1

MUTUAL FUNDS

_______________________

1

Marijana Ćurak - University of Split, Faculty of Economics

Academic year 2014/2015

10/23/2014

International Week – New Frontiers in Finance and Accounting 2014

University of Economics in Katowice

Course: Financial Institutions

These lecture slides are based on the

book:

Mishkin F. S., Eakins, S. G. (2012), Financial

Markets + Institutions, Addison Wesley

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

2

AGENDA

Benefits of mutual funds

Mutual fund structure

Investment objective classes

Fee structure of investment funds

Review points

Marijana Ćurak - University of Split, Faculty of Economics

3

10/23/2014

2

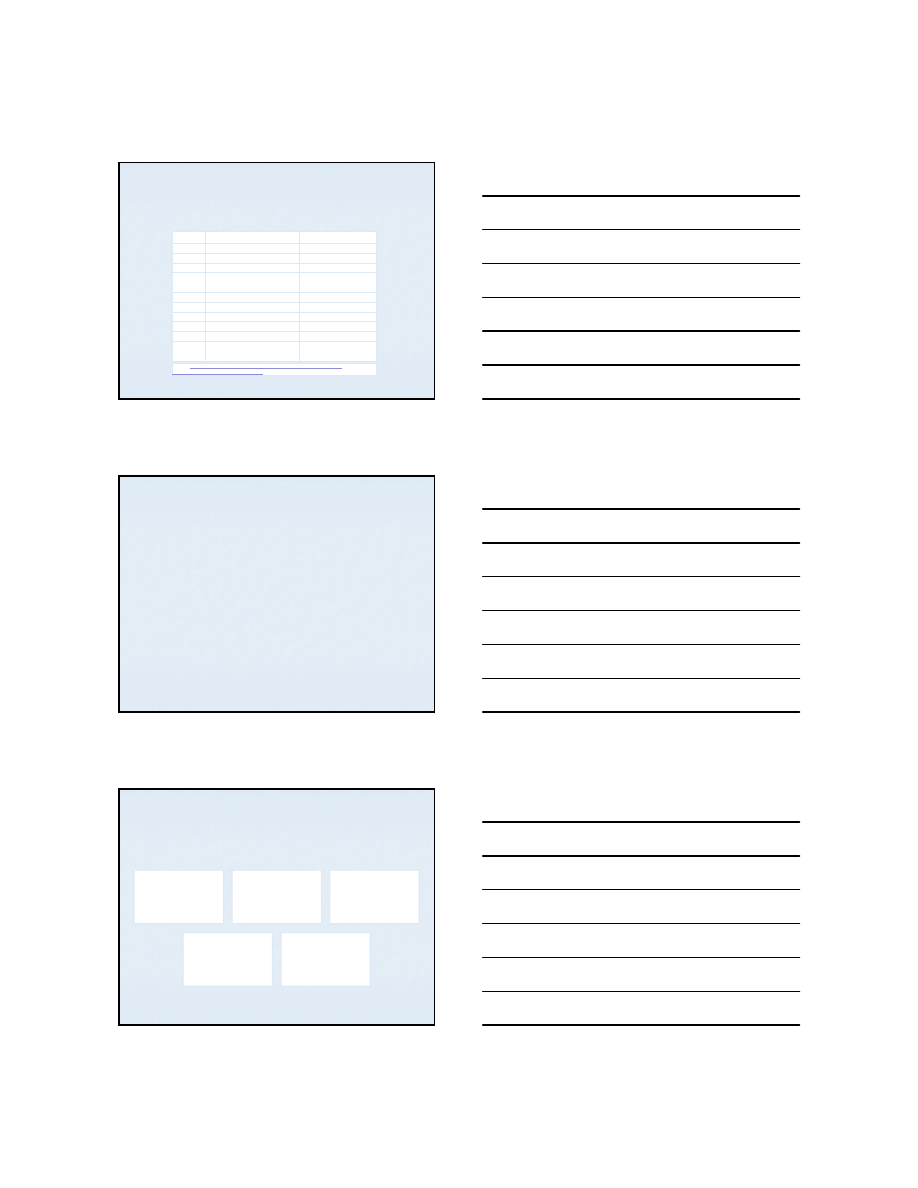

TOP TEN MUTUAL FUNDS IN 2013

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

4

Family

Retail Net Assets

1

Fidelity Investments

$984,173,589,258

2

Vanguard Group

$962,331,327,507

3

American Fund

$956,584,547,987

4

Franklin Templeton

Investments

$377,385,331,414

5

T. Rowe Price & Co.

$345,725,591,811

6

Columbia Management

$167,493,529,444

7

Dodge & Cox

$126,826,526,974

8

OppenheimerFund

$125,473,946,434

9

John Hancock Fund

$119,789,419,458

10

Pacific Investment

Management Co.

