Wykład I

FINANSE

FINANSE PUBLICZNE

SEKTOR FINANSÓW PUBLICZNYCH

Etymologia

finire – finare- finato (łac.) = kończyć,

ograniczać

orzeczenie sądowe kończące spór

(finis), którego treścią była należność

pieniężna (financia pecuniara).

Pojęcie finansów w nauce

J. Harasimowicz: finanse to stosunki społeczne powstające

w związku z gromadzeniem i wydatkowaniem środków

pieniężnych.

L. Kurowski, uważa, że należy posługiwać się terminem

gospodarka finansowa, którą stanowi posługiwanie się

pieniądzem.

S. Bolland: zjawiska i procesy pieniężne.

M. Weralski: finanse to pieniężna forma podziału dochodu

narodowego.

Ogół zjawisk ekonomicznych związanych

z gromadzeniem i podziałem zasobów pieniężnych.

E. Ruśkowski, zjawiska związane z gromadzeniem i

wydatkowaniem środków pieniężnych.

E. Denek: finanse to proces gromadzenia i rozdziału

zasobów pieniężnych, a w potocznym rozumieniu tego

pojęcia-same zasoby pieniężne, którymi dysponują

podmioty publiczne i prywatne.

S. Owsiak: przez finanse rozumie się ogół zjawisk

pieniężnych powstających w związku z działalnością

gospodarczą i społeczną człowieka.

WNIOSKI

Finanse rozumie się zwykle jako pewien

proces, a jedynie potocznie, jako zasoby

pieniężne (czyli fundusze).

Gromadzenie i podział pieniędzy są istotą

finansów.

Zjawiska finansowe

ZJAWISKA

FINANSOWE

ZJAWISKA

PIENIĘŻNE

ZJAWISKA PIENIĘŻNE

>

ZJAWISKA FINANSOWE

CENA

ZAPŁATA

WG

OKREŚLONE

J CENY

Kwestia sporna.

Czy zjawiska pieniężne (cena, kredyt, podatek, kredyt) należą

do nauki finansów?

Klasyfikacja zjawisk

finansowych

PODMIOTOWA

(tzw. nauki finansowe)

Finanse publiczne

(finanse państwa,

samorządów i ubezpieczeń

społecznych)

Finanse banków (tzw.

bankowość)

Finanse przedsiębiorstw

Finanse ubezpieczeń

gospodarczych

Finanse międzynarodowe

Finanse gospodarstw domowych

PRZEDMIOTOWA

• Materialne (realne)

• Transferowe

(redystrybucyjne)

• Osobowe

• Opłaty za usługi

społeczne

• Kredytowe

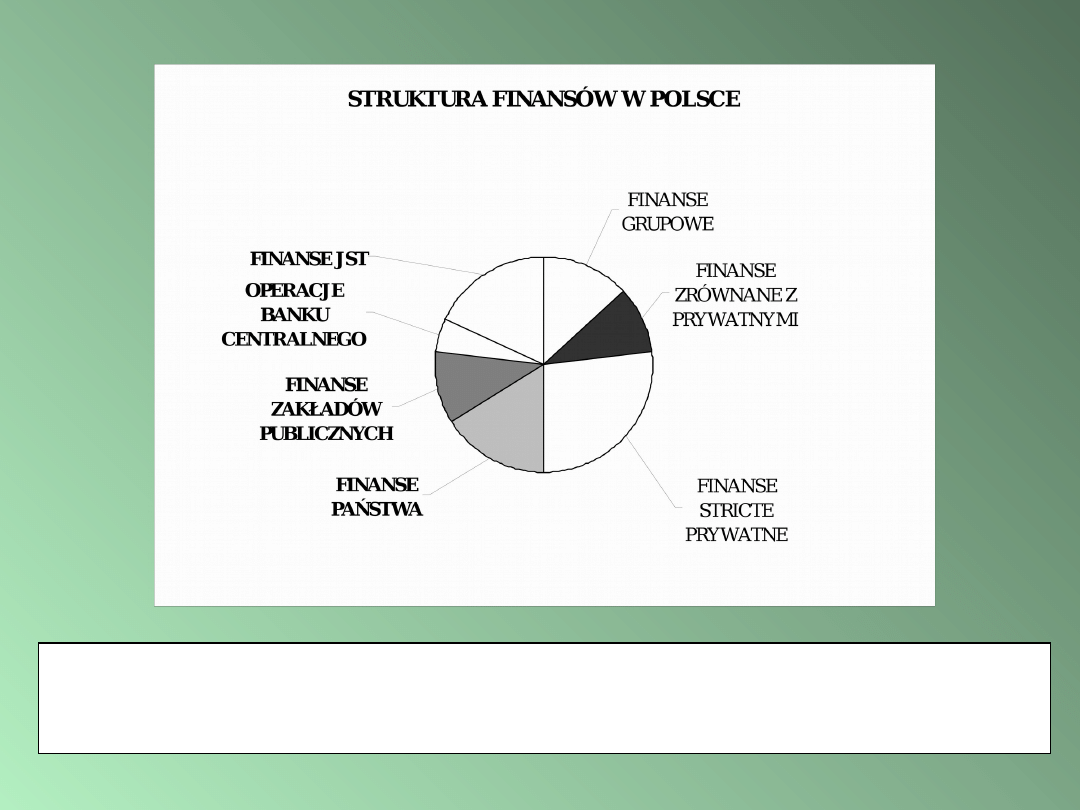

FINANSE PRYWATNE SENSU STRICTE = FINANSE OSÓB FIZYCZNYCH, PRZEDSIĘBIORCÓW I GOSPODARSTW

DOMOWYCH

FINANSE GRUPOWE = FINANSE PARTII, FUNDACJI, STOWARZYSZEŃ, KOŚCIOŁÓW

FINANSE ZRÓWNANE Z PRYWATNYMI = FINANSE PRZEDSIĘBIORSTW I BANKÓW PAŃSTWOWYCH OPRÓCZ

BANKU CENTRALNEGO

Źródło: Finanse publiczne i prawo finansowe, pod red. C. Kosikowskiego i E. Ruśkowskiego, Dom Wydawniczy ABC, Warszawa

2003, 22

.

FINANSE

sensu largo

ZASOBY

PIENIĘŻNE

np.

kwota w portfelu

(gotówka),

środki na rachunku

bankowym do bieżących

płatności (pieniądz

bezgotówkowy),

OPERACJE

ZASOBAMI

PIENIĘŻNYMI

gromadzenie, podział

<=>

dochody, wydatki

np.

zapłata podatku,

przekazanie dywidendy,

zapłata pensji

pracownikom,

SFORMALIZOWA

NE ZASADY

GROMADZENIA I

PODZIAŁU

FUNDUSZY

np.

ustawa o finansach

publicznych,

ustawa o NBP,

ustawa Prawo

bankowe,

ustawa o systemie

ubezpieczeń

społecznych

UJĘCIE

POTOCZNE

ZJAWISKA

FINANSOWE

PRAWO

FINANSOWE

FINANSE

PUBLICZNE

sensu largo

ZASOBY

PIENIĘŻNE

PUBLICZNE

np.

środki na rachunku

bankowym

jednostki budżetowej

OPERACJE

ZASOBAMI

PIENIĘŻNYMI

PUBLICZNYMI

gromadzenie, podział

<=>

dochody, wydatki

np.

zapłata podatku

wypłata emerytury

SFORMALIZOWA

NE ZASADY

GROMADZENIA I

PODZIAŁU

FUNDUSZY

PUBLICZNYCH

np.

ustawa o finansach

publicznych,

ustawa o systemie

ubezpieczeń

społecznych

UJĘCIE

POTOCZNE

ZJAWISKA

FINANSOWE

PRAWO

FINANSOWE

Finanse publiczne w UOFP art. 3

Finanse publiczne obejmują procesy związane z

gromadzeniem środków publicznych oraz ich

rozdysponowaniem, a w szczególności:

1) gromadzenie dochodów i

przychodów

publicznych;

2) wydatkowanie środków publicznych;

3)

finansowanie potrzeb pożyczkowych budżetu państwa

;

4)

finansowanie potrzeb pożyczkowych budżetu jednostki

samorządu terytorialnego;

5) zaciąganie zobowiązań angażujących środki publiczne;

6) zarządzanie środkami publicznymi;

7) zarządzanie długiem publicznym;

8)

rozliczenia z budżetem Unii Europejskiej.

Sektor publiczny a sektor finansów

publicznych

Struktura sektora finansów publicznych w

Polsce

Struktura sektora general government w Unii

Europejskiej

Finanse publiczne w Konstytucji

Finanse publiczne w ustawie o finansach

publicznych

Sektor publiczny

Sektor publiczny - definicje

Sektor publiczny można wyróżnić stosując

kryterium przedmiotu wydatków:

Sektor publiczny stanowić będą podmioty

ponoszące:

– wydatki materialne (zakup przez państwo

dóbr i usług, które realizować będą jego cele

publiczne),

– wydatki transferowe będące wyrazem

realizacji funkcji redystrybucji dochodów

(emerytury, renty, dotacje, subwencje).

S. Owsiak, Finanse publiczne. Teoria i praktyka, Wydawnictwo Naukowe PWN, Warszawa

2006, 97-99.

Sektor publiczny - definicje

Według kryterium majątkowego sektor

publiczny tworzy:

•

majątek służący władzy i administracji

państwowej,

•

majątek służący publicznym instytucjom

usługowym,

•

majątek w użytkowaniu publicznym,

•

majątek zaangażowany w działalność publiczną.

S. Owsiak, Finanse publiczne. Teoria i praktyka, Wydawnictwo Naukowe PWN, Warszawa 2006,

97-99

Sektor publiczny - definicje

Sektor publiczny albo

sektor rządowy

, to ta

część gospodarki, która dotyczy transakcji

dokonywanych przez rząd. Rząd czerpie

dochody z podatków i innych przychodów i w

ten sposób wpływa na funkcjonowanie

gospodarki przez swe własne decyzje i

wydatki inwestycyjne (wydatki rządowe), a

przez swą kontrolę (drogą polityki

monetarnej i fiskalnej) na wydatki i decyzje

inwestycyjne innych sektorów gospodarki.

Collins Reference Dictionary: Economic, Christopher Pas, Beyan Lowes

and Leslie Davies, London and Glasgow, 2000, s.439-440

.

Sektor publiczny – def.

formalna IBnGR 1999

1. Sektor publiczny tworzą podmioty i

jednostki sektora publicznego.

2. Podmiotami sektora publicznego są:

–

Skarb Państwa,

–

jednostki samorządu terytorialnego i ich

związki,

–

posiadające osobowość prawną jednostki

sektora publicznego.

E. Malinowska, W. Misiąg, A. Niedzielski, J. Pancewicz, Zakres sektora publicznego

w Polsce, IBnGR, Warszawa 1999, s. 29.

Sektor publiczny – def.

formalna IBnGR 1999 cd.

3. Jednostkami sektora publicznego są:

• jednostki budżetowe i zakłady budżetowe,

• państwowe i gminne fundusze celowe

• państwowe szkoły wyższe, państwowe wyższe szkoły

zawodowe i wyższe szkoły wojskowe,

• państwowe i komunalne instytucje kultury,

• publiczne zakłady opieki zdrowotnej i kasy chorych,

• ZUS

• KRUS

• posiadające osobowość prawną podmioty, utworzone i

działające na podstawie odrębnych ustaw, powołane w

celu wykonywania zadań publicznych, z

wyłączeniem

przedsiębiorstw, banków państwowych i spółek prawa

handlowego.

SEKTOR PUBLICZNY – ujęcie

szerokie

W najszerszym ujęciu sektor publiczny jest definiowany jako zbiór

wszystkich państwowych i komunalnych osób prawnych oraz

nie posiadających osobowości prawnej jednostek

organizacyjnych podległych organom władzy publicznej.

Wyodrębnienie sektora publicznego opiera się w tym

przypadku o kryterium własności i podległości. Powoduje

to, że do sektora publicznego można wtedy zaliczyć również

podmioty komercyjne, których większościowym udziałowcem

jest Skarb Państwa albo JST.

[PRZYKŁADY: PKO BP S.A., POCZTA POLSKA, BANK

GOSPODARSTWA KRAJOWEGO, PKP, PKS, PAŃSTWOWE

GOSPODARSTWO LEŚNE „LASY PAŃSTWOWE]

W. Misiąg, Finanse publiczne w Polsce.

Sektor publiczny – def.

formalna IBnGR 1999 cd.

• Zaletą takiego szerokiego podejścia, jest ukazanie pełnego zakresu

obecności państwa w gospodarce, w której jest ono właścicielem i

zarządca części sfery komercyjnej.

• Wadą szerokiego ujęcia sektora publicznego jest to, że składające się

nań podmioty mają różne cele i działają na odmiennych zasadach.

• Aby ograniczyć zakres sektora publicznego można przyjąć, że

stanowią go następujące podmioty: Państwowe i samorządowe

instytucje i jednostki organizacyjne finansowane głównie ze

środków Skarbu Państwa i JST, wykonujące na zasadach

niekomercyjnych zadania publiczne.

• Takie podejście eliminuje z zakresu sektora publicznego

przedsiębiorstwa państwowe oraz spółki prawa handlowego

(chociaż niektóre z tych ostatnich mają publiczny charakter np.: PAP

S.A., Agencja Rozwoju Przemysłu S.A., Państwowa Agencja Inwestycji

Zagranicznych S.A.) co pozwala bardziej precyzyjnie określić zakres

sektora publicznego

.

ESA 95

European System of National and Regional Accounts

Europejski System Rachunków Narodowych i Regionalnych

General government (S.13)

2.68 .

Definition:

The sector general government (S.13) includes all institutional units which are other non-market producers (see

= other non-market producers are local KAUs [kind of activity unit] or institutional units

whose major part of output is provided free or at not economically significant prices)

whose output is intended for individual and collective consumption, and mainly financed by compulsory

payments made by units belonging to other sectors, and/or all institutional units principally engaged in the

redistribution of national income and wealth.

2.69 . The institutional units included in sector S.13 are the following:

a) general government entities (excluding public producers organised as public corporations or, by virtue of

special legislation, recognised as independent legal entities, or quasi-corporations, when any of these are

classified in the non-financial or financial sectors) which administer and finance a group of activities,

principally providing non-market goods and services, intended for the benefit of the community

;

b) non-profit institutions recognised as independent legal entities which are other non-market producers and

which are controlled and mainly financed by general government;

c) autonomous pension funds if the two requirements of paragraph

. are met.

2.70 . The general government sector is divided into four sub-sectors:

a) central government (S.1311);

b) state government (S.1312);

c) local government (S.1313);

d) social security funds (S.1314).

http://circa.europa.eu/irc/dsis/nfaccount/info/data/esa95/en/een00080.htm#0002c4dc

•

ESA 95

European System of National and Regional Accounts

Europejski System Rachunków Narodowych i Regionalnych

Sektor władz publicznych obejmuje jednostki instytucjonalne, których efekty

działalności są przeznaczone do spożycia indywidualnego i zbiorowego

na

zasadach nierynkowych

, a koszty działalności są finansowane

głównie z obowiązkowych świadczeń przekazywanych przez inne

sektory, których podstawowym zadaniem jest redystrybucja dochodu

narodowego.

Jednostkami instytucjonalnymi sektora władz publicznych są:

jednostki władz publicznych, które administrują i finansują działalność

polegającą głównie na dostarczaniu nierynkowych towarów i usług

przeznaczonych głównie na zaspokojenie potrzeb społeczeństwa;

jednostki niekomercyjne, uznane za osoby prawne, kontrolowane i

finansowane głównie przez władze publiczne.

