Legal environment for M&A

EU, US and international antitrust policies

Mariusz-

Jan Radło, Ph.D.

Outline & references

Rationale for merger regulations

EC Merger Regulation

US antitrust law

Merger control in Poland

Case study GE/Honeywell Merger

References:

DePamphilis (2010) Chapter 2.

COUNCIL REGULATION (EC) No 139/2004 of 20 January 2004 on the

control of concentrations between undertakings (the EC Merger Regulation)

Desai M.A. and Villalonga B. (2003) Antitrust Regulations in a Global

Setting: The EU Investigation of the GE/Honeywell Merger, Harvard

Business School, 9-204-081, December 23, 2003.

Rationale for merger regulations

Merger can bring benefits to the economy

and companies by increased efficiency

and higher-quality goods at fairer prices.

1.

Combining forces of various companies by mergers

and acquisitions can expand markets and bring

benefits to the economy and these companies.

2.

E.g.: companies after the merger can develop new

products more efficiently or to reduce production or

distribution costs.

3.

Thanks to their increased efficiency, the market

becomes more competitive and consumers benefit

from higher-quality goods at fairer prices.

Rationale for merger regulations

Mergers may

reduce competition

by

creating/strengthen

ing a dominant

player.

This can lead to:

higher prices,

reduced choice

less innovation.

Rationale for merger regulations

Mergers are also affected by other

legislation concerning e.g.:

labor market,

environment

or specific sectors

Mergers and the EU Single

market

Growing internal market of the EU make it more

attractive for companies to join forces.

This can result in growth of the competitiveness of European

industry and the raise of the standard of living in the EU.

However, it can also impede competition and result in additional

costs for European customers.

Therefore, the objective of the EU competition policy is to

prevent harmful effects of M&A on competition.

M&A going beyond the national borders of any one

Member State are examined at European level.

Antitrust regulations and M&A

strategy

Antitrust regulations are one of the most

important issues of the M&A planning process

A large number of regulatory agencies and

regulatory laws makes many mergers difficult

and costly.

Case:

Coca-Cola

’s 1999 acquisition of the Cadbury

Schweppes beverage brands, including Schweppes,

Dr. Pepper, and Canada Dry:

more than 160 countries.

more than 40 jurisdictions around the world

fees for seeking approval ranged from $77 to $2.5 billion in various

countries

EU Merger Law

In the European Union mergers going beyond

the national borders of any one Member State

are examined at European level. This allows

companies trading in different EU Member

States to obtain clearance for their mergers in

one go.

The general test is whether a concentration (i.e.

merger or acquisition) with a community

dimension (i.e. affects a number of EU member

states) might significantly impede effective

competition.

EU Merger Law

Treaty of Rome did not deal specifically

with mergers and acqusitions. In the early

years of the EEC the treatment of M&A

was by case law in the ECJ.

Articles 81 and 82 of the Treaty

Establishng the European Community

The Continental Can case of 1973 (Art. 82)

The BAT/PhillipMorris case of 1987 (Art. 81)

EU Merger Law

Articles 81 and 82 of the Treaty

Establishng the European Community

The Continental Can case of 1973

established that Art. 82 could apply to

mergers.

Article 82 EC deals with monopolies, or more

precisely firms who have a dominant market

share and abuse that position.

EU Merger Law

Articles 81 and 82 of the Treaty Establishng the

European Community

In 1987 BAT/PhillipMorris case the ECJ went further and

declared that in the absence of the domiant position, a horizontal

qcquisition could be penalised as forming an anti-competitive

agreement under Art.. 81.

Article 81 of the Treaty Establishng the EC (formerly the Treaty

of Rome). The European Community is the name for the

economic and social pillar of EU law, under which competition

law falls. EC, which deals with cartels and restrictive vertical

agreements. Prohibited are: "(1) ...all agreements between

undertakings, decisions by associations of undertakings and

concerted practices which may affect trade between Member

States and which have as their object or effect the prevention,

restriction or distortion of competition within the common

market...„

EU Merger Law

Also under Article 82 EC, the European

Council was empowered to enact a

regulation to control mergers between

firms, currently the latest known by the

abbreviation of Regulation 139/2004/EC.

