High Probability Futures Options

Trading with Seasonal Straddles

Steve Lentz

Director of Education and Research

OptionVue Research, Inc.

Disclaimer

Option trading can involve highly volatile

returns and unlimited risk. Option trading is

not suitable for every investor.

Results depicted in this presentation come

from historical and theoretical option prices.

Future results will vary and not necessarily

match the results presented here.

Overview

Introduction to the Straddle Play

The Role of Volatility

Coffee

Soybeans

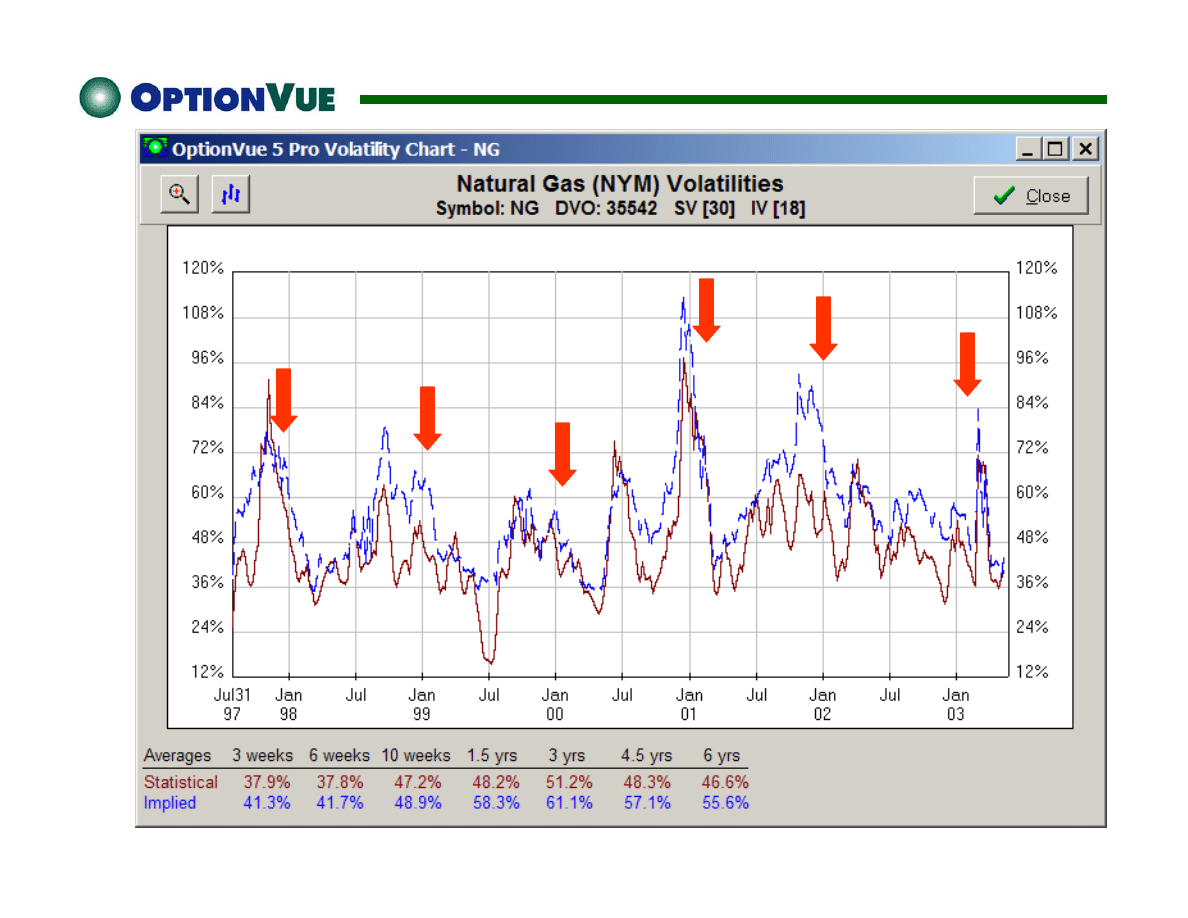

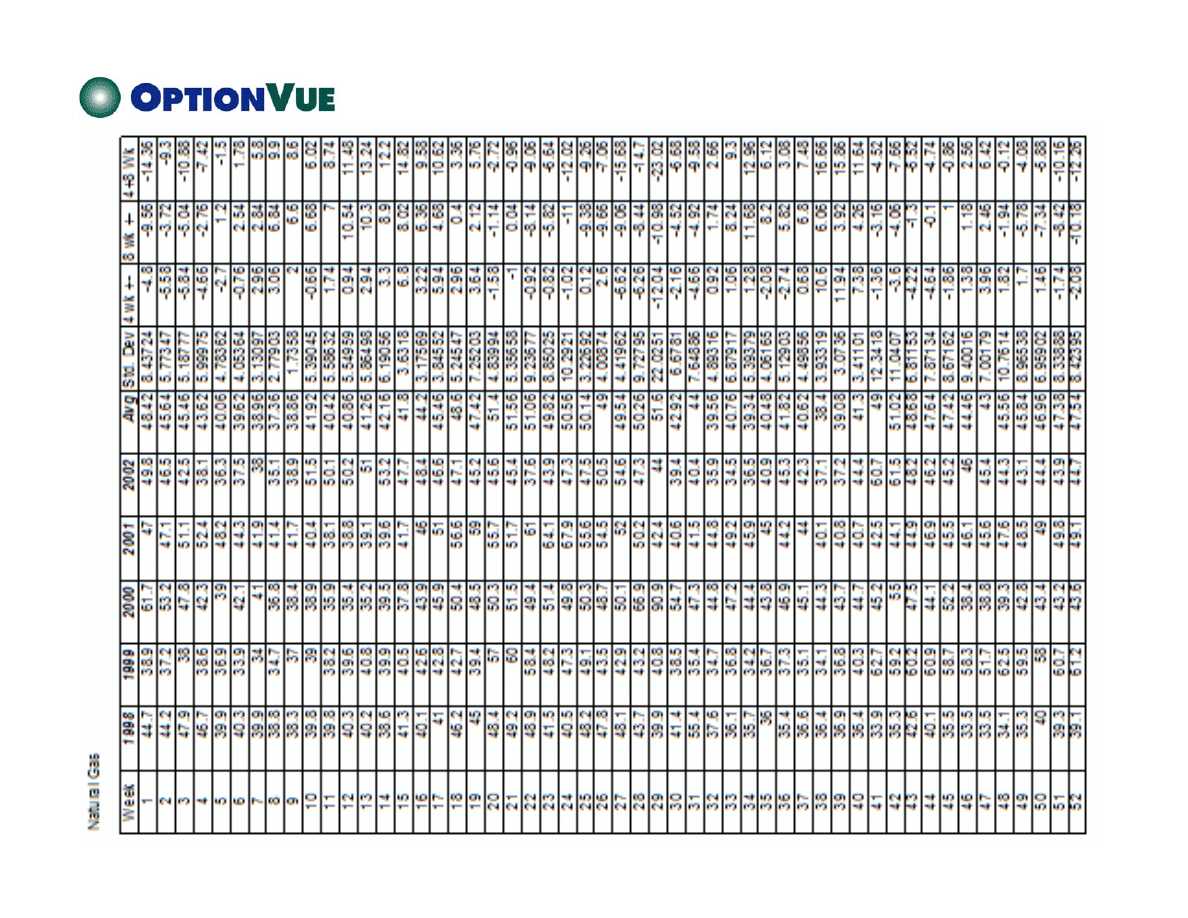

Natural Gas

Introduction to the

Straddle Play

Call Option – Right but not obligation to buy a futures

contract at a certain price on a certain date

Put Option – Right but not obligation to sell a futures

contract at a certain price on a certain date

Last MIV Trade Last MIV Trade Last MIV Trade

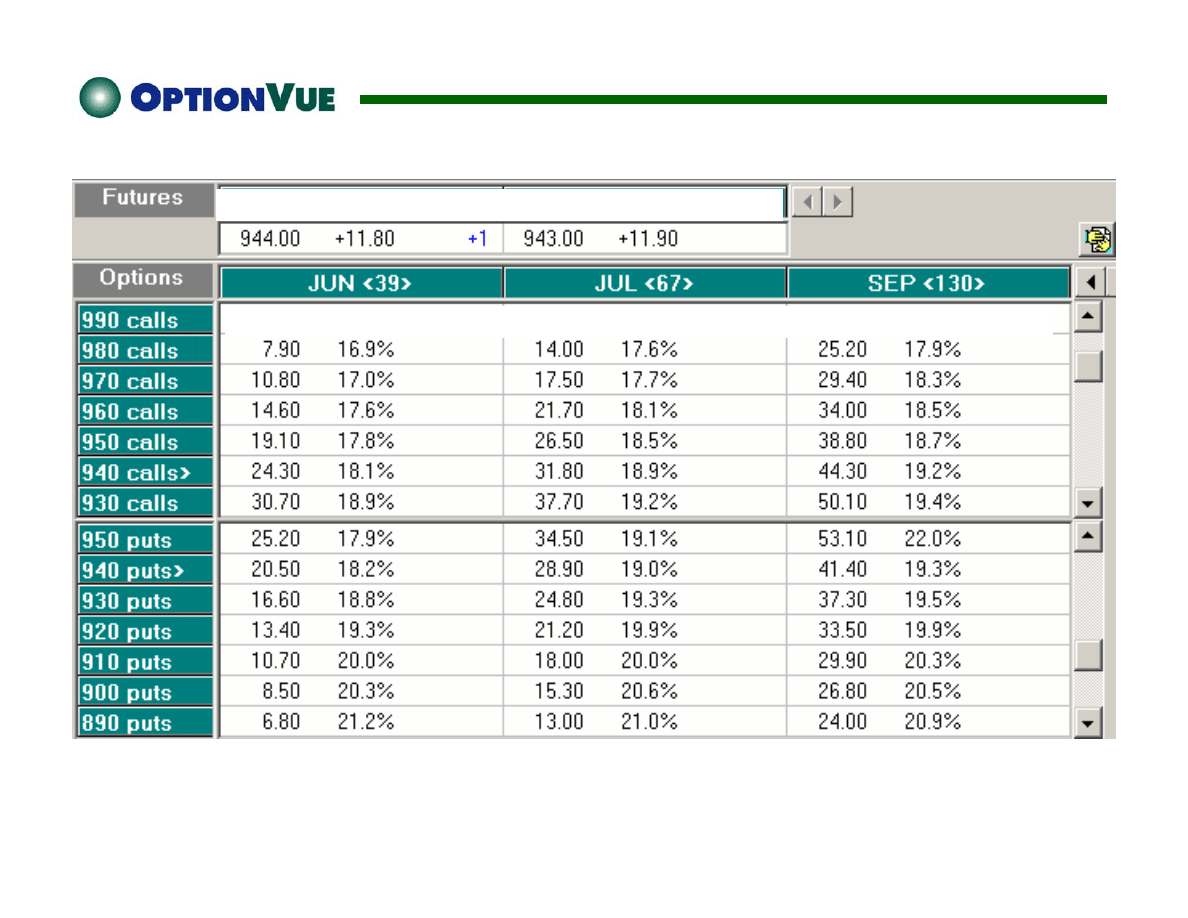

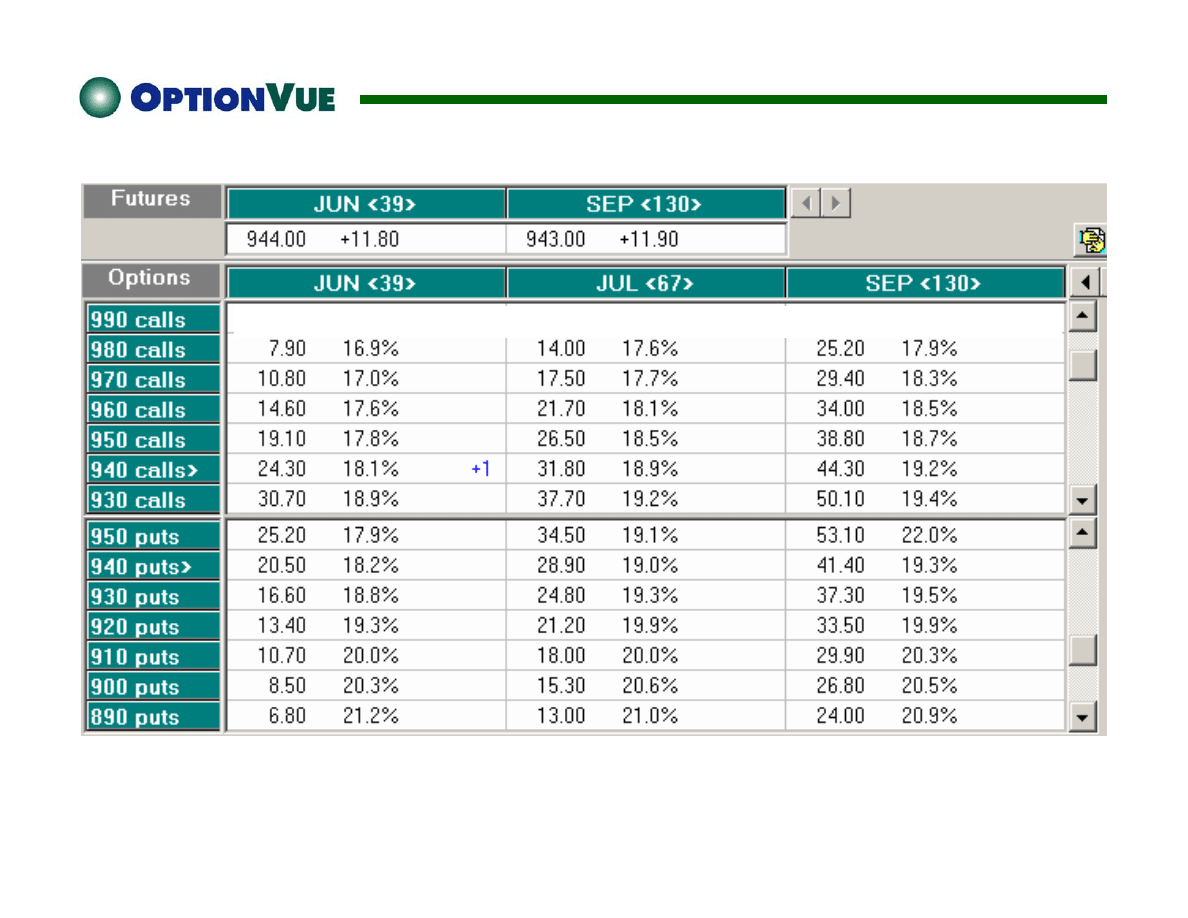

S&P 500 Index Futures

5/12/03

Last Change Trade Last Change

Trade

S&P 500 Index Futures

5/12/03

Long 1 June Futures Contract

Last MIV Trade Last MIV Trade Last MIV Trade

S&P 500 Index Futures

5/12/03

S&P 500 Index Futures

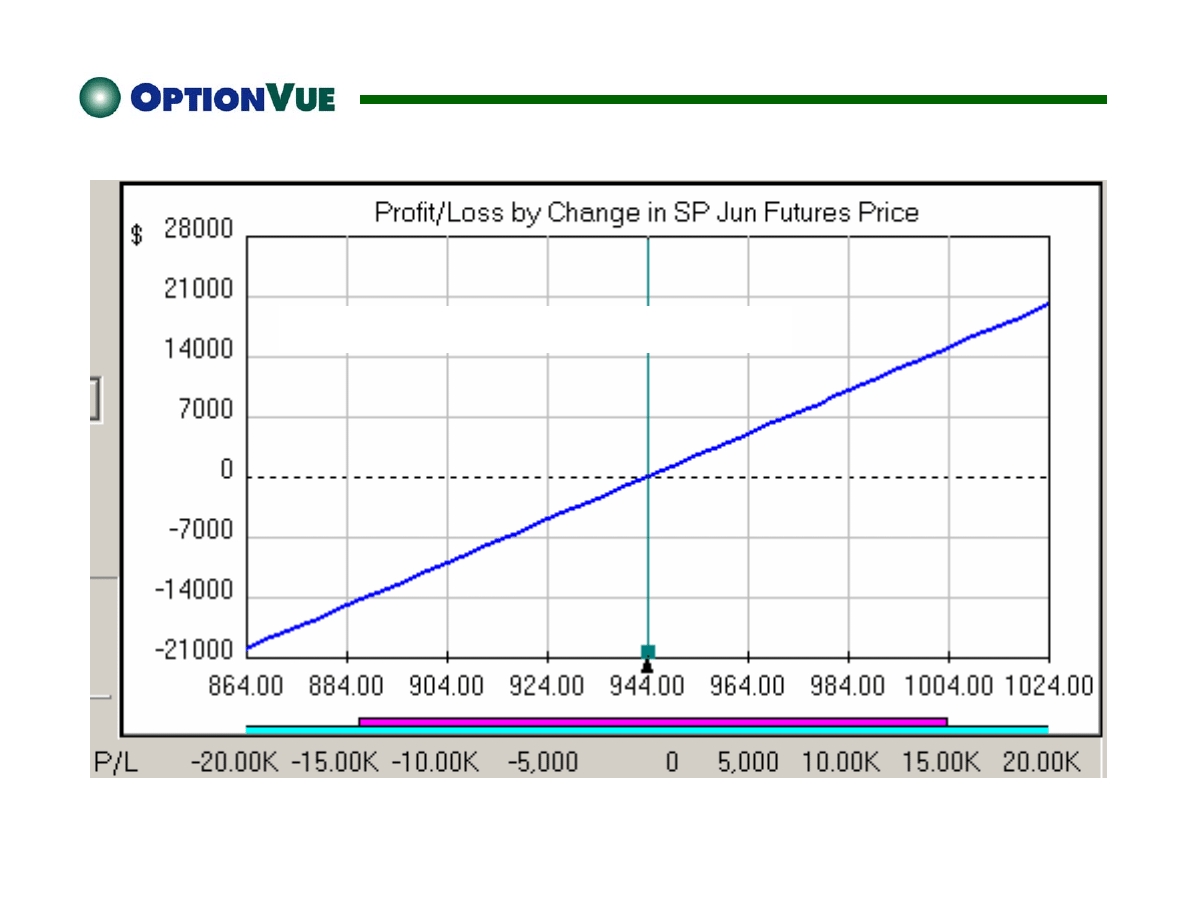

Today’s Risk/Reward Line

S&P 500 Index Futures

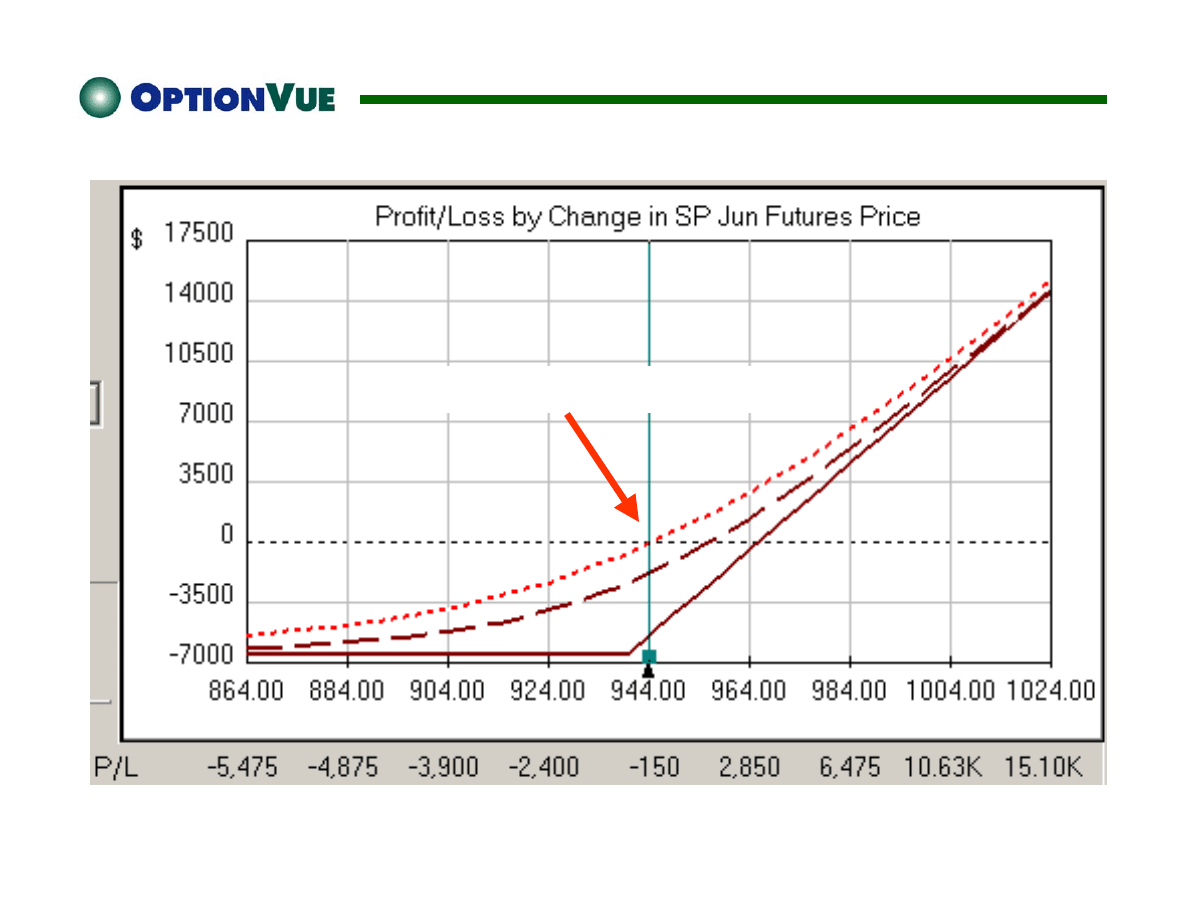

Risk/Reward Line for 20 Days Away

S&P 500 Index Futures

1

st

Standard Deviation of

Possible Price Outcomes

Based on Last Month of Trading

S&P 500 Index Futures

Risk/Reward Line for Expiration in 39 Days

S&P 500 Index Futures

Buy 1 June 940 Put Option

S&P 500 Index Futures

Straddle

Buy 1 June 940 Call Option

Buy 1 June 940 Put Option

The Role of Volatility

IMPLIED VOLATILITY (IV)