Sektor władz publicznych tworzą:

– sektor centralnych władz publicznych,

– sektor władz publicznych sfederowanych,

– sektor lokalnych władz publicznych,

– sektor funduszy zabezpieczenia społecznego.

OECD

• The public sector comprises the general

government sector plus all public

corporations including the central bank.

• Sektor publiczny obejmuje sektor rządowy

oraz wszystkie korporacje publiczne, w

tym bank centralny.

OECD, 1997, Measuring Public Employment in OECD Countries: Sources, Methods and

Results, OECD, Paris

UNECE - United Nations Economic Commission for

Europe Europejska Komisja Gospodarcza

Public sector comprises the sub-sectors of general government

(mainly central, state and local government units together with

social security funds imposed and controlled by those units) as

well as public corporations, ie corporations that are subject to

control by government units (usually defined by the government

owning the majority of shares).

Sektor publiczny obejmuje subsektor rządowy (złożony głównie z

sektora centralnego, regionalnego i lokalnego wraz z

funduszami zabezpieczenia społecznego, pozostającymi w

jurysdykcji tych podmiotów) oraz korporacji publicznych, tj.

takich które funkcjonują pod nadzorem jednostek rządowych

(zwykle są one definiowane, jako podmioty w których władze

dysponują większością udziałów.

Public sector - Wikipedia

The public sector is the part of economic and administrative life that deals with the delivery of goods and

, whether national,

or

.

Sektor publiczny stanowi formę ekonomicznej i administracyjnej aktywności, w ramach której są

dostarczane dobra i usługi ,dzięki i na rzecz władz, zarówno centralnych, regionalnych jak i

lokalnych.

Examples of public sector activity range from delivering

and

.

The organization of the public sector (

) can take several forms, including:

Direct administration funded through

; the delivering organization generally has no specific

requirement to meet

success criteria, and production decisions are determined by government.

(in some contexts, especially manufacturing, "

"); which

differ from direct administration in that they have greater commercial freedoms and are expected to operate

according to commercial criteria, and production decisions are not generally taken by government (although

goals may be set for them by government).

Partial

(of the scale many businesses do, e.g. for IT services), is considered a public sector model.

or contracting out, with a privately owned corporation delivering the entire service on

behalf of government. This may be considered a mixture of private sector operations with public ownership of

assets, although in some forms the private sector's control and/or risk is so great that the service may no

longer be considered part of the public sector. (See Britain's

.)

In spite of their name,

are not part of the public sector; they are a particular kind of

company that can offer their shares for sale to the general public.

The decision about what are proper matters for the public sector as opposed to the private sector is probably the

single most important dividing line among

with (broadly) socialists preferring greater state involvement, libertarians favoring minimal state involvement,

and conservatives and liberals favouring state involvement in some aspects of the society but not others.

•

http://en.wikipedia.org/wiki/Public_sector

Typowe wyłączenia podmiotowe z

zakresu sektora publicznego w krajach

Unii Europejskiej

• przedsiębiorstwa państwowe, korzystające z

subsydiów,

• szkoły niepubliczne (w tym również

dotowane),

• spółki obsługujące podmioty sektora

publicznego.

Konsorcja celowe - Public – Private –

Partnership?

kwestia sporna

Sektor publiczny a finanse

publiczne -

różnice

• Sektor publiczny wytwarza dobra i usługi

• Finanse publiczne reprezentują zjawiska

i procesy pieniężne

• W sektorze publicznym dominujące

znacznie ma majątek (metoda zasobowa)

• W analizie finansów publicznych

charakterystyczna jest metoda

strumieniowa. Okresem analizy jest

zwykle rok (periodyczność dochodów i

wydatków).

Sektor publiczny a finanse

publiczne -

różnice

• Tylko część sektora publicznego

realizuje cele publiczne i społeczne;

część sektora realizuje cele

ekonomiczne/komercyjne

(przedsiębiorstwa państwowe i

samorządowe).

• Nie całość środków publicznych jest

wykorzystywana przez sektor

publiczny (emerytury, renty zasiłki).

Sektor publiczny a finanse

publiczne -

różnice

• Majątek publiczny stanowi

zabezpieczenie długu publicznego.

• Środki publiczne finansują obsługę

długu publicznego.

WNIOSEK

Bez finansów publicznych sektor

publiczny nie może funkcjonować.

Sektor finansów publicznych

Sektor finansów publicznych

Sektor finansów publicznych

SEKTOR PUBLICZNY

=

SEKTOR FINANSÓW PUBLICZNYCH

=

FINANSE

PUBLICZNE

USTAWA O FINANSACH PUBLICZNYCH

BRAK DEF.

NORMATYWNEJ!

SFP -1998

Art. 5. 1. Do sektora finansów publicznych zalicza się:

1) organy władzy publicznej i podległe im jednostki

organizacyjne,

2) państwowe osoby prawne oraz inne państwowe jednostki

organizacyjne nie objęte Krajowym Rejestrem Sądowym,

których działalność jest finansowana ze środków

publicznych w całości lub części, z wyjątkiem:

a) przedsiębiorstw państwowych,

b) banków państwowych,

c) spółek prawa handlowego.

2. Sektor finansów publicznych dzieli się na:

1) sektor rządowy,

2) sektor samorządowy, obejmujący jednostki samorządu

terytorialnego i ich organy oraz podległe tym organom

jednostki organizacyjne

Sektor finansów publicznych w UOFP art.4

1) organy władzy publicznej, w tym organy administracji rządowej,

organy kontroli

państwowej i ochrony prawa, sądy i trybunały;

2) gminy, powiaty i samorząd województwa, zwane dalej „jednostkami

samorządu

terytorialnego”, oraz ich związki;

3) jednostki budżetowe, zakłady budżetowe i gospodarstwa

pomocnicze jednostek

budżetowych;

4) państwowe i samorządowe fundusze celowe;

5) państwowe szkoły wyższe;

6) jednostki badawczo-rozwojowe;

7) samodzielne publiczne zakłady opieki zdrowotnej;

8) państwowe i samorządowe instytucje kultury;

9) Zakład Ubezpieczeń Społecznych, Kasa Rolniczego Ubezpieczenia

Społecznego i zarządzane przez nie fundusze;

10) Narodowy Fundusz Zdrowia;

11) Polska Akademia Nauk i tworzone przez nią jednostki

organizacyjne;

12) inne państwowe lub samorządowe osoby prawne utworzone na

podstawie odrębnych ustaw w celu wykonywania zadań publicznych,

z wyłączeniem przedsiębiorstw, banków i spółek prawa

handlowego.

Podsektory finansów

publicznych

RZĄDOWY obejmujący organy władzy publicznej, organy

kontroli państwowej i ochrony prawa, sądy i trybunały, organy

administracji rządowej, Polską Akademię Nauk i tworzone

przez nią jednostki organizacyjne oraz jednostki wymienione

w ust. 1 pkt 3-8, 10 i 12, dla których organem

założycielskim lub nadzorującym jest organ administracji

rządowej albo inna jednostka zaliczana do podsektora

rządowego;

SAMORZĄDOWY obejmujący jednostki samorządu

terytorialnego, ich organy oraz związki i jednostki

organizacyjne wymienione w ust. 1 pkt 3, 4, 7, 8 i 12, dla

których organem założycielskim lub nadzorującym jest

jednostka samorządu terytorialnego;

UBEZPIECZEŃ obejmujący jednostki wymienione w ust. 1

pkt 9.

SEKTOR FINANSÓW PUBLICZNYCH - SCHEMAT

Organy władzy publicznej, organy administracji rządowej, organy

kontroli państwowej i ochrony prawa, sądy i trybunały a także jednostki

samorządu terytorialnego

i ich organy oraz związki

Formy organizacyjno-

prawne jednostek sektora

finansów publicznych

- jednostki budżetowe,

- zakłady budżetowe,

- gospodarstwa pomocnicze

jednostek

budżetowych,

- fundusze celowe.

Ubezpieczenia społeczne

ZUS+fundusze,

KRUS+fundusze,

Narodowy Fundusz Zdrowia,

samodzielne publiczne zakłady

opieki zdrowotnej.

INNE

•Państwowe Szkoły Wyższe

• jednostki badawczo rozwojowe,

•PAN i jej jednostki organizacyjne,

•państwowe lub samorządowe osoby prawne utworzone na podstawie odrębnych ustaw w celu

wykonania zadań publicznych (np. AGENCJE PUBLICZNE)

•państwowe lub samorządowe instytucje kultury (teatry, opery, operetki, filharmonie, kina

PODMIOTY WYŁĄCZONE

przedsiębiorstwa (państwowych)

banków (państwowych)

spółek prawa handlowego

Organy władzy publicznej

SEJM

SENAT

PREZYDENT RP

RADA MINISTRÓW

Organy kontroli państwowej i ochrony prawa sądy i

trybunały

NIK

RPO

PiP

GIDO KRRiT NSA

TK

SN

Jednostki samorządu terytorialnego i ich organy oraz

związki

GMINY

, POWIATY

WOJEWÓDZTWA

ZWIĄZKI GMIN

PAŃSTWOWE

Fundusz Ubezpieczeń Społecznych,

Fundusz Emerytalno - Rentowy KRUS,

Fundusz Prewencji i Rehabilitacji,

Fundusz Administracyjny,

Fundusz Pracy,

Fundusz Gwarantowanych Świadczeń Pracowniczych,

Państwowy Fundusz Kombatantów,

Narodowy Fundusz Ochrony Środowiska i Gospodarki

Wodnej,

Centralny Fundusz Ochrony Gruntów Rolnych,

Państwowy Fundusz Gospodarki Zasobem Geodezyjnym i

Kartograficznym,

Fundusz Promocji Twórczości,

Fundusz Nauki i Technologii Polskiej,

Fundusz Zajęć Sportowo-Rekreacyjnych dla Uczniów,

Fundusz Rozwoju Kultury Fizycznej,

Fundusz Promocji Kultury,

Fundusz Reprywatyzacji,

Fundusz Restrukturyzacji Przedsiębiorców,

Fundusz Skarbu Państwa,

Fundusz Wsparcia Policji,

Fundusz Modernizacji Bezpieczeństwa Publicznego,

Fundusz – Centralna Ewidencja Pojazdów i Kierowców,

Fundusz Pomocy Postpenitencjarnej,

Fundusz Rozwoju Przywięziennych Zakładów Pracy,

Fundusz Modernizacji Sił Zbrojnych,

Państwowy Fundusz Rehabilitacji i Osób

Niepełnosprawnych.