EC Merger Regulation (2004) - ECMR

European Commission

– responsible for

execution of the EU Merger Law

EU Merger Law

The EC has exclusive jurisdiction over a

“concentration” of a “community

dimension.”

The EU Member States may not apply

their merger regimes to such transactions

(ECMR, Art. 21(3.)), except where the EC

refers such a transaction to Member State

authorities under ECMR Art. 9.2

What is concentration?

the merger of two or more previously independent

undertakings,

the acquisition (of one or more persons already

controlling at least one undertaking, or by one or more

undertakings - whether by purchase of securities or

assets, by contract or by any other means) of direct or

indirect control of the whole or parts of one or more

other undertakings,

the creation of a joint venture performing on a

lasting basis all the functions of an autonomous

economic entity.

A concentration has a Community

dimension where:

Test 1

worldwide turnover is exceeds EUR 5 billion and the

aggregate Community-wide turnover of each of at

least two firms involved exceeds EUR 250 million

None of the firms involved achieves more than two-

thirds of its aggregate Community-wide turnover

within one member state (MS).

A concentration has a Community

dimension where:

Test 2:

worldwide turnover of all firms exceeds EUR 2.5

billion

in each of at least three MS, the turnover of all firms

involved exceeds EUR 100 million

in each of at least three above MS the turnover of

each of at least two of the firms involved exceeds

EUR 25 million

the Community-wide turnover of each of at least two

of the firms involved exceeds EUR 100 million, unless

each of the undertakings concerned achieves more

than two-thirds of its aggregate Community-wide

turnover within one and the same Member State.

When Member States may review

Concentrations of a Community Dimension?

When:

1. the merger threatens to affect significantly competition

in a market within that Member State, which presents all

the characteristics of a distinct market; or

2. the merger affects competition in a market within that

Member State, which presents all the characteristics of a

distinct market and which does not constitute a

substantial part of the common market.