$118,411,876,036

Source:

http://education.howthemarketworks.com/mutual-funds/mutual-funds-

intermediate/largest-mutual-fund-families/

(Accessed: October 13, 2014)

MUTUAL FUNDS

Financial intermediaries that pool the

resources of many small investors by

selling them shares in the fund and using

the proceeds to buy securities

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

5

BENEFITS OF MUTUAL FUNDS

Liquidity

intermediation

Denomination

intermediation

Diversification

Cost

advantages

Managerial

expertise

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

6

3

LIQUIDITY INTERMEDIATION

Investors can convert their investments

into cash quickly and at a low cost

Mutual funds allow investors to buy and

redeem at any time and in any amount

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

7

DENOMINATION INTERMEDIATION

It allows small investors access to

securities they would be unable to

purchase without the mutual funds

By pooling money, mutual funds can

purchase securities in large denominations

on behalf of investors

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

8

DIVERSIFICATION

Small investors buying stocks individually

may find it difficult to acquire enough

securities in enough different industries to

capture benefit of diversification

Mutual funds provide a low-cost way to

diversify into various securities

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

9

4

COST ADVANTAGE

Mutual funds negotiate much lower

transaction fees than are available to

individual investors

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

10

MANAGERIAL EXPERTISE

Professional money managers

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

11

MUTUAL FUNDS STRUCTURE

Mutual funds are structured in two ways:

Closed-end fund

Open-end fund

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

12

5

CLOSE-END FUNDS (1)

A fixed number of nonredeemable shares are

sold at an initial offering and are then traded in

the over-the-counter market like common stock

Once shares have been sold, the fund cannot

take in any more investment money

Thus, to grow the fund managers must start a

whole new fund

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

13

CLOSE-END FUNDS (2)

Investors cannot make withdrawals

The only way investors have of getting

money out of their investment in the fund

is to sell shares

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

14

OPEN-END MUTUAL FUNDS (1)

Investors can contribute to an open-end

fund at any time

The fund simply increases the number of

shares outstanding

The fund agrees to buy back shares from

investors at any time

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

15

6

OPEN-END MUTUAL FUNDS (2)

Because the fund agrees to redeem shares at

any time, the investment is very liquid

The open-end structure allows mutual funds to

grow unchecked

As long as investors want to put money into the

fund, it can expand to accommodate them

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

16

OPEN-END MUTUAL FUNDS (3)

Each day the fund’s net asset value is

computed based on the number of shares

outstanding and the net assets of the fund

All shares bought and sold that day re

traded at the same net asset value

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

17

NET ASSET VALUE

It is the total value of the mutual fund’s

stocks, bonds, cash, and other assets

minus any liabilities such as fees, divided

by the number of shares outstanding

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

18

7

INVESTMENT OBJECTIVE CLASSES

Four primary classes of mutual funds are

available to investors:

Stock funds (equity funds)

Bond funds

Hybrid funds

Money market funds

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

19

STOCK FUNDS (EQUITY FUNDS)

They seek rapid capital appreciation

(increase in share prices) and are not

concerned with dividends

Many of these funds are relatively risky n

that the fund managers are attempting to

select companies incurring rapid growth

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

20

BOND FUNDS

Less riskier than stock funds

They invest in corporate bonds,

goverment bonds and municipal bonds

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

21

8

HYBRID FUNDS

They combine stock and bonds into one

fund

The idea is to provide an investment that

diversifies across different types of

securities as well as across different

issuers of a particular type of security

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

22

MONEY MARKET MUTUAL FUNDS

MMMFs are open-end investment funds that

invest only in money market securities

Most funds do not charge investors any fee for

purchasing or redeeming shares

The funds usually require a minimum initial

investment

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

23

INDEX FUNDS

They contain the stocks in an index

The stock are held in a proportion such that changes to

the fund value closely match changes to the index level

The funds do not require managers to choose securities.

As a result, these funds tend to have lower fees than

other actively managed funds.

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

24

9

FEE STRUCTURE (1)

The purpose of loads is to provide

compensation for sales brokers

Load funds

Front-end load

The fee is charged when the funds are deposited

Deferred load

The fee is charged when funds are taken out

(usually a declining fee over five years)

The motivation for this fee is to discourage early

withdrawal of deposits

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

25

FEE STRUCTURE (2)

No-load funds

The funds that do not charge a direct load

Most no-load funds can be purchased directly

by individual investors, and no middleman is

required

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

26

FEE STRUCTURE (3)

The usual fees charged by mutual funds

are the following:

A contingent deferred sales charge imposed

at the time of redemption is an alternative

way to compensate financial professionals for

their services

A redemption fee is back-end charge for

redeeming shares

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

27

10

FEE STRUCTURE (4)

A exchange fee – may be charged when

transferring money from one fund to

another within the same fund family

An account maintenance fee is charged by

some funds to maintain low balance

accounts

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

28

REVIEW POINTS (1)

Mutual funds provide liquidity

intermediation, denomnation

intermediation, diversification, cost

advantages and managerail expertise

Mutual funds can be organized as either

open- or closed-end funds

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

29

REVIEW POINTS (2)

The primary classes of mutual funds are

stock funds, bond funds, hybrid funds and

money market funds

10/23/2014

Marijana Ćurak - University of Split, Faculty of Economics

30

11

REFERENCES AND SOURCE OF DATA

Mishkin F. S., Eakins, S. G. (2012), Financial

Markets + Institutions, Addison Wesley, p. 528-

550.

http://education.howthemarketworks.com/mutu

al-funds/mutual-funds-intermediate/largest-

mutual-fund-families/

(Accessed: October 13,

2014)

Marijana Ćurak - University of Split, Faculty of Economics

31

10/23/2014

Wyszukiwarka

Podobne podstrony:

MUTUAL FUNDS ON POLISH MARKET(1)

Amibroker Technical Analysis Software Charting, Backtesting, Scanning Of Stocks, Futures, Mutual Fu

hedge funds

ROLE OF THE COOPERATIVE BANK IN EU FUNDS

mutualizm seminarium

Dickens Our Mutual Friend

Pension Funds

Sovereign Wealth Funds

Mutual DCP nowy

hedge funds

(Trading) Gregory Connor and Mason Woo Introduction To Hedge Funds (2003)

Gayle Buck Mutual Consent (pdf)

więcej podobnych podstron