SAMORZĄDOWE

GMINNE, POWIATOWE,

WOJEWÓDZKIE

oPowiatowe i gminne

Fundusze Ochrony

Środowiska i Gospodarki

Wodnej

oWojewódzkie, powiatowe i

gminne Fundusze

Gospodarki Zasobem

Geodezyjnym i

Kartograficznym,

oNarodowy Fundusz

Rewaloryzacji Zabytków

Krakowa

Fundusze celowe

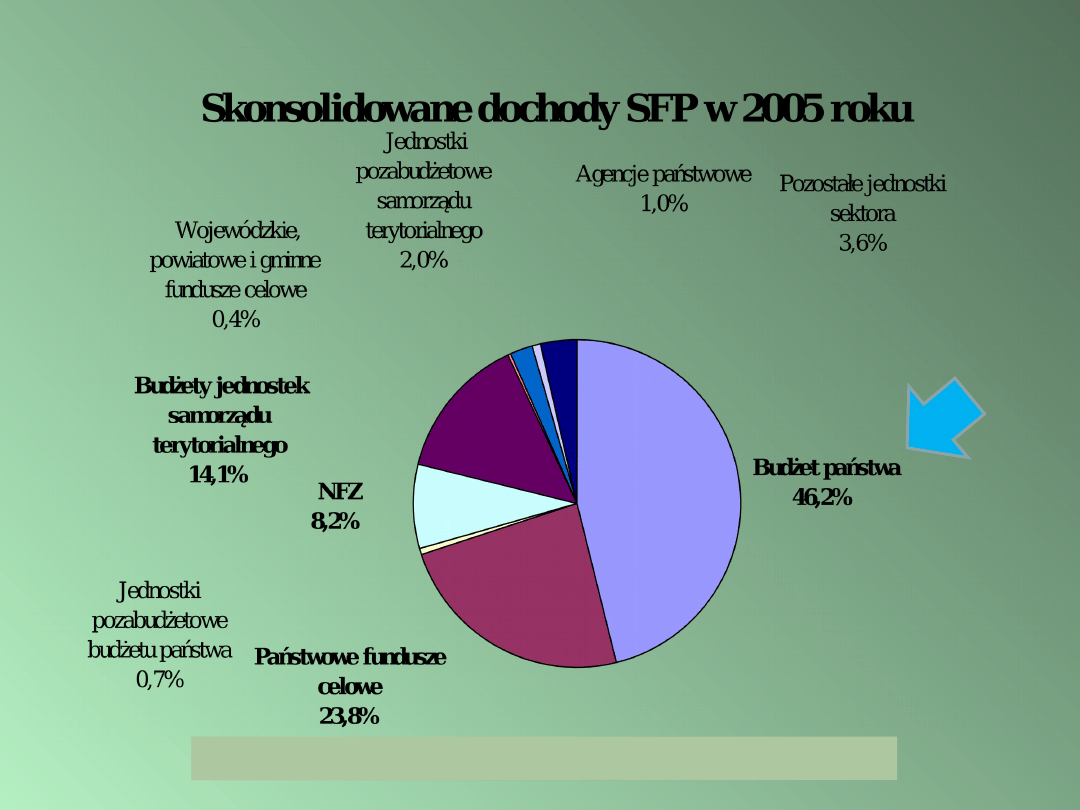

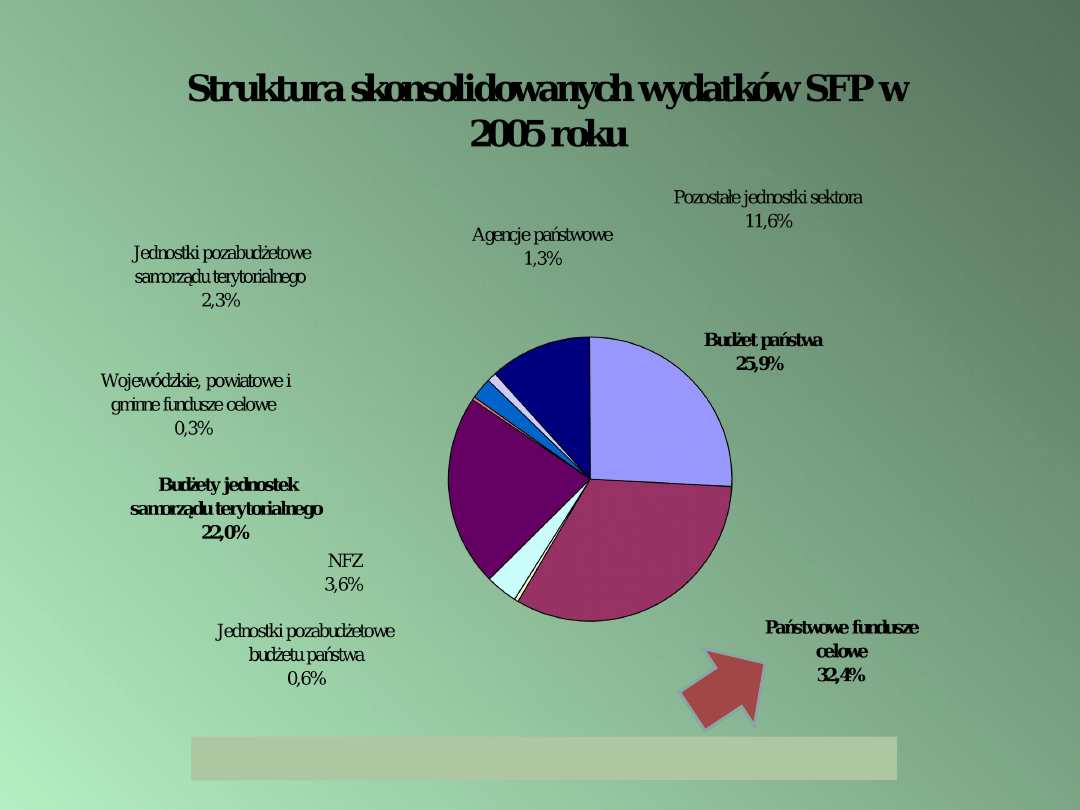

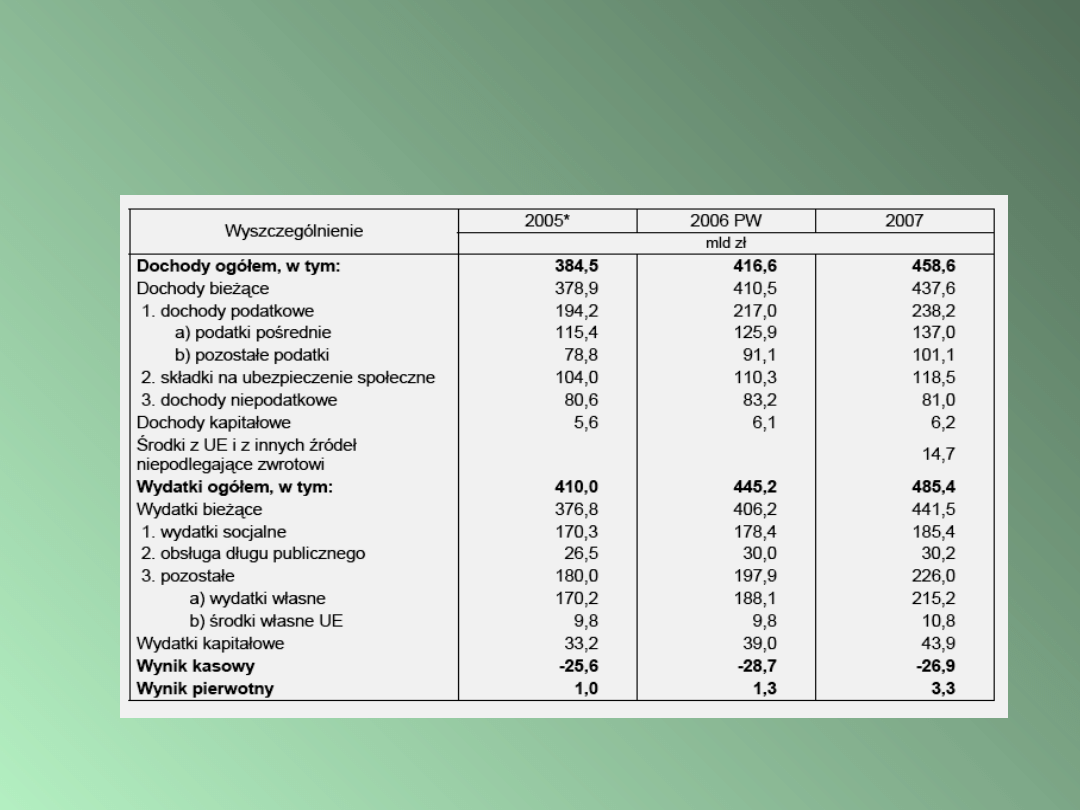

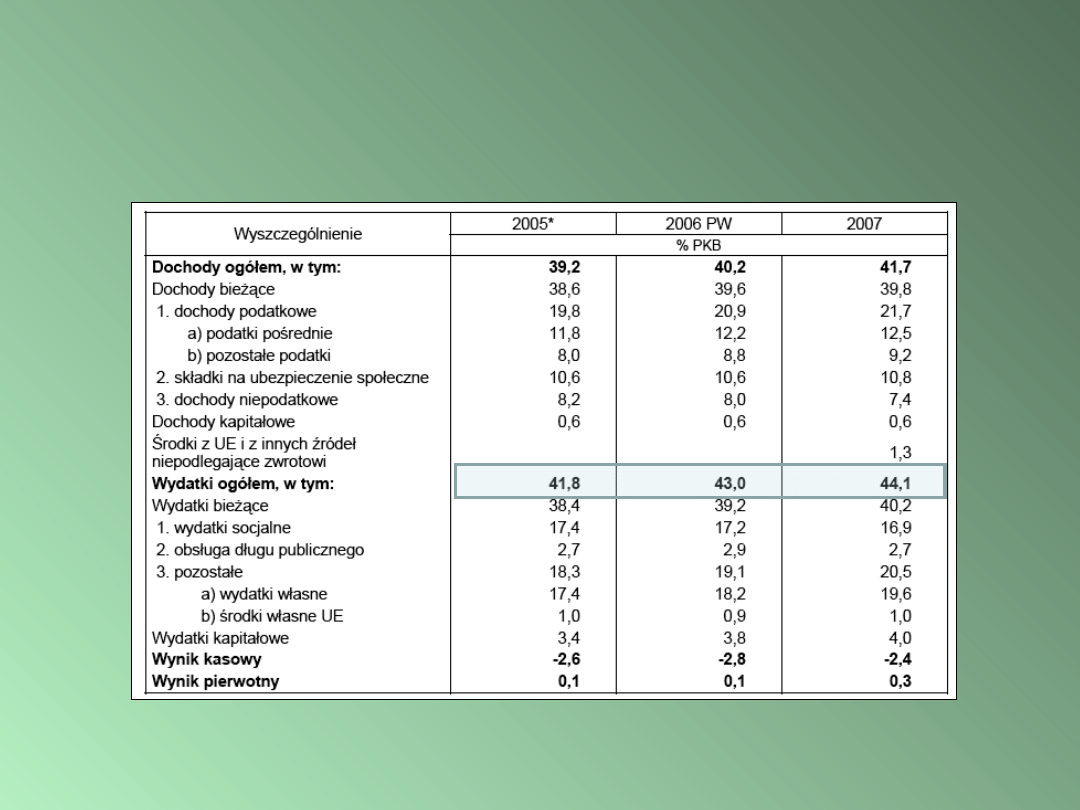

348,5 mld zł = 39,2 % PKB

410 mld zł = 41,8 % PKB

Skonsolidowane dochody i

wydatki SFP w ujęciu

rodzajowym - lata 2005-2007

Źródło: Uzasadnienie do ustawy budżetowej na 2007 rok, rozdz. IX, s.13.

Skonsolidowane dochody i wydatki

SFP w ujęciu rodzajowym - lata

2005-2007 (% PKB)

Źródło: Uzasadnienie do ustawy budżetowej na 2007 rok, rozdz. IX, s.13.

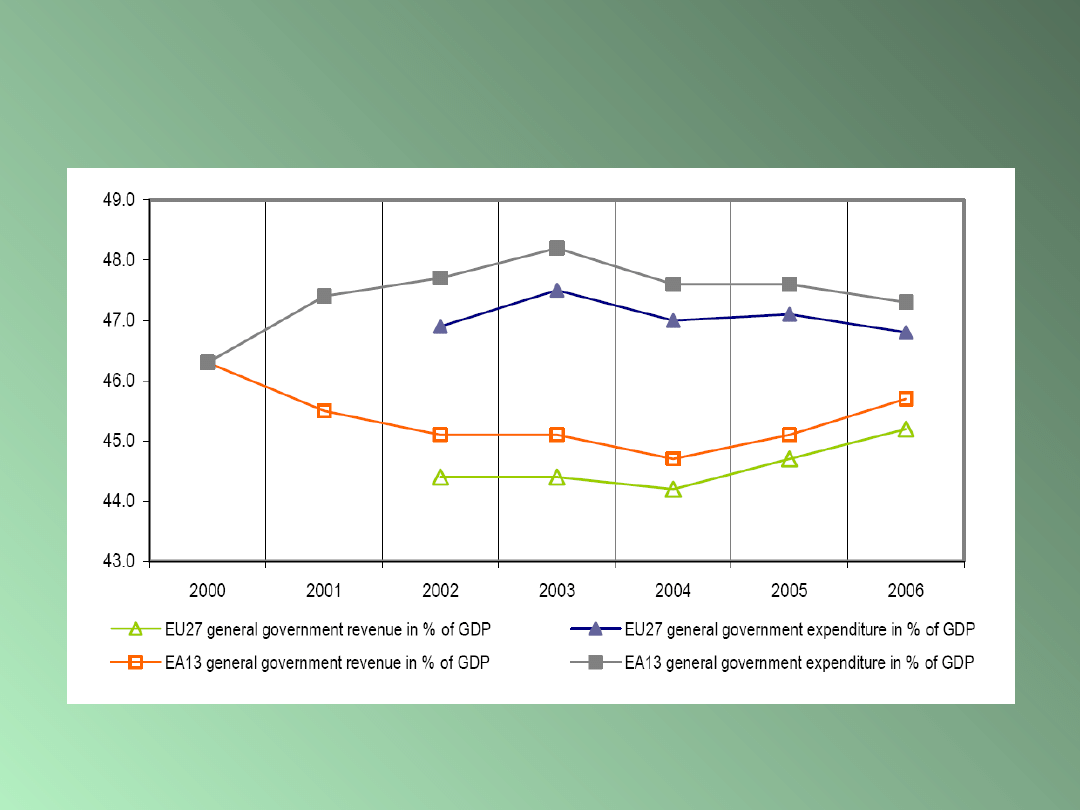

Zakres sektora general

government w Unii

Europejskiej

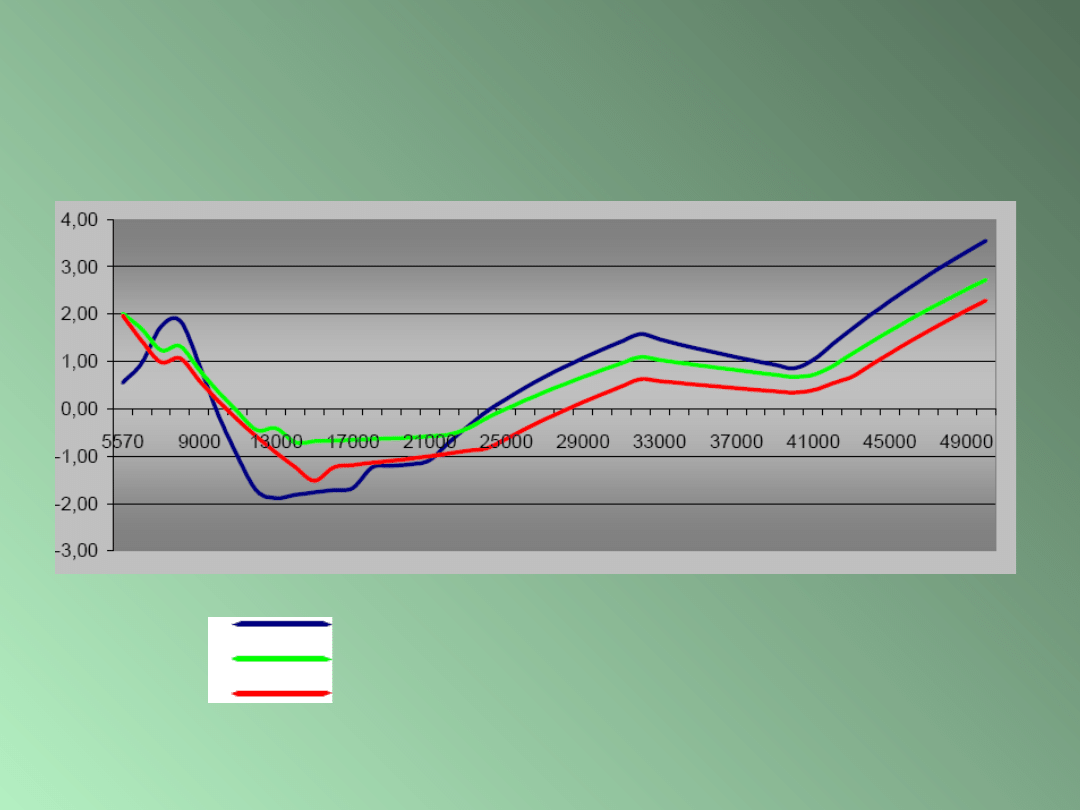

Dochody i wydatki rządowe jako %

PKB w latach 2000-2006

Anne Paternoster ,Monika Wozowczyk, Alessandro Lupi ,General government expenditure and revenue in the EU,

2006, Eurostat 2008, s. 1.

http://epp.eurostat.ec.europa.eu/cache/ITY_OFFPUB/KS-SF-08-023/EN/KS-SF-08-023-EN.PDF

http://epp.eurostat.ec.europa.eu/cache/ITY_OFFPUB/KS-SF-08-054/EN/KS-SF-08-054-EN.PDF

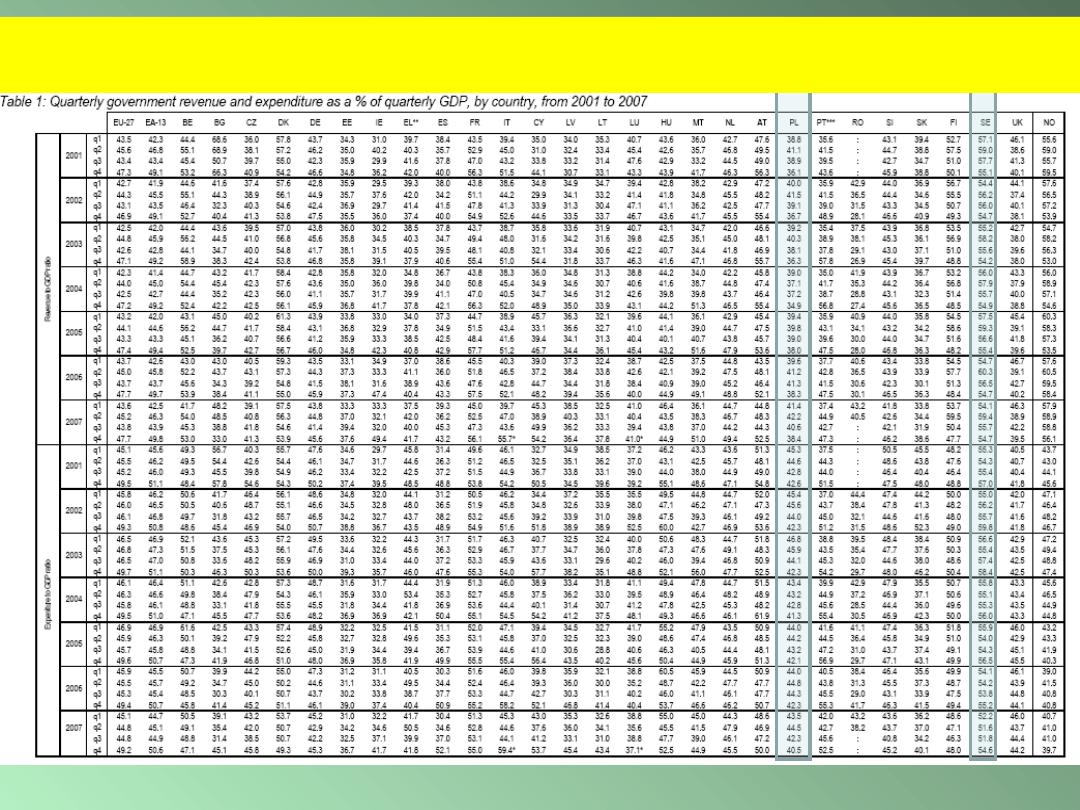

Dochody i wydatki sektora rządowego w UE-27 w latach 2001-2007

wg kwartałów

http://ec.europa.eu/economy_finance/indicators/general_government_data/2007/ggd01_112007en.pdf

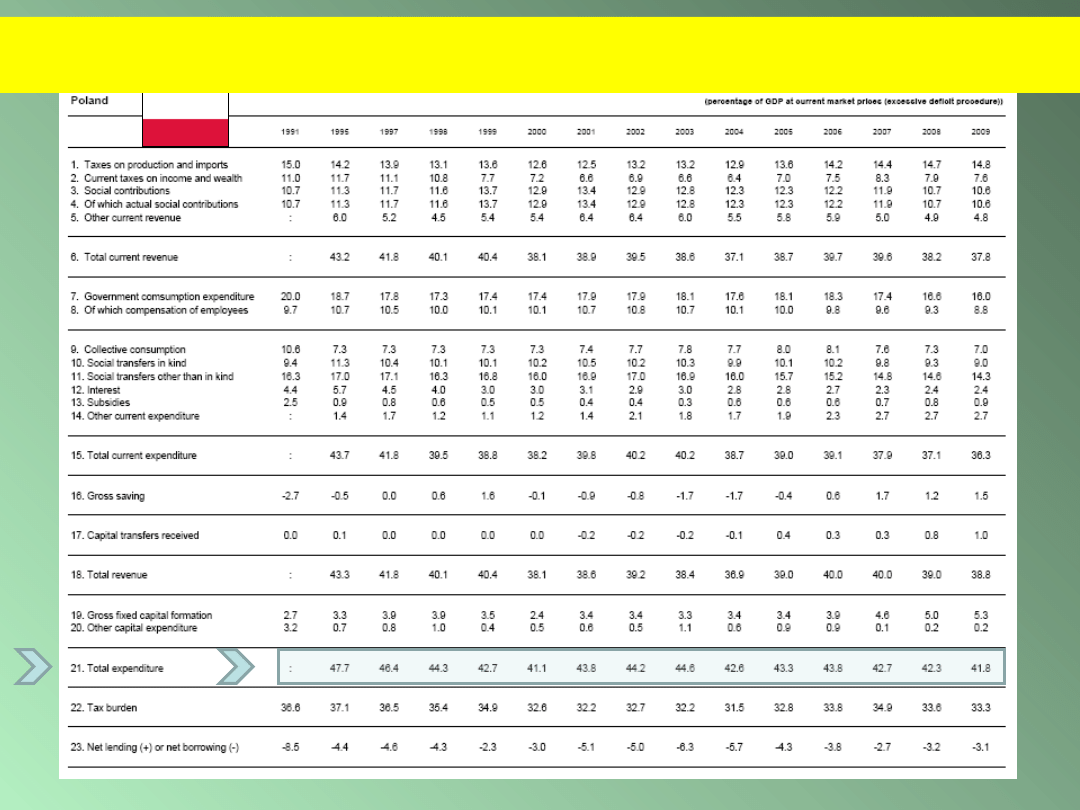

Dochody i wydatki sektora rządowego w Polsce w latach 1991-2008

(%PKB)

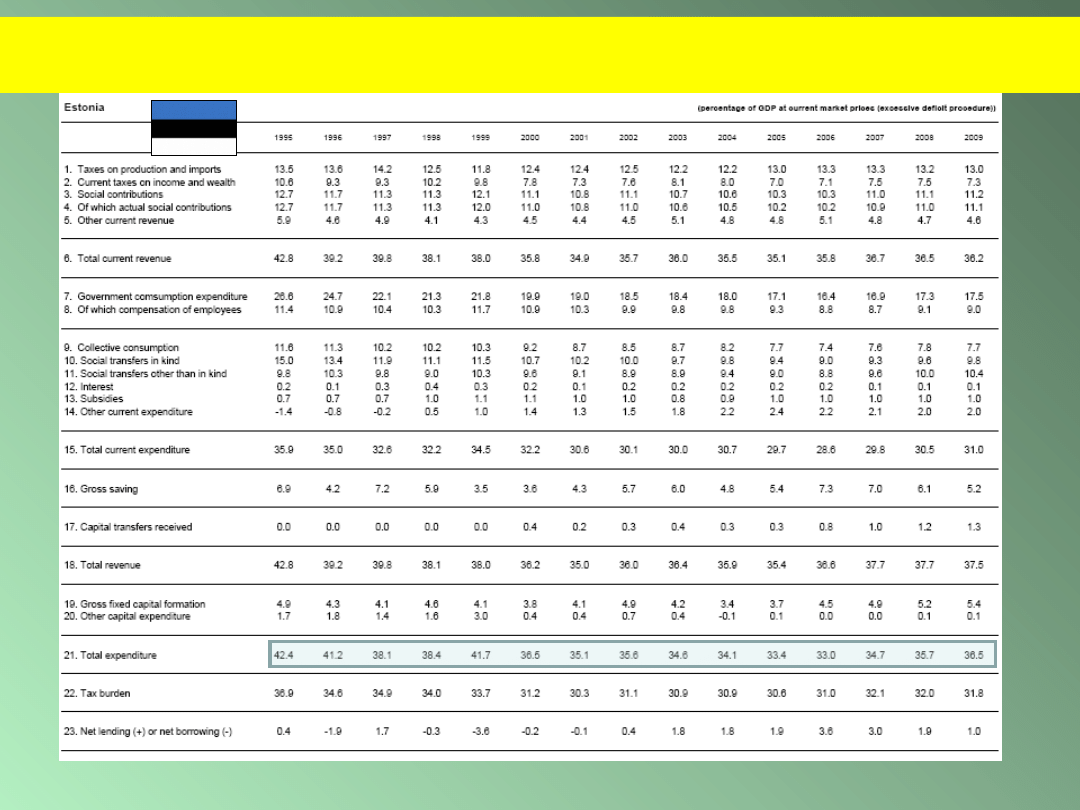

Dochody i wydatki sektora rządowego w Estonii w latach 1995-2008

(%PKB)

http://ec.europa.eu/economy_finance/indicators/general_government_data/2007/ggd01_112007en.pdf

http://epp.eurostat.ec.europa.eu/cache/ITY_OFFPUB/KS-SF-08-054/EN/KS-SF-08-054-EN.PDF

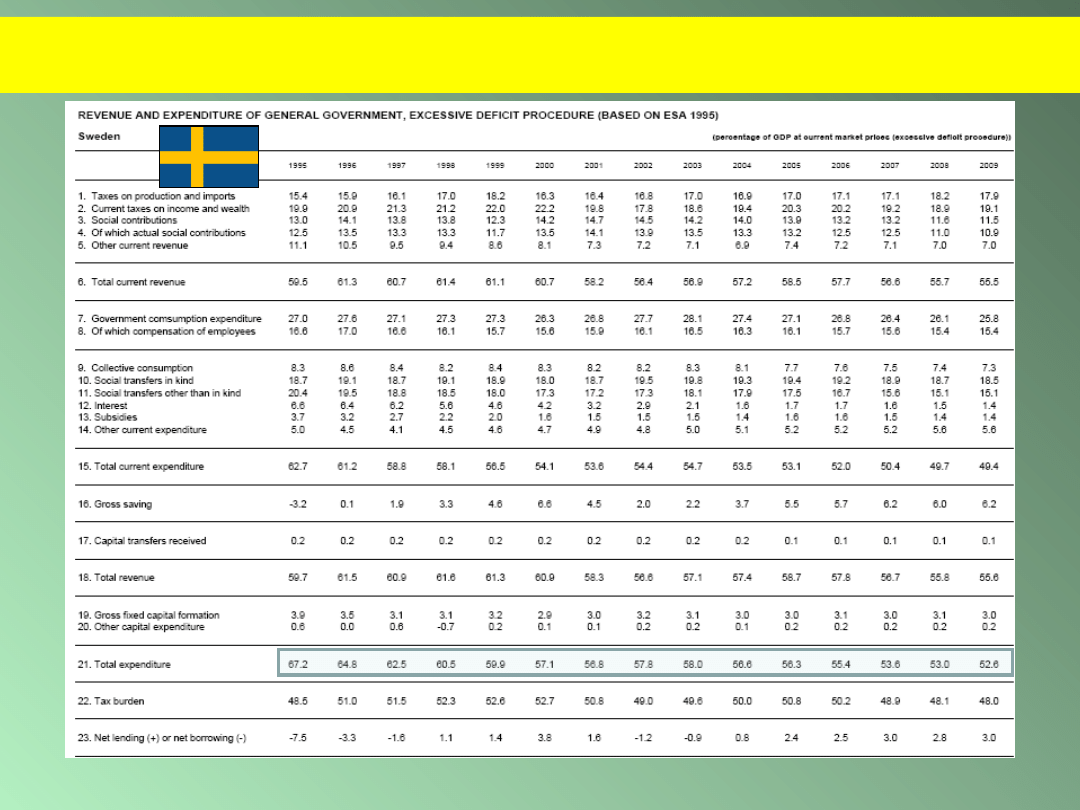

Dochody i wydatki sektora rządowego w Szwecji w latach 1996-2008

(%PKB)

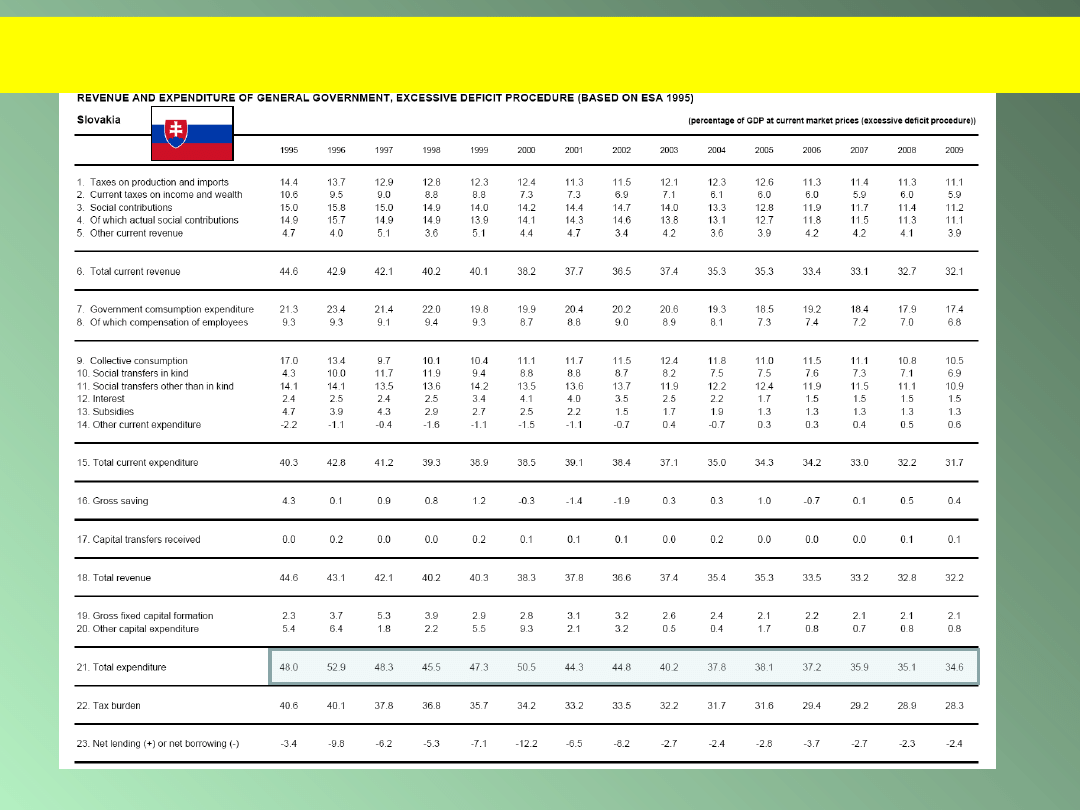

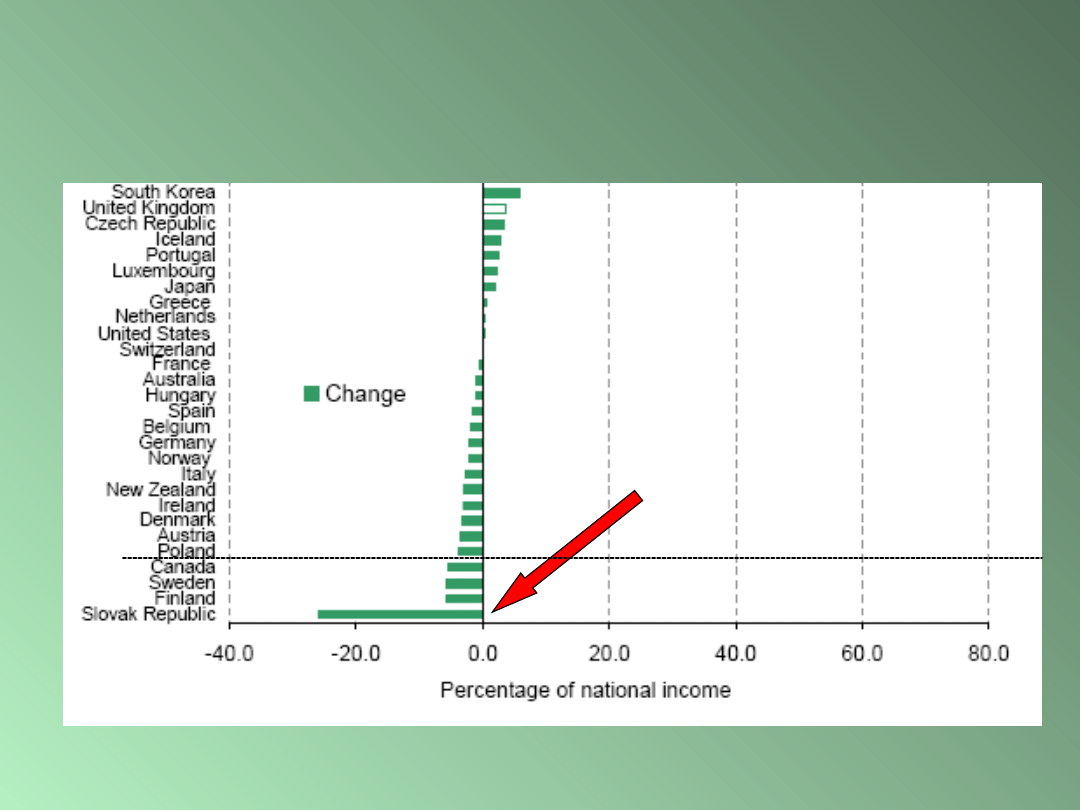

Dochody i wydatki sektora rządowego na Słowacji w latach 1995-

2008 (%PKB)

Podatki w Słowacji jako procent PKB

w latach 2003-2009*

Wyszczególnienie

200

3

200

4

200

5

200

6

200

7

200

8

200

9

A. Dochody rządowe ogółem

35,

7

34,3

37,0

36,0

34,8

34,2

34,2

Dochody podatkowe razem, w

tym:

17,

8

17,4

18,4

17,1

17,1

17

17

1. Podatki bezpośrednie razem

6,8

5,3

5,7

5,7

5,5

5,7

5,9

1.1. podatek dochodowy od osób fiz.