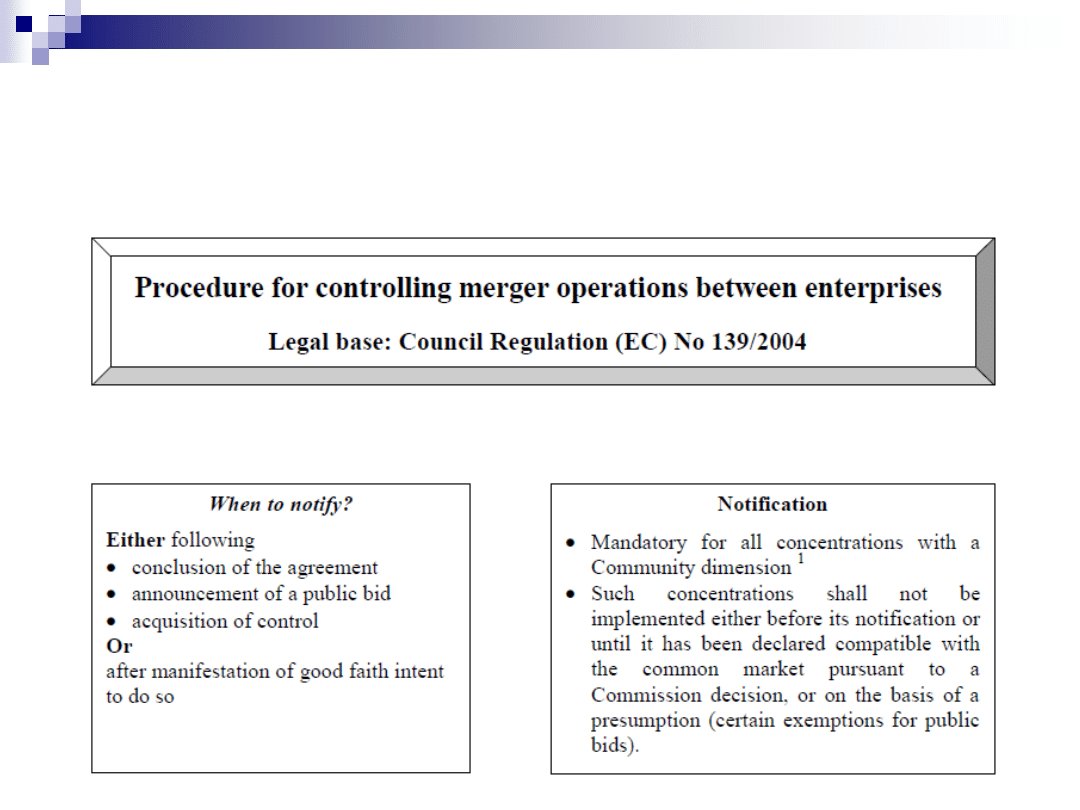

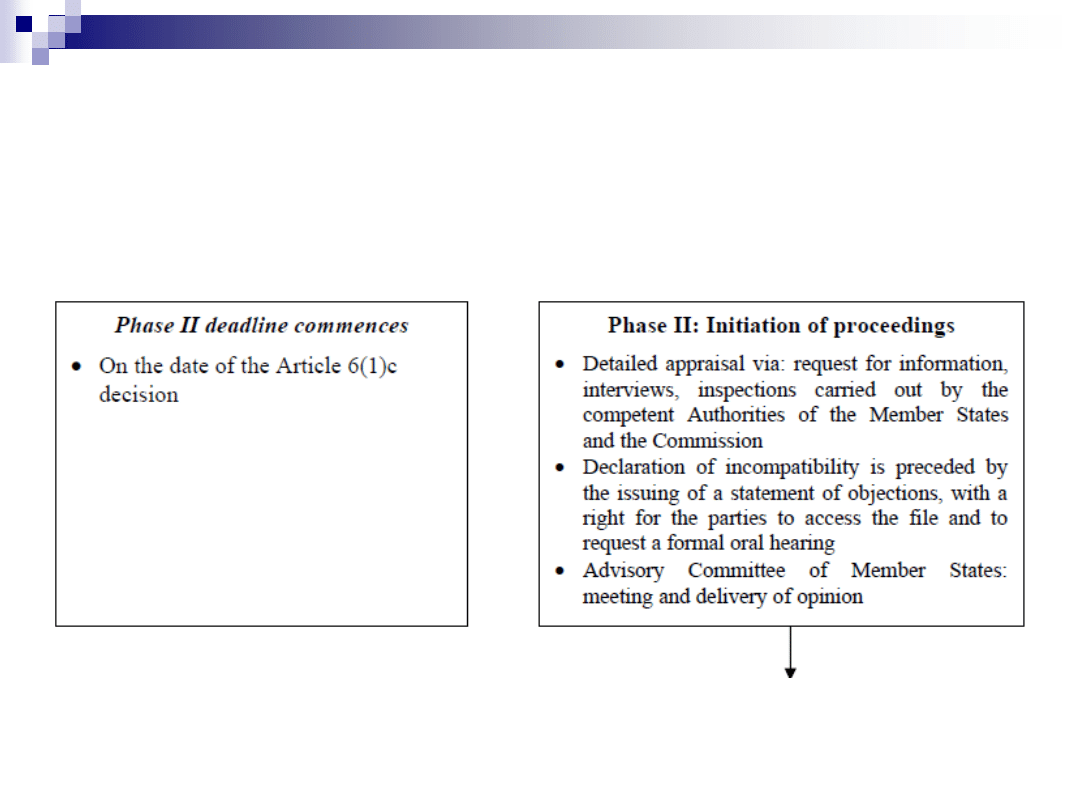

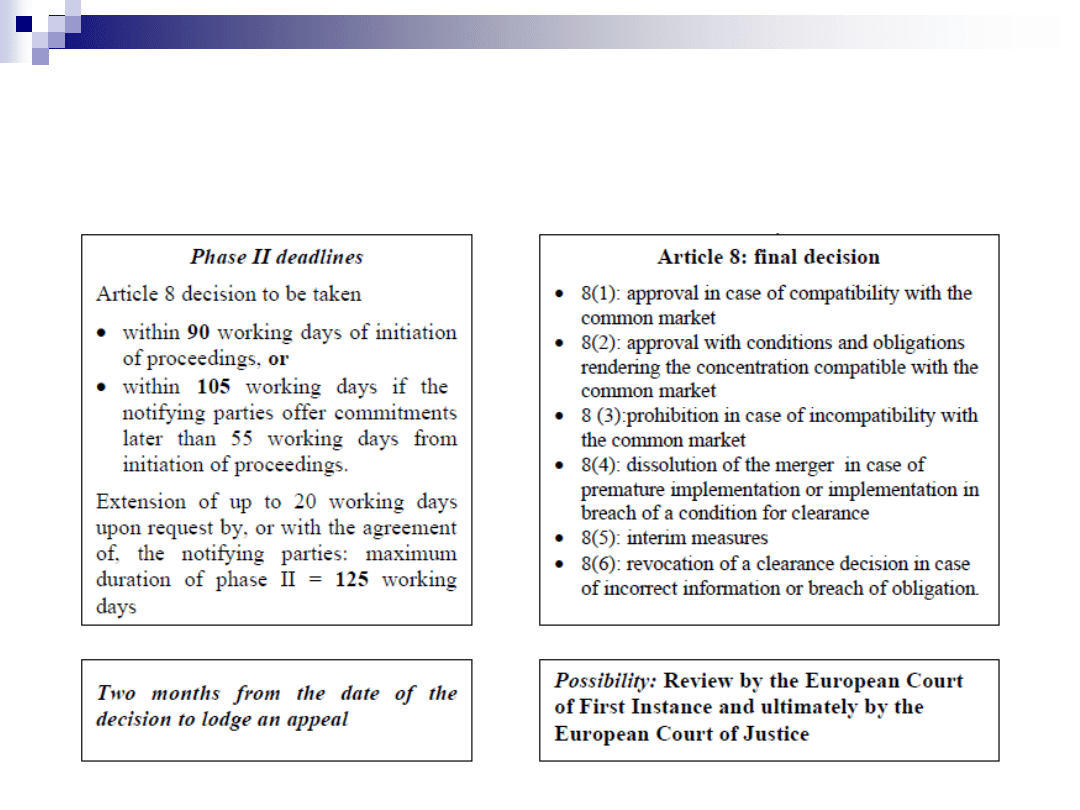

Procedure for controlling

mergers in the EU

Procedure for controlling

mergers in the EU

Procedure for controlling

mergers in the EU

When are mergers prohibited or

approved?

Mergers are aproved unconditionally when they

do not significantly impede effective competition

in the EU.

If they do, and no commitments aimed at

removing the impediment are proposed by the

merging firms, they must be prohibited.

Mergers may be prohibited, if the merging parties are major

competitors or if the merger would otherwise significantly

weaken effective competition in the market, in particular by

creating or strengthening a dominant player.

When mergers are approved

conditionally?

Even if the proposed merger could distort

competition, the parties may commit to taking

action to try to correct this likely effect.

They may commit, for example, to sell part of the combined

business or to license technology to another market player.

If the European Commission is satisfied that the commitments

would maintain or restore competition in the market it can give

conditional clearance for the merger.

The EC monitors whether the merging companies fulfill their

commitments and may intervene if they do not.

US antitrust law

Sherman Act of 1890

Clayton Act of 1914

Hart-Scott-Rodino Act of 1976

The Antitrust Guidelines

US antitrust law

Sherman Act of 1890

Section 1: prohibits mergers that would tend

to create a monopoly or undue market control.

Case: merger between Staples and Office Depot.

Section 2 is directed against firms that had

already become dominant in their markets in

the view of the government.

This was the basis for actions against IBM and

AT&T in the 1950s.

US antitrust law

Clayton Act of 1914

Created the Federal Trade Commission

– it

can block mergers resulting in tendency

toward increased concentration

It is illegal for a company to acquire another

company if competition could be adversely

affected.

US antitrust law

Hart-Scott-Rodino Act of 1976

Strengthened the powers of the Department

of Justice and and the Federal Trade

Commission by requiring approval before a

merger could take place.

Hart-Scott-Rodino Act requires that mergers

exceeding a certain size must notify the FTC

and DoJ at the time it makes an offer to the

target.

Before HSR, antitrust actions were usually

taken ex post.