Measures the volatility of the underlying asset

implied by current option prices

Higher IV Means More Time Premium to Buy or Sell

The Role of Volatility

STATISTICAL VOLATILITY (SV)

Measures how much the price of the asset itself has

bounced around recently

Higher SV Means a Wider Standard Deviation of

Possible Price Outcomes

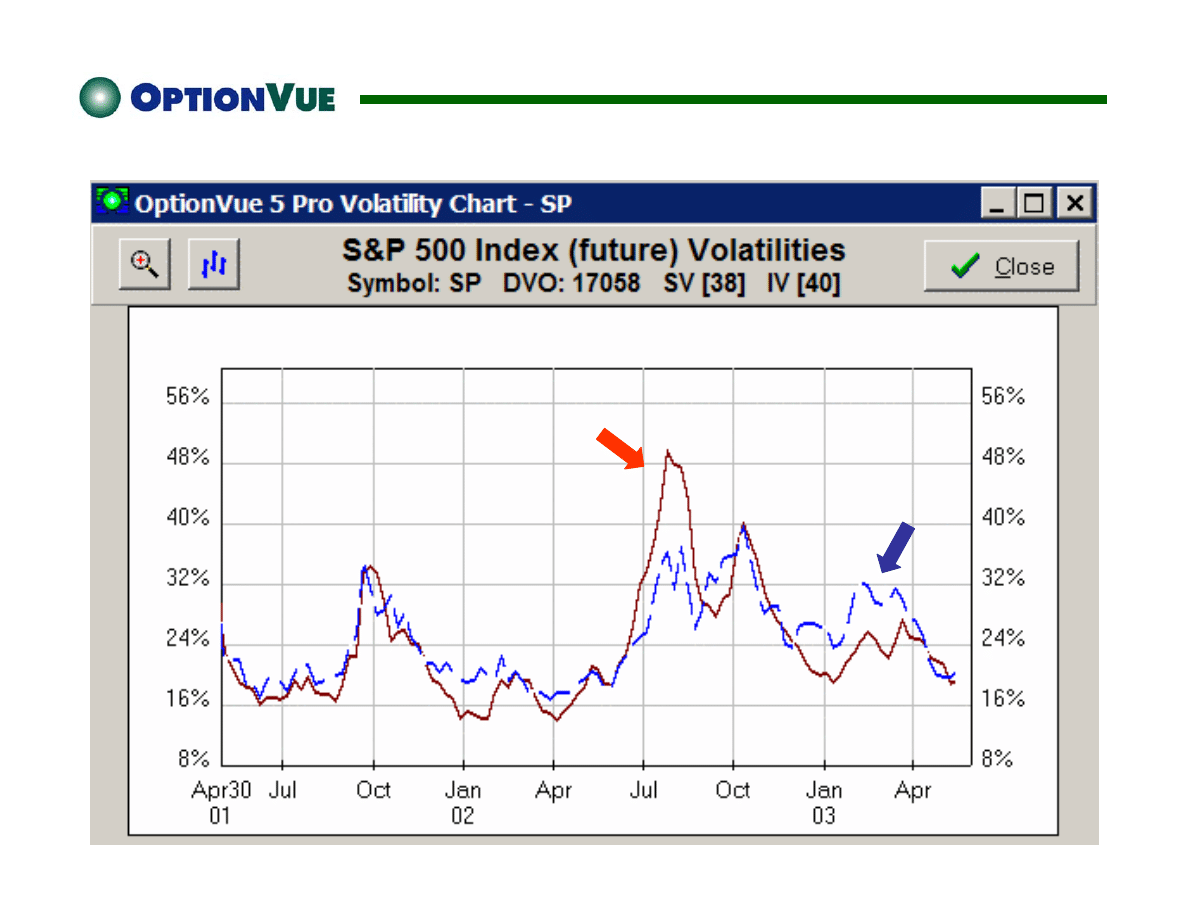

S&P 500 Index Futures

SV

IV

S&P 500 Index Futures

June Straddle

20 Days Out

S&P 500 Index Futures

June Straddle

20 Days Out

IV Increases by 7 %

The Role of Volatility

Vega

Option’s Sensitivity to IV Movement

Daily $ Amount Gained/Lost with a 1% IV Move

Theta

Option’s Sensitivity to Time

Daily $ Amount Gained/Lost with 1 Day of Time Decay

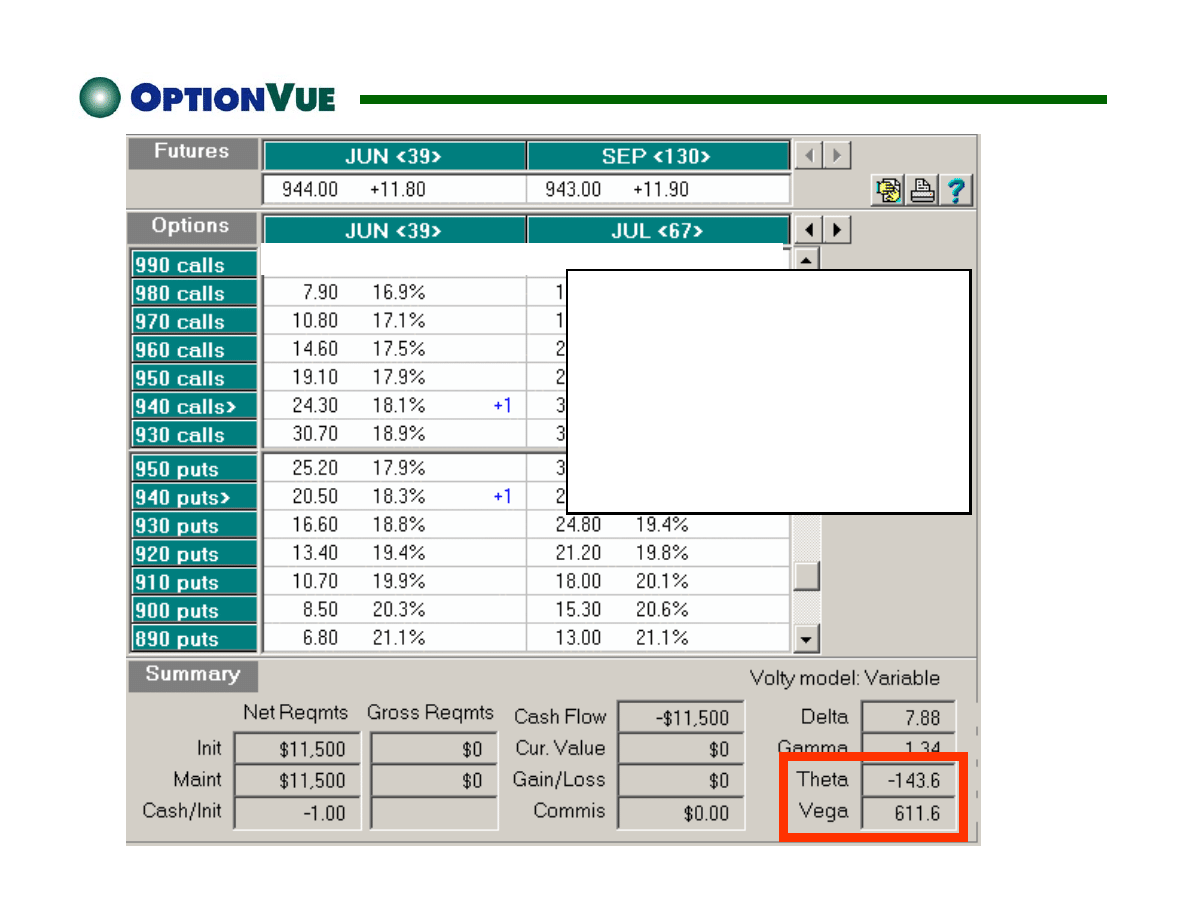

Last MIV Trade Last MIV

Trade

5/12/03

[Vega / Theta]

=

[611.6 / -143.6] =

4.26

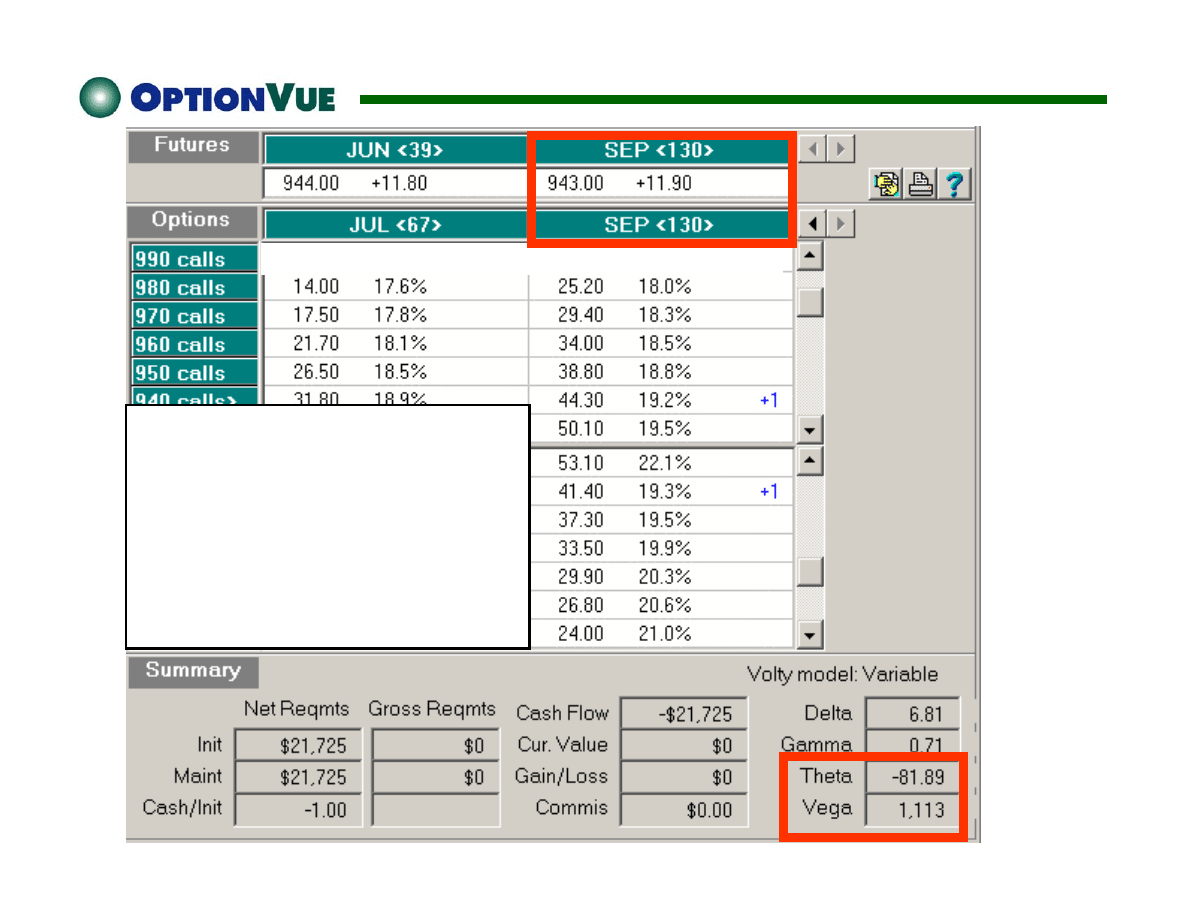

Last MIV Trade Last MIV

Trade

5/12/03

[Vega / Theta]

=

[1113 / -81.89] =

13.59

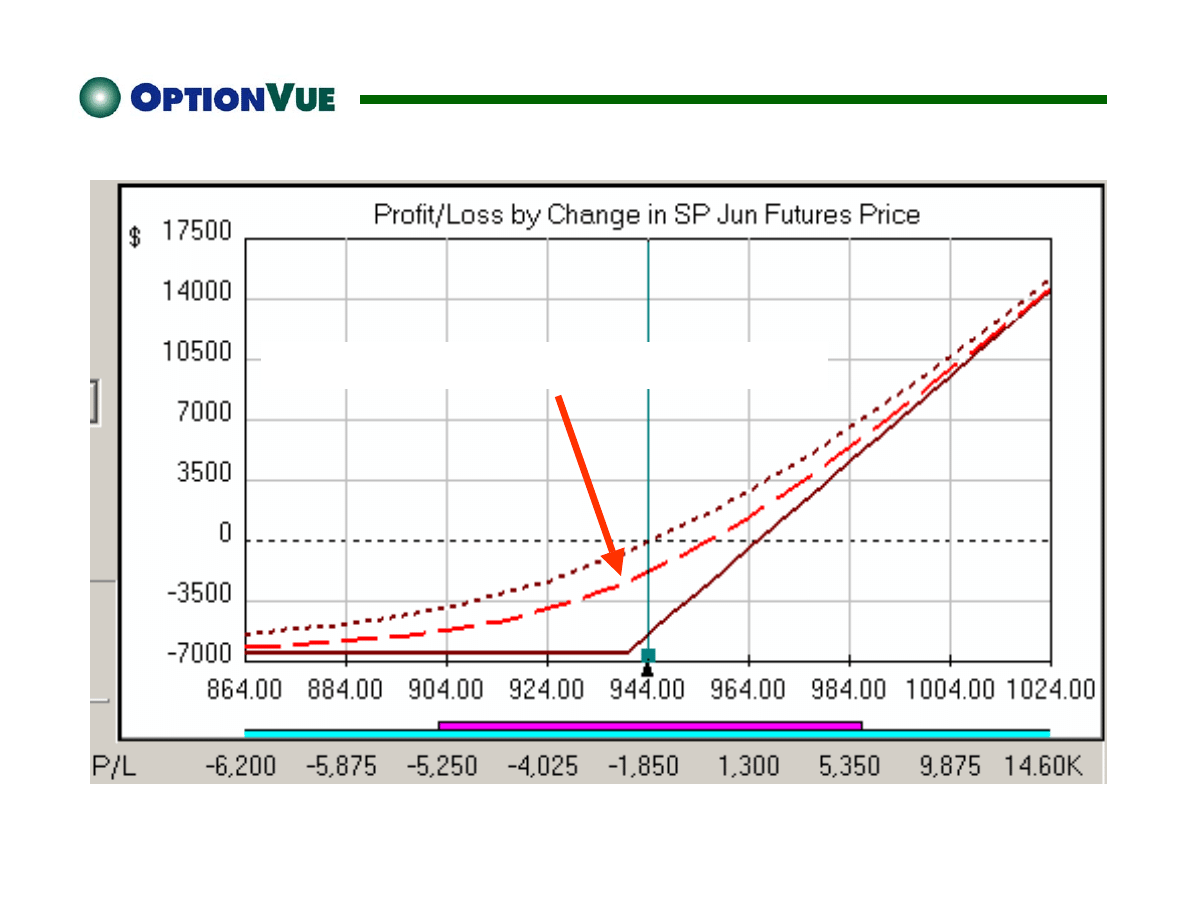

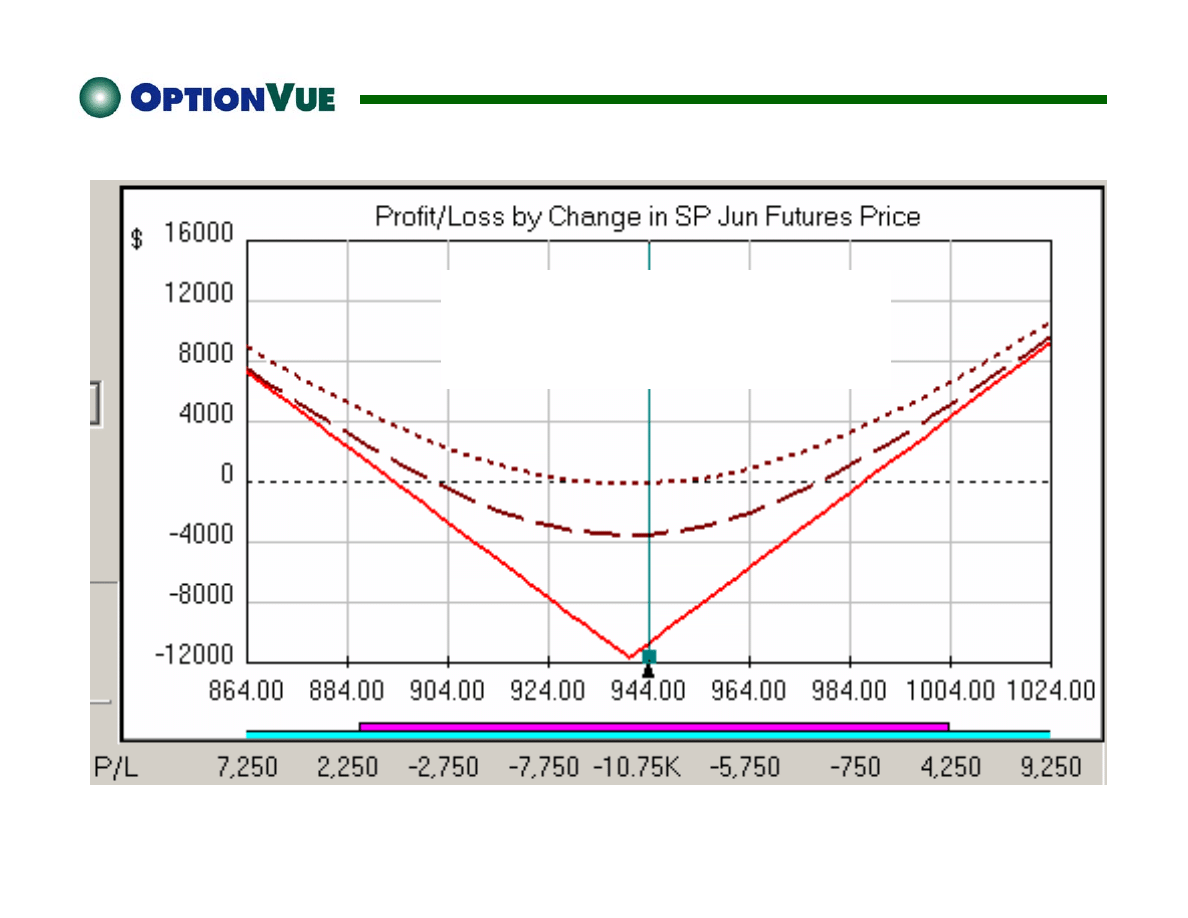

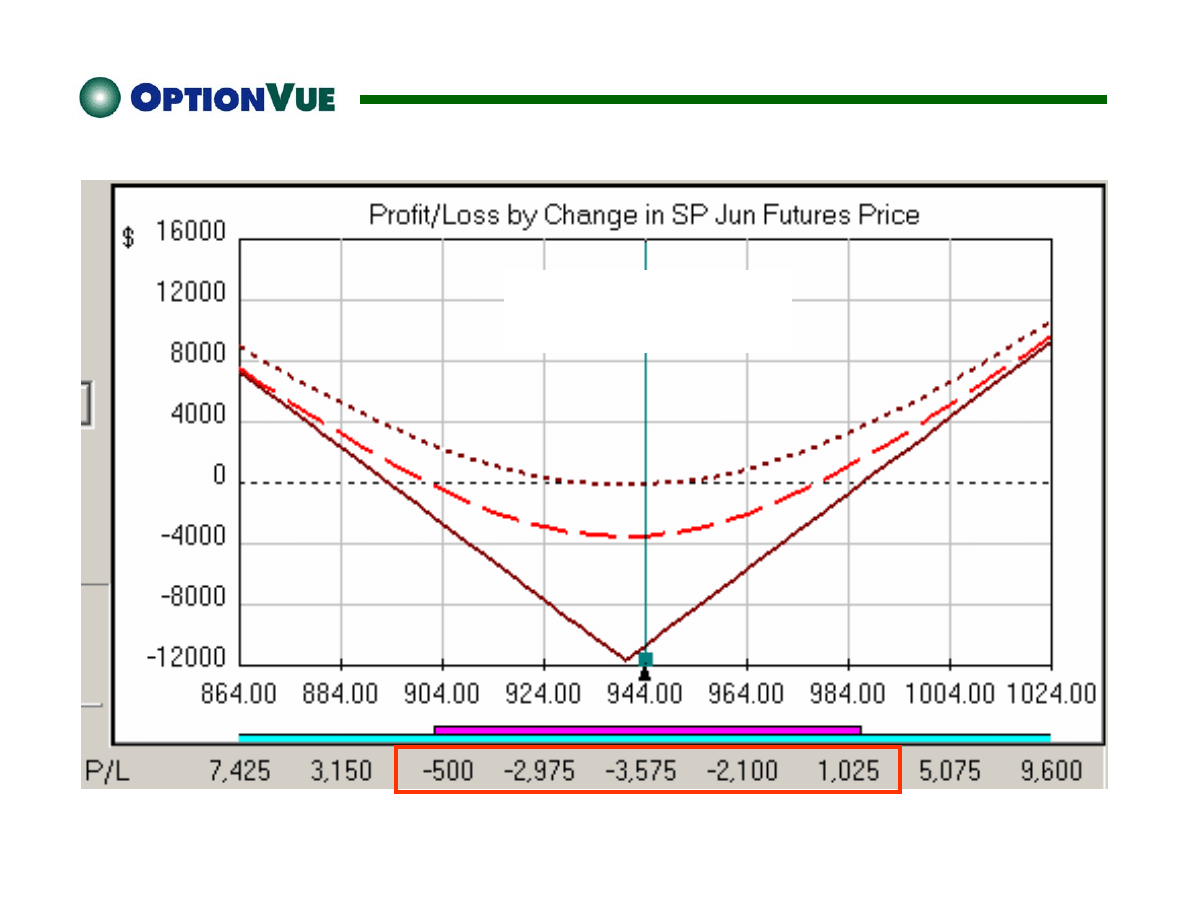

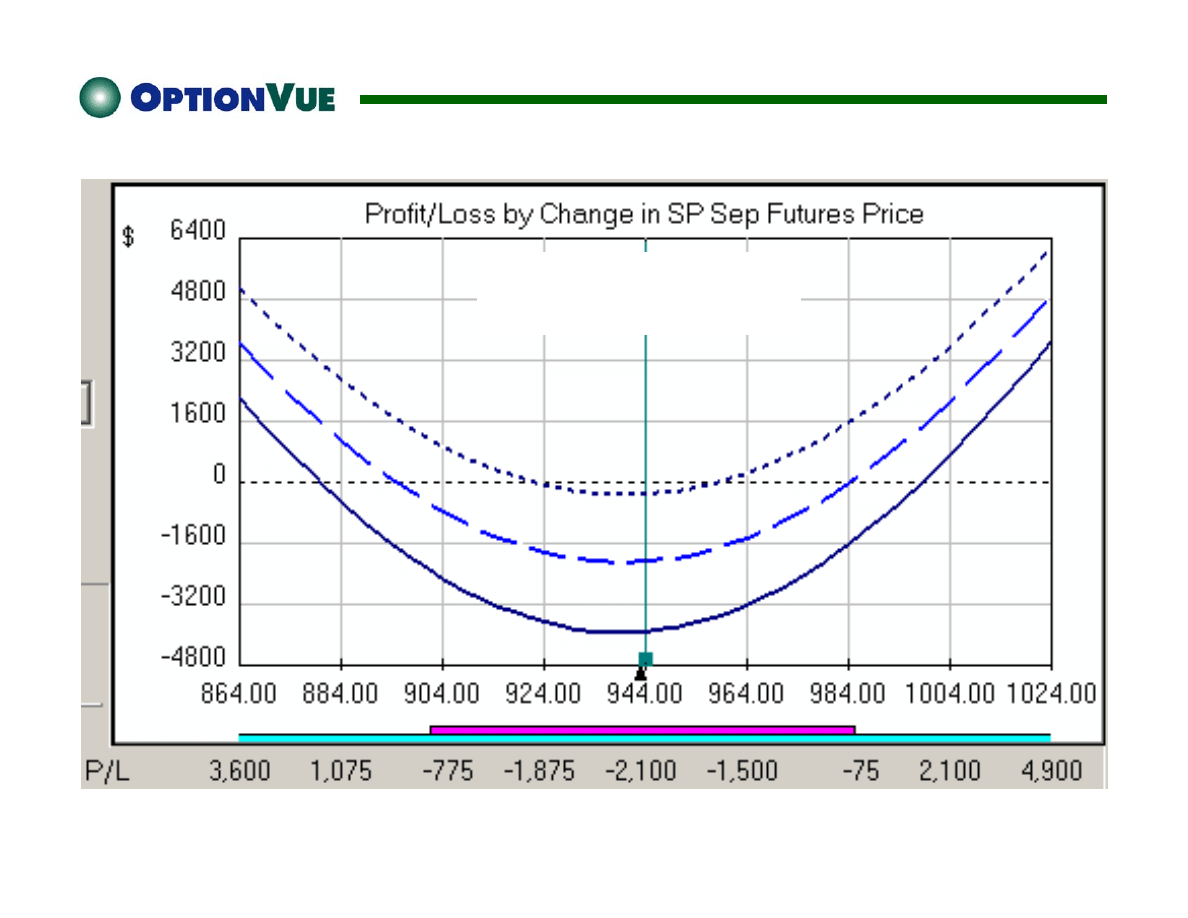

S&P 500 Index Futures

5/12/03

June Straddle

20 Days Out

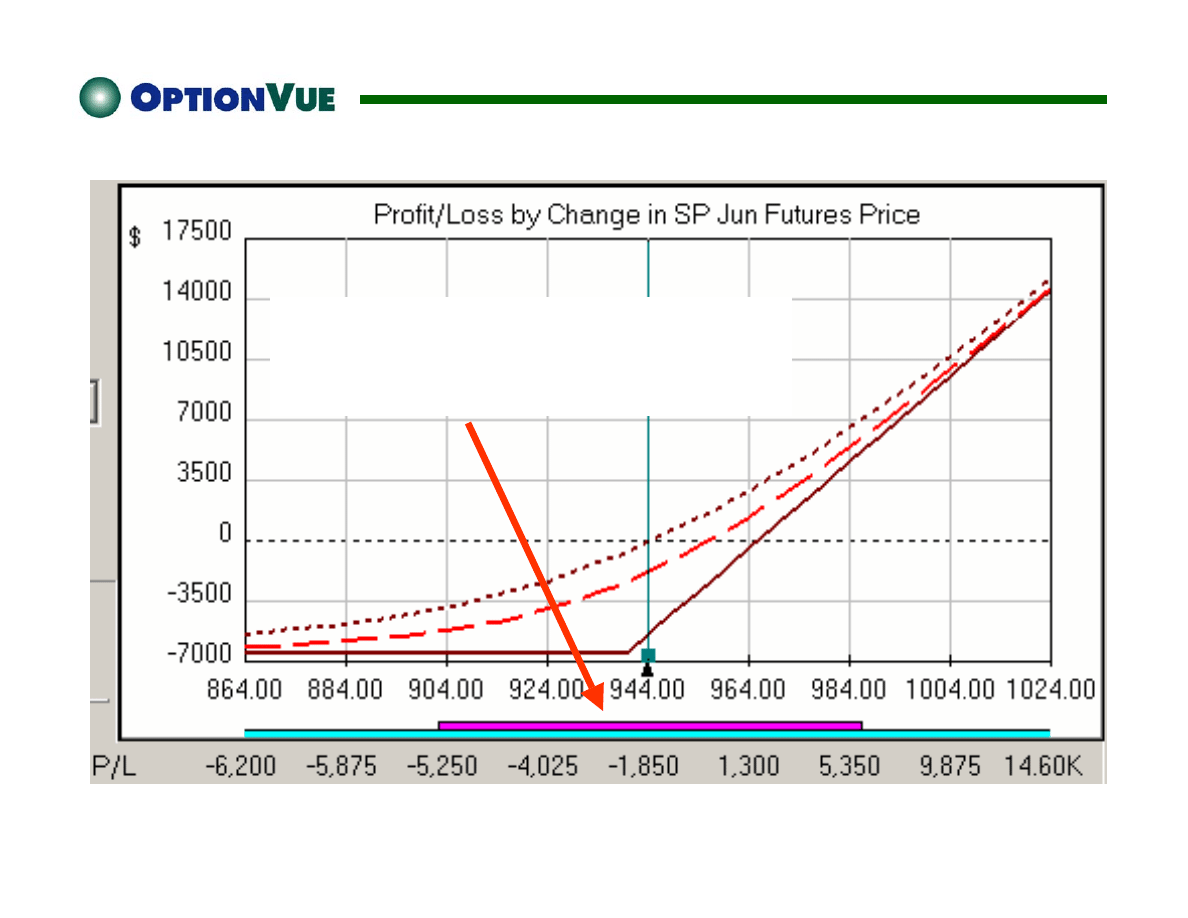

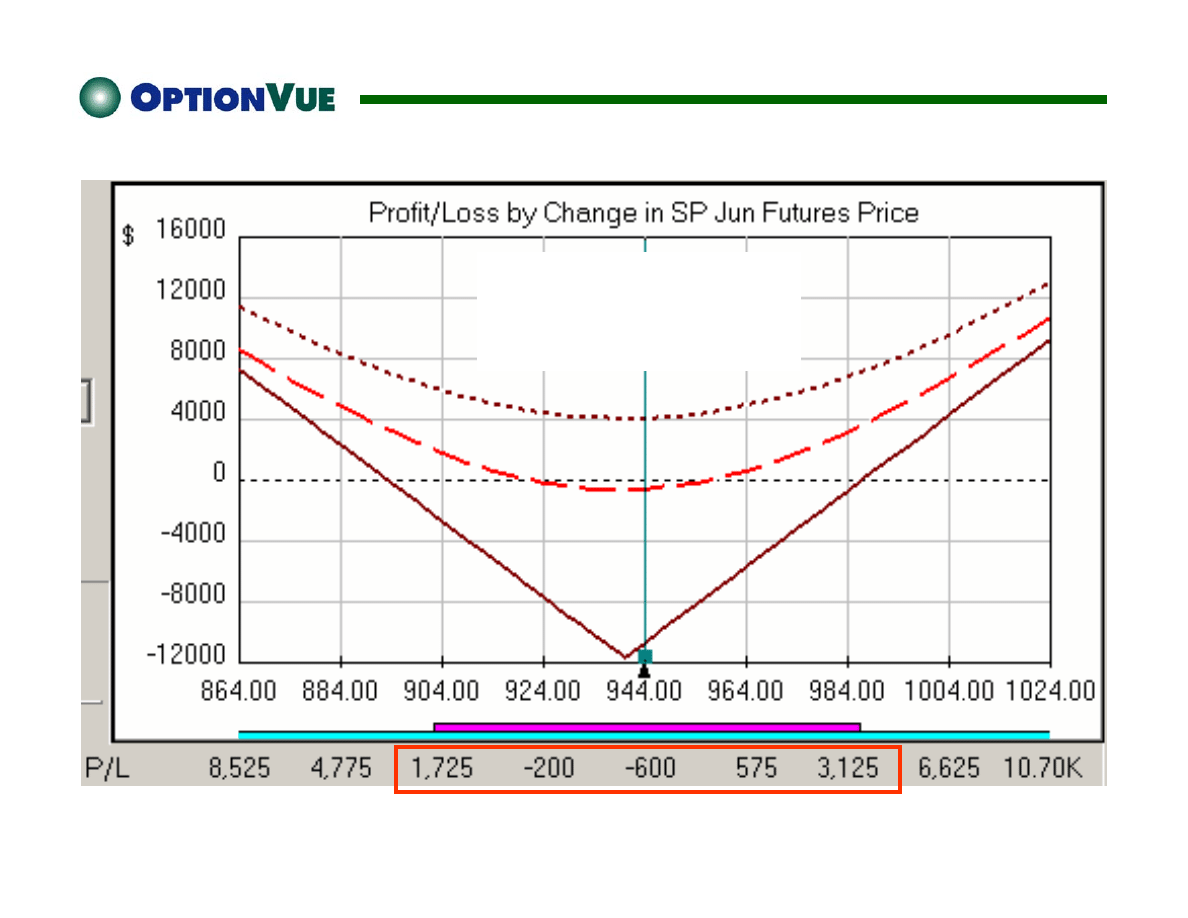

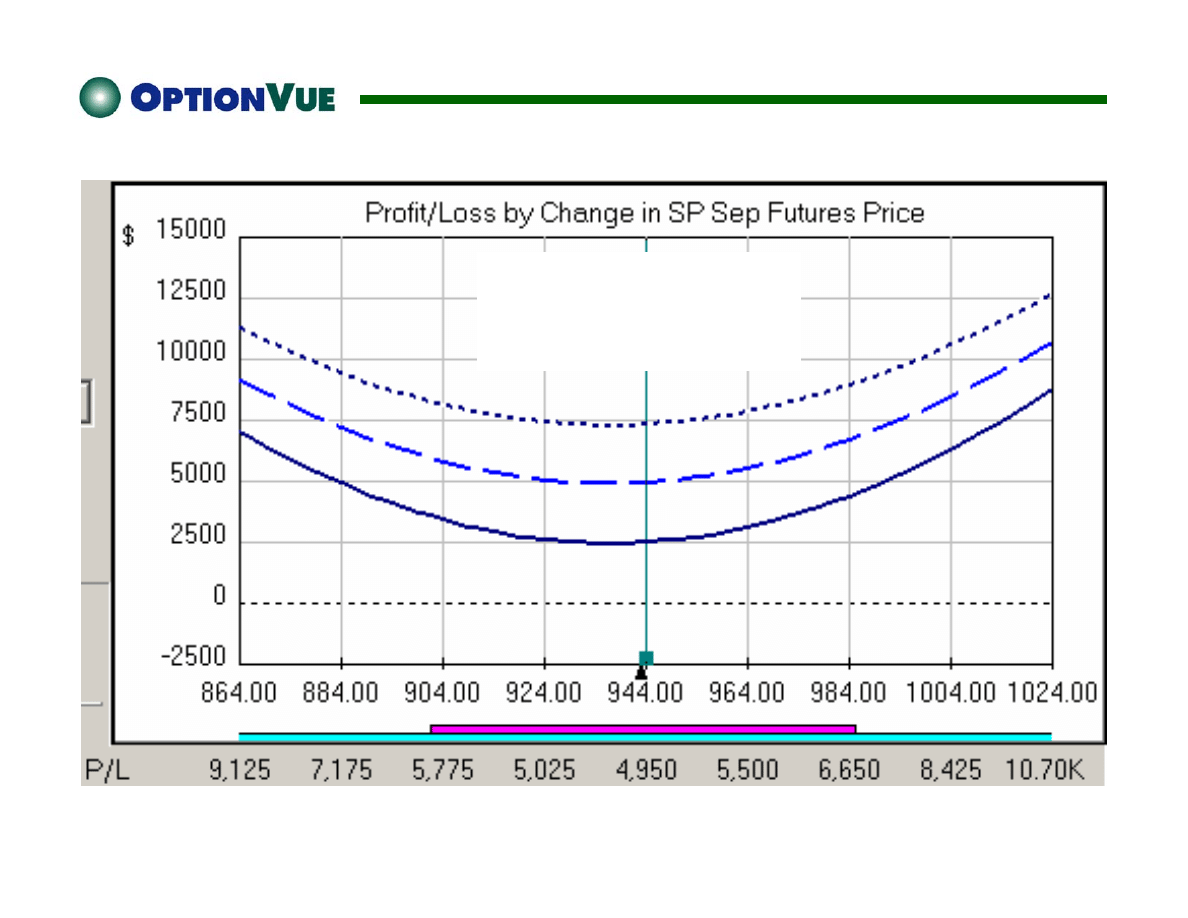

S&P 500 Index Futures

5/12/03

June Straddle

20 Days Out

IV Increases by 7%

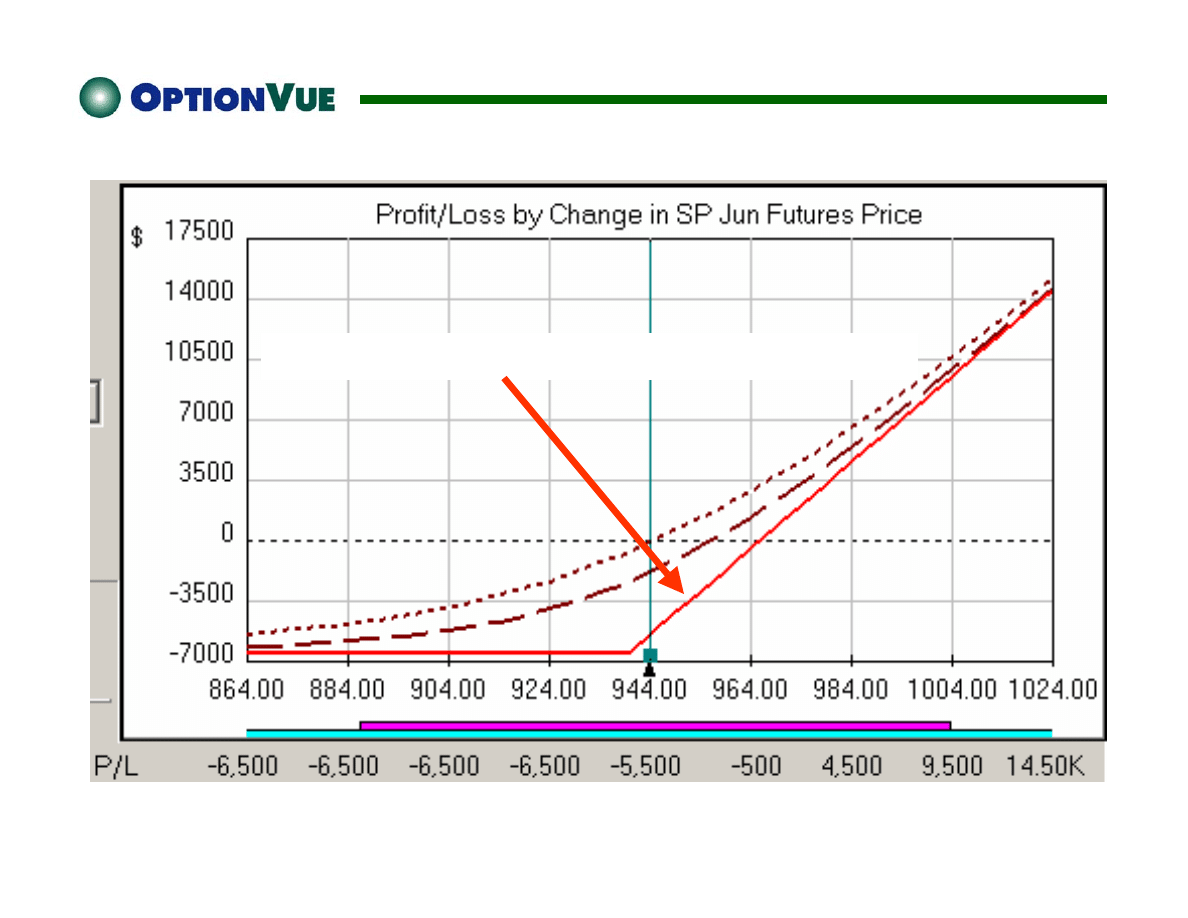

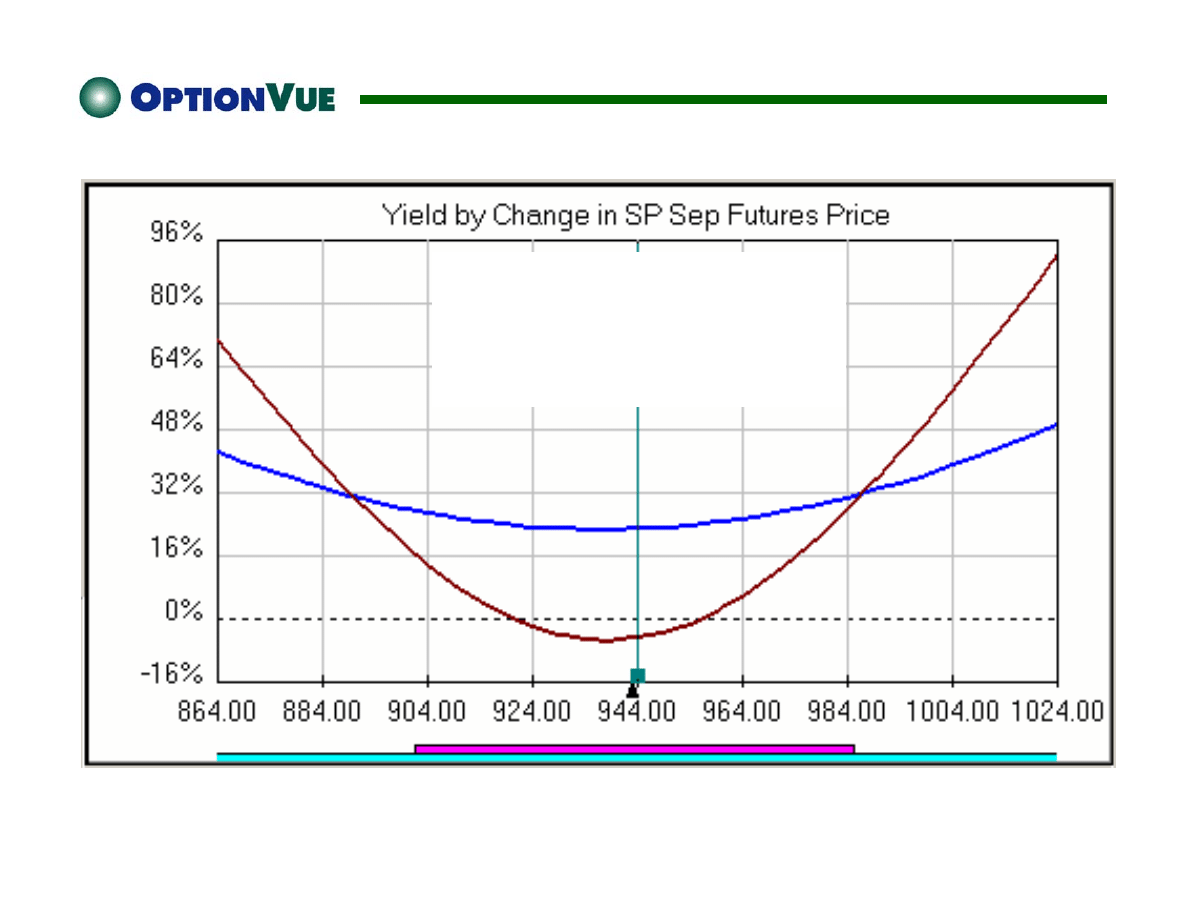

S&P 500 Index Futures

5/12/03

Yield Comparison of

June versus Sept Straddle

20 Days Out

IV Increases by 7%

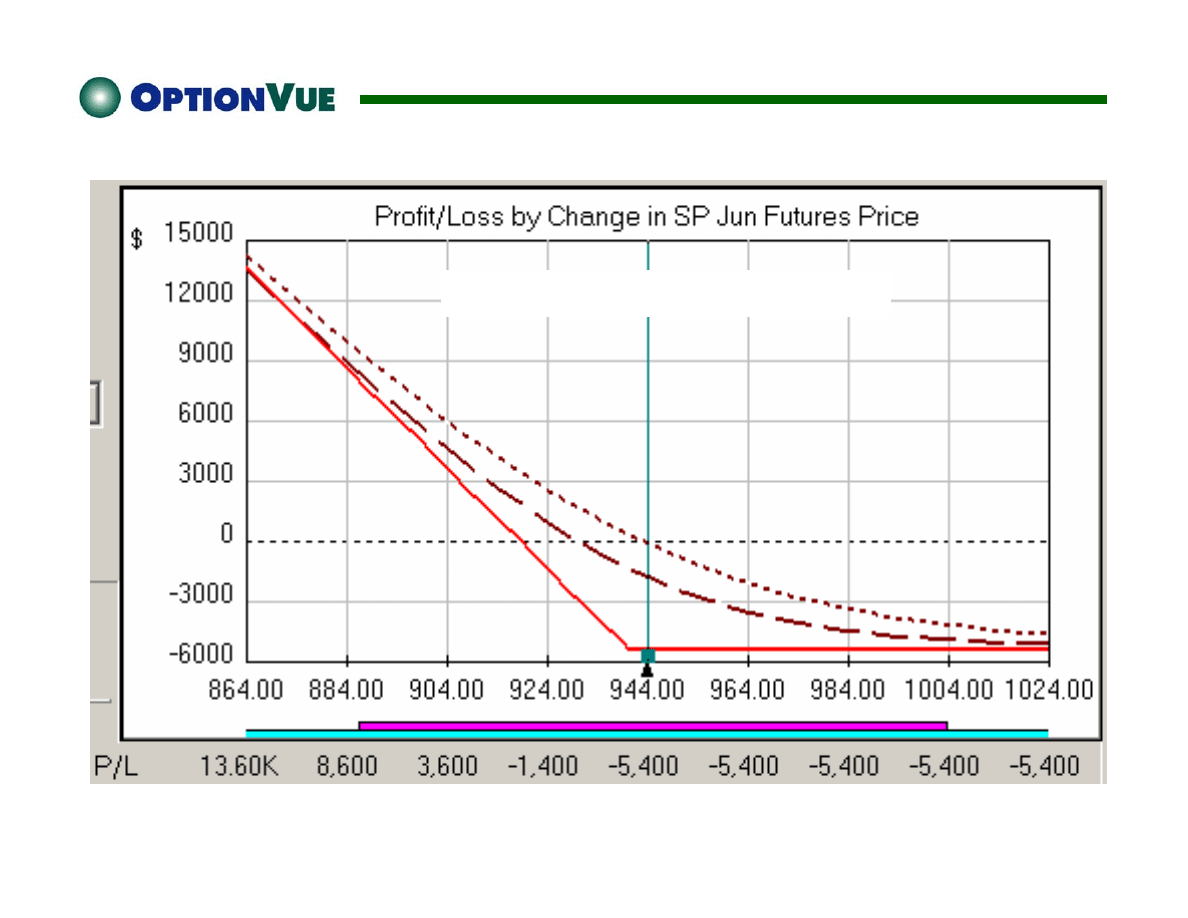

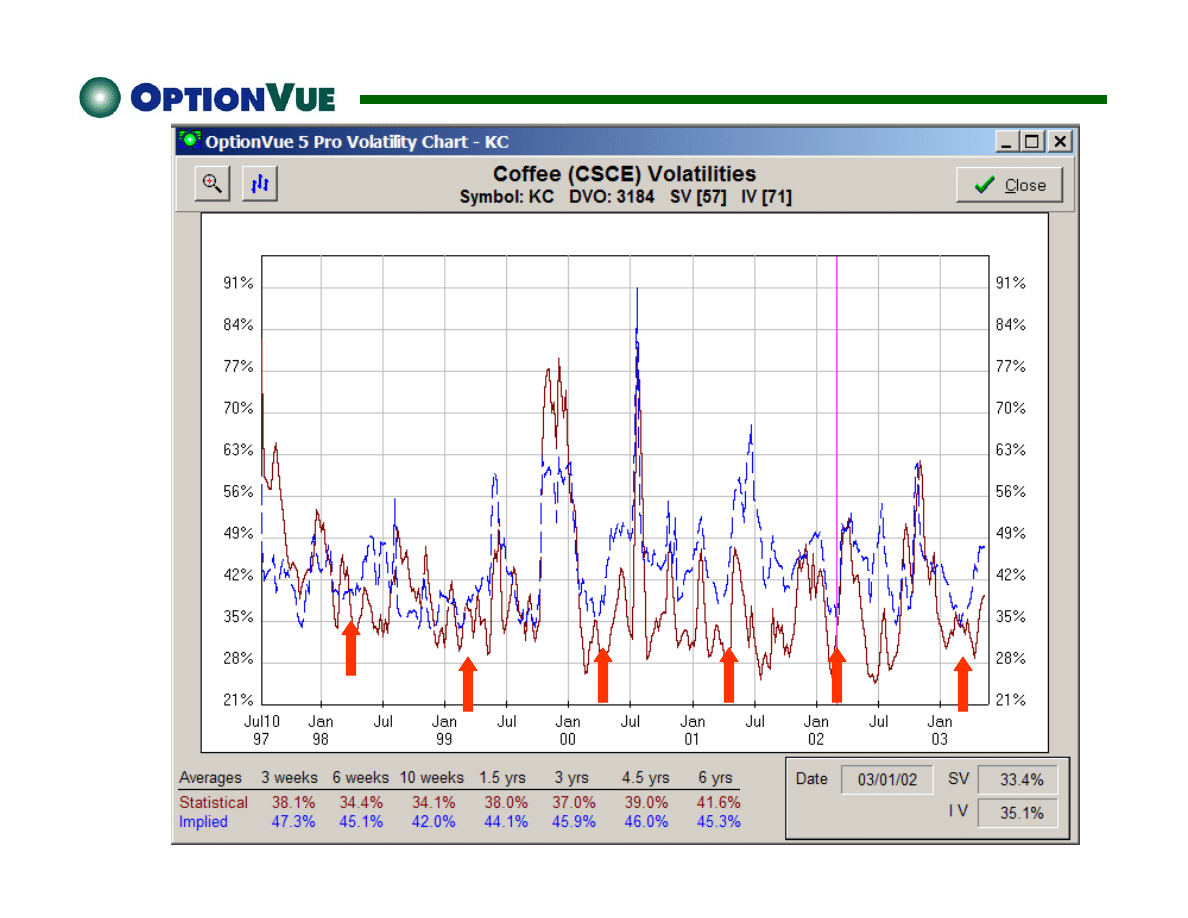

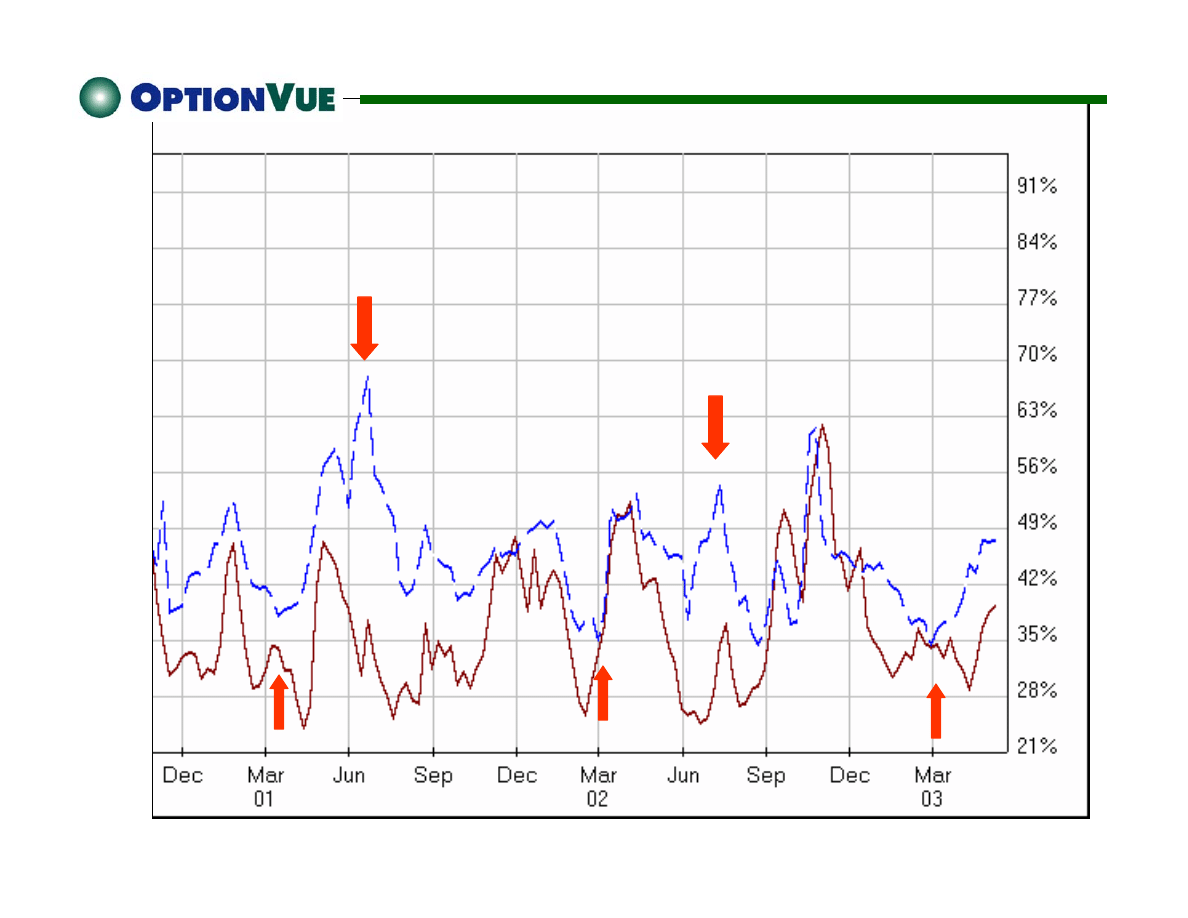

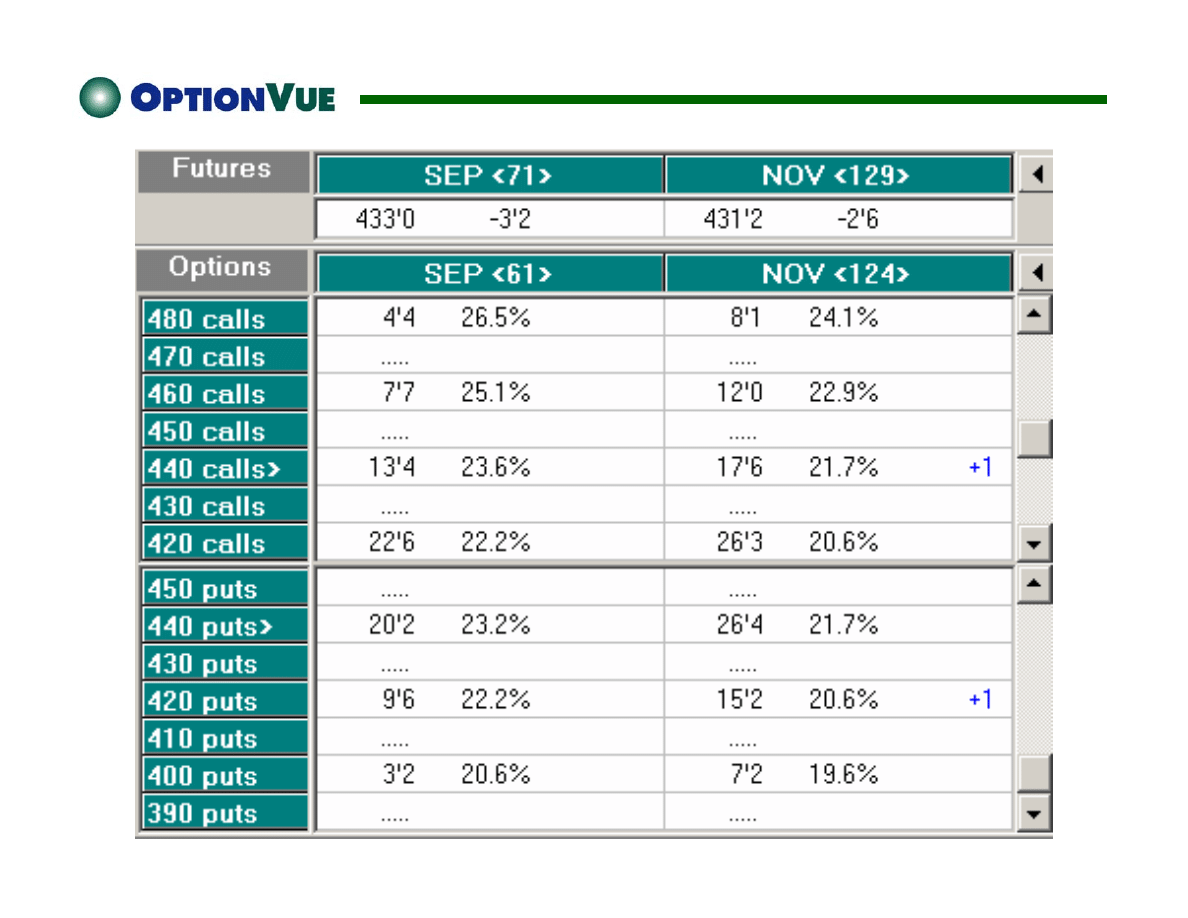

Coffee

Coffee

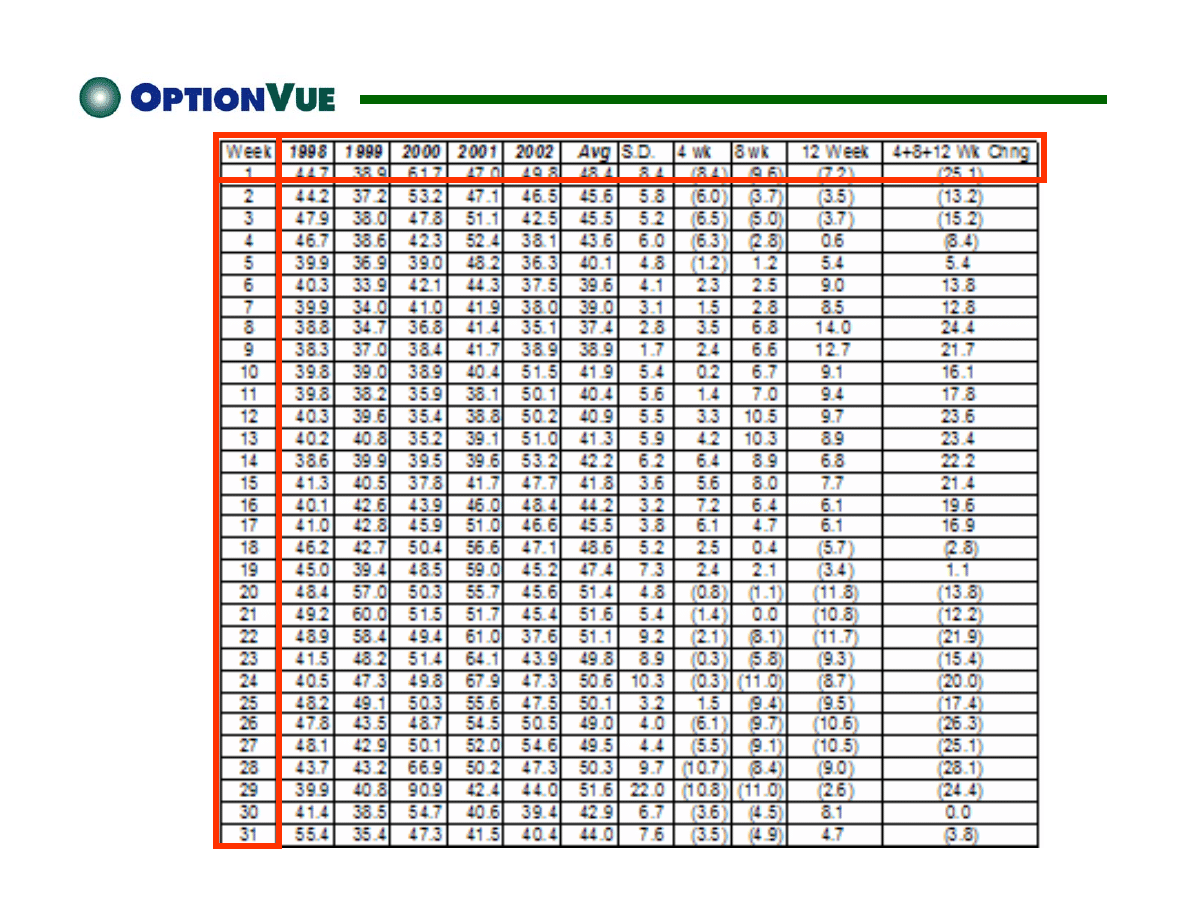

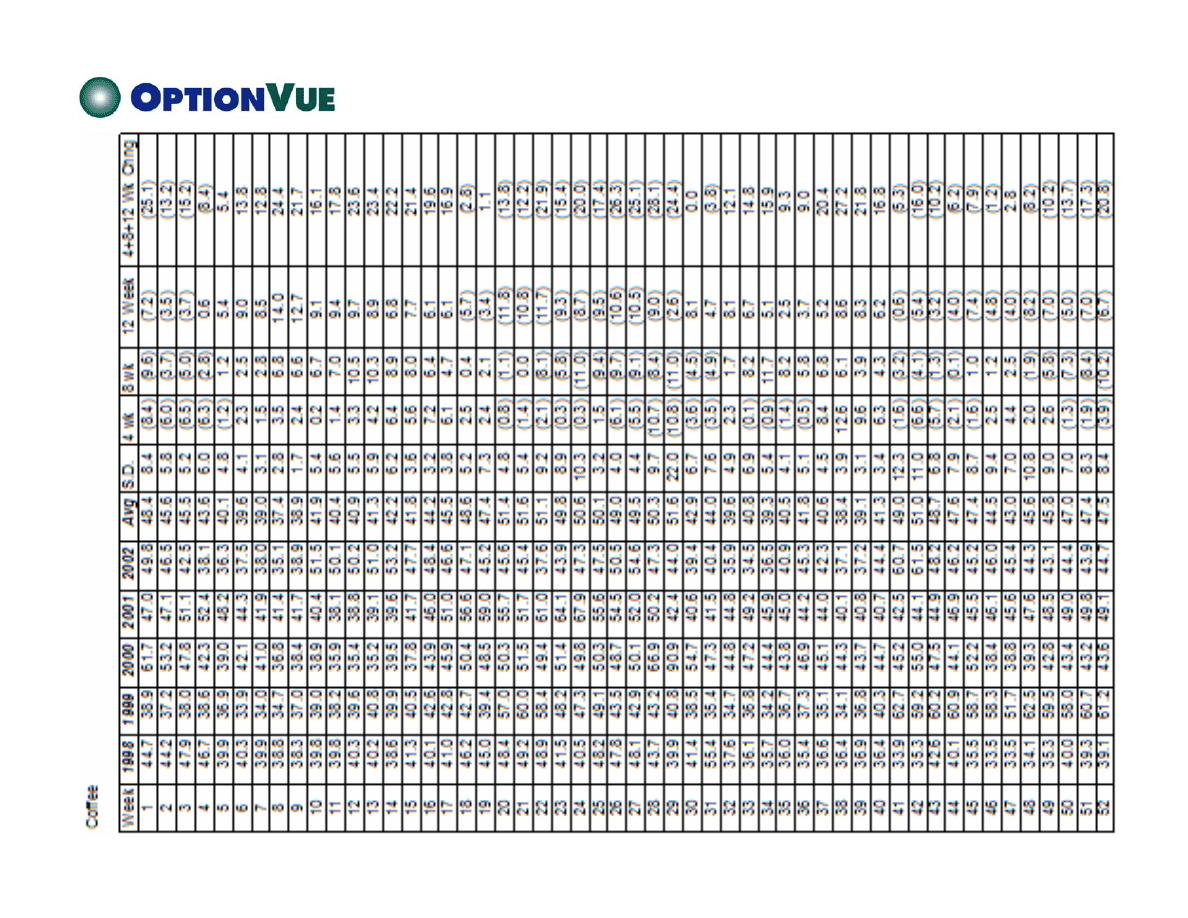

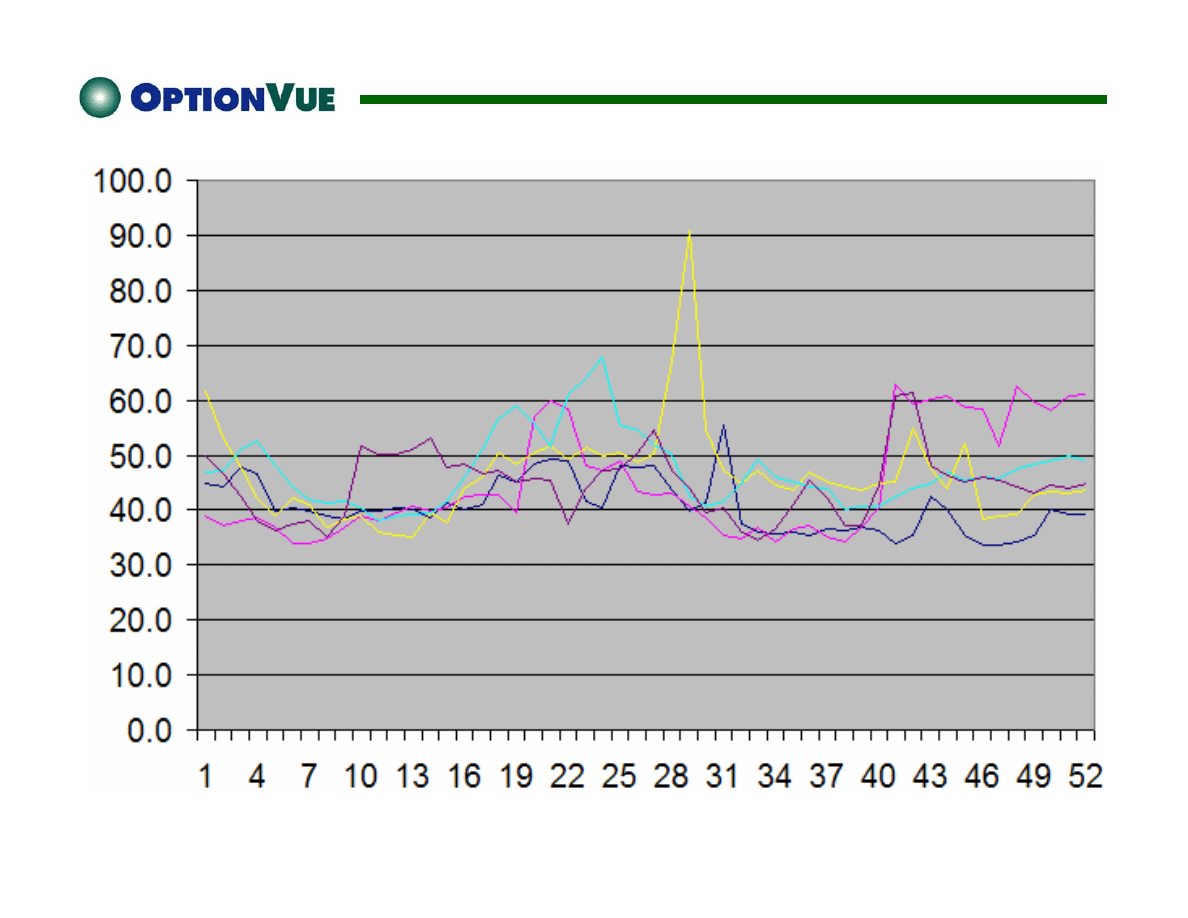

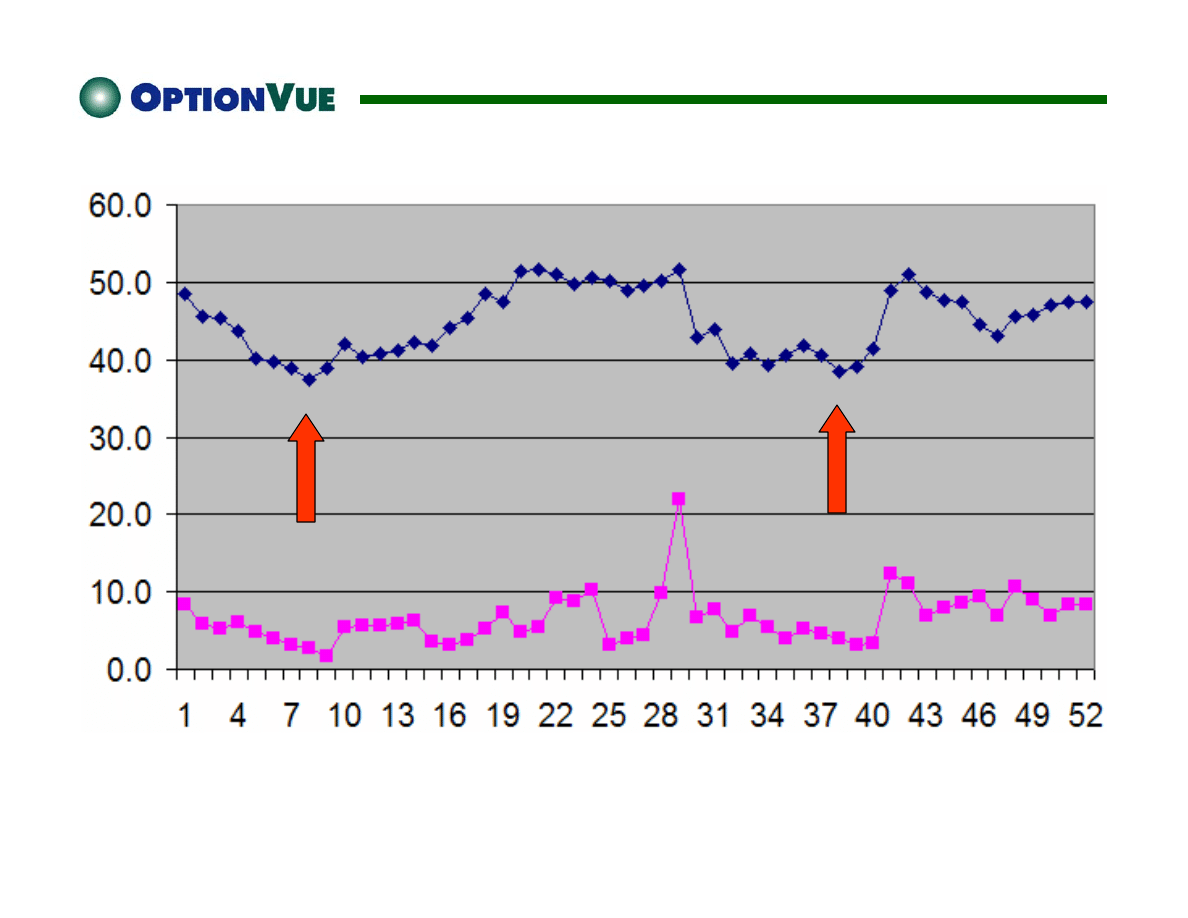

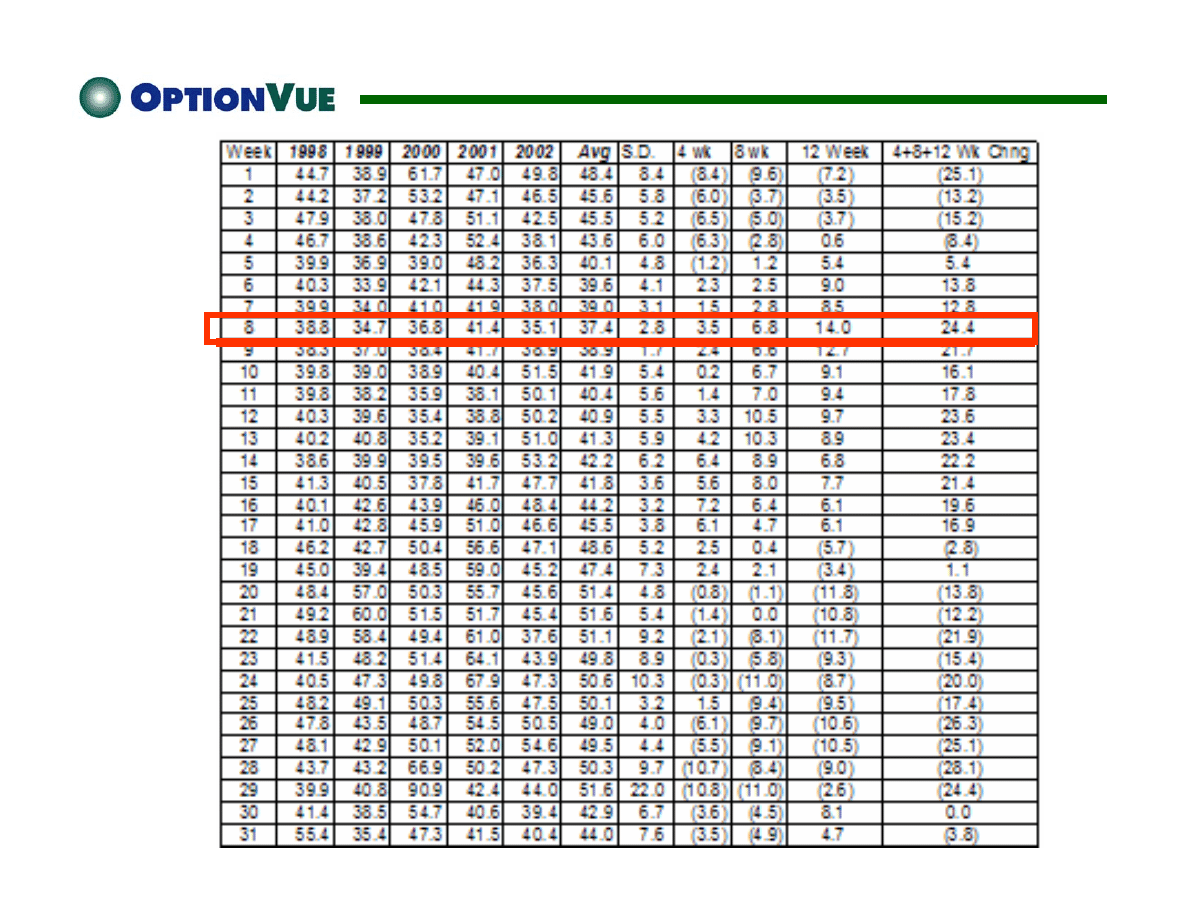

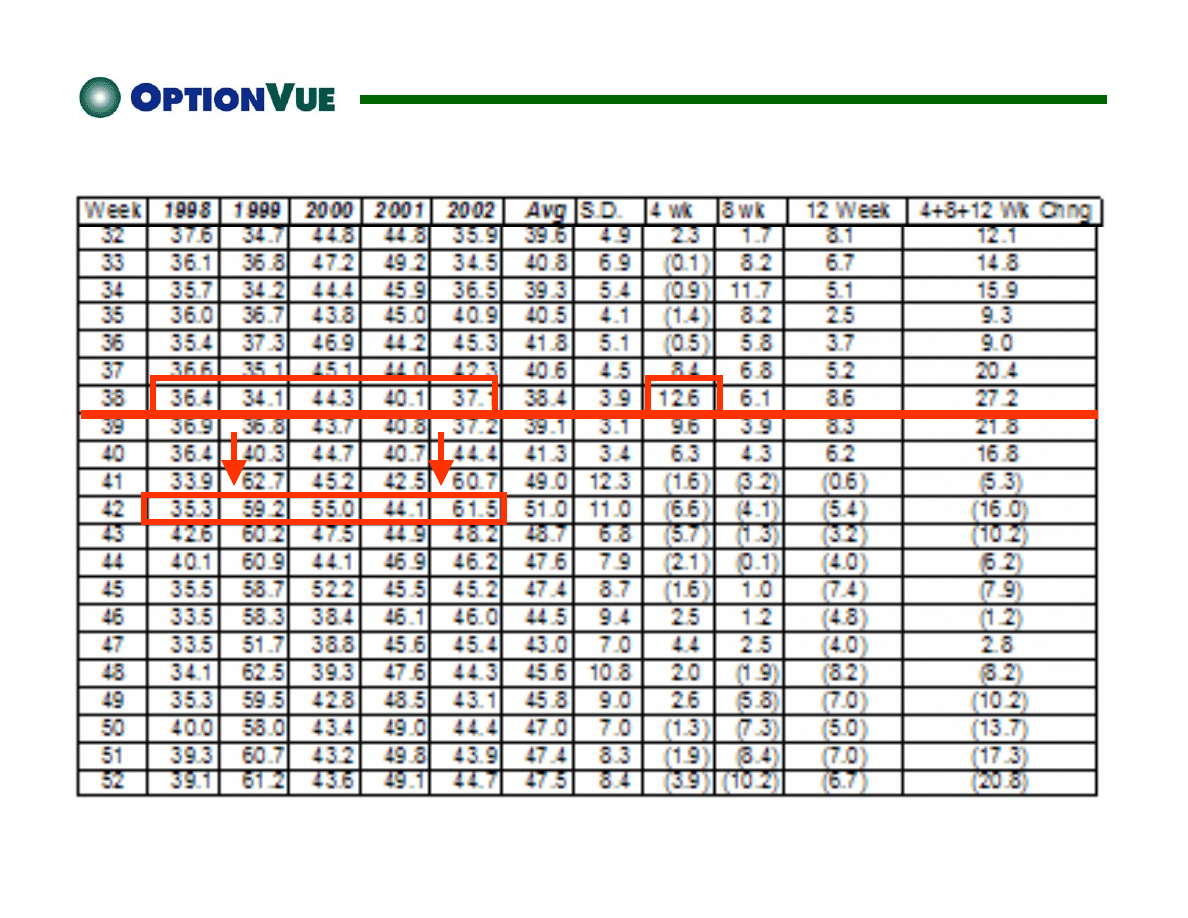

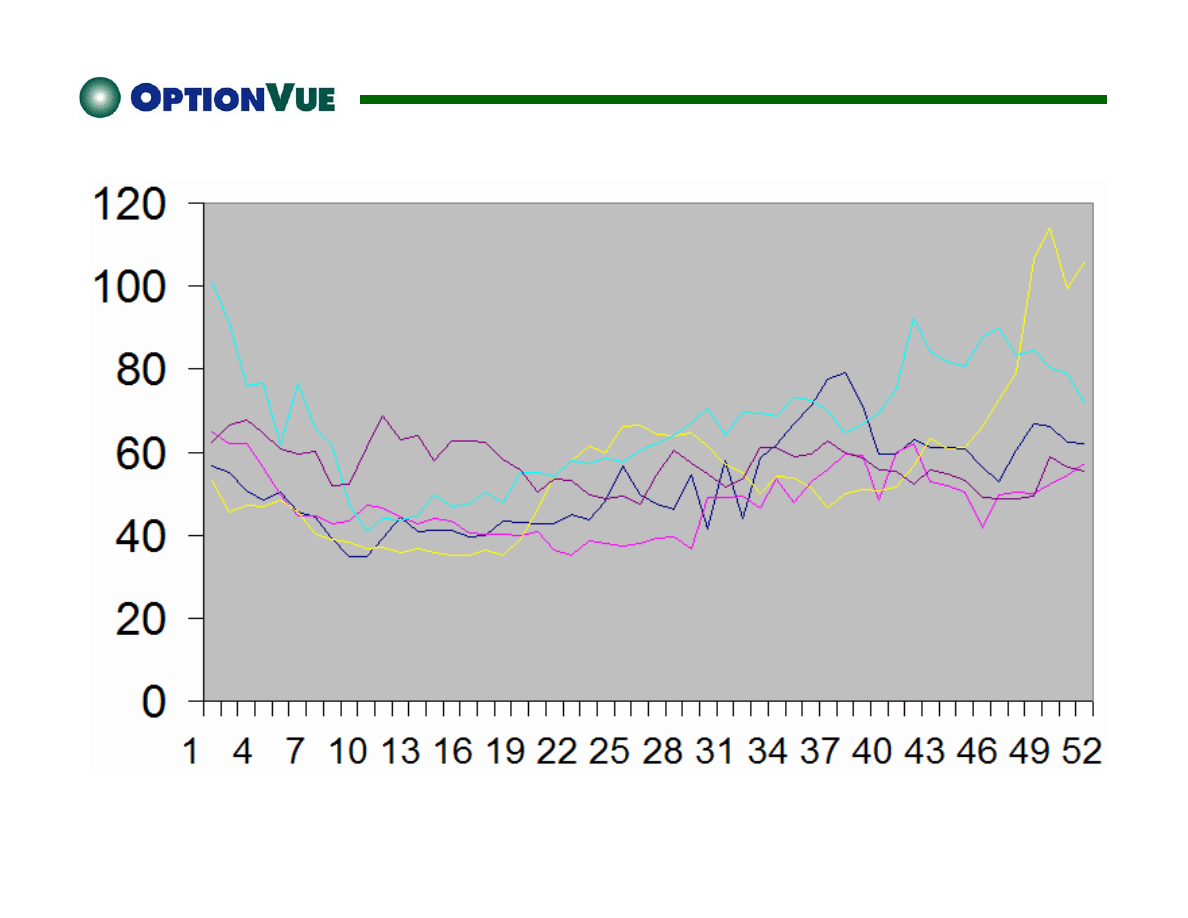

Coffee IVs by Year

Coffee Average IVs

Coffee

Coffee

9/30/02

Last MIV Trade Last MIV Trade

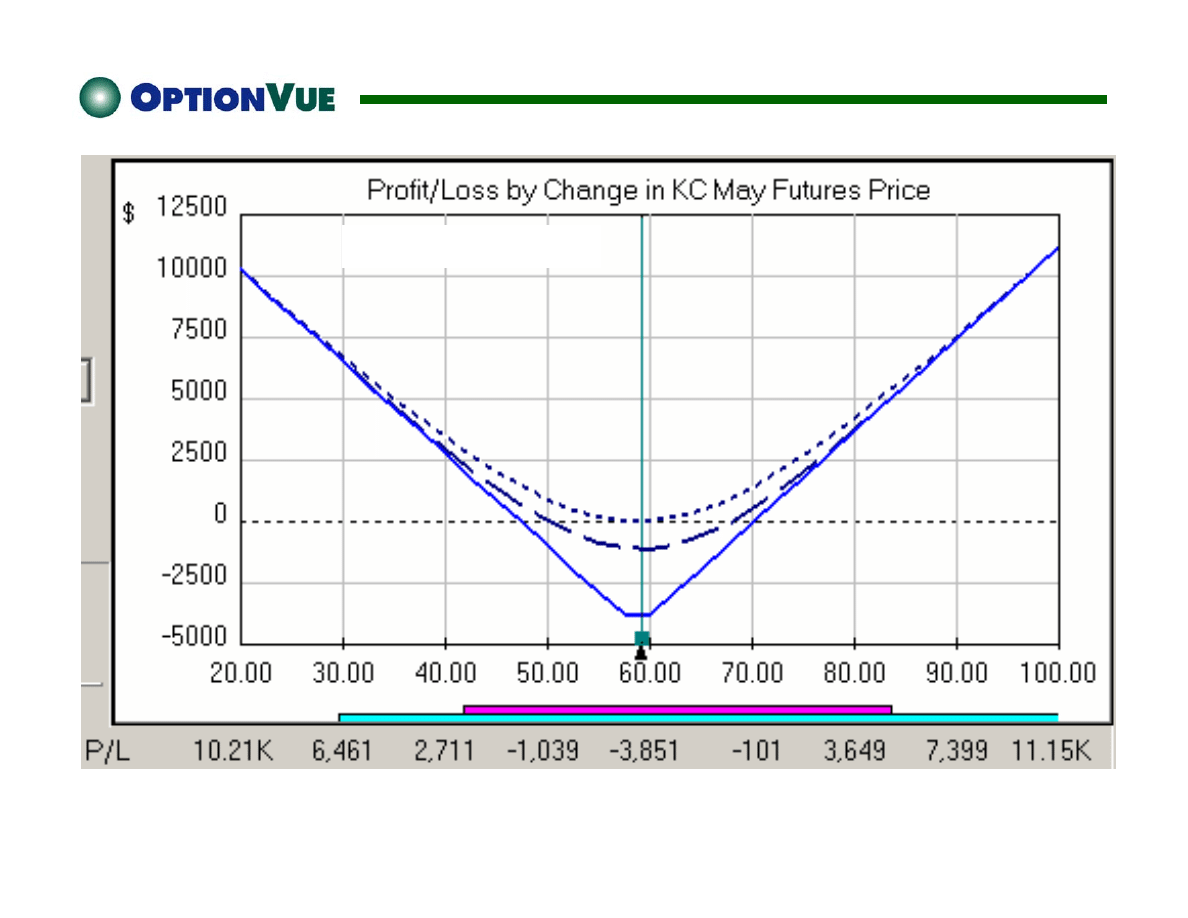

$3851 Requirement

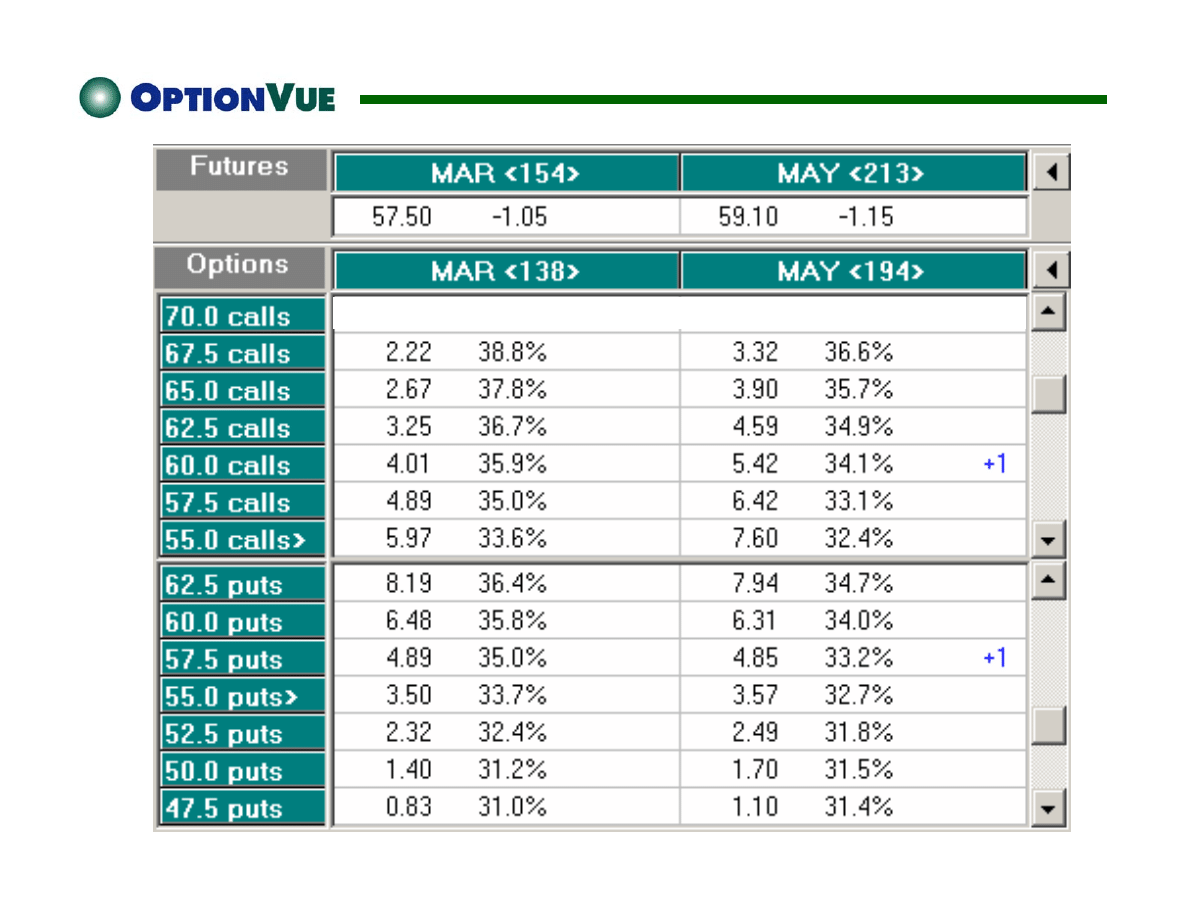

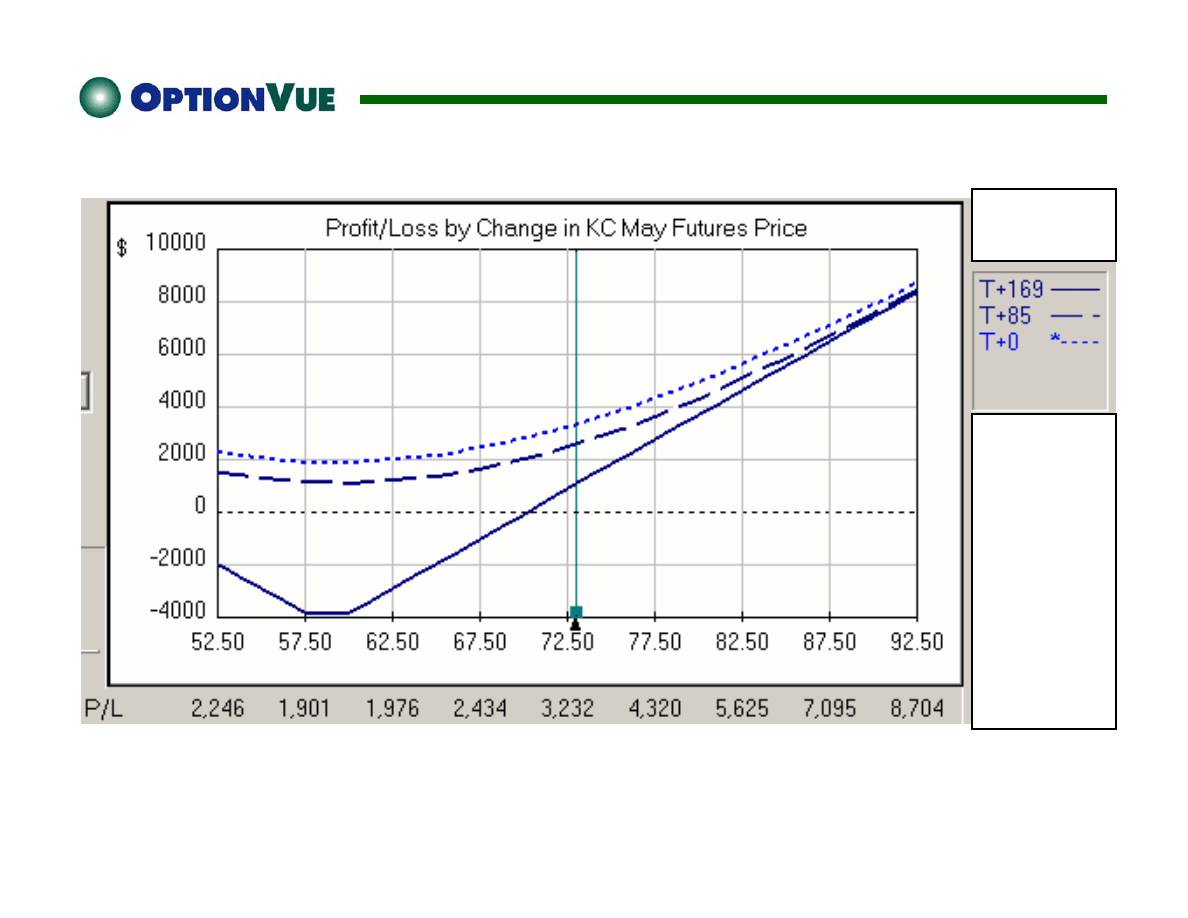

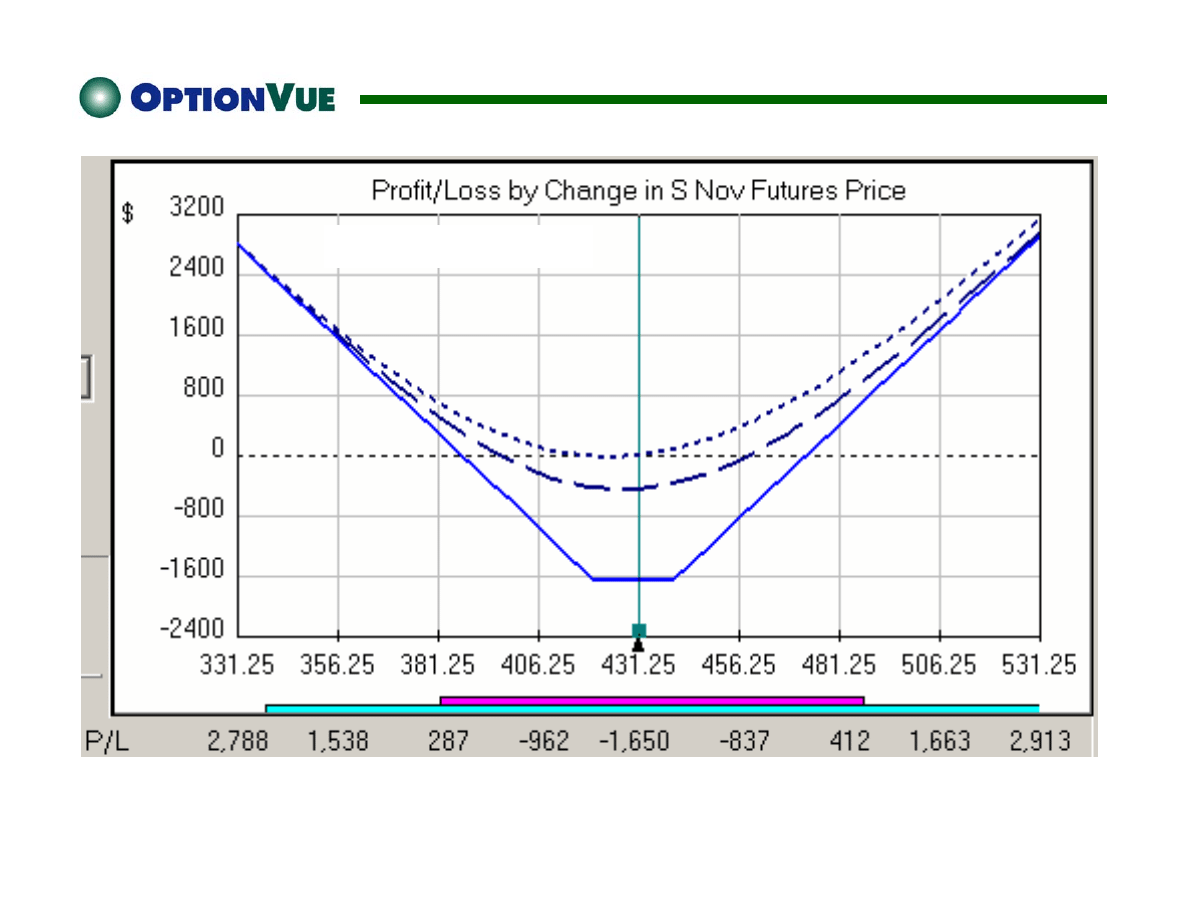

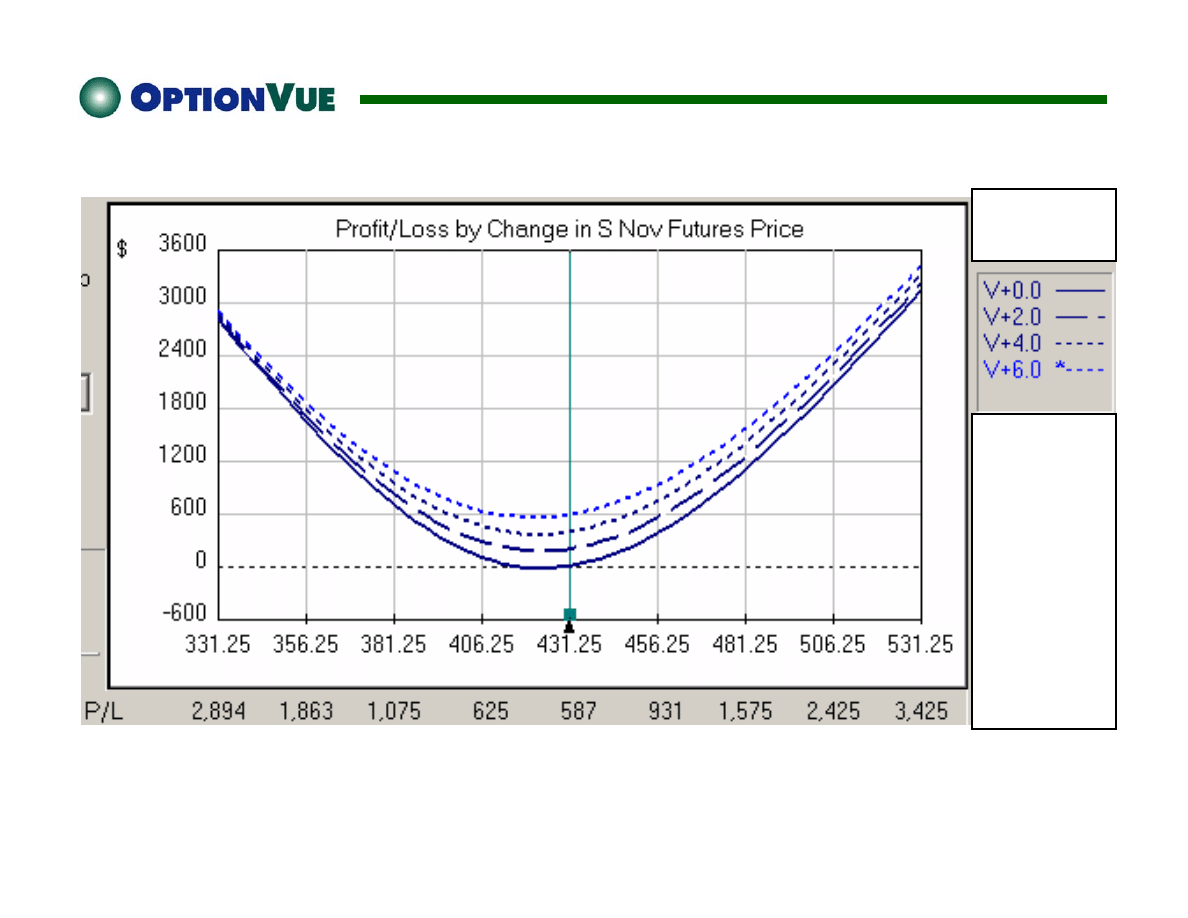

Coffee Straddle -- 30 Days Out

Coffee Straddle -- 30 Days Out

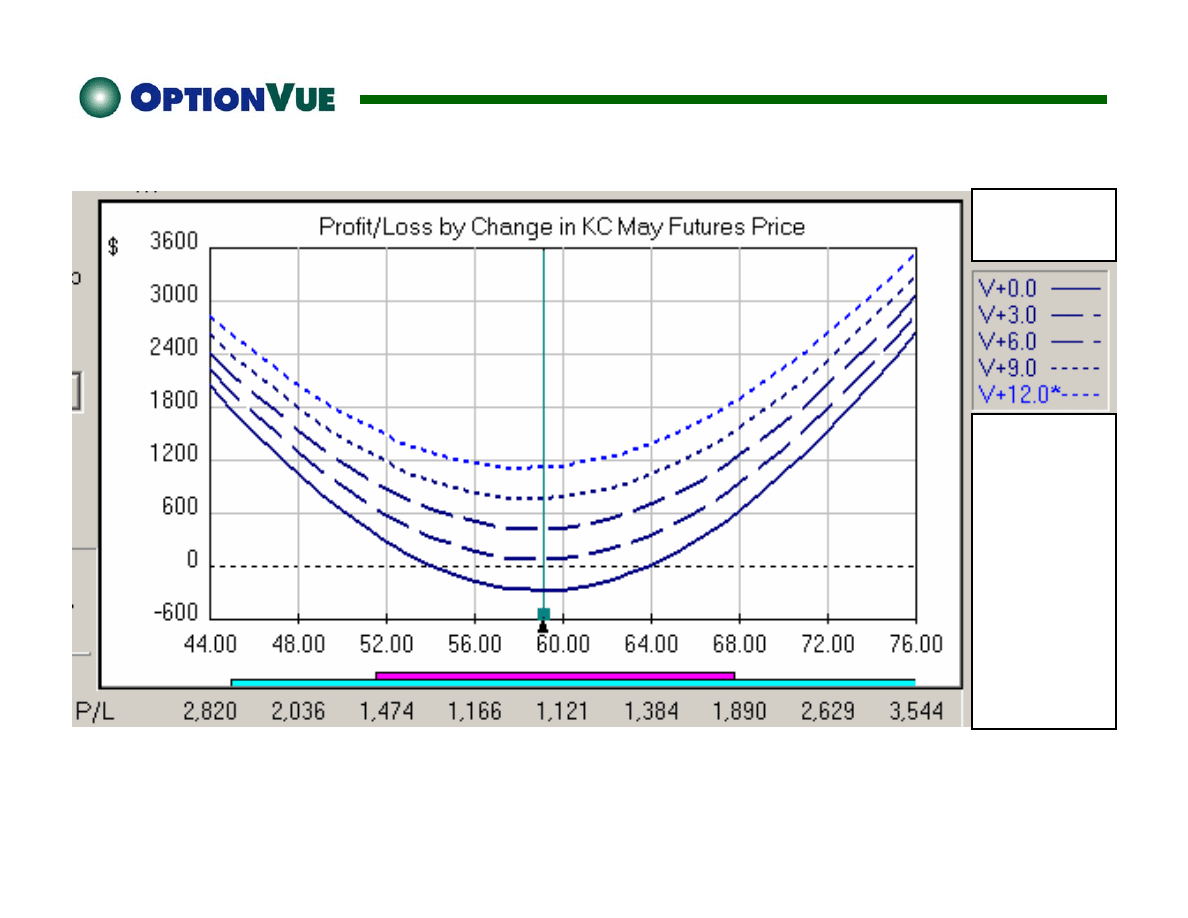

Coffee Straddle -- 30 Days Out – No IV Change

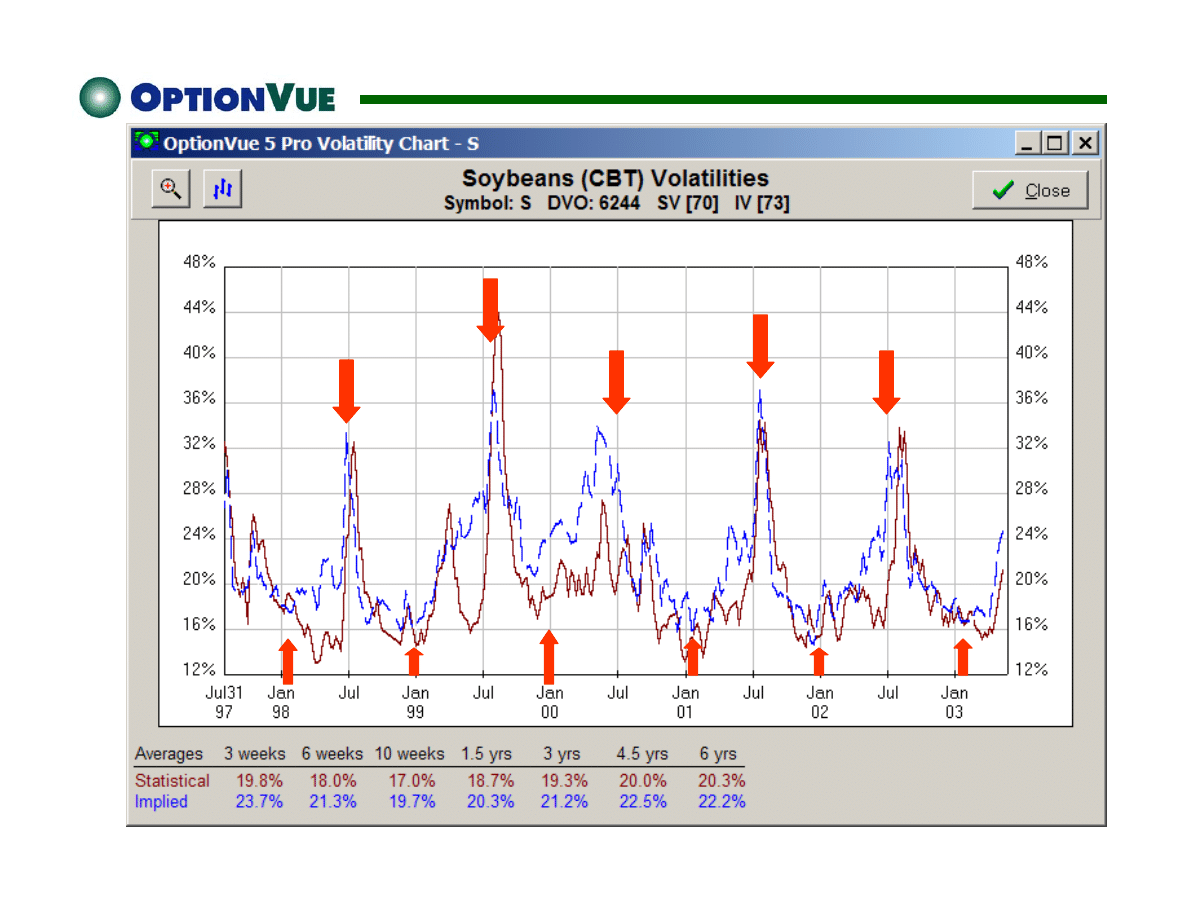

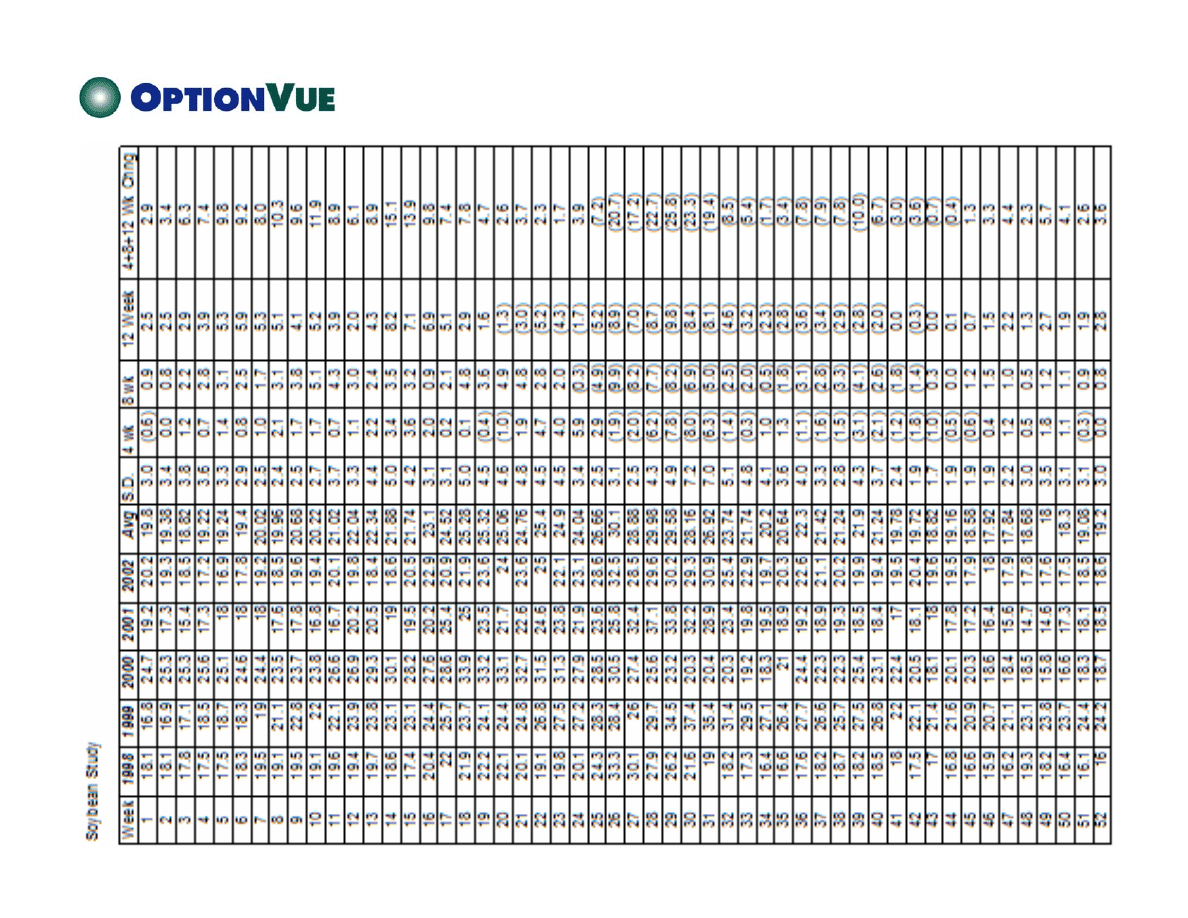

Soybeans

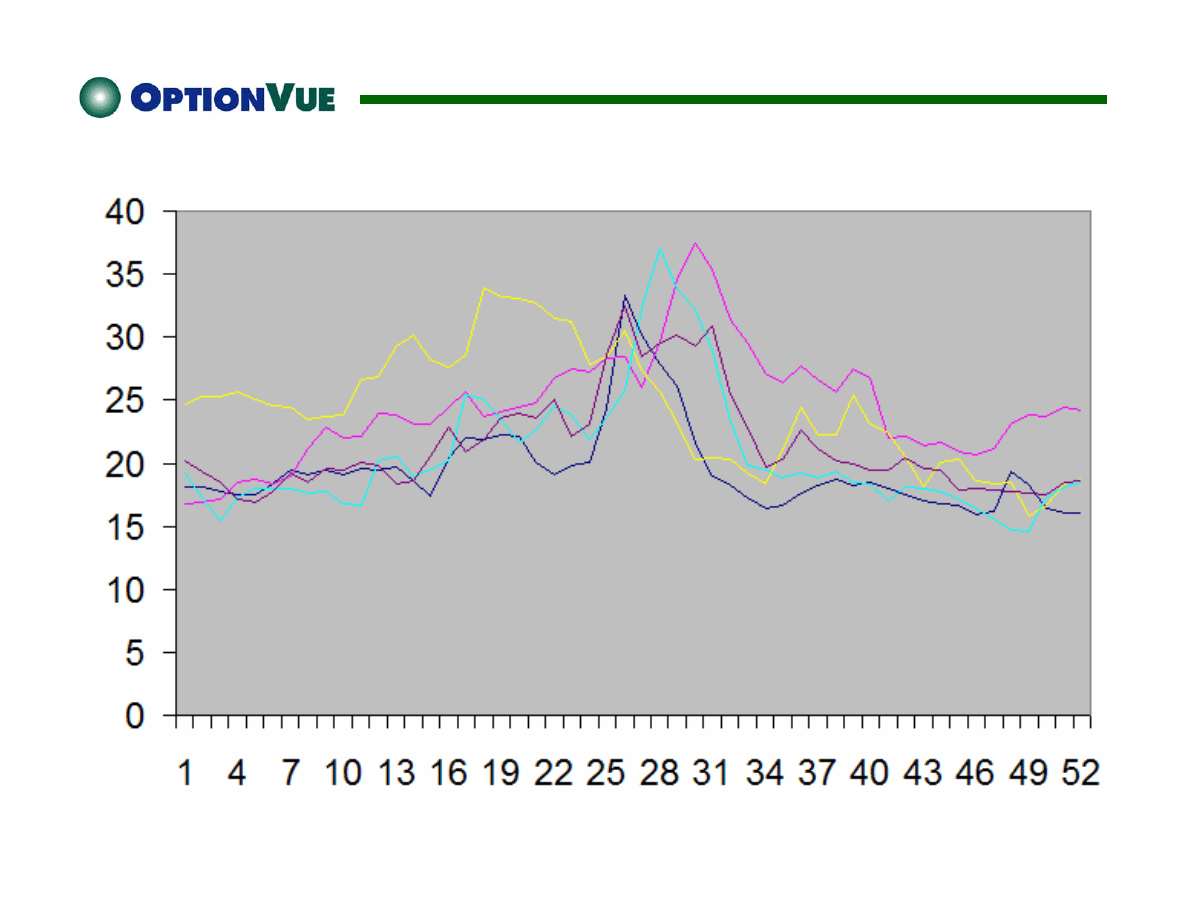

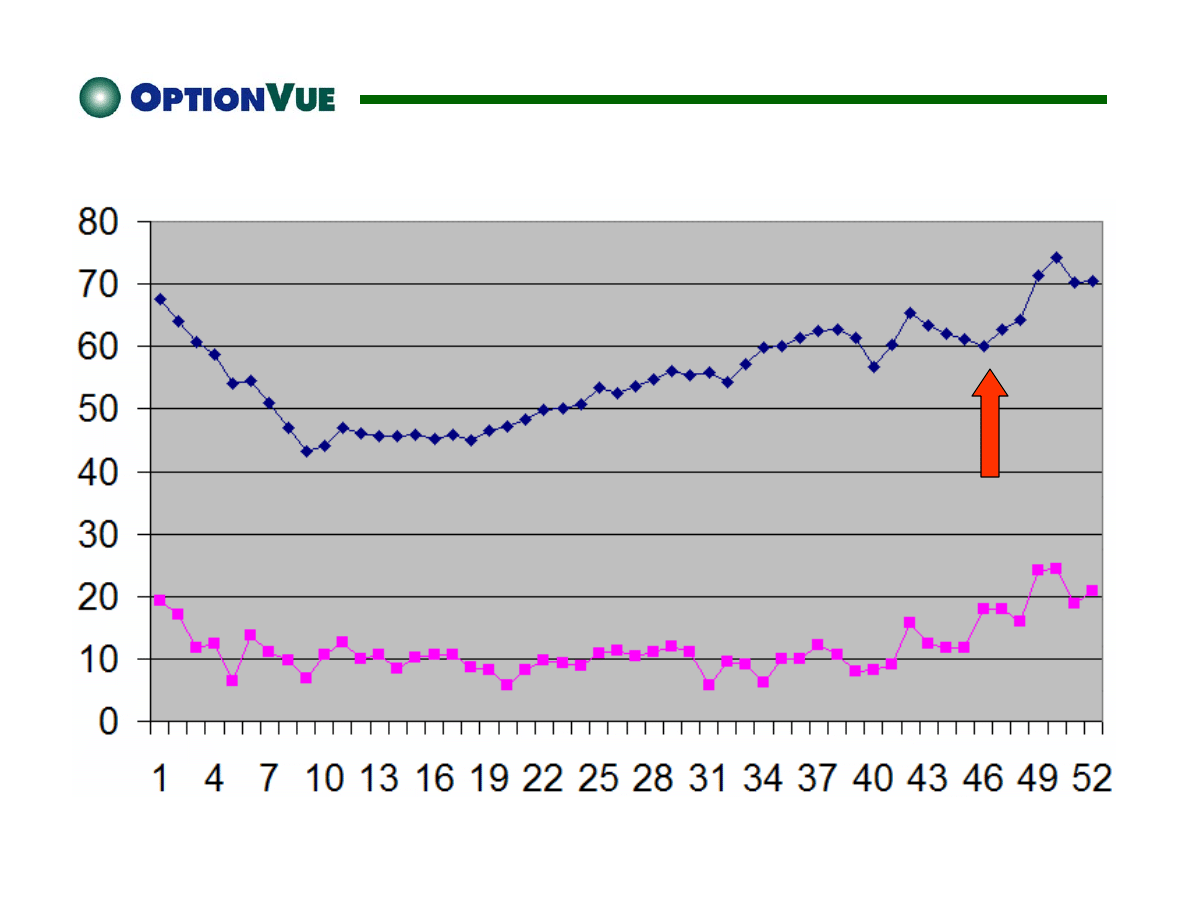

Soybeans IVs by Year

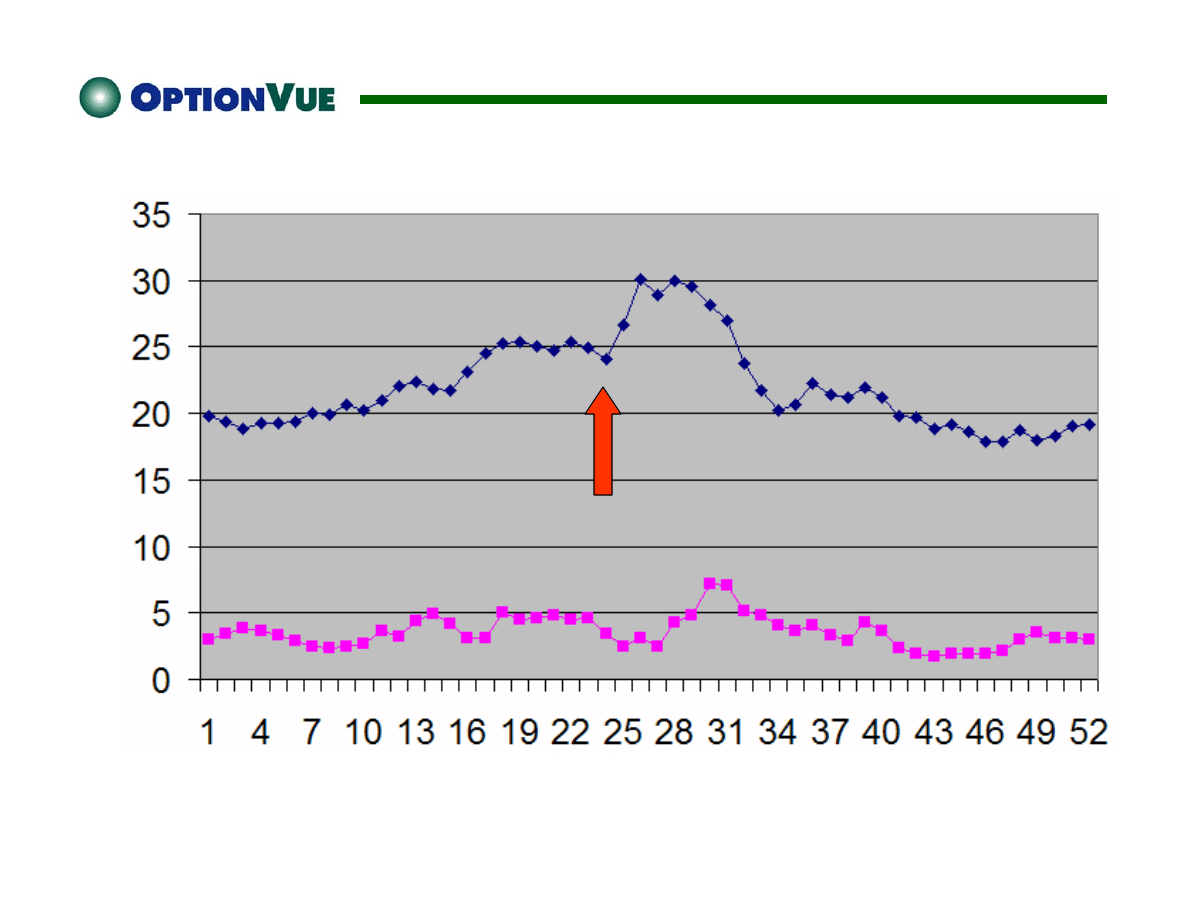

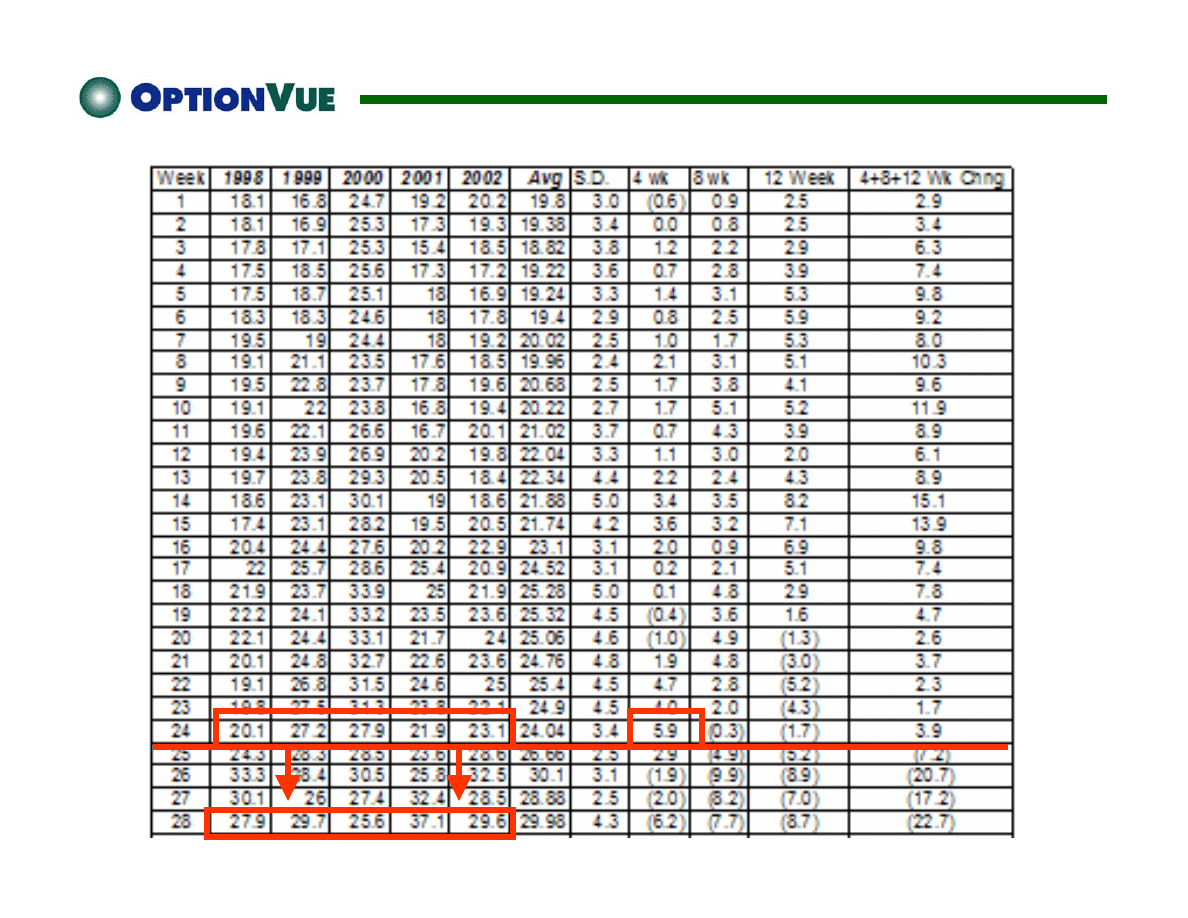

Soybeans Average IVs

Soybeans

6/25/01

$1650 Requirement

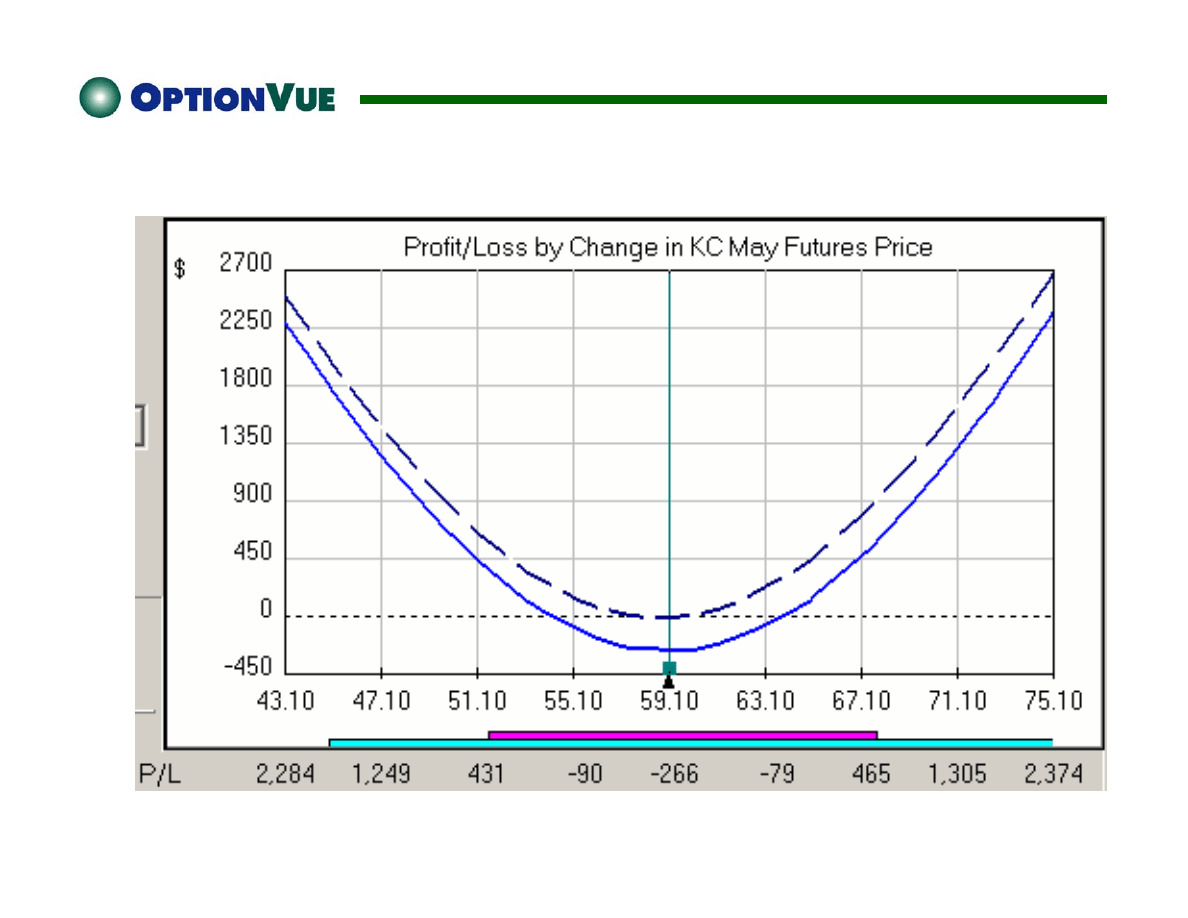

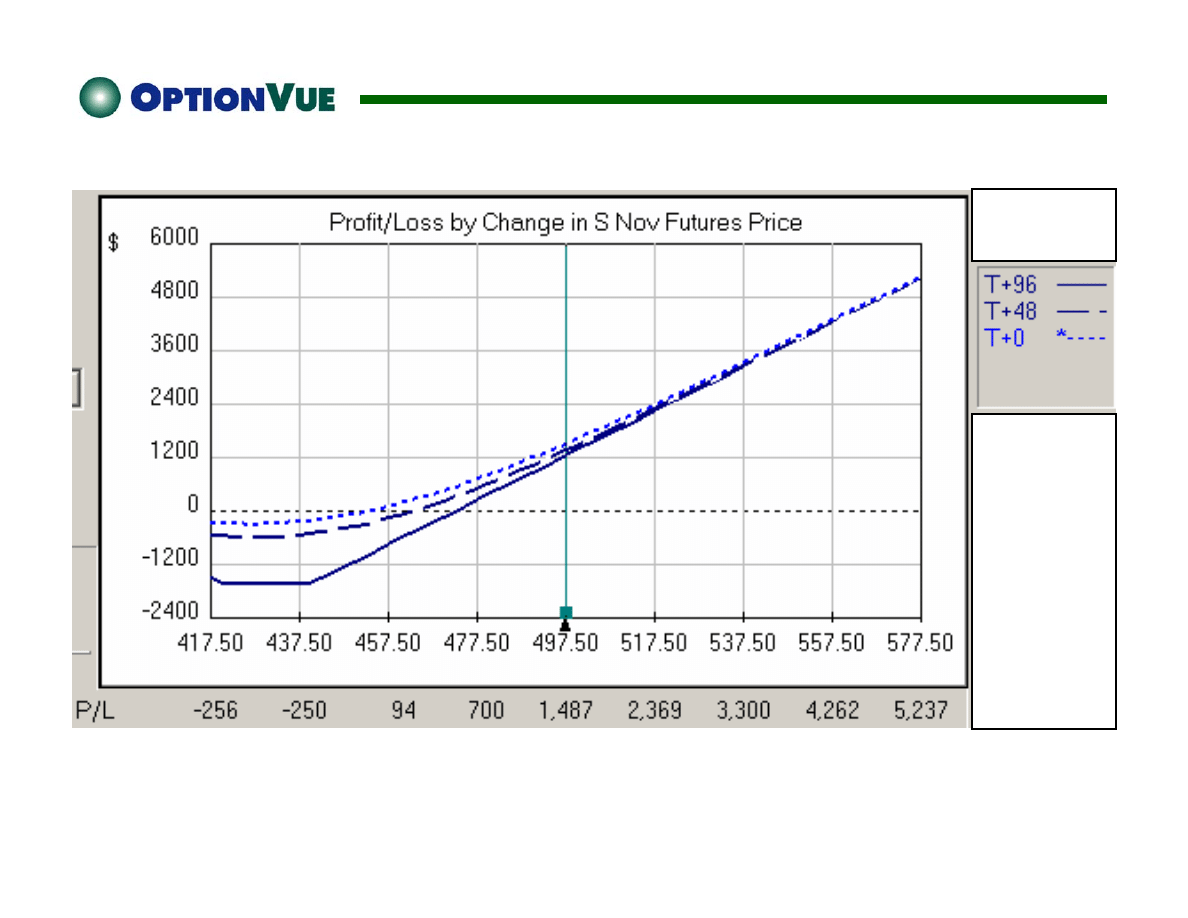

Soybeans Straddle -- 30 Days Out

7/23/01

Soybean Straddle -- 30 Days Out

7/23/01

Soybeans Straddle -- 30 Days Out – No IV Change

Natural Gas

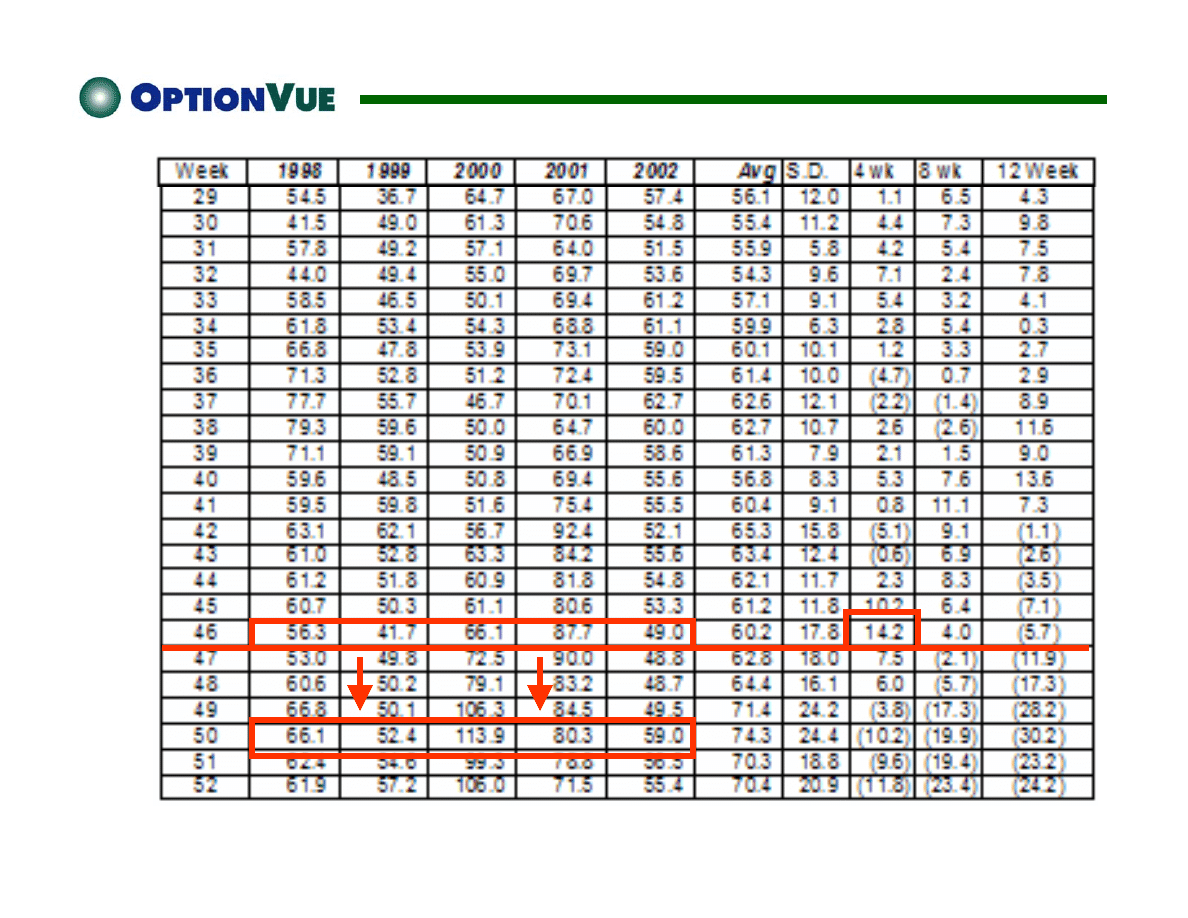

Natural Gas IVs by Year

Natural Gas Average IVs

Natural Gas

11/25/02

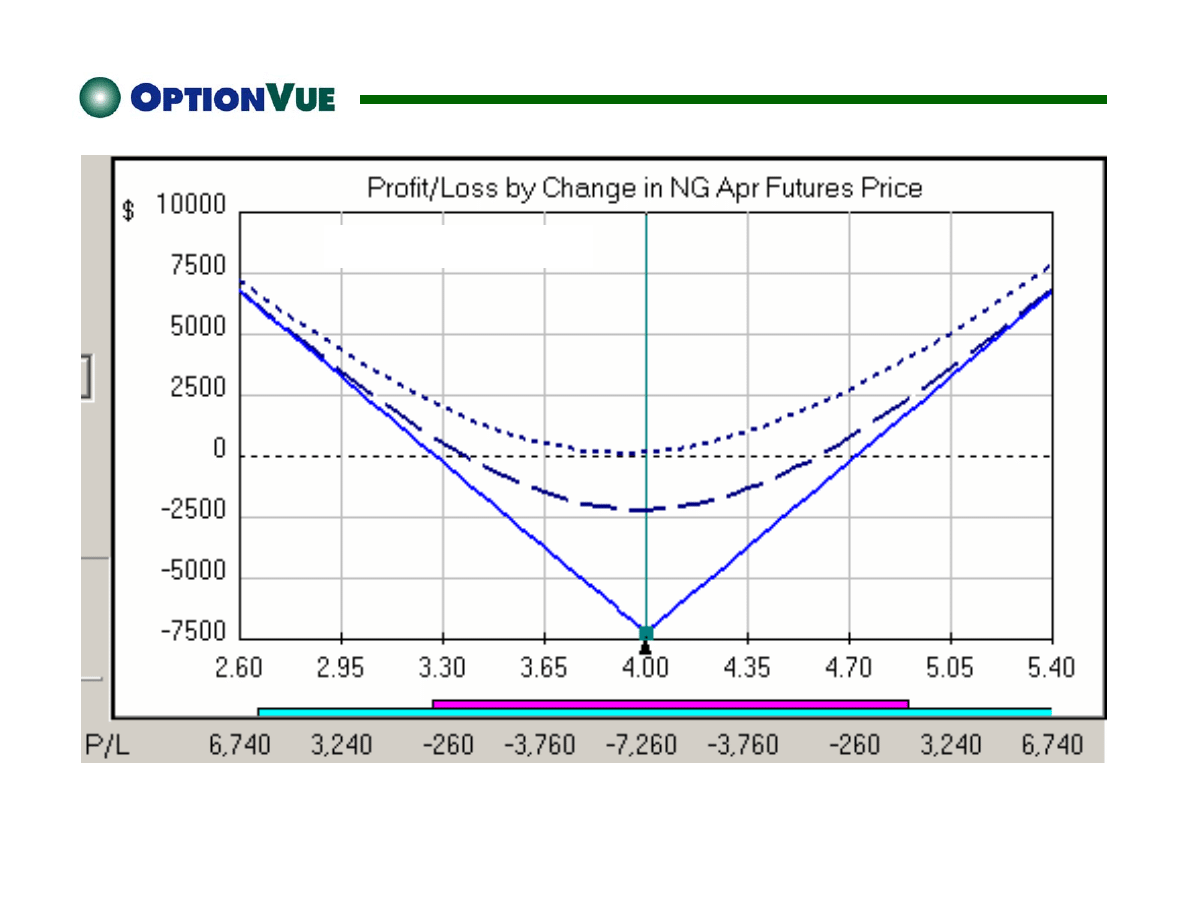

$7260 Requirement

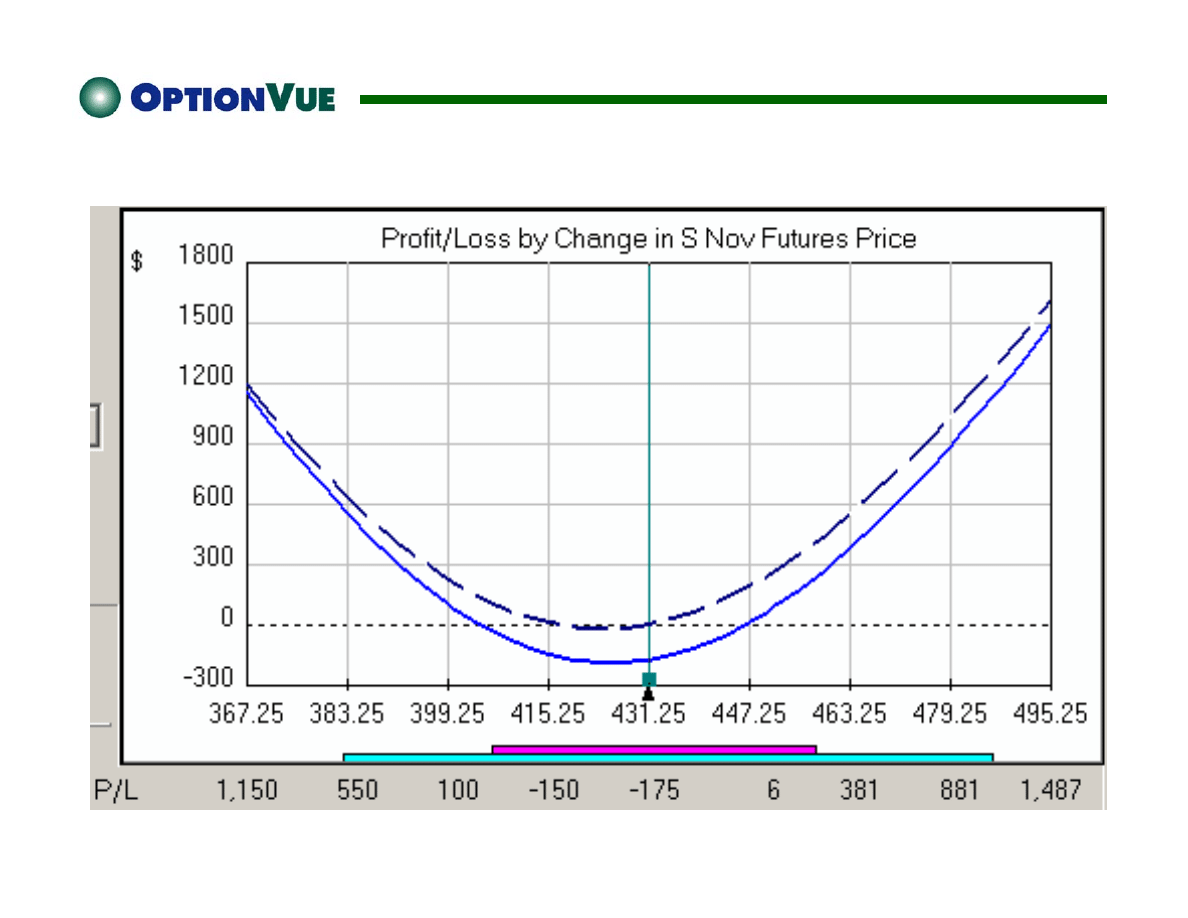

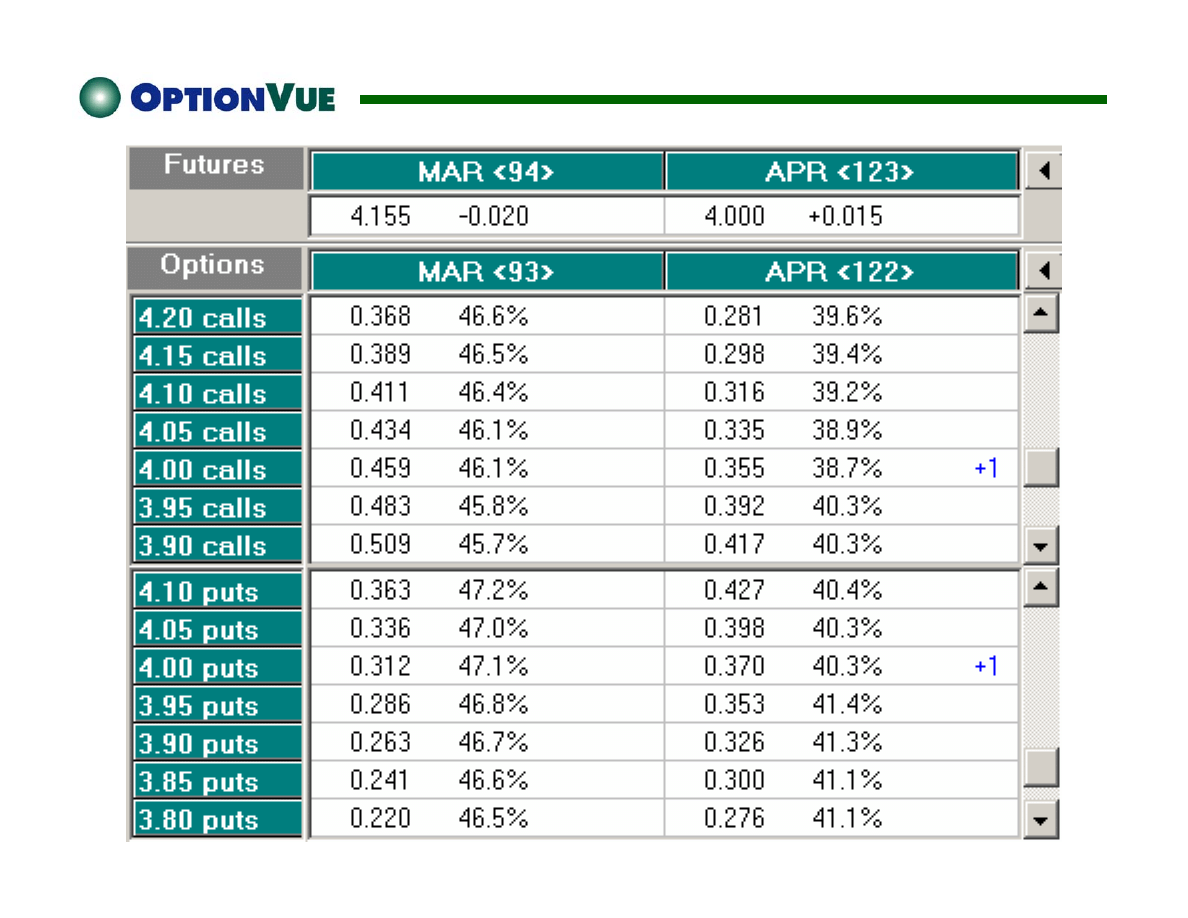

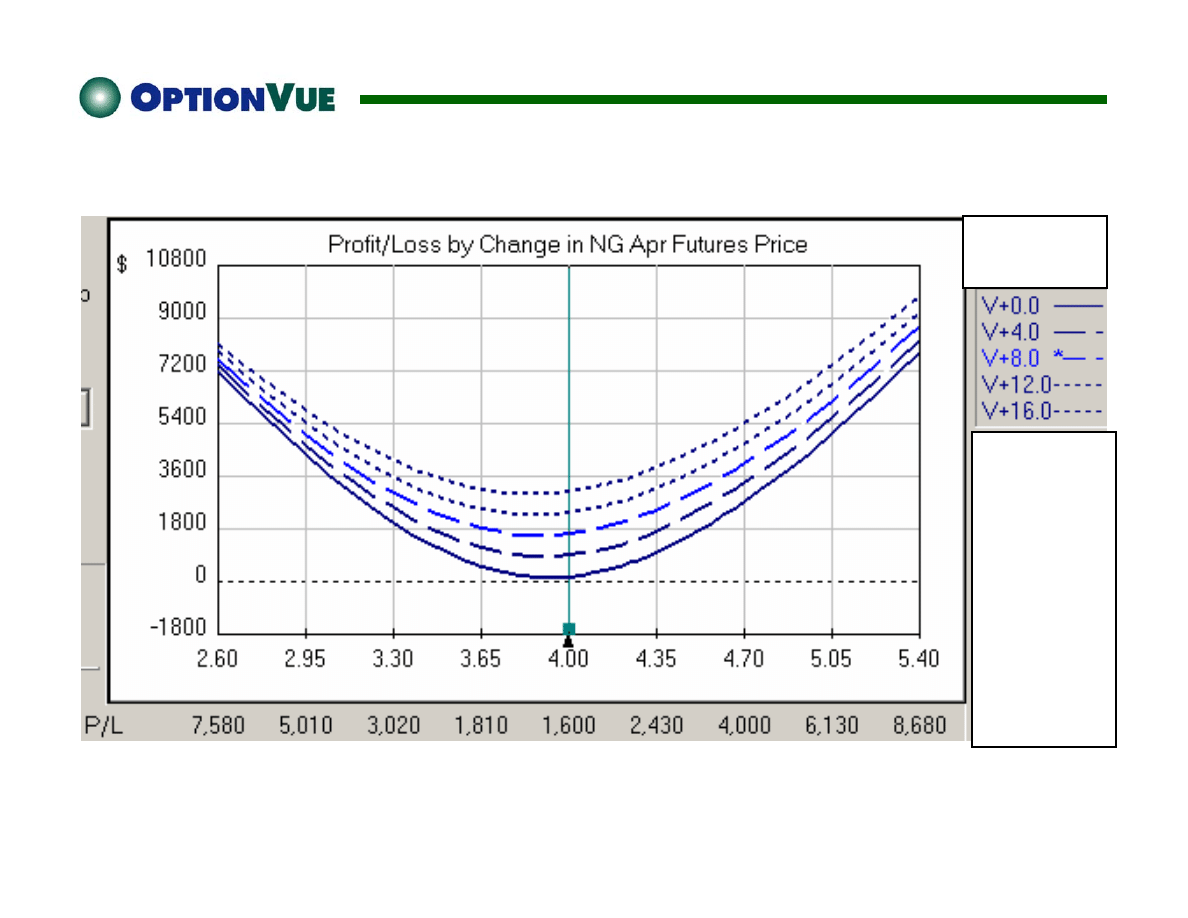

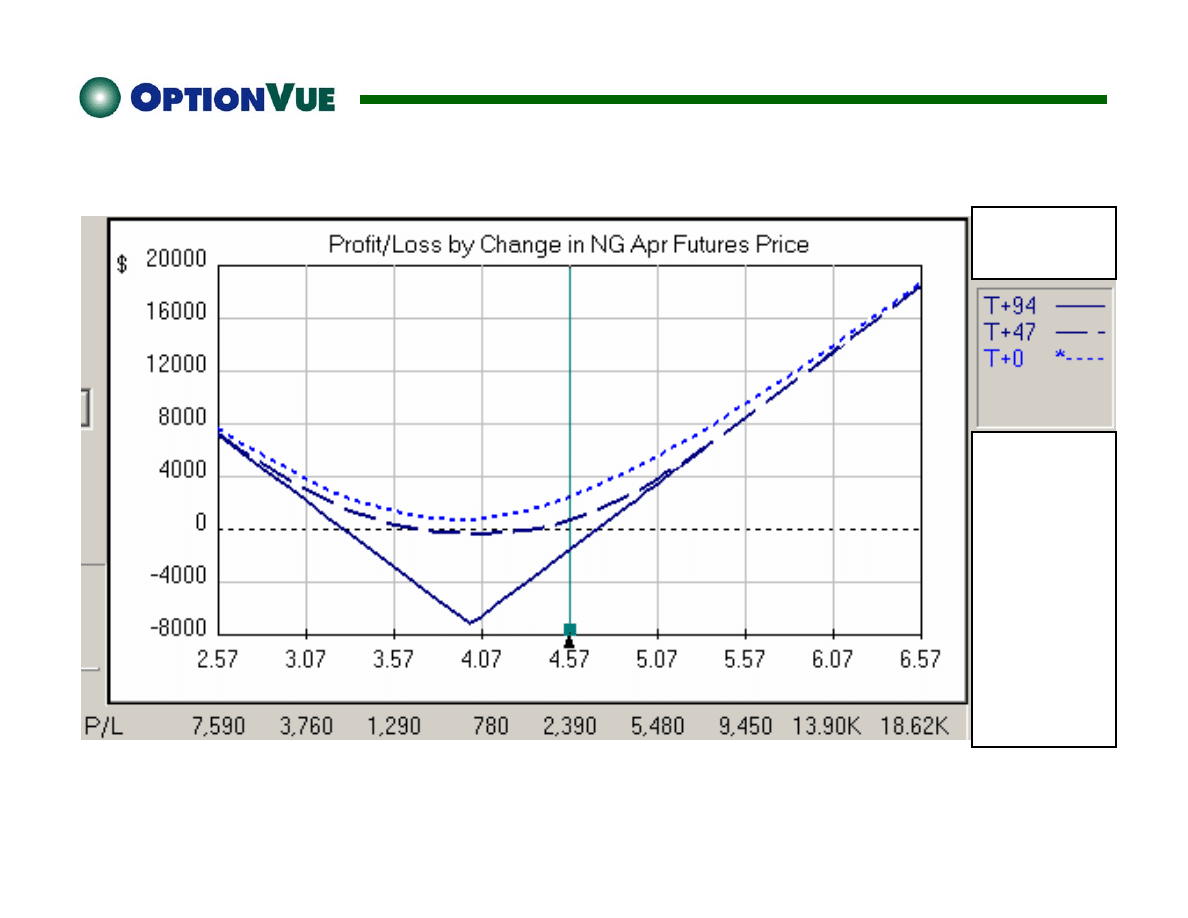

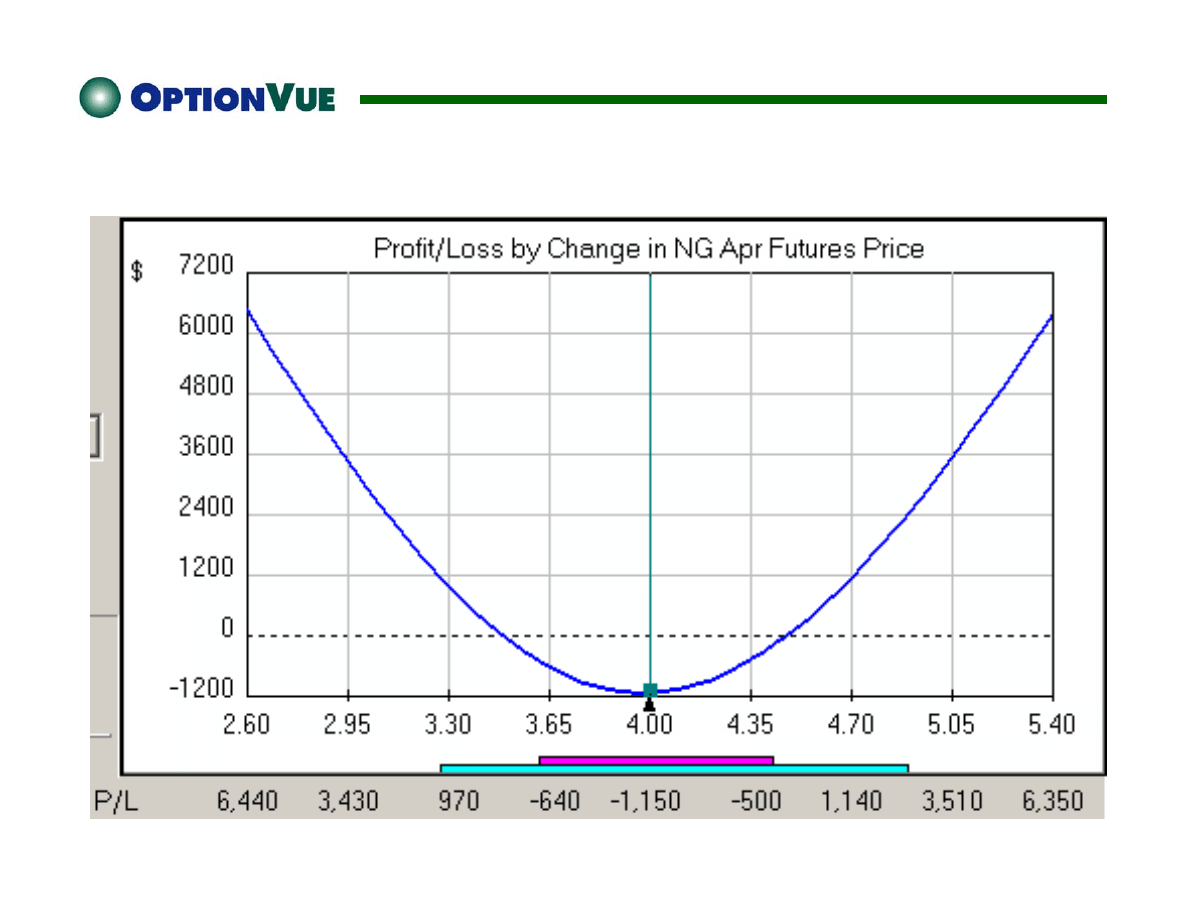

Natural Gas Straddle -- 30 Days Out

12/23/02

Natural Gas Straddle -- 30 Days Out

12/23/02

Natural Gas Straddle -- 30 Days Out – IV Drops 7%

High Probability Futures Options

Trading with Seasonal Straddles

Steve Lentz

Director of Education and Research

OptionVue Research, Inc.

Wyszukiwarka

Podobne podstrony:

chlamydiofiloza bo i ov

ov calendar m

ov covered

MBSE, mbse ov

chlamydiofiloza bo i ov

chor grucz mlek u Ov i kóz

jak wgrać soft OV Newbase

s og g ov t ac

Janez Jalen Ovčar Marko

więcej podobnych podstron