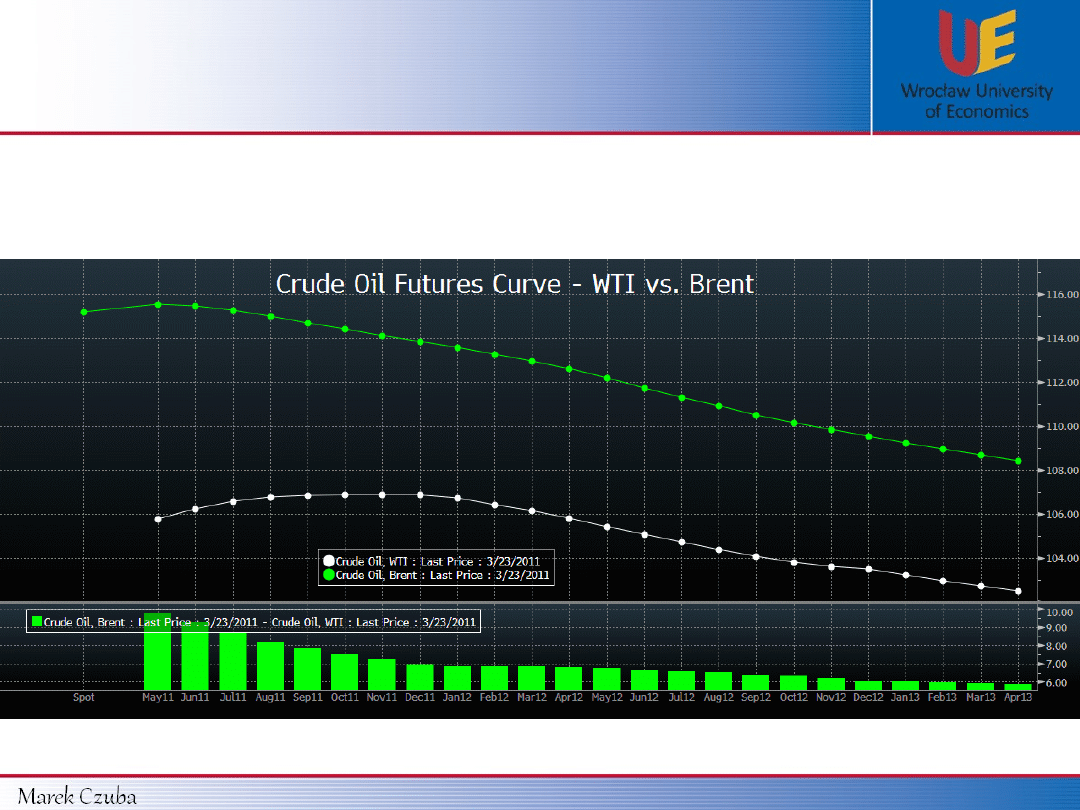

Derivatives Market - Contango

Contango

(inverted futures yield)

Financial Market

Derivatives Market - Backwardation & Contango

From Backwardation to Contango

Financial Market

Derivatives Market - Backwardation & Contango

How clearing companies maintain the default risk ??

1. Both sides must provide

Initial Margin

SELLER

BUYER

Buyer’s Account

Seller’s Account

Let’s assume TVN stock market price is 9 zł.

FTVNZ13 price is 10 zł (N = 100). Initial margin for TVN stock futures contracts is

15,00%.

Futures price * multiplier * initial margin level * number of contracts

=

Initial margin =

= 10 * 100 * 15,00% * 1 = 150 zł

150 zł

150 zł

Financial Market

Derivatives Market - Futures

2. Daily Profit/Loss has to be

paid in cash

by participants (

from Initial Margin

)

When the underlying security price changes rapidly,

initial margin might be not enough to prevent default risk:

SELLER

BUYER

Buyer’s Account

Seller’s Account

Let’s assume that the price of FTVNZ13 raises from 10.00 zł to 10.50 zł at closing.

150 zł

150 zł

50 zł

25 zł

275 zł

The next day FTVNZ13 futures price raises from 10.50 zł to 11.25 zł.

75 zł

100 zł

200 zł

If the price of FTVNZ13 will continue to raise, seller won’t be able to pay the buyer.

Financial Market

Derivatives Market - Futures

Futures price * multiplier * maintenance margin level * number of contracts

=

Maintenance margin =

= 10 * 100 * 10,00% * 1 =

100 zł

Because the futures price can change rapidly until maturity,

clearing companies came up with idea of

maintenance margin

.

Maintenance margin

is just the amount of money, our account cannot go below.

If it will, we are required to refill our account

to the level of initial margin

.

Let’s assume TVN stock market price is 9 zł.

FTVNZ13 price is 10 zł (N = 100).

Initial margin

for TVN stock futures contracts is

15,00%

,

maintenance margin

is

10,00%

.

Initial margin =

10 * 100 * 15,00% * 1 =

150 zł

Financial Market

Derivatives Market - Futures

SELLER

BUYER

Buyer’s Account

Seller’s Account

250 zł

150 zł

1. FW20Z11 = 10 zł,

Margins: Initial: 15,00%, Maintenance: 10,00%

2. FW20Z11 = 11 zł,

100 zł

50 zł

150 zł

Seller account is below maintenance margin (50 zł <

110 zł).

115 zł

165 zł

3. FW20Z11 = 11.30

zł,

30 zł

135 zł

280 zł

Margins:

Initial: 150

zł,

Maintenance: 100

zł

Margins:

Initial: 165 zł,

Maintenance: 110 zł

It needs to be refill to initial margin level

(165 zł).

Maintenance: 113 zł

Margins:

Financial Market

Derivatives Market - Futures

Market

Exchange

OTC

Standardization

Standardized

Negotiable

Risk

Taken by clearinghouse Default risk

Settlement

Marking to market

At delivery

Initial margin

Yes

No

FUTURES

FORWARD

Financial Market

Derivatives Market – Forward vs Futures

Document Outline

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

- Slide 17

- Slide 18

- Slide 19

- Slide 20

Wyszukiwarka

Podobne podstrony:

Forward Futures

forward futures

kontrakty futures i forward (7 stron) 6XOASEQA6JZ6UMUE63OED7ZWNUVGLVDG3MVPAJI

kontrakty futures and forwards prez

141 Future Perfect Continuous

2010 regional future plid 27071 ppt

hawking the future of quantum cosmology

Future Simple Użycie

A Toffler Future Shock

Lekcja 20 Czas Future Perfect, lekcje

28 Future neurosurgery

FUTURE

Future Simple Budowa

Future Perfect Simple Użycie

Linear Motor Powered Transportation History, Present Status and Future Outlook

Edmond Hamilton Captain Future's Worlds of Tomorrow 17 Futuria

Edmond Hamilton Captain Future's Worlds of Tomorrow 05 Mars

test Exercise 9 Verbs Future

więcej podobnych podstron