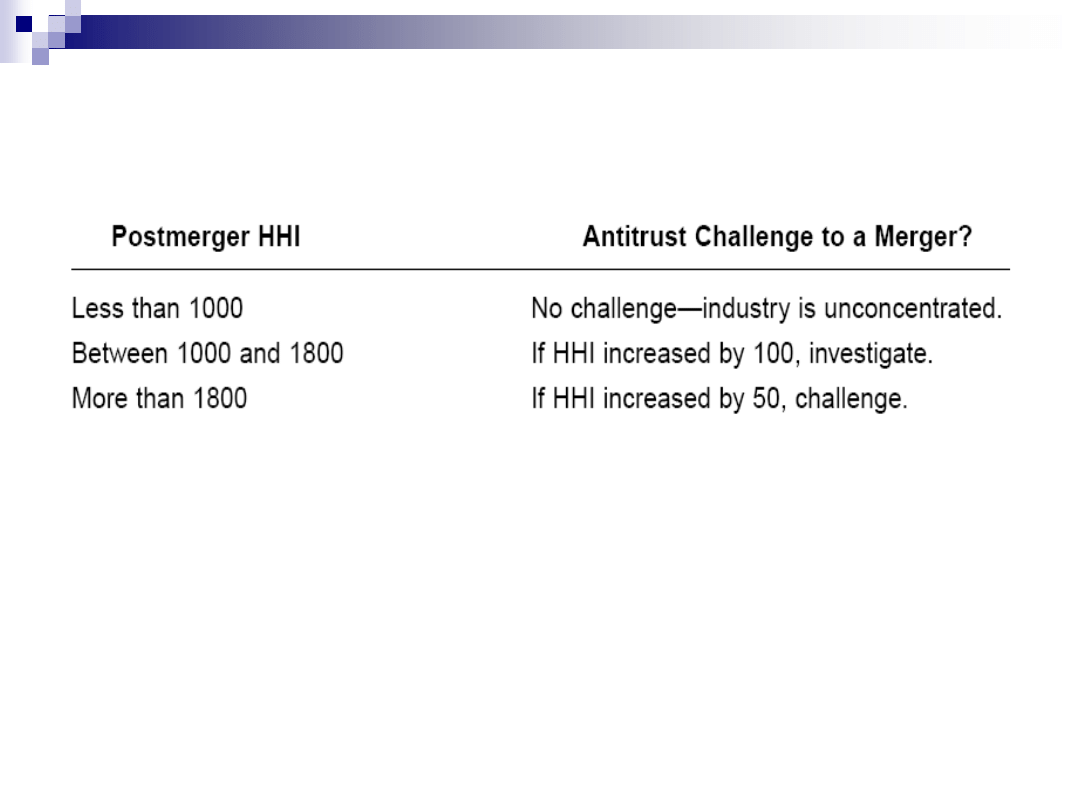

US Critical Concentration Levels

Herfindahl-Hirschman Index (HHI) - a concentration measure

(the sum of the squares of market shares of each firm in the industry).

E.g.: 10 firms:

>>>>>>>each 10 percent market share: HHI=1000

>>>>>>>one 90 percent market share, and the nine others a

1 percent market share: HHI=8109

Market characteristics: the ability of the competitors to expand

the supply of a product if one firm tries to restrict output

…

Poland: merger control

Office for Competition and Consumer Protection (UOKiK)

Participants of the planned transaction are obligated to

obtain prior clearance of the President of the Office of

Competition and Consumer Protection when:

their turnover in the year preceding the application exceeded EUR 1

billion in the world

or EUR 50 million in Poland.

The obligation to notify is excluded due to potentially

insignificant impact of the planned transaction on the

market when:

the turnover of the target enterprise did not exceed the equivalent of EUR

10 million in Poland in any of the two financial years preceding the

notification or if the merger involves entities belonging to one capital group

Poland: merger control

The UOKiK clears transactions which do not lead to a

significant restriction of competition. Otherwise, it forbids

the consolidation.

It is also possible that a merger or acquisition clearance is

subject to certain terms and conditions, for example resale

of a part of assets.

Moreover, UOKiK may clear a transaction leading to a

significant lessening of competition if it simultaneously

contributes to economic development or technical

progress or has a favorable impact on the economy.

Poland: merger control

The President of the Office may impose a fine of

up to 10 % of previous year’s revenue, if an

enterprise, even unintentionally, carries out a

merger or acquisition without obtaining the

President’s prior consent.

Furthermore, if this merger proved to have been

anticompetitive structural sanctions may be

applied.

Office for Competition and Consumer Protection:

the most recent decision blocking the merger

The Office for Competition and Consumer Protection (UOKiK)

did not agree to the merger of two leading online stores: Empik

and Merlin.pl.

According to the UOKIK the takeover of Merlin by Empik would

result in:

significant limitation of free competition on the market of books

and music.

Analysts admit that the decision will have negative

consequences for both companies.

Case study: UOKiK blocks

acquisition of Energa by PGE

Case study: UOKiK blocks

acquisition of Energa by PGE

September 16, 2010

Ministry of Treasury signed an initial agreement with

state-owned PGE (leading energy producer on polish

market) concerning sell of 84,19 % of shares of third

largest energy producer on polish market Energa

for 7,529, bln zloty.

Case study: UOKiK blocks

acquisition of Energa by PGE

After Ministry announced preliminary agreement with

PGE was obliged to apply for clearance from UOiKiK

PGE had to provide full documentation of the planned

deal, market share, future plans, ect.- everything which

would be connected with the deal.

It was done on 20

th

of October 2010.

After that UOiKiK had 3 months to analyze possible

consequences of the transaction.

Case study: UOKiK blocks

acquisition of Energa by PGE

After in-depth analysis on January 13,

2011 UOiKiK decided to not agree on

merger.

Firstly UOKiK assumed that the scope of

energy market is internal. It means polish.

There are no reasons to widen definition of

the market taking to consideration weak

international trade possibilities within next few

years.

Case study: UOKiK blocks

acquisition of Energa by PGE

Secondly after investigation of possible

consequences on energy wholesale market

UOKiK verified that combined companies will

strengthen dominating position of PGE and

essentially reduce competition on this market.

PGE will control over 40 % share of sales.

Case study: UOKiK blocks

acquisition of Energa by PGE

Thirdly there will be also negative impact on

retail market. PGE will have more than 40% of

market sales ,and one of important

competitors will cease to exist.

After examining vertical and horizontal

integrations between merged companies

UOKiK verified that transaction will seriously

restrict completion.

Trends

Economic globalisation results in growing international competition

–

thus concentration ratios must take into account international

markets

…

The pace of technological change and the pace of industrial change

has increased substantially

– this requires more frequent

adjustments by firms, including M&A.

Deregulation in a number of major industries requires industrial

realignment and readjustments. These require greater flexibility in

government policy.

New institutions, particularly among financial intermediaries,

represent new mechanisms for facilitating the restructuring

processes that are likely to continue.

Case study

Antitrust Regulations in a Global Setting:

The EU Investigation of the GE/Honeywell

Merger

Wyszukiwarka

Podobne podstrony:

03 skąd Państwo ma pieniądze podatki zus nfzid 4477 ppt

03. Zasady systemu Gabelsbergera, Czajkowski Karol 'Nauka stenografii polskiej wg systemu Gabelsberg

(03) Unia ma konstytucję Balcerowicz

rachunkowo 9c e6+ma b3ych+firm+9 03 2005 ZAXZKHJNEJNRQNPH6CYJK6ZFGEOW2TXFL73QUZA

03 skąd Państwo ma pieniądze podatki zus nfzid 4477 ppt

2013 03 19 Krab pęka, Regina ma kłopoty

03 INSTRUKCJA EPISKOPATU POLSKI W SPRAWIE DUSZPASTERSTWA MAú»EĐSTW O RO»NEJ PRZYNALE»NOŽCI KOŽCIELNE

2012 03 27 Nawet na własnej działce nie ma wolności

2019 03 14 Trwa nękanie Jaydy Fransen Ma być bezdomna lub trafi do więzienia! wPrawo

2015 10 03 Błędna decyzja urzędnika Niepełnosprawna ma oddać ponad 30 tys

2013 03 06 Piotrek nie ma rąk i nóg

2019 06 03 Płód nie ma niezależnych praw Illinois liberalizuje prawo aborcyjne Do Rzeczy

Japonia nie ma wyjścia Nasz Dziennik, 2011 03 16

Nie ma to jak hotel s 03 (2007 2008)

Sejm ma tylko uchwalić Nasz Dziennik, 2011 03 10

2019 05 03 Ks Isakowicz Zaleski Unia ma dziś wymiar antychrześcijański Do Rzeczy

więcej podobnych podstron