3,3

2,5

2,7

2,6

2,6

2,7

2,8

- podatek dochodowy od płac

2,9

2,2

2,3

2,2

2,2

2,4

2,5

- podatek dochodowy od

samozatrudnionych

0,3

0,3

0,4

0,4

0,4

0,4

0,4

1.2. podatek dochodowy od

os.prawnych

2,8

2,3

2,8

2,8

2,7

2,8

2,9

1.3. podatek od dochodów

kapitałowych

0,7

0,4

0,3

0,3

0,2

0,2

0,2

2. podatki pośrednie

9,7

11,1

11,7

10,5

7,9

7,8

7,7

2.1. podatek od wartości dodanej

6,6

7,8

8,0

7,6

7,5

7,4

7,4

2.2. podatek akcyzowy

3,1

3,3

3,7

2,9

0,4

0,4

0,3

B. Wydatki rządowe ogółem

39,

0

38,0

39,2

38,3

36,6

35,4

34,9

*Prognoza na lata 2007-2009

Źródła: Opracowanie własne na podstawie danych z raportów MFW z lat 2005-2007; www.imf.org

Kto zyskał kto stracił na reformie

podatkowej

w Słowacji

Wpływ słowackiej reformy podatkowej na miesięczny dochód brutto

osoba samotna, bez dzieci,

para pracująca, jedno dziecko,

para pracująca, dwoje dzieci

.

Źródło: P. Goliaš, R. Kičina, Slovak tax reform: one year after, INEKO – Institute for Economic and Social Reforms,

2005, s. 13, http://www.ineko.sk/reformy2003/menu_dane_paper_golias.pdf

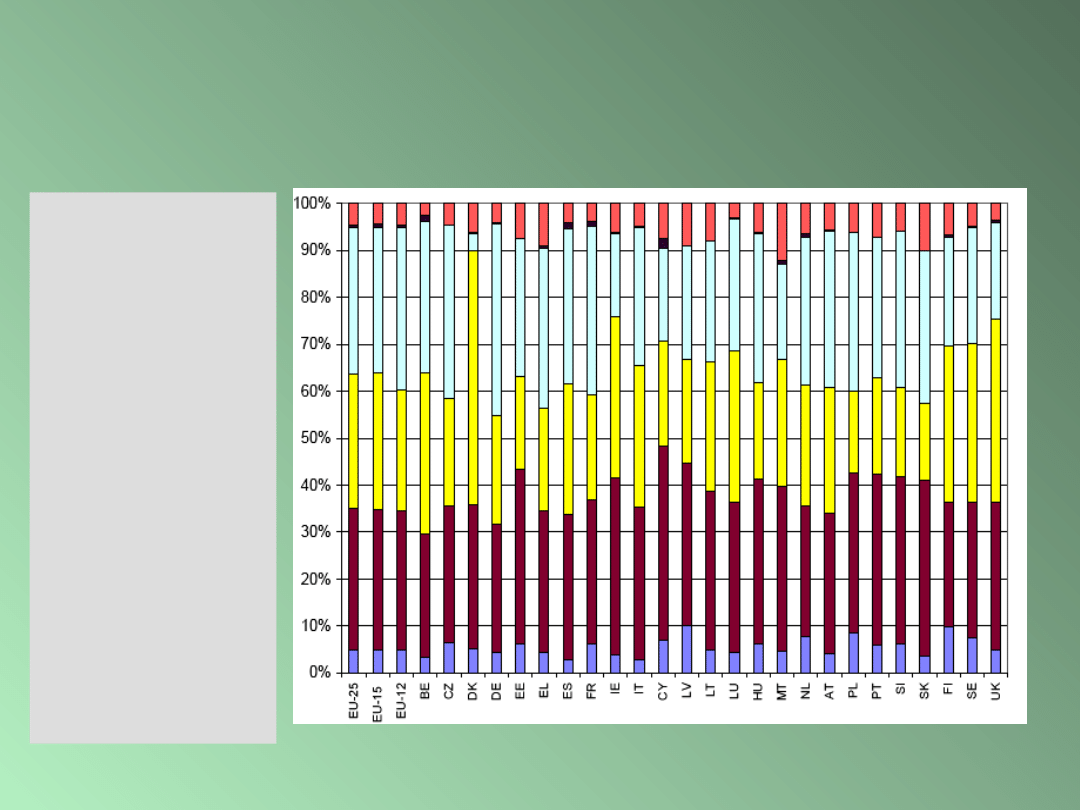

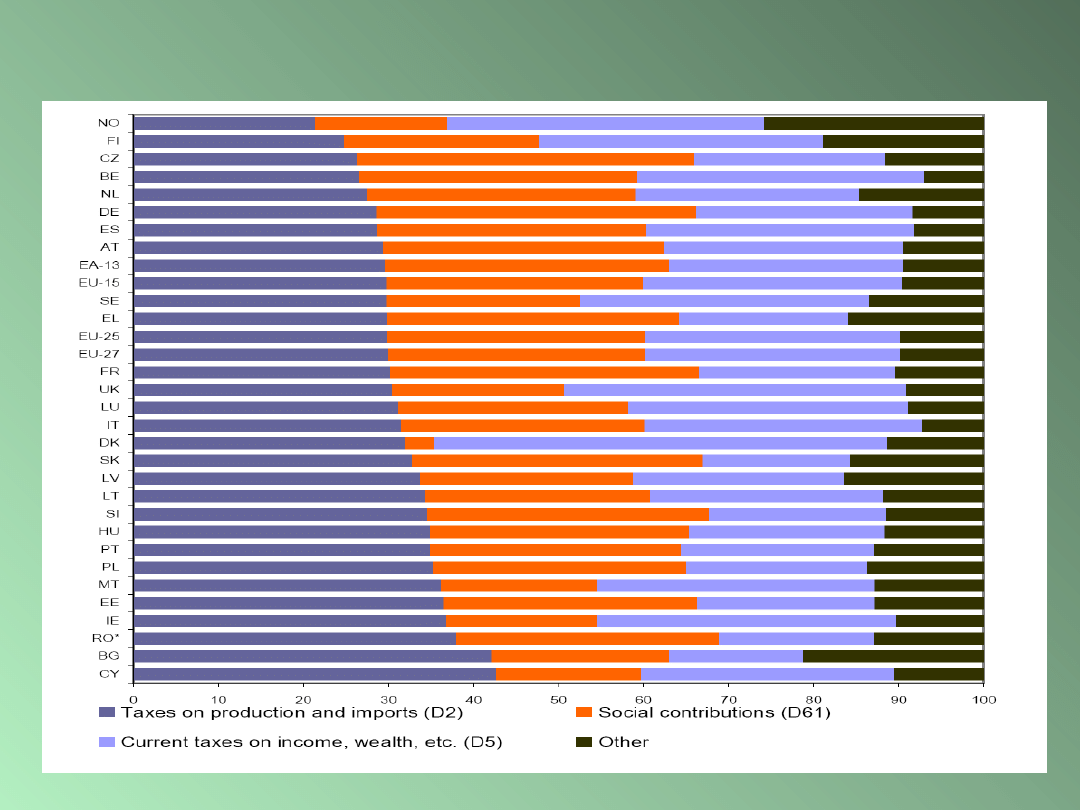

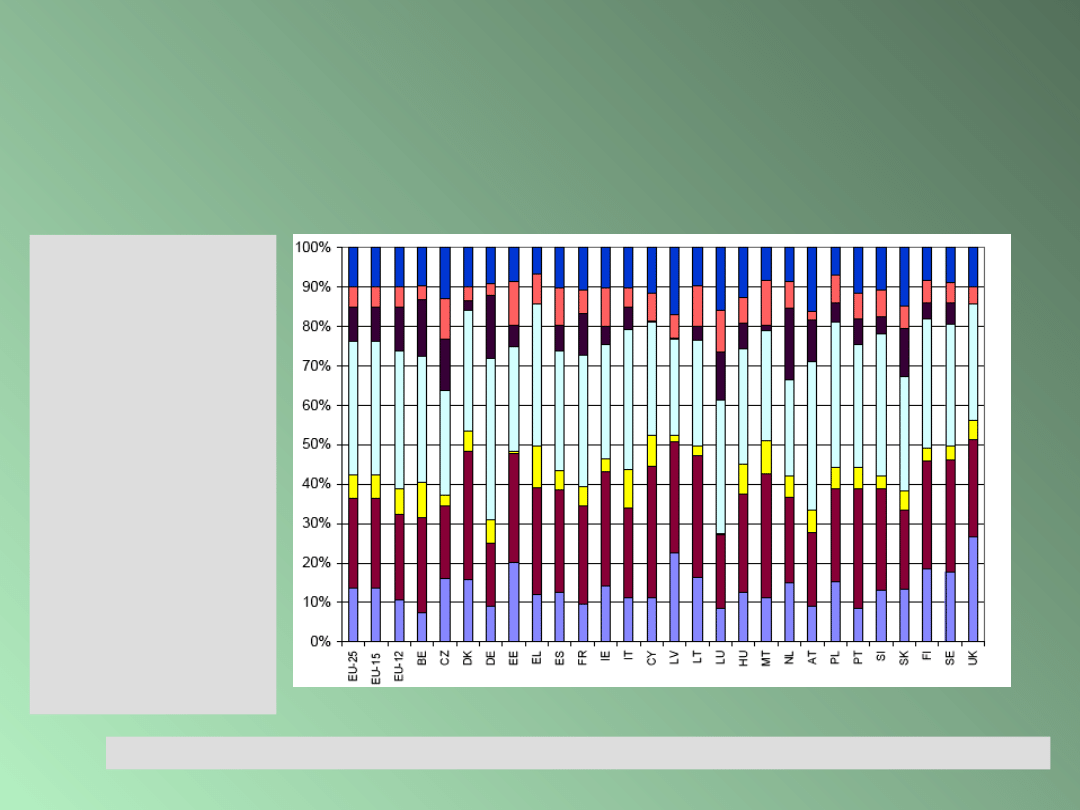

Główne składniki dochodów

publicznych w UE-25 w 2005

roku

Ivana Yablonska, General government

expenditure

and revenue 2005 data, Eurostat 2006, s. 4.

Inne

Podatki od

kapitału

Składki

ubezpieczeni

owe

Podatki

dochodowe

Podatki od

konsumpcji

Dochody

rynkowe

Główne składniki dochodów

publicznych w UE-27 w latach

2000-2007

http://epp.eurostat.ec.europa.eu/cache/ITY_OFFPUB/KS-SF-08-054/EN/KS-SF-08-054-EN.PDF

European System of National and

Regional Accounts (ESA 95)

CHAPTER 4 DISTRIBUTIVE

TRANSACTIONS

http://circa.europa.eu/irc/dsis/nfaccount/info/data/esa95/en/esa95en

.htm

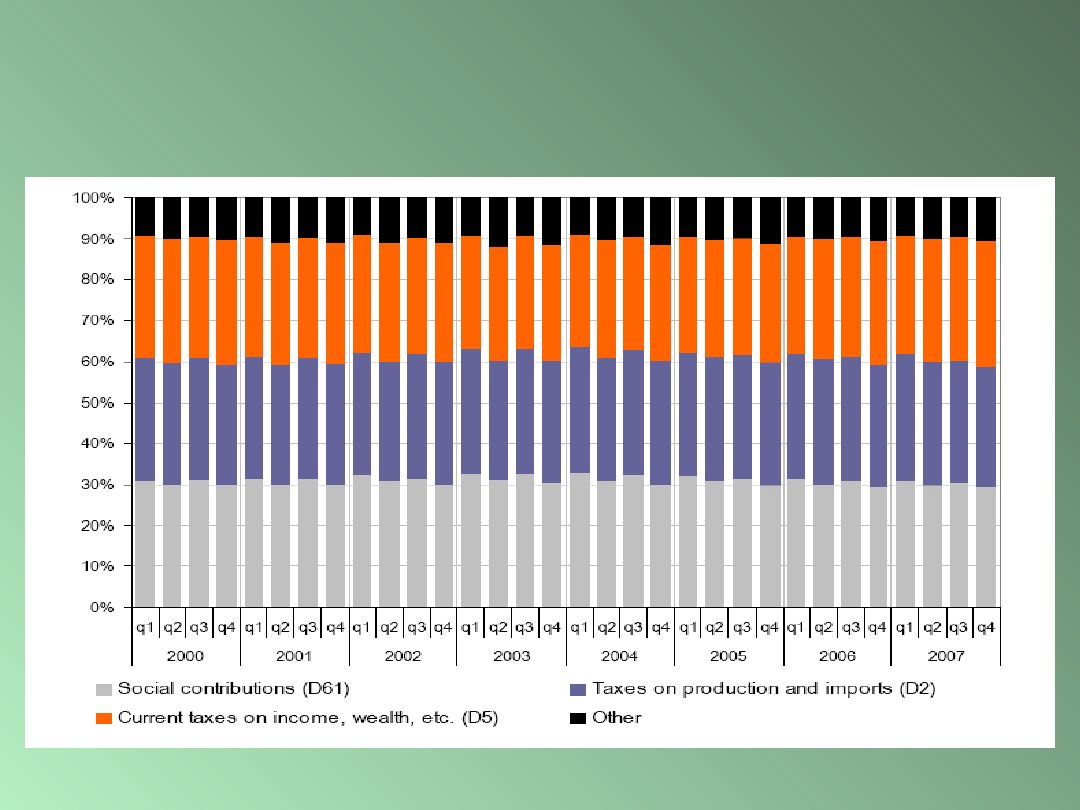

Social contributions (D.61)

Actual social contributions (D. 611)

4.92 . Actual social contributions include:

a) employers actual social contributions (D.6111). These correspond to flow D.121.

Employers’ actual social contributions are paid by employers to social security funds, insurance enterprises or autonomous as well as non autonomous pension funds administering social insurance

schemes to secure social benefits for their employees.

As employers’ actual social contributions are made for the benefit of their employees, their value is recorded as one of the components of compensation of employees together with wages and

salaries in cash and in kind. The social contributions are then recorded as being paid by the employees as current transfers to the social security funds, insurance enterprises or autonomous

as well as non autonomous pension funds;

b) employees’ social contributions (D.6112): these are social contributions payable by employees to social security, private funded and unfunded schemes. Employees ’ social contributions consist of

the actual contributions payable plus, in the case of private funded schemes, the contribution supplements payable out of the property income attributed to insurance policy holders

received by employees participating in the schemes, minus the service charges. All the service charges are treated as charges against the employees ’ contributions and not the employers’;

c) social contributions by self-employed and non-employed persons (D.6113): these are social contributions payable for their own benefit by persons who are not employees ‘ namely, self-employed

persons (employers or own-account workers), or non-employed persons. They also include the value of the contribution supplements payable out of the property income attributed to

insurance policy holders received by participating individuals that they are recorded as paying back to the insurance enterprises in addition to their other contributions.

Social contributions payable to the general government sector recorded in the accounts may be derived from two sources: amounts evidenced by assessments and declarations or cash receipts.

(a) If assessments and declarations are used, the amounts shall be adjusted by a coefficient reflecting assessed and declared amounts never collected. As an alternative treatment, a capital transfer

to the relevant sectors could be recorded equal to the same adjustment. The coefficients shall be estimated on the basis of past experience and current expectations in respect of assessed

and declared amounts never collected. They shall be specific to different types of social contributions.

(b) If cash receipts are used, they shall be time-adjusted so that the cash is attributed when the activity took place to generate the social contribution liability (or when the liability is created). This

adjustment may be based on the average time difference between the activity (or the creation of the liability) and cash receipt.

When retained at source by the employer, social contributions payable to the general government sector should be included in wages and salaries even if the employer did not in fact pass them on

to the general government. The households sector is then shown as paying the full amount on to the general government sector. The amounts actually unpaid have to be neutralised under

D.995 as a capital transfer from general government to the employers' sectors.

4.93 . Payments of actual social contributions may be compulsory by virtue of a statute or regulation, or they may be paid as a result of collective agreements in a particular industry or agreements

between employer and employees in a particular enterprise, or because they are written into the contract of employment itself. In certain cases, the contributions may be voluntary.

The voluntary contributions referred to here cover:

a) social contributions which persons who are not, or who are no longer, legally obliged to contribute pay or continue to pay to a social security fund;

b) social contributions paid to insurance enterprises (or friendly societies and pension funds classified in the same sector) as part of supplementary insurance schemes organised by enterprises for

the benefit of their employees and which the latter join voluntarily;

c) contributions to friendly societies with membership open to employees or self-employed workers.

4.94 . To distinguish between social contributions that are compulsory and those that are not, a supplementary level is introduced in the classification:

a) compulsory employers’ actual social contributions (D.61111);

b) voluntary employers’ actual social contributions (D.61112);

c) compulsory employees’ social contributions (D.61121);

d) voluntary employees’ social contributions (D.61122);

e) compulsory social contributions by self and non-employed persons (D.61131);

f) voluntary social contributions by self and non-employed persons (D.61132).

4.95 . Actual social contributions to social security funds or other government agencies are recorded gross as distributive transactions.

On the other hand, social contributions paid under private funded schemes to insurance enterprises, and to friendly societies and autonomous pension funds included in the same sector, are

recorded net, i.e. after deducting that part of the contribution which represents the value of the insurance service provided to (resident and non-resident) households. Under the conventions

adopted, this part of the contribution represents, in effect, the payment for a market service which forms part of the final consumption of households or, in the case of contributions paid by

non-resident households, part of exports of services.

In the case of non-autonomous private funded social insurance schemes, where employers maintain their own segregated reserves, no service charge is deducted from contributions paid by the

employees. As such schemes do not constitute separate institutional units from the employers, the costs of managing and administering the funds are assimilated with the employers ’

general production costs.

4.96 . Time of recording: Employers’ actual social contributions (D.6111) and employees’ social contributions (D.6112) are recorded at the time when the work that gives rise to the liability to pay

the contributions is carried out. Social contributions by self-employed and non-employed persons (D.6113) are recorded when the liabilities to pay are created.

4.97 . In the system of accounts, actual social contributions are recorded:

a) among uses in the secondary distribution of income account of households;

b) among uses in the external account of primary incomes and current transfers (in the case of non-resident households);

c) among resources in the secondary distribution of income account of resident insurers or employers;

d) among resources in the external account of primary incomes and current transfers (in the case of non-resident insurers or employers).

Imputed social contributions (D.612)

4.98 . Imputed social contributions (D.612) represent the counterpart to social benefits (less eventual employees’ social contributions) paid directly by employers

(i.e. not linked to employers’ actual contributions) to their employees or former employees and other eligible persons. They correspond to flow D.122. Their

value should, in principle, be based on actuarial considerations.

4.99 . It is necessary to introduce imputed social contributions if the social benefits distributed directly by employers are to be included in the accounts under the

heading social benefits and if the cost of these benefits (for the part which is not covered by employees’ actual contributions) is to be included in the

compensation of employees paid by the employer.

When employers provide social benefits themselves directly to their employees, ex-employees or dependants out of their own resources without involving a social

security fund, an insurance enterprise or an autonomous pension fund, and without creating a special fund or segregate reserve for the purpose, beneficiaries

may be considered as being protected against various specific needs, or circumstances, even though no payments are being made to cover them.

Remuneration should therefore be imputed for employees equal in value to the amount of social contributions that would be needed to secure the de facto

entitlements to the social benefits they accumulate. These amounts depend not only on the levels of the benefits currently payable but also on the ways in

which employers’ liabilities under such schemes are likely to evolve in the future as a result of factors such as expected changes in the numbers, age

distribution and life expectancies of their present and previous employees. Thus, the values that should be imputed for the contribution ought, in principle, to

be based on the same kind of actuarial considerations that determine the levels of premiums charged by insurance enterprises. When as a result of political

events or economic changes, the ratio between the number currently employed and the number receiving pensions changes appreciably and becomes

abnormal, the value of the imputed contributions for current employees should be estimated, which will be different from the actual value of the pensions paid

out. A reasonable percentage of wages and salaries paid to current employees can be used for this purpose.

In practice, however, it may be difficult to decide how large such imputed contributions should be. The enterprise may make estimates itself, perhaps on the basis of

the contributions paid into similar funded schemes, in order to calculate its likely liabilities in the future. Otherwise, the only practical alternative may be to

use the unfunded social benefits payable by the enterprise during the same accounting period (after deducting actual contributions made by employees

themselves) as an estimate of the imputed remuneration that would be needed to cover the imputed contributions. While there are obviously many reasons

why the value of the imputed contributions that would be needed may diverge from the unfunded social benefits actually paid in the same period, such as the

changing composition and age structure of the enterprise’s labour force, the benefits actually paid in the current period (less employees’ social contributions)

may nevertheless provide sufficient estimates of the contributions and associated imputed remuneration.

4.100 . Employers are recorded, in the generation of income account, as paying to their existing employees as a component of their compensation an amount

described as imputed social contributions equal in value to the estimated social contributions that would be needed to provide for the unfunded social benefits

to which they become entitled. Employees are recorded, in the secondary distribution of income account, as paying back to their employers the same amount

of imputed social contributions (i.e. current transfers) as if they were paying them to a separate social insurance scheme.

4.101 . Time of recording: Imputed social contributions which represent the counterpart of compulsory direct social benefits are recorded at the time the obligation

to pay the benefits arises.

Imputed social contributions which represent the counterpart of voluntary direct social benefits are recorded at the time the benefits are provided.

4.102 . In the system of accounts, imputed social contributions are recorded:

a) among uses in the secondary distribution of income account of households and in the external account of primary incomes and current transfers;

b) among resources in the secondary distribution of income account of the sectors to which the employers belong and in the external account of primary incomes

and current transfers

CURRENT TAXES ON INCOME, WEALTH, ETC.

(D.5)

4.77 . Definition:

Current taxes on income, wealth, etc. (D.5) cover all compulsory, unrequited payments,

in cash or in kind, levied periodically by general government and by the rest of the

world on the income and wealth of institutional units, and some periodic taxes which

are assessed neither on the income nor the wealth.

Current taxes on income, wealth, etc. are divided into:

a) taxes on income (D.51);

b) other current taxes (D.59).

TAXES ON PRODUCTION AND IMPORTS (D.2)

4.14 . Definition:

Taxes on production and imports (D.2) consist of compulsory, unrequited payments, in

cash or in kind which are levied by general government, or by the Institutions of the

European Union, in respect of the production and importation of goods and services,

the employment of labour, the ownership or use of land, buildings or other assets

used in production. These taxes are payable whether or not profits are made.

4.15 . Taxes on production and imports are divided into:

a) taxes on products (D.21):

(1) value added type taxes (VAT) (D.211);

(2) taxes and duties on imports excluding VAT (D.212):

import duties (D.2121);

taxes on imports excluding VAT and import duties (D.2122);

(3) taxes on products, except VAT and import taxes (D.214).

b) other taxes on production (D.29).

Other

Other

4.139 . a) Current transfers from NPISHs to general government which are not taxes;

b) payments by general government to public enterprises classified in the sector non-financial

corporate and quasi-corporate enterprises intended to cover abnormal pension charges;

c) travelling fellowships and awards paid to resident or non-resident households by general

government or NPISHs;

d) bonus payments on savings granted at intervals by general government to households in

order to reward them for their saving during the period;

e) the refunds by households of expenditure incurred on their behalf by social welfare

organisations;

f) current transfers from NPISHs to the rest of the world;

g) sponsoring by corporations if those payments cannot be regarded as purchases of

advertising or other services (for instance, transfers for a good cause, or scholarships);

h) current transfers from general government to households in their capacity as consumers, if

not recorded as social benefits.

4.140 . Time of recording: These transfers are recorded when they are made, except those

from or to general government, which are recorded when they are to be made.

In the system of accounts, miscellaneous current transfers appear:

a) among resources and uses in the secondary distribution of income account of all sectors;

b) among resources and uses in the external account of primary incomes and current

transfers.

Główne składniki dochodów publicznych w poszczególnych

krajach UE w 2007

http://epp.eurostat.ec.europa.eu/cache/ITY_OFFPUB/KS-SF-08-054/EN/KS-SF-08-054-EN.PDF

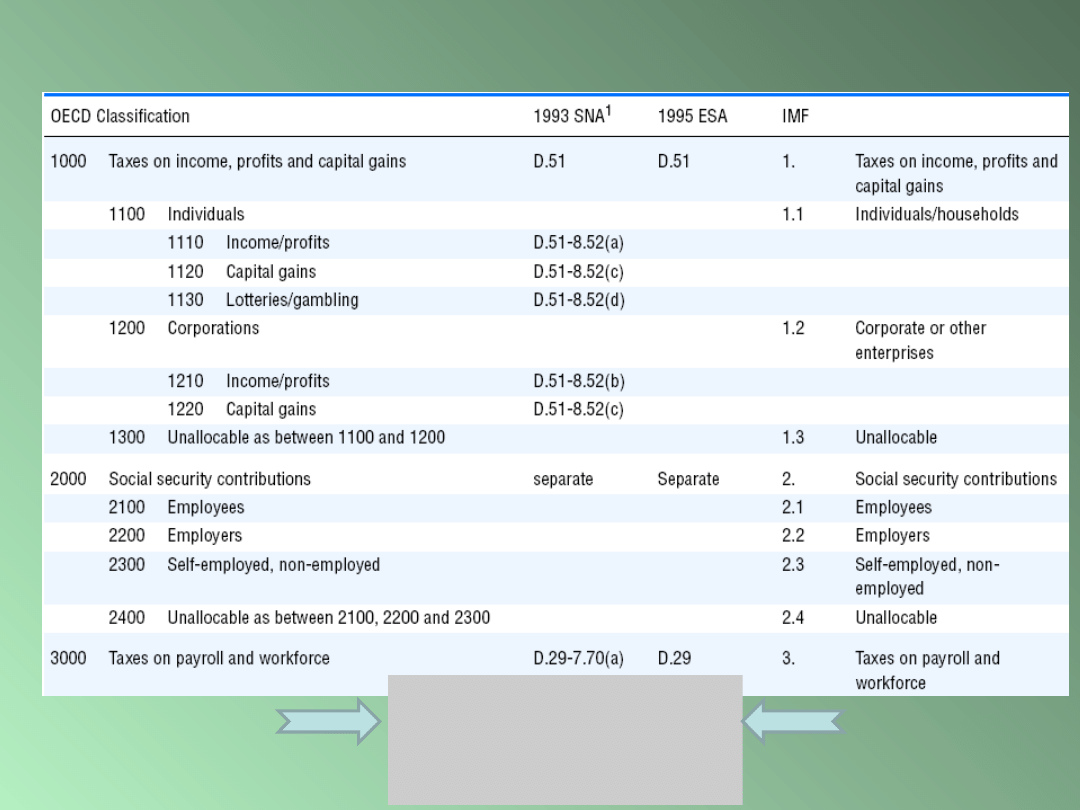

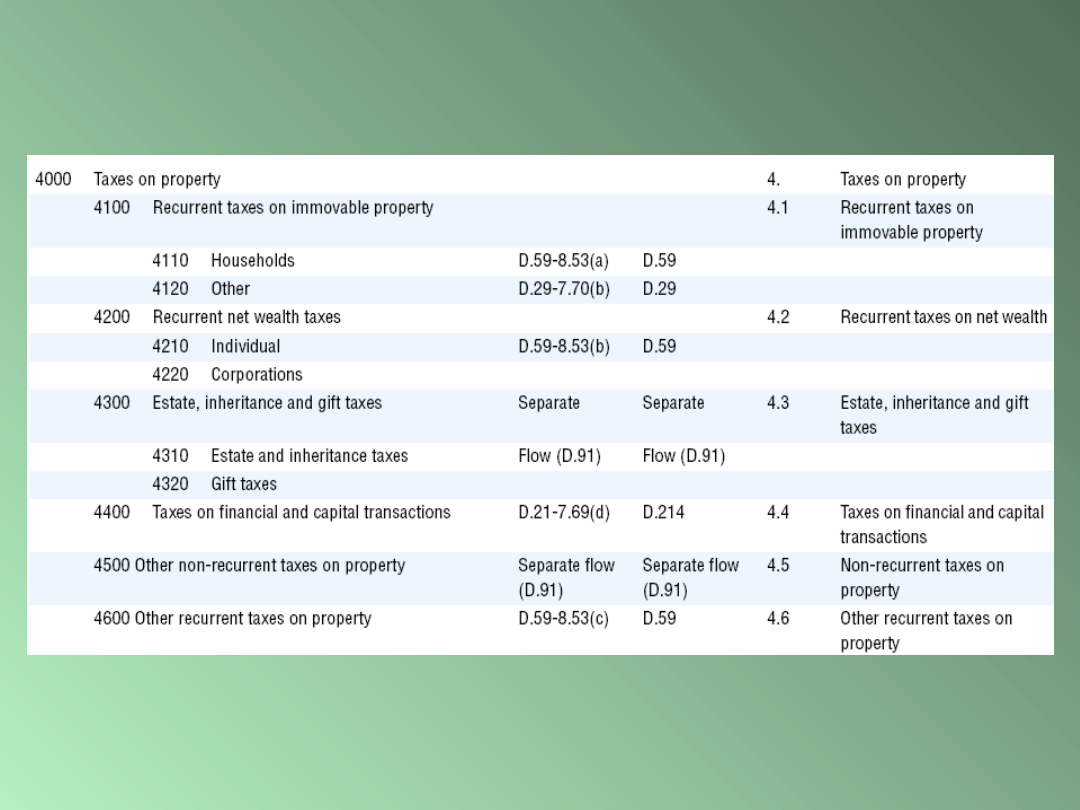

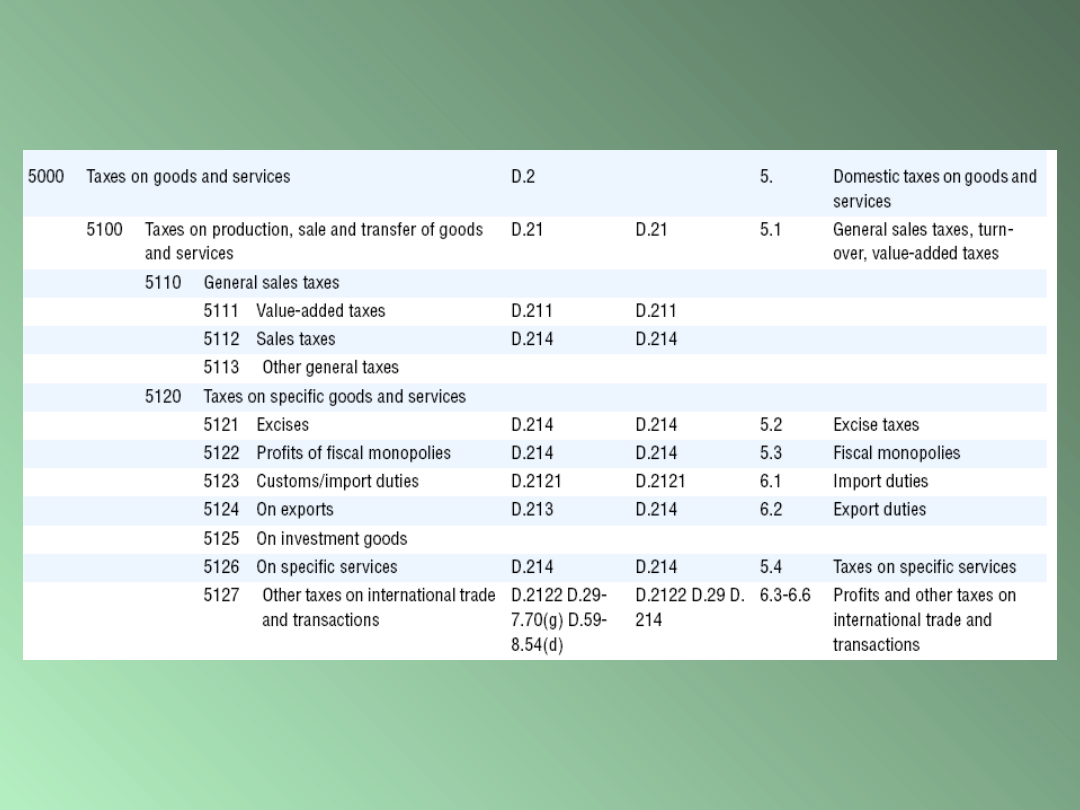

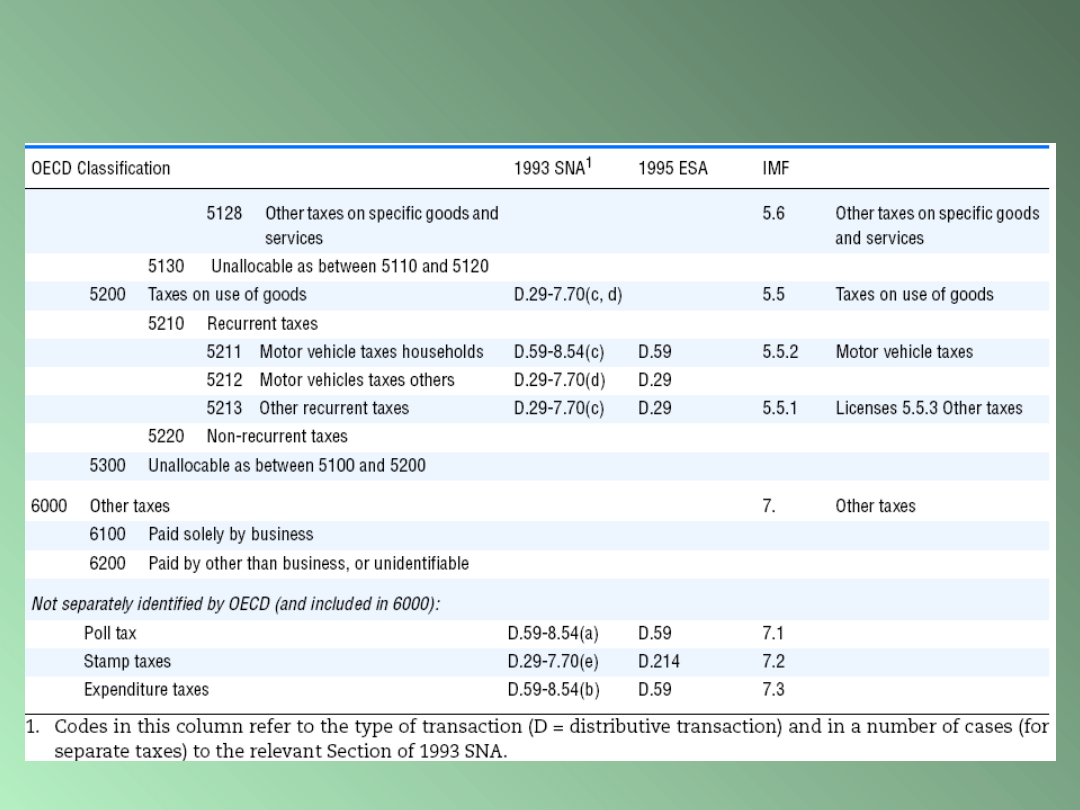

Porównanie klasyfikacji podatków wg

nomenklatury OECD – SNA – IMF

(GFS)

System of National Accounts (1993

SNA);

European System of Accounts (1995

ESA);

IMF Government Finance Statistics

(IMF).

Źródło: Revenue Statistics 1965-2006, OECD 2007, ISBN 978-92-64-03834-9, s. 306 i następne

.

Klasyfikacje dochodów publicznych

OECD – SNA - IMF

Klasyfikacje dochodów publicznych

OECD – SNA - IMF

Klasyfikacje dochodów publicznych

OECD – SNA - IMF

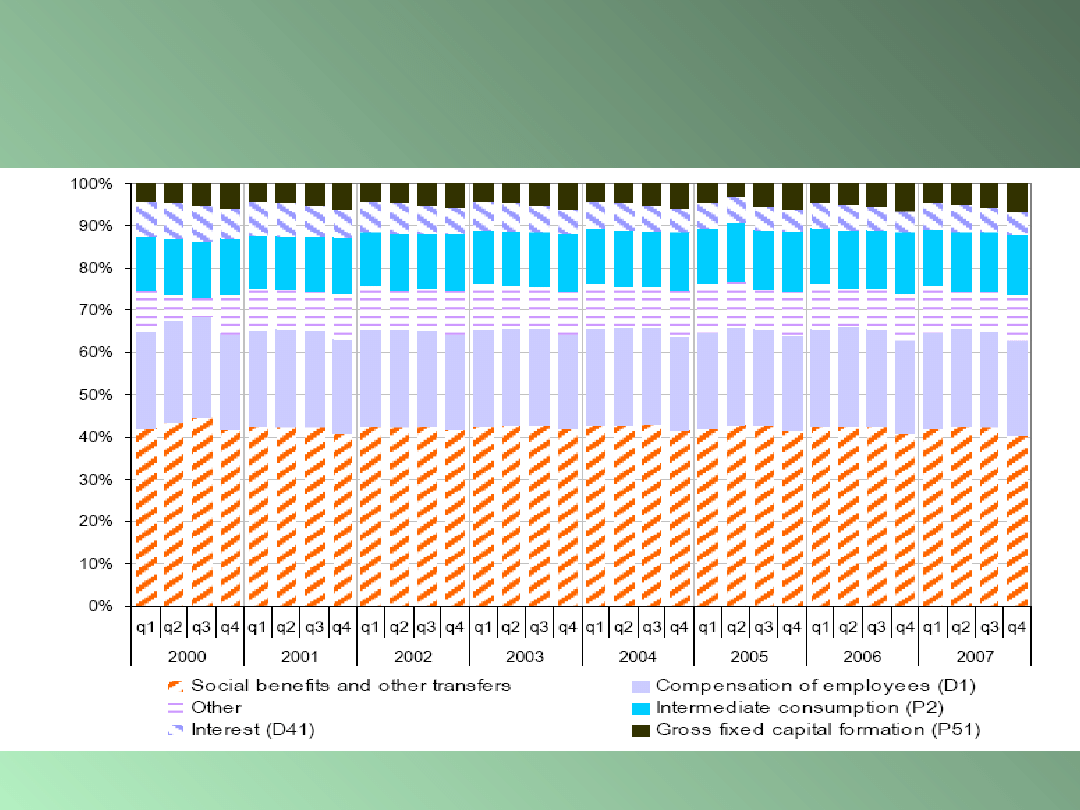

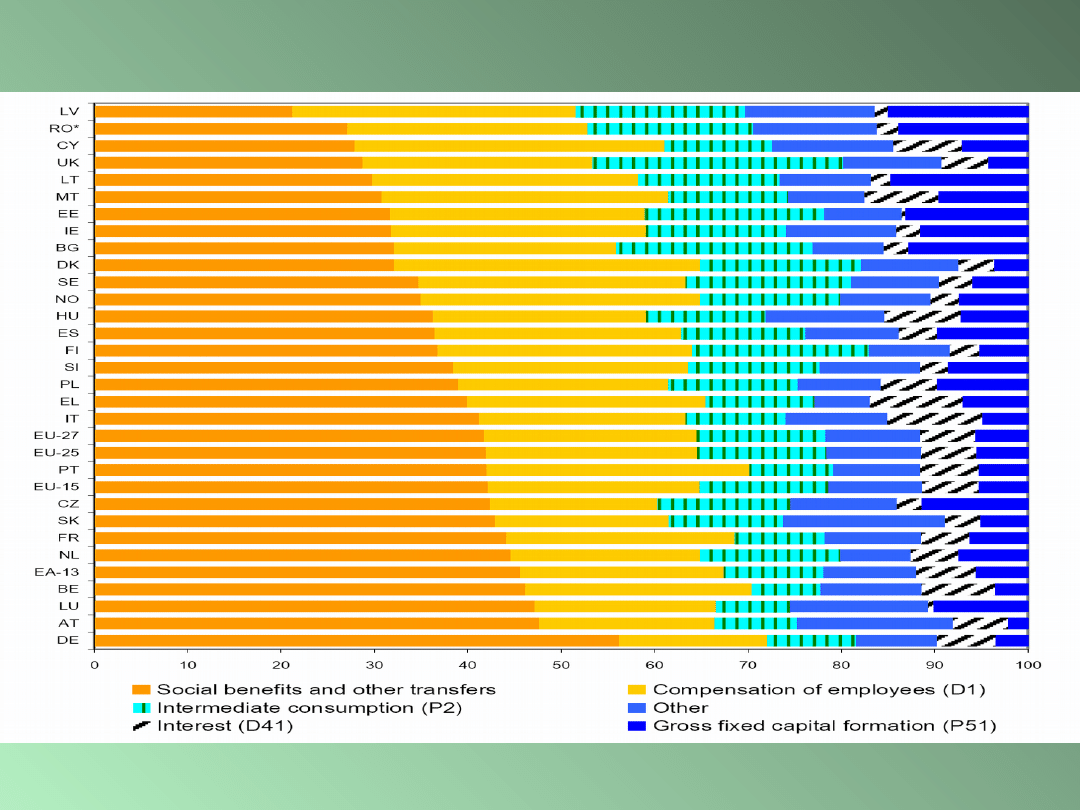

Główne kierunki wydatków

publicznych w UE-25 w 2005 roku

Ivana Yablonska, General government

expenditure

and revenue 2005 data, Eurostat 2006, s. 3.

•Inne

•Majątkowe

•Subsydia do

cen towarów

•Inne zasiłki

socjalne

•Odsetki

•Wynagrodze

nia i

pochodne

•Konsumpcja

pośrednia

Główne kierunki wydatków

publicznych w UE-27 w latach

2000-2007 roku

http://epp.eurostat.ec.europa.eu/cache/ITY_OFFPUB/KS-SF-08-054/EN/KS-SF-08-054-EN.PDF

Interest (D.41)

4.42 . Definition:

Under the terms of the financial instrument agreed between them, interest

(D.41) is the amount that the debtor becomes liable to pay to the creditor over

a given period of time without reducing the amount of principal outstanding.

4.43 . Creditors lend funds to debtors that lead to creation of one or other of the

financial instruments listed below.

This form of property income is receivable by the owners of certain kinds of

financial assets:

a) deposits (AF.2);

b) securities other than shares (AF.3);

c) loans (AF.4);

d) other accounts receivable (AF.7).

COMPENSATION OF EMPLOYEES (D.1)

4.02 . Definition:

Compensation of employees (D.1) is defined as the total remuneration,

in cash or in kind, payable by an employer to an employee in return

for work done by the latter during the accounting period.

Compensation of employees is broken down into:

a) wages and salaries (D.11): wages and salaries in cash; wages and

salaries in kind;

b) employers’ social contributions (D.12): employers’ actual social

contributions (D.121); employers’ imputed social contributions

(D.122).

INTERMEDIATE CONSUMPTION (P.2)

3.69 . Definition:

Intermediate consumption consists of the value of the goods and services consumed as inputs by a process of production, excluding fixed assets whose consumption is

recorded as consumption of fixed capital. The goods and services may be either transformed or used up by the production process.

3.70 . Intermediate consumption includes the following borderline cases:

a) the value of all the goods or services used as inputs into ancillary activities. Common examples are purchasing, sales, marketing, accounting, data processing,

transportation, storage, maintenance, security, etc. These goods and services are not distinguished from those consumed by the principal (or secondary) activities

of a local KAU;

b) the value of goods and services which are received from another local KAU of the same institutional unit (only if they comply to the general definition in paragraph

3.69.);

c) the costs of using rented fixed assets, e.g. the operational leasing of machines or cars;

d) the subscriptions, contributions or dues paid to non-profit business associations (see paragraph 3.35.);

e) items not treated as gross capital formation, like:

(1) small tools which are inexpensive and used for relatively simple operations, such as saws, hammers, screwdrivers and other hand tools; small devices, such as pocket

calculators. By convention, in the ESA, all expenditure on such durables which does not exceed 500 ECU (in prices of 1995) per item (or, when bought in

quantities, for the total amount bought), should be recorded as intermediate consumption;

(2) the ordinary, regular maintenance and repair of fixed assets used in production;

(3) military weapons of destruction and the equipment needed to deliver them (but not light weapons or armoured vehicles acquired by police and security forces, which

are treated as gross fixed capital formation);

(4) services of research and development, staff training, market research and similar activities, purchased from an outside agency or provided by a separate local KAU of

the same institutional unit.

f) payments for the use of intangible non-produced assets like patented assets, trade marks, etc. (excluding payments for the purchase of such property rights: these are

treated as acquisitions of an intangible non-produced assets);

g) expenditure by employees, reimbursed by the employer, on items necessary for the employers’ production, like contractual obligations to purchase on own-account

tools or safety-wear;

h) expenditure by employers which is to their own benefit as well as to that of their employees, because it is necessary for the employers ’ production. Cases in point are:

(1) reimbursement of employees for travelling, separation, removal and entertainment expenses incurred in the course of their duties;

(2) providing amenities at the place of work;

a more extensive list is presented in the paragraphs on compensation of employees (D.1) (see paragraph 4.07.).

i) non-life insurance service charges paid by local KAUs (see also Annex III Insurance): in order to record only the service charge as intermediate consumption the

premiums paid should be discounted for, e.g. claims paid out and the net change in actuarial reserves. The latter can be allocated to local KAUs as a proportion of

the premiums paid;

j) the use of financial intermediation services indirectly measured by resident producers;

(k) by convention, the central bank output should be entirely allocated to the intermediate consumption of other financial intermediaries (subsectors S122 Đ S123).

3.71 . Intermediate consumption excludes:

a) items treated as gross capital formation, like:

(1) valuables;

(2) mineral exploration;

(3) major improvements which go considerably beyond what is required simply to keep the fixed assets in good working order, e.g. renovation, reconstruction or

enlargement;

(4) software purchased or produced on own-account.

b) expenditure by employers treated as wages and salaries in kind (see paragraph 4.05.);

c) use by market or own-account producer units of collective services provided by government units (treated as collective consumption expenditure by government);

d) goods or services produced and consumed within the same accounting period and within the same local KAU (they are also not recorded as output);

e) payments for government licenses and fees that are treated as taxes on production (see paragraphs 4.79. 4.80.).

Gross fixed capital formation (P.51)

3.102 . Definition:

Gross fixed capital formation (P.51) consists of resident producers acquisitions, less disposals, of fixed assets during a given period plus certain additions to

the value of non-produced assets realized by the productive activity of producer or institutional units. Fixed assets are tangible or intangible assets

produced as outputs from processes of production that are themselves used repeatedly, or continuously, in processes of production for more than one

year.

3.103 . Gross fixed capital formation consists of both positive and negative values:

a) positive values:

(1) new or existing fixed assets purchased;

(2) fixed assets produced and retained for producers own use (including own account production of fixed assets not yet completed or fully mature);

(3) new or existing fixed assets acquired through barter;

(4) new or existing fixed assets received as capital transfers in kind;

(5) new or existing fixed assets acquired by the user under a financial lease;

(6) major improvements to fixed assets and existing historic monuments;

(7) natural growth of those natural assets that yield repeat products.

b) negative values, i.e. disposals of fixed assets recorded as negative acquisitions:

(1) existing fixed assets sold;

(2) existing fixed assets surrendered in barter;

(3) existing fixed assets surrendered as capital transfers in kind.

3.104 . The disposals components of fixed assets exclude:

a) consumption of fixed capital (which includes anticipated normal accidental damage);

b) exceptional losses, such as those due to drought or other natural disasters (recorded as an other change in the volume of assets).

3.105 . The following types of gross fixed capital formation may be distinguished:

a) acquisitions, less disposals, of tangible fixed assets:

(1) dwellings;

(2) other buildings and structures;

(3) machinery and equipment;

(4) and cultivated assets, e.g. trees and livestock.

b) acquisitions, less disposals, of intangible fixed assets:

(1) mineral exploration;

(2) computer software;

(3) entertainment, literary or artistic originals;

(4) other intangible fixed assets.

c) major improvements to tangible non-produced assets, in particular those pertaining to land (though the acquisition of non-produced assets is not

included);

d) costs associated with the transfers of ownership of non-produced assets, like land and patented assets (though the acquisition of these assets themselves

is not included).

Gross fixed capital formation (P.51)

3.106 . Major improvements to land include:

a) reclamation of land from sea by the construction of dikes, sea walls or dams for this purpose;

b) clearance of forests, rocks, etc. to enable land to be used in production for the first time;

c) draining of marshes or the irrigation of deserts by the construction of dikes, ditches and irrigation channels;

d) prevention of flooding or erosion by the sea or rivers by the construction of breakwaters, sea walls or flood barriers.

These activities may lead to the creation of substantial new structures such as sea walls, flood barriers and dams but these are not themselves used directly to produce

other goods and services in the way that most structures are. Their construction is undertaken to obtain more or better land, and it is the land, a non-produced

asset, that is needed for production. For example, a dam built to produce electricity serves quite a different purpose from a dam built to keep out the sea. Only

building the latter type of dam should be classified as an improvement to land.

3.107 . Gross fixed capital formation includes borderline cases like:

a) acquisitions of houseboats, barges, mobile homes and caravans used as residences of households and any associated structures such as garages;

b) structures and equipment used by the military (similar to those utilized by civilian producers) such as airfields, docks, roads and hospitals;

c) light weapons and armoured vehicles used by non-military units;

d) changes in livestock used in production year after year, such as breeding stock, dairy cattle, sheep reared for wool and draught animals;

e) changes in trees that are cultivated year after year, such as fruit trees, vines, rubber trees, palm trees, etc.;

f) improvements to existing fixed assets that go well beyond the requirements of ordinary maintenance and repairs;

g) the acquisition of fixed assets by financial leasing.

3.108 . Gross fixed capital formation excludes:

a) transactions included in intermediate consumption, like:

(1) purchase of small tools for production purposes (see paragraph 3.70. e);

(2) ordinary maintenance and repairs;

(3) purchase of military weapons and their supporting systems;

(4) the purchase of fixed assets to be used under an operational leasing contract (see also Annex II Leasing and hire purchase of durable goods).

b) transactions recorded as changes in inventories;

(1) animals raised for slaughter, including poultry;

(2) trees grown for timber (work-in-progress).

c) machinery and equipment acquired by households for purposes of final consumption (final consumption expenditure);

d) holding gains and losses on fixed assets (other changes in assets);

e) catastrophic losses on fixed assets (other changes in assets), e.g. destruction of cultivated assets and livestock by outbreaks of disease (and not normally covered by

insurance) or damage due to abnormal flooding, wind damage or forest fires (see chapter 6.).

3.109 . Gross fixed capital formation in the form of improvements to existing fixed assets is to be classified with acquisitions of new fixed assets of the same kind.

3.110 . Intangible fixed assets typically consist of new information, specialized knowledge, etc. and comprise:

a) mineral exploration comprising costs of actual test drilling, aerial or other surveys, transportation costs, etc.;

b) computer software and large data bases to be used in production for more than one year;

c) literary and artistic originals of manuscripts, renderings, models, films, sound recordings, etc.

3.111 . For both fixed assets and non-produced non-financial assets, the costs of ownership transfer incurred by their new owner consist of:

a) charges incurred in taking delivery of the asset (new or existing asset) at the required location and time, such as transport charges, installation charges, erection

charges, etc.;

b) professional charges or commissions incurred, such as fees paid to surveyors, engineers, lawyers, value's, etc., and commissions paid to estate agents, auctioneers,

etc.;

c) taxes payable by the new owner on the transfer of ownership of the asset.

All these costs are to be recorded as gross fixed capital formation by the new owner. Note that the taxes are to be treated as taxes on the services of intermediaries and

not as taxes on the asset bought.

http://circa.europa.eu/irc/dsis/nfaccount/info/data/esa95/en/een00137.htm

http://epp.eurostat.ec.europa.eu/cache/ITY_OFFPUB/KS-SF-08-054/EN/KS-SF-08-054-EN.PDF

Główne kierunki wydatków publicznych w poszczególnych

krajach UE w 2007

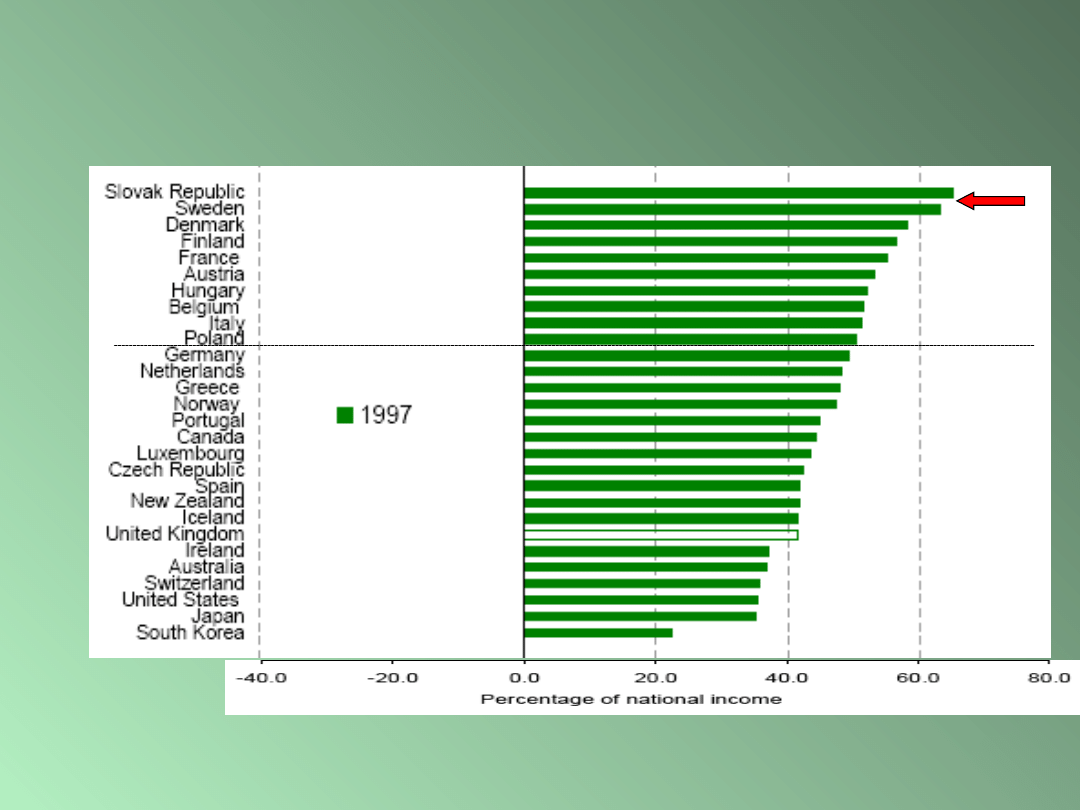

Wydatki publiczne w 1997 roku

w wybranych krajach

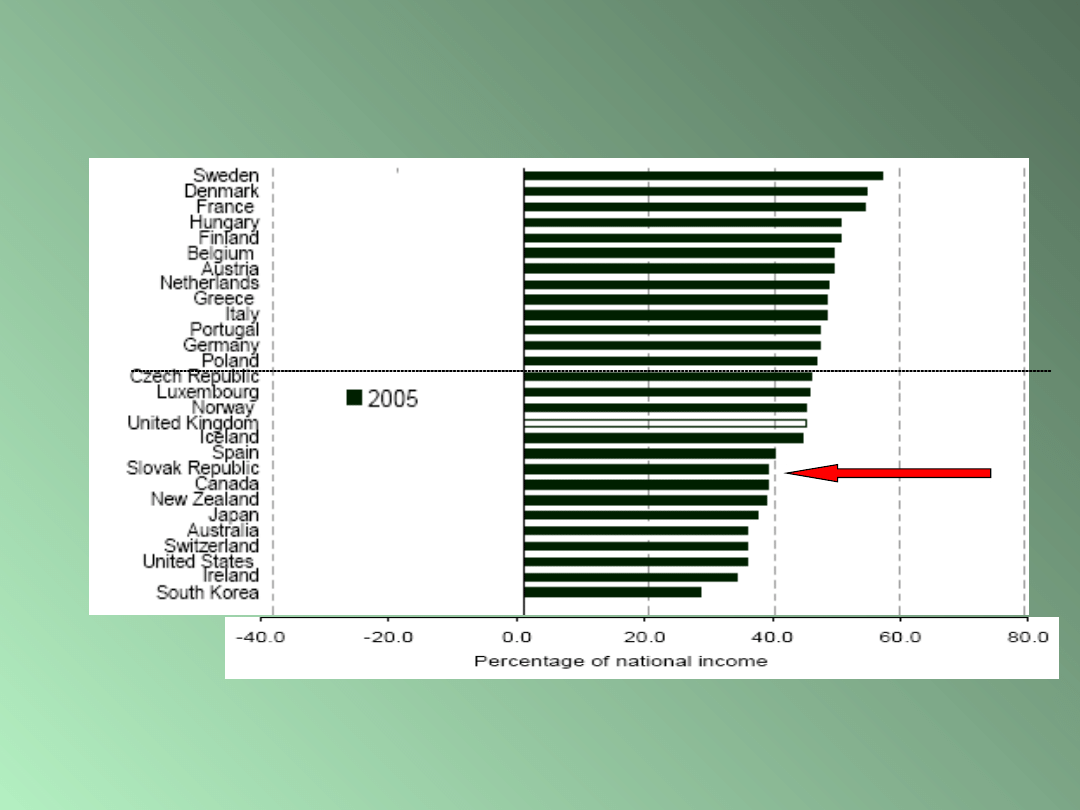

Wydatki publiczne w 2005 roku

w wybranych krajach

Zmiana w poziomie wydatków

publicznych

w latach 1997-2005

Finanse publiczne w

Konstytucji RP

Finanse publiczne w Konstytucji

RP

•Konstytucja RP jest aktem prawnym najwyższej rangi w

polskim systemie prawnym, co oznacza, że inne akty prawne

wewnętrzne, w tym zwłaszcza ustawy podatkowe nie mogą być

sprzeczne z jej przepisami.

•Obecna Konstytucja z 1997, w przeciwieństwie do poprzedniej

(tj. z 1952 r.) stosunkowo szeroko normuje kwestie finansów

publicznych, co należy uznać za jej zaletę. Podobne rozwiązania

stosuje większość państw rozwiniętych.

•Przepisy Konstytucji dotyczą regulują problematykę finansów

publicznych wprost albo też pośrednio.

• Najważniejsza część przepisów odnoszących się do tematyki

finansów publicznych zawarta jest w rozdziale X (finanse

publiczne) oraz VII (samorząd terytorialny).

FINANSE PUBLICZNE w KONSTYTUCJI - PRZYKŁADY

Art. 216.

Nie wolno zaciągać pożyczek lub udzielać gwarancji i

poręczeń finansowych, w następstwie których państwowy

dług publiczny przekroczy 3/5 wartości rocznego

produktu krajowego brutto. Sposób obliczania wartości

rocznego produktu krajowego brutto oraz państwowego

długu publicznego określa ustawa.

Art. 217.

Nakładanie podatków, innych danin publicznych,

określanie podmiotów, przedmiotów opodatkowania i

stawek podatkowych, a także zasad przyznawania ulg i

umorzeń oraz kategorii podmiotów zwolnionych od

podatków następuje w drodze ustawy.

Document Outline

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

- Slide 17

- Slide 18

- Slide 19

- Slide 20

- Slide 21

- Slide 22

- Slide 23

- Slide 24

- Slide 25

- Slide 26

- Slide 27

- Slide 28

- Slide 29

- Slide 30

- Slide 31

- Slide 32

- Slide 33

- Slide 34

- Slide 35

- Slide 36

- Slide 37

- Slide 38

- Slide 39

- Slide 40

- Slide 41

- Slide 42

- Slide 43

- Slide 44

- Slide 45

- Slide 46

- Slide 47

- Slide 48

- Slide 49

- Slide 50

- Slide 51

- Slide 52

- Slide 53

- Slide 54

- Slide 55

- Slide 56

- Slide 57

- Slide 58

- Slide 59

- Slide 60

- Slide 61

- Slide 62

- Slide 63

- Slide 64

- Slide 65

- Slide 66

- Slide 67

- Slide 68

- Slide 69

- Slide 70

- Slide 71

- Slide 72

- Slide 73

- Slide 74

- Slide 75

- Slide 76

Wyszukiwarka

Podobne podstrony:

Wyklad FP II dla studenta

Wyklad FP V

Wyklad FP IV

wyklad FP III dla studenta

Wyklad FP VI

Wyklad FP I dla studenta

WYKLADY FP

wyklady fp sciaga1, Finanse przedsiębiorstw

Wyklady- FP, T: Pojęcie i struktura finansów publicznych

Wyklad FP II dla studenta

Wyklad FP V

Wyklad FP IV

wykład FP

wyklad 2 metodologia pracy naukowej, Ekonomia

EIE wykład 3 - 02.04.2011 r, Ekonomia integracji europejskiej

Finanse - WYKLAD 3, Różne Dokumenty, MARKETING EKONOMIA ZARZĄDZANIE

wykład 6- (05. 04. 2001), Ekonomia, Studia, I rok, Finanase publiczne, Wykłady-stare, Wykłady

więcej podobnych podstron