Background

• From Taylor to Skinner, through the

Quality gurus, an increasing requirement

to measure throughout business

• Led to ― the unanticipated consequences

of measurement” (Ridgway, 1956)

• Balanced set of measures first mooted by

Drucker in 1954 as a potential solution

solution to the issues raised by these

themes.

Balanced Measures

“ market standing, innovation, productivity,

physical and financial resources,

profitability, manager performacne and

development, worker performance and

attitude, and public responsibility”

…..are all appropriate performance criteria

Drucker(1954:??)

Balanced Business Scorecard

is both a process and a tool

– Thinking process

to define what constitutes

a thriving business, and what matters most to

your business

– Communications tool

to tell people what

they need to do to achieve success

– Management tool

to trace performance

problems to their cause

The Balanced Scorecard

What it does:

• Measures the achievement of the

business strategy

• Communicates strategic direction

• Establishes key performance measures

and performance targets at the

organisational level

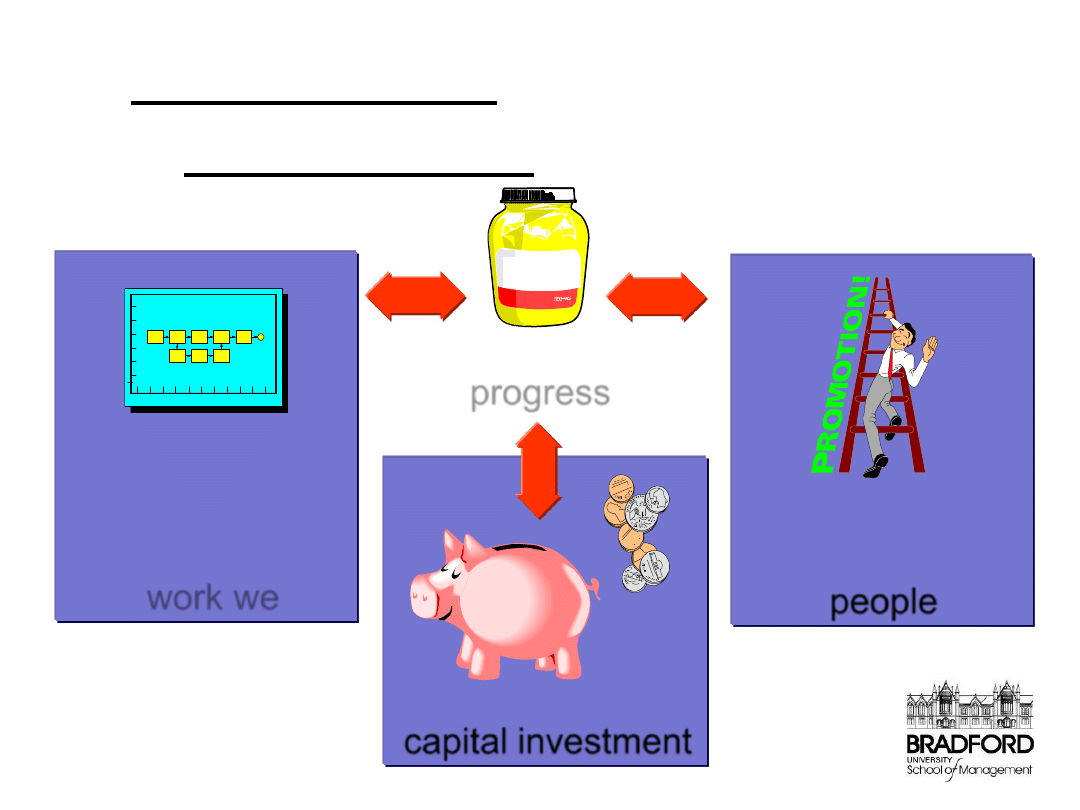

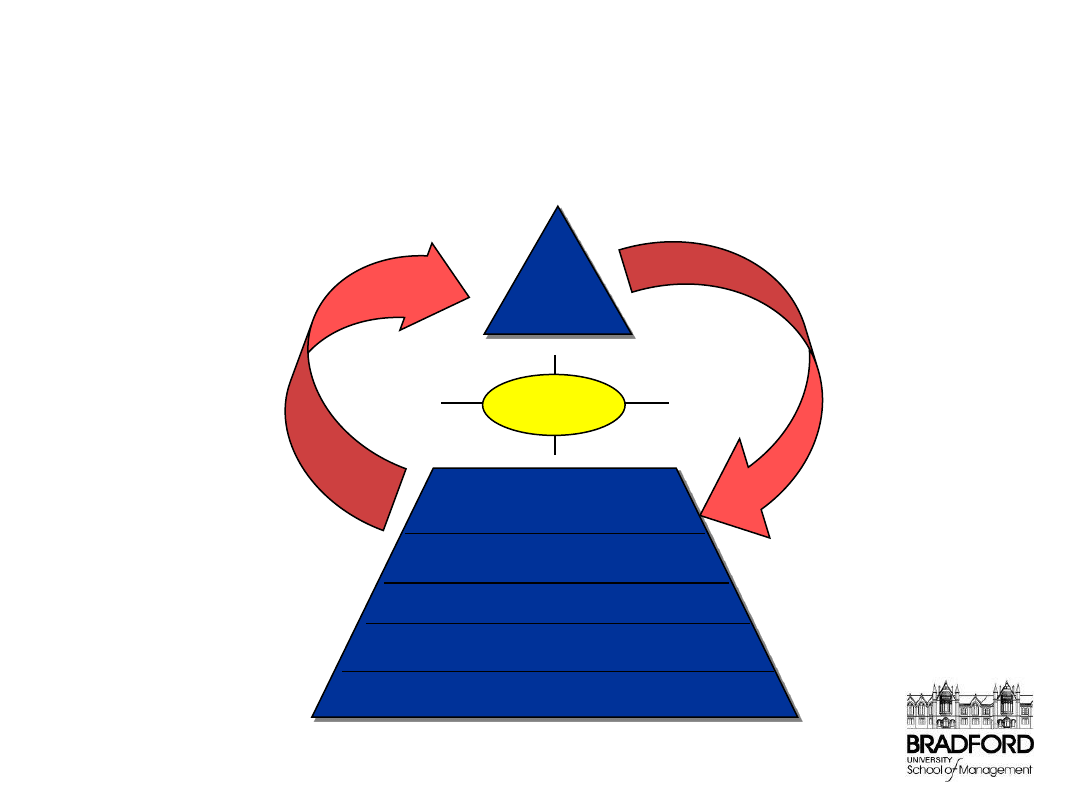

Measurement links the 3 areas

of Management in any business

How we manage

the work we do

How we manage

people

How we manage

capital investment

GLUE

How we measure

progress

Using the scorecard to drive a

performance culture

Team Target Setting

Linkage to Change Programmes

Team Accountability & Rewards

Bottom Up Goal Setting

Corporate Linkage: Organisation Design

The Vision

Learning

Feedback

Systems

1. The Creation Phase

Develop the scorecard.

Clarify

the vision and gain

executive

consensus

2. The Deployment Phase

Communicate the vision

to all levels of the

organisation and create

team scorecards

4. The Ongoing Improvement Phase

Integrate the scorecard into the

management process

• monthly management review

• strategic planning update

3. The Commitment Phase

Deploy the scorecard down to

individuals and embed them in

the reward system

The Four Perspectives

How do we look to

shareholders?

What must we

excel at?

Can we continue to

improve and add value?

How do customers

see us?

GOALS MEASURES

Customer

Perspective

Financial

Perspective

GOALS MEASURES

Innovation & Learning

Perspective

GOALS MEASURES

Internal Business

Perspective

GOALS MEASURES

Vision

and

Strategy

The components

• Goals/objectives – needs to articulate

them into observable and measurable

parts

• Metrics – actionable and tangible, support

the tracking of achieving the objects

• Targets – performance level expectations

set against the strategic plan

A Balanced Scorecard……..

• Provides managers with the instrumentation they need to

navigate to future competitive success

• Provides executives with a comprehensive framework

that translates a company’s vision and strategy into a

coherent set of performance measures

• The whole organisation understands how they are

contributing to the achievement of the vision of an

organisation

• Enables businesses to look and move forward rather

than backward

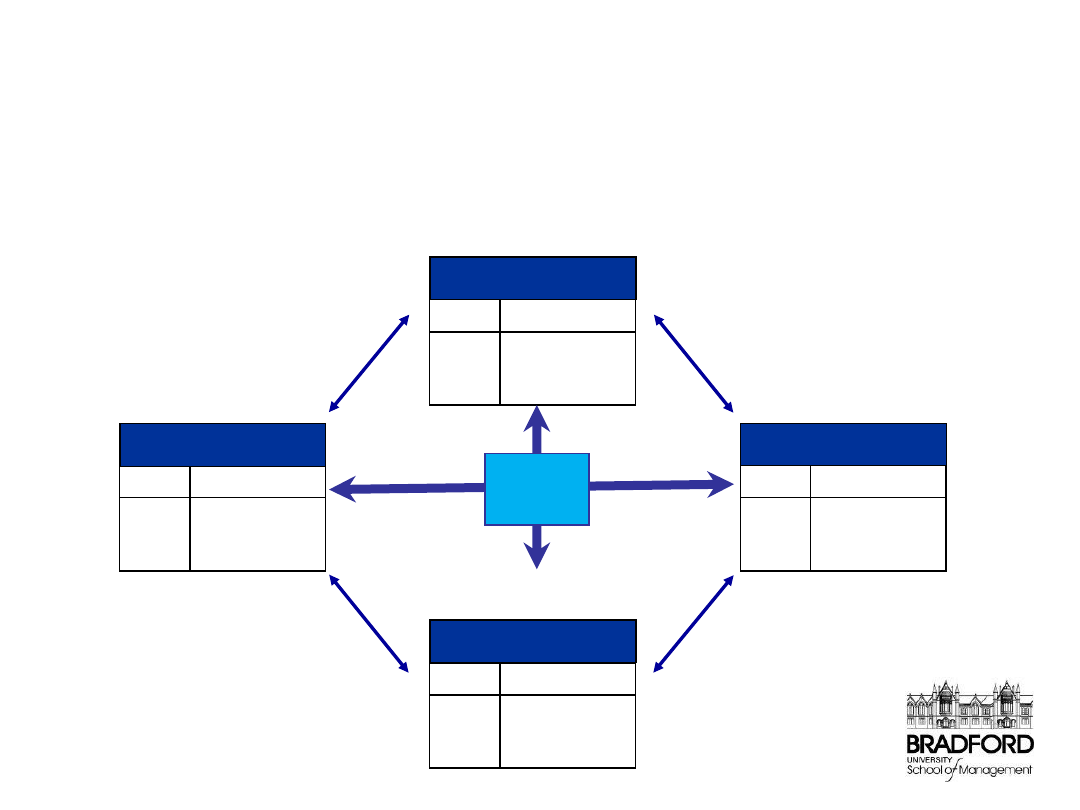

The Scorecard Architecture

Organization

Group/ Department

Individual

Select

group

impactable

CSFs

Identify

organisational

objectives to

reach strategy

Identify

organisational

strategy

Group/

department

measures and

metrics

Group/

department

objectives

Individual

goals

Select

individual

impactable

CSFs

Organisation

level

scorecard

Group

/department

level

scorecard

Individual

measures &

metrics

scorecard

Common questions #1:

How many measures?

•

Longevity:

– businesses

change

;

some change very fast

– focus on individual

measures also

changes

– it takes

time to

implement

performance

measurement

frameworks and tools

– better to have over-

catered than under-

catered...

– … so long as you

support this with

appropriate

technology

•

Technology:

– most

Executive

Information Systems

allow you to set

thresholds

– good management

focuses on those

measures that have

dropped below a

certain threshold

– so at any one time the

technology can

filter

out only a small

number of

critical

measures, from a pool

of

useful

measures

Accountabilities:

•

Balanced Business Score

Cards assume a

cascade

of information

•

at any one time, any one

individual, should have

only a small number of

measures to consider

•

but these measures

combine and aggregate

•

… for example

Common questions #2:

Why is it called ―balanced‖?

– Balance of measures

• at least 4 areas of measurement

• not all financial

– Balance of types of measure

• leading and lagging measures

• helps to forecast and follow through

• not just ―oh dear, haven’t we done badly last month!‖

– Balance of how measures are used

• cascade encourages teamwork

• ―detective search‖ for the causes of underperformance

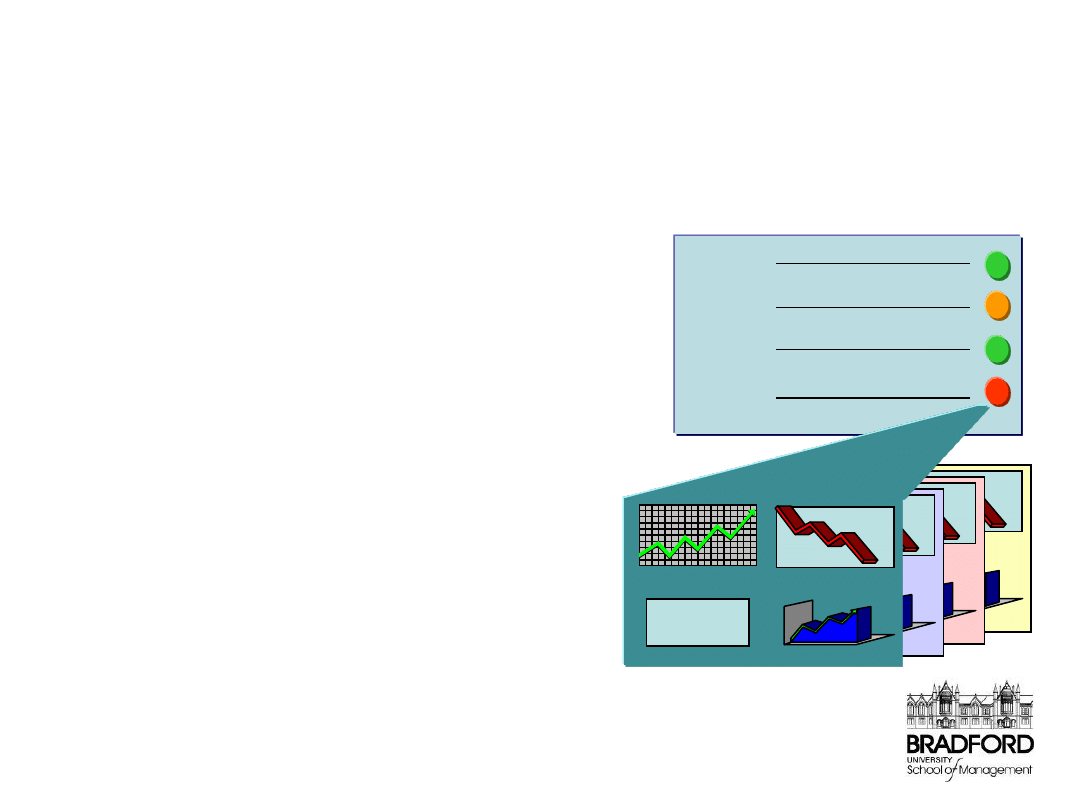

Common questions #3:

So how is it used?

– Performance Dashboard

and Traffic Light Reports

• flag measures that

have gone critical/are

going critical

• focus attention on

where it matters most

• communicate why

certain action is

required

• provide feedback on

the results of past

action

– Actions are set as a result

of regular review of the

dashboard

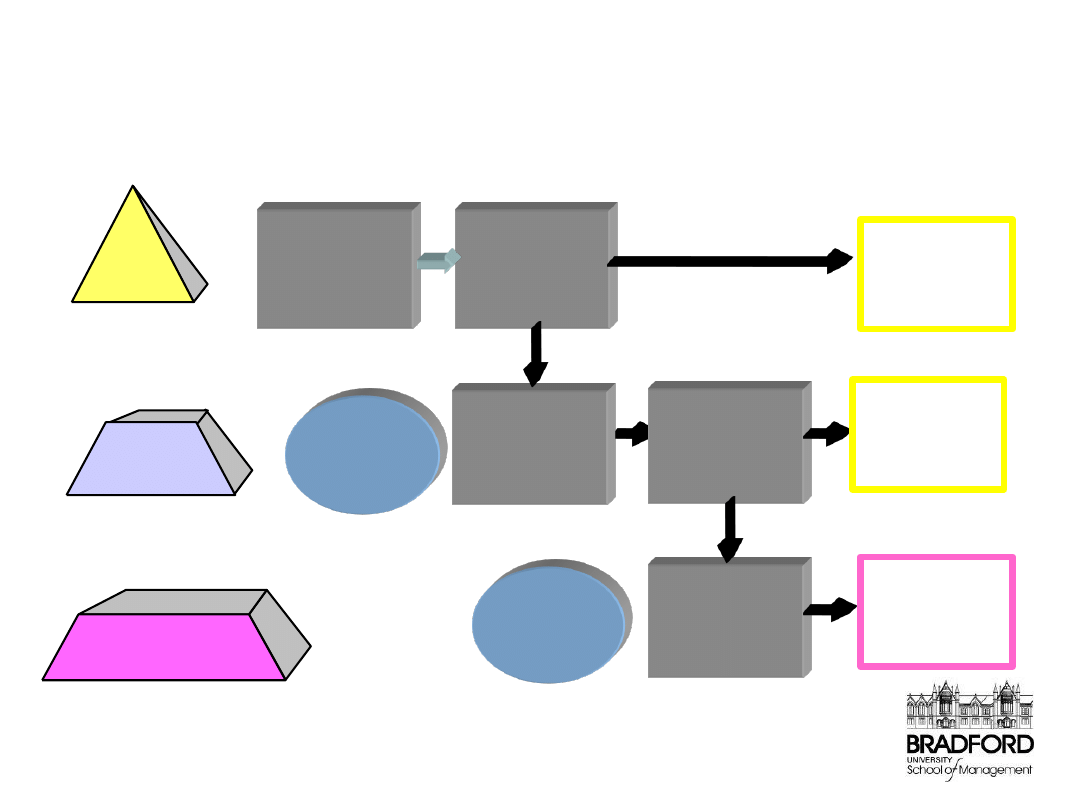

Measure 1

Measure 2

Measure 3

Measure 4

Measure 1

Measure 2

Measure 3

Measure 4

Measure 1

Measure 2

Measure 3

Measure 4

CSF 1

CSF 2

CSF 3

CSF 4

Measure 1

Measure 2

Measure 3

Measure 4

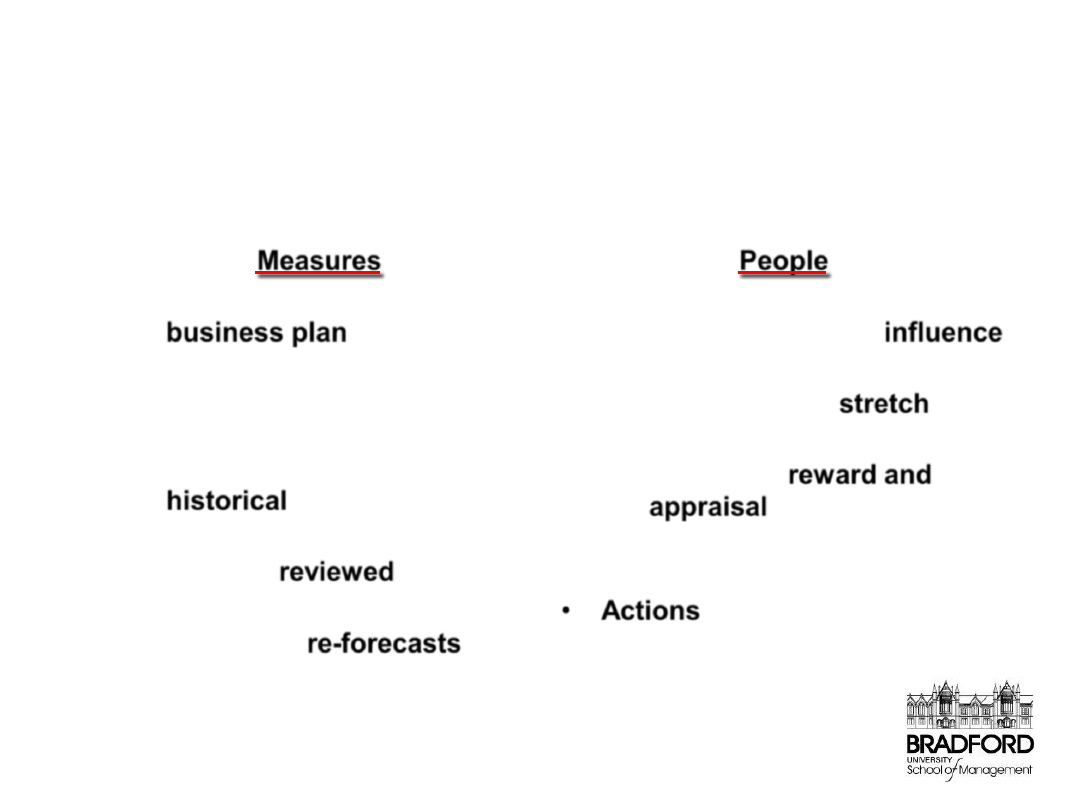

Common questions #4:

How are targets set?

•

Targets for

Measures

...

– … are set based on the

business plan

, given the

required/desired

performance for the

business

– … are compared with

historical

data

– … are set at the start of the

year and

reviewed

regularly

•

It helps to have a part of the

dashboard that

re-forecasts

year end results given actual

performance to date

•

Targets for

People

…

– … are set with regard to

measures they can

influence

— the cascade concept

– … are normally

stretch

targets

— requiring some effort

– … relate to

reward and

appraisal

— they are the

―contract‖ a business has with

its employees

•

Actions

taken to achieve those

targets matter as much as whether

they were achieved or not

Five simple steps to

balanced measurement

1. Agree business objectives

2. Develop a strawman Balanced Scorecard

3. Discuss, debate and check how realistic it

would be to implement

– use it as a starting

point

4. Finalise it

5. Ensure operational systems and processes

can deliver the indicators

• A

thriving

business must address at least:

Can we

continue to

improve and

add value?

Innovation

What must

we excel at?

Quality

How do we

keep our

customers?

Customers

Are we

satisfying

those who

fund us?

Financial

Balanced Business

Scorecard focuses on at

least four main areas

Wyszukiwarka

Podobne podstrony:

BALANCED SCORECARD PROJEKTU pusty dla studentów

Balanced Scorecard synteza wskazniki 2011

Balanced Scorecard demo

Balanced Scorecard, ZARZĄDZANIE, RACHUNKOWOŚĆ, Rachunkowość(3)

Balanced Scorecard, Balanced Scorecard - Strategiczna Karta Wyników

BALANCED SCORECARD PROJEKTU pusty dla studentów

Create a Balanced Scorecard (SharePoint Server 2010)

Balanced Scorecard

IR Lecture1

uml LECTURE

lecture3 complexity introduction

196 Capital structure Intro lecture 1id 18514 ppt

Lecture VIII Morphology

benzen lecture

lecture 1

więcej podobnych